Oral Peptides Gain Momentum: AbbVie, J&J, MSD, and Novo Nordisk Race to Enter the Market

Johnson & Johnson

Medical Device R&D and Manufacturer

In the autoimmune therapy market, the oral peptide market is beginning to emerge.

Recently, AbbVie announced a definitive acquisition agreement with Nimble Therapeutics. Through this acquisition, AbbVie will obtain Nimble's core assets, including its leading program—a preclinical oral peptide IL-23 inhibitor for the treatment of psoriasis—and a pipeline of innovative oral peptide candidates targeting various autoimmune diseases. Additionally, AbbVie will acquire Nimble’s peptide synthesis, screening, and optimization platform, which utilizes proprietary technology to accelerate the discovery and optimization of peptide candidates against multiple targets.

AbbVie's Layout in the Immunology Field Has a Long History. As Humira’s Patent Expires, AbbVie Is Actively Seeking New Growth Points. This Acquisition of Nimble Therapeutics Not Only Enriches AbbVie’s Product Pipeline But Also Strengthens Its R&D Capabilities in the Oral Peptide Therapy Field.

In the field of oral psoriasis treatment, Johnson & Johnson's JNJ-2113 has demonstrated Best in class potential, outpacing other competitors. Just last month, Johnson & Johnson announced the topline results of the ICONIC-LEAD clinical study, marking the imminent market entry of Icotrokinra, the world’s first targeted oral peptide that selectively blocks the IL-23 receptor. In response to this advancement by Johnson & Johnson, AbbVie is sparing no effort to ensure it maintains its leading position in this competitive landscape. With the former blockbuster Humira having fallen off the patent cliff, can AbbVie rebuild its status as the "king of immunology"?

AbbVie and Johnson & Johnson

The Dual Powerhouses in the Field of Psoriasis Treatment

According to statistics, the number of psoriasis patients worldwide has exceeded 125 million. This chronic disease, characterized by its slow progression and long-term course, requires patients to undergo long-term treatment, thereby giving rise to a vast treatment market.

Psoriasis is a representative target indication in the field of autoimmune diseases. Globally, the market size for therapeutic drugs targeting this condition is rapidly expanding. According to GlobalMarket data, the global psoriasis market has reached $26.5 billion, and it is projected that the global autoimmune treatment drug market will maintain a compound annual growth rate of 8.6% from 2022 to 2030.

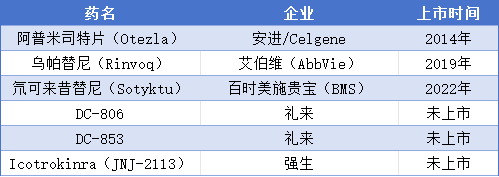

For the treatment of plaque psoriasis, 22 targeted therapies have been approved globally. Among these treatments, AbbVie and Johnson & Johnson are undoubtedly the market leaders. AbbVie has secured a significant position in the market with its three main products: Humira (TNFα inhibitor), Risankizumab (IL-23 inhibitor), and Upadacitinib (JAK inhibitor). Meanwhile, Johnson & Johnson also demonstrates outstanding performance in the psoriasis treatment market with its four products: Infliximab and Golimumab (both TNFα inhibitors), Ustekinumab (IL-12/IL-23 inhibitor), and Guselkumab (IL-23 inhibitor).

For patients requiring long-term treatment, oral medications have become a more popular choice due to their convenience. Currently, oral drugs include the PDE4 inhibitor apremilast, the TYK2 allosteric inhibitor deucravacitinib, and the JAK inhibitor upadacitinib. In addition, numerous multinational corporations (MNCs) are also actively expanding into the field of oral treatments for psoriasis.

Psoriasis Oral Medications

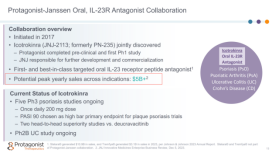

In terms of efficacy, oral formulations do not have an advantage. However, Johnson & Johnson's JNJ-2113 (Icotrokinra), as the world's first oral IL-23 receptor antagonist, relies on Protagonist Therapeutics' proprietary peptide technology platform, successfully overcoming development challenges such as low oral bioavailability of peptides, permeability and stability issues, and gastrointestinal degradation. In the phase III ICONIC-LEAD study, it demonstrated superior data compared to other competing oral drugs.

Driven by robust efficacy data, Johnson & Johnson has high confidence in the drug JNJ-2113 and projects its market potential to reach $5 billion.

As Johnson & Johnson makes breakthrough progress in the field of oral medications for psoriasis, AbbVie is also actively expanding its product line to maintain its leading position in the treatment of autoimmune diseases.

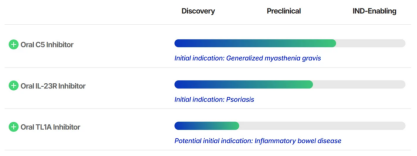

AbbVie Sets Its Sights on Nimble Therapeutics, a Biotech Company Focused on Developing Oral Peptide Therