Domestic TCE Therapies Attract Over $3 Billion in Global Investments as MNCs Rush to Secure Pipeline Assets

AbbVie

Innovative Drug Developer

EvolveImmune Therapeutics

Cancer Treatment Drug Developer

GSK

Pharmaceutical R&D Manufacturer

MSD

Pharmaceutical R&D and Manufacturer

Curon BioPharma

Developer of Oncology Immunotherapy Drugs

As BD transactions between MNCs and domestic Biotech companies continue to emerge, TCE therapy has surfaced, becoming a key focus and heavily invested track in the pharmaceutical industry.

On October 31, AbbVie Invests $1.465 Billion in TCE, Partners with EvolveImmune Therapeutics to Co-Develop Oncology Drugs Using Its Proprietary TCE Platform.

On October 29, GSK announced that it had reached an agreement with Chimagen Biosciences to acquire CMG1A46, a dual T-cell engager (TCE) targeting CD19 and CD20, which is currently in the clinical stage, for a prepayment of $300 million. Chimagen Biosciences will be eligible to receive up to $550 million in development and commercial milestone payments for CMG1A46.

On August 9, MSD acquired CN201, a next-generation CD19×CD3 bispecific antibody and TCE drug in development for B-cell depletion therapy by Tongrun Bio-pharmaceutical (Shanghai) Co., Ltd., for $1.3 billion. The upfront payment was an astonishing $700 million, with Tongrun Bio-pharmaceutical also eligible to receive up to $600 million in milestone payments.

Looking back at the overseas BD transactions of pharmaceutical companies in China in 2024, the pipelines of several Biotech companies going abroad are directly targeting TCE therapy. Apart from Chimagen Biosciences and Tongrun Bio-pharmaceutical (Shanghai) Co., Ltd., Genor Biopharma, EpimAb Biotherapeutics, ConMab, and WuXi Biologics have also achieved BD licensing for TCE therapy, with the total transaction amount reaching up to 3 billion US dollars.

Phenomenal events continue to emerge. Candid Therapeutic, an overseas innovative pharmaceutical company, announced in mid-September 2024 the completion of a $370 million financing round, setting a record for the highest fundraising amount in the biopharmaceutical industry in 2024. Both of its core products were acquired from a newly established overseas NewCo company originating from a Chinese pharmaceutical enterprise, and both are currently popular TCE bispecific antibody varieties targeting autoimmune diseases.

In addition to BD transactions, Amgen's TCE bispecific antibody drug Imdelltra was approved by the FDA for marketing in May this year, becoming the world's first TCE therapy for the treatment of solid tumors.

From hematological tumors to solid tumors, and further expanding to autoimmune diseases, TCE therapy may become the next golden apple contested by numerous players in the pharmaceutical industry.

Where Does TCE Bispecific Antibody Excel?

TCE (T cell Engager), a type of T cell engager drug, achieves cancer treatment by leveraging the killing effect of T cells on tumor cells and has already shown significant success in the field of hematological malignancies.

In the treatment of hematological tumors, TCE has achieved significant therapeutic effects by binding CD3 with different B-cell targets (such as CD19, CD20, and BCMA). One end of the TCE bispecific antibody binds to T cells through CD3, while the other end (or both ends) binds to TAA (tumor-associated antigens), helping T cells locate and activate their cytotoxic capabilities to achieve the purpose of killing tumor cells.

TCE and CAR-T both rely on T cells to achieve therapeutic effects, and their expansion path—from hematologic malignancies to solid tumors and then to autoimmune diseases—is similar to that of CAR-T. Based on the similarity in mechanisms of action between TCE and CAR-T, the industry often compares the two therapies to see which can gain a competitive edge in the market. So, compared with CAR-T, where does the differentiation of TCE lie?

Firstly, in the field of hematological tumors, there are currently multiple products on the market for both TCE and CAR-T. CAR-T demonstrates superior efficacy, but all the marketed CAR-T products are autologous, which are costly, have long production cycles, and are expensive. In contrast, TCE drugs, as "off-the-shelf" therapies, are easier to promote and use.

In the field of solid tumors, with Amgen's Tarlatamab (CD3/DLL3) receiving FDA approval in May this year for the treatment of small cell lung cancer, TCE therapy for solid tumors has achieved initial breakthroughs. Although certain efficacy has been observed clinically with GPC3 CAR-T and Claudin 18.2 CAR-T, there is still a considerable distance from regulatory approval. Therefore, it is expected that TCE will lead CAR-T in solid tumor treatment for some time.

In the field of autoimmune diseases, CAR-T may cause cytokine release syndrome (CRS) in terms of safety, while TCE drugs can better control risks by dose adjustment. For example, Teclistamab has demonstrated good safety during treatment through dose escalation, with no neurotoxicity or bone marrow suppression, and only low-grade CRS.

In addition, as chronic diseases, patients with autoimmune diseases have higher requirements for long-term efficacy, safety, and cost-effectiveness of treatment compared to cancer. The CAR-T manufacturing process is complex, and the treatment process also includes multiple steps such as apheresis and lymphodepletion, after which patients need to be hospitalized for observation. On the other hand, TCE can be administered subcutaneously, offering significant advantages in terms of administration and patient compliance.

According to industry insiders, the mechanism of TCE is very similar to that of ADC, both having three domains: one domain binds to a component of the T-cell receptor, another domain binds to tumor-associated antigens, and the third domain provides additional functions, such as extending half-life. Mechanistically, compared with conventional IgG, TCEs are considered more effective than Fc-mediated ADCs. Moreover, since the process of killing tumor cells is carried out by the body's own T cells, their toxicity is lower than that of ADCs.

Thanks to numerous advantages, TCE bispecific antibodies, particularly CD3+ T cell redirecting bispecific antibodies, have become a research hotspot in the bispecific antibody field in recent years and are also regarded as potential drugs that could succeed ADCs.

Significant Progress in Hematological Tumor Treatment, New Breakthroughs in Solid Tumor Research

Generally speaking, the industry divides the development of TCE bispecific antibodies into three stages, corresponding to the three treatment areas of hematological tumors, solid tumors, and autoimmune diseases.

In the field of hematological tumors, TCE bispecific antibodies continue to make progress. According to Mordor Intelligence data, the global hematological tumor market size is expected to reach approximately USD 67 billion in 2024 and about USD 98 billion in 2029, with a compound annual growth rate (CAGR) of 7.8%.

Currently, there are 10 TCE bispecific antibodies approved globally, with 7 for hematological tumors, mainly from Amgen, Roche, and AbbVie, covering targets such as BCMA, GPRC5D, CD20, and CD19. These have been approved for multiple hematological tumor indications including multiple myeloma and diffuse large B-cell lymphoma. Among these, two products have been approved in China: Blinatumomab from Amgen/BeiGene and Glofitamab from Roche.

10 TCE Drugs Already on the Market

10 TCE Drugs Already on the Market

In addition, Johnson & Johnson received approvals for its TCE bispecific antibody drugs in 2022 and 2023. With subsequent combination therapies and full coverage from late-line to front-line patients, the expected sales of Johnson & Johnson's two TCE bispecific antibody drugs, Talquetamab and Teclistamab, are both close to $5 billion.

It is worth mentioning that the cost-effectiveness of TCE bispecific antibodies provides a new treatment option for end-stage multiple myeloma (MM) patients. The global population of multiple myeloma patients is approximately 450,000. Currently used drugs include proteasome inhibitors, immunomodulatory agents, and anti-CD38 antibodies, among others. However, recurrence and drug resistance have always been difficult issues to resolve, resulting in limited benefits for end-stage MM patients.

The emergence of cell therapy and TCE bispecific antibodies has demonstrated high response rates in R/R MM patients. The updated NCCN guidelines recommend CAR-T and TCE bispecific antibodies as preferred therapies for patients who have received ≥4 lines of treatment.

Compared with CD38 monoclonal antibodies, Teclistamab and Elranatamab monotherapy for RRMM in end-stage MM patients demonstrated higher objective response rates (ORR: 61-63% vs 31%) and potentially doubled survival benefits (mPFS: 11.3 vs 3.7, mOS: 18.3 vs 9.3). Although the efficacy of BCMA/CD3 bispecific antibodies is slightly inferior to CAR-T therapy (ORR: 98% vs 61-63%), they offer better safety (CRS: 95% vs 58%-72%) and lower treatment costs. The excellent accessibility of TCE provides these patients with another option.

In the field of solid tumors, TCE bispecific antibodies (TCE bispecifics) have seen slower progress in solid tumors compared to hematological malignancies, primarily due to several key factors. On one hand, early targets developed for solid tumors, such as HER2, EGFR, TROP2, and MUC1, are also expressed in normal tissues. Given the high activity of TCE bispecifics, this can lead to T cells "accidentally harming" normal tissues while attacking the target. Increasing the dose further compromises safety, necessitating a balance between efficacy and safety.

On the other hand, the immunosuppressive nature of the tumor microenvironment is a significant factor that restricts the activity and efficacy of T cells. Moreover, the limited infiltration levels of T cells also constrain the therapeutic effectiveness of TCE bispecific antibodies in solid tumors.

As understanding of these challenges deepens and new strategies are developed, the potential of TCE bispecific antibodies in solid tumor treatment is gradually being unlocked and realized. For instance, the design of a new generation of TCE bispecific antibody drugs for solid tumors is progressively broadening in approach. First, in terms of target selection, there is a preference for targets with stronger tumor-specific expression, such as DLL3 and PSMA. At the same time, the potency and affinity of the antigen recognition arms are optimized to enhance selectivity for tumor tissues. Finally, combination therapies are employed to overcome immunosuppression.

In May this year, Amgen's Tarlatamab was granted accelerated approval by the FDA for the treatment of third-line small cell lung cancer, becoming the first TCE drug to treat solid tumors and paving the way for TCE to shine in the field of solid tumors. In addition, TCE bispecific antibodies targeting PSMA, STEAP-1, and other targets are continuously releasing early promising data for prostate cancer. In the future, the explosion of TCE drugs in the field of solid tumors is yet to be seen.

Over 20 autoimmune products in development, poised to open up the next billion-dollar market

Regarding the recent surge in acquisitions of TCE bispecific antibody assets within the industry, some professionals have noted that this is partly due to multinational corporations (MNCs) recognizing the potential of TCE in autoimmune diseases such as systemic lupus erythematosus, ankylosing spondylitis, and psoriasis. Treatments for these autoimmune conditions are expected to become highly sought-after targets among pharmaceutical companies in the future.

As is well known, B cells play a key role in various autoimmune diseases, and the deep depletion of B cells can treat multiple autoimmune conditions. TCE bispecific antibodies, which inherently target immune cells, can naturally be developed into products for autoimmune regulation. Some also believe that this field may eventually become independent from oncology, emerging as the next mega-track with a potential market worth hundreds of billions.

In fact, while deeply exploring the oncology field, some pharmaceutical companies have indeed set their sights on the autoimmune market.

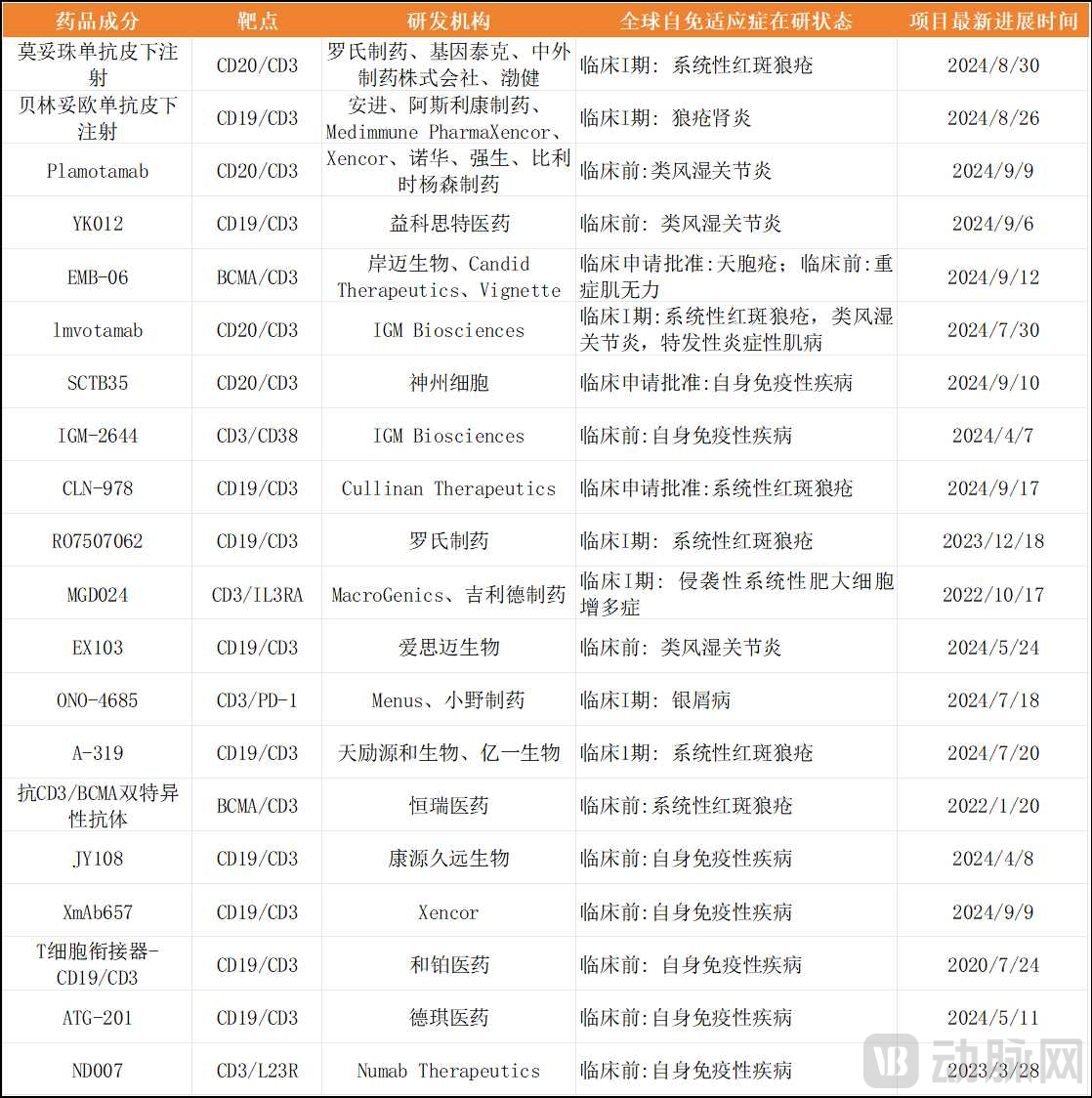

Currently, there are more than 20 TCE drugs globally in active status that have initiated clinical research related to autoimmune diseases, with target combinations mainly focusing on CD3×CD19, CD3×CD20, CD3×BCMA, etc.

TCE bispecific antibodies for autoimmune diseases under research globally

Among overseas MNCs, Roche's CD20/CD3 bispecific antibody and Amgen's BCMA/CD3 bispecific antibody have successively initiated clinical trials for TCE bispecific antibodies in autoimmune indications. This also signifies that TCE bispecific antibodies could potentially tap into the vast market space of autoimmune diseases.

Previously, MSD spent $1.3 billion to acquire Tongrun Bio-pharmaceutical (Shanghai) Co., Ltd.'s CD3xCD19 bispecific antibody CN201, due to the potential of CN201 to break through in the autoimmune field. It is under this logic that more multinational corporations (MNCs) are targeting Chinese-produced molecules, hoping to tap into the potential of TCE multi-specific antibodies in the autoimmune market.

In China, in the field of TCE autoimmune applications and bispecific antibodies targeting CD3/BCMA, aside from EpimAb Biotherapeutics and Keymed Biosciences, which have reached deals, Zhi Xiang Jin Tai, CT&T, New Times Pharma, and Yikang Biotech also have similar products entering the clinical research stage.

In the bispecific antibodies targeting CD3/CD19, besides Tongrun Bio-pharmaceutical (Shanghai) Co., Ltd., similar products from Yikexinte, Yiyi Bio, Luzhu Bio, and New Era Pharmaceutical have also entered the clinical research stage.

In the bispecific antibodies targeting CD3/CD20, similar products from Exemab, Conxima, Yiteng Jiahe, Tian Guangshi, CTTQ, Junshi Biosciences, and Sino Biological have also entered the clinical research stage.

In addition, Innovent Biologics' CD3/CLDN18.2 bispecific antibody has entered Phase II clinical trials, with its R&D progress ranking among the global leaders.

China-produced TCE takes a unique R&D path, showing promise in multiple indications

As the TCE platform gradually matures, domestic companies in China have also begun to lay out their TCE platforms. We have also observed that, compared to the overseas R&D route which mainly progresses from hematological tumors to solid tumors and then to autoimmune diseases, the R&D layout of TCE drugs in China is somewhat different. Many companies have even bypassed the oncology field and directly started research in the autoimmune area.

By contrast, the initial development of TCE abroad mainly focused on hematological tumors, such as multiple myeloma and diffuse large B-cell lymphoma, showing significant efficacy in the treatment of certain hematological tumors, with a relatively mature market. Although China is also actively promoting the research and development of TCE drugs, due to the relatively small market and most being in the early clinical stage, market progress has been relatively slow.

In China, the initial focus was more on the solid tumor field. However, due to the complexity and safety challenges of solid tumors, there is a gradual strengthening in the research of TCE drugs in the autoimmune field.

In terms of safety, one of the challenges in designing TCE drugs is how to balance efficacy and safety, especially in controlling cytokine storms. Foreign companies have conducted more in-depth technical research in this area. Chinese companies are actively exploring designs that reduce CD3 affinity to improve the safety of TCE drugs during development.

Overall, there are different focuses and challenges in the R&D of TCE at home and abroad. However, with the continuous advancement of technology and the accumulation of clinical data, TCE drugs are expected to play an important role in more cancer treatments.

In China, Zelgen Biopharmaceuticals has made significant progress in the field of solid tumors. Its first triple antibody targeting DLL3 is the most advanced globally, showing great potential. As a domestic counterpart to Amgen's Tarlatamab (DLL3/CD3) in the small cell lung cancer sector, it demonstrates higher activity and an enhanced ability to bind to low and medium expression sites compared to Amgen's product.

ZhiXiang JinTai has a layout in hematological tumors, and the clinical data of its core product GR1803 shows a 100% ORR for patients with extramedullary lesions, with excellent results.

In addition, Innovent Biologics has a layout in both solid tumors and hematological malignancies; Tongrun Bio-pharmaceutical (Shanghai) Co., Ltd.'s CN201 and other companies are expected to establish a presence in autoimmune indications; EpimAb Biotherapeutics has a CD3/ROR1 bispecific antibody; YZY Biopharma’s CD3/EpCAM-targeting bispecific antibody is advancing rapidly and has entered Phase III clinical trials, among others.

In the future, as research on TCE in China matures, we are optimistic about subsequent breakthroughs of various types of TCE drugs across multiple indications.

BD, Financing, M&A, NewCo... TCE Blooming in Multiple Areas

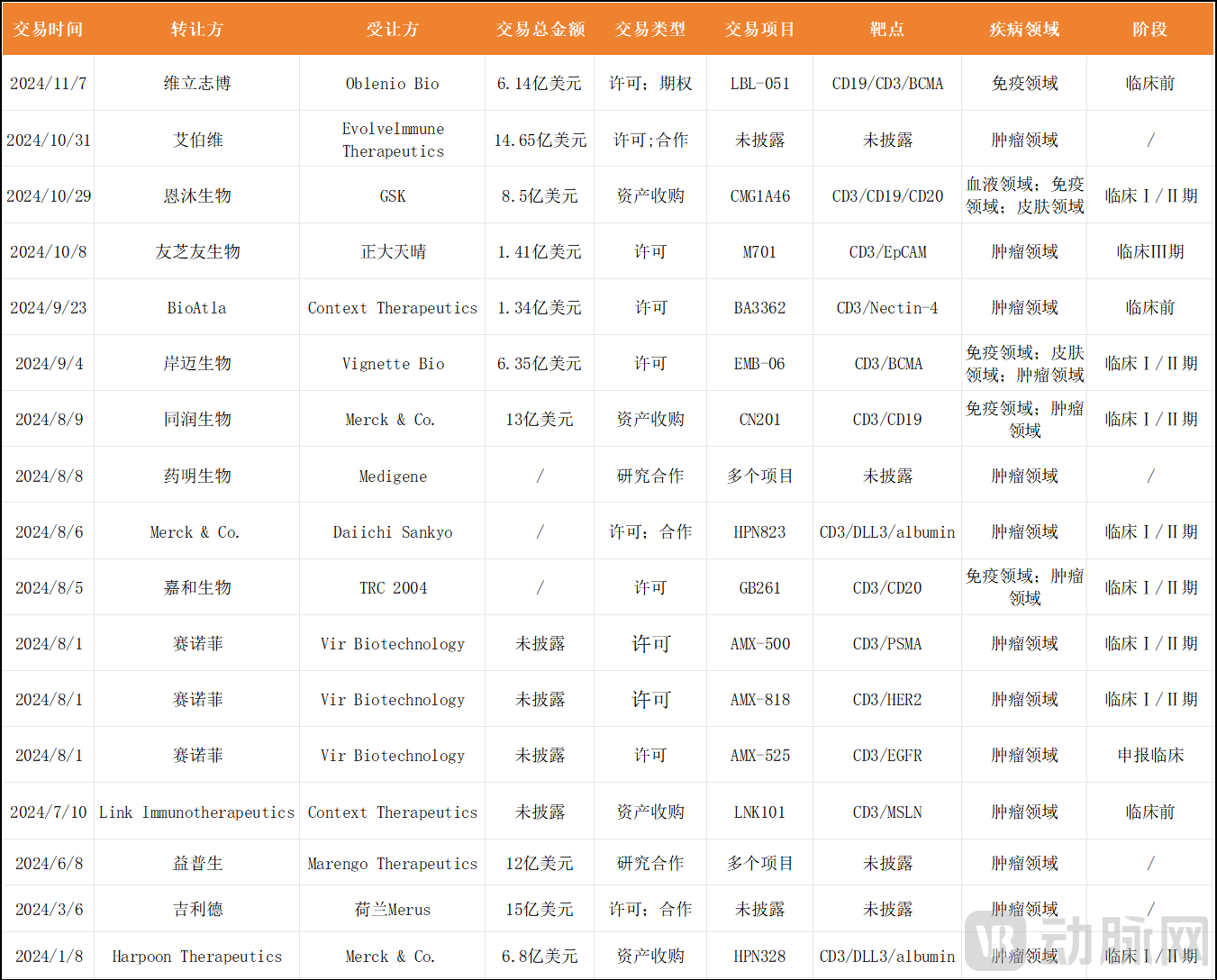

In 2024, the TCE bispecific antibody field has undoubtedly become the focus of the market, with blockbuster deals, large-scale financing, mergers and acquisitions, or the NewCo model… TCE has demonstrated extraordinary vitality and popularity, appearing extremely hot from every perspective.

TCE Trading Situation in 2024 (Incomplete Statistics)

TCE Trading Situation in 2024 (Incomplete Statistics)

In terms of transactions, according to incomplete statistics from VCBeat, nearly 20 deals occurred in 2024, with a total value exceeding 8.5 billion US dollars. Among these transactions, the two deals involving the highest amounts for projects in China were the CD3/CD19 bispecific TCE deal between Tongrun Bio-pharmaceutical (Shanghai) Co., Ltd. and MSD (1.3 billion US dollars), and the CD3/CD19/CD20 trispecific TCE deal between Chimagen Biosciences and GSK (850 million US dollars).

In the TCE field, NewCo's capital operation model is gaining increasing popularity. For instance, in September this year, EpimAb Biotherapeutics' BCMA×CD3 bispecific antibody EMB-06 went overseas through the NewCo model, with a significant portion of the $60 million upfront payment being made in the form of equity. It is understood that the transferee in this deal, Vignette Bio, was incubated by Foresite Capital, with Qiming Venture Partners also participating in its financing. In September this year, prior to this BD deal, the company was acquired by Candid Therapeutics.

Notably, in terms of financing, also in September this year, following this transaction, Candid Therapeutics secured a $370 million Series A financing round for the treatment of autoimmune diseases, setting a record for the largest single-round financing in the European and American life sciences sector this year.

In terms of acquisitions, in January this year, MSD announced the acquisition of Harpoon for $23 per share, totaling $680 million. Through this acquisition, MSD not only gained a promising DLL3/CD3 antibody currently in clinical trials but also acquired Harpoon's multiple tri-specific antibody platforms, including the next-generation multi-specific antibody platform — ProTriTAC and TriTAC-XR tri-specific antibody platforms that are specifically activated in the tumor microenvironment, thereby quickly entering the TCE track.

Whether viewed from BD, financing, M&A, or the NewCo model, the TCE track shows a situation of blooming in multiple areas, indicating the vigorous development and future potential of this field.

Of course, for a drug, its clinical competitiveness is the most critical aspect. In this regard, TCE has infinite potential and room for imagination, whether in hematological tumors, solid tumors, or autoimmune diseases.

In the field of multiple myeloma, several TCE bispecific antibodies are undergoing head-to-head phase I and phase II clinical trials worldwide against standard therapies, with the hope of becoming the next-generation cornerstone drug for multiple myeloma in the future. In the DLBCL field, CD20/CD3 bispecific antibodies aim to make the leap from third-line to second-line and first-line treatments. If their benefits can be clinically proven, TCE bispecific antibodies will inevitably compete with CAR-T, ADCs, and others.

Currently, compared with CAR-T, TCE bispecific antibodies, although weaker in efficacy, demonstrate better performance in terms of safety and convenience. In the face of the popular ADC, TCE bispecific antibodies also show significant differentiation—on one hand, they require lower target expression levels but demand higher tumor specificity, potentially allowing them to form a competitive niche.

It is foreseeable that TCE bispecific antibodies will continue to lead the industry trend in the future, giving rise to more landmark blockbuster deals. This not only brings opportunities for pharmaceutical companies to make a comeback but also is expected to spark a revolution of innovation and disruption in product development and market layout.

References:

TCE Bispecific Antibody: The Next Breakthrough in Antibody Drugs — Hematologic Tumors + Solid Tumors + Autoimmunity — Chen Xiaofei's Log

Behind the Surge of Dual Antibody License Outs: Two Trends and Rising Stars —— PharmaCube Info

TCE vs CAR-T: Market Response - VCBeat

TCE Bispecific Antibodies Are Gaining Even More Momentum — Amino Observation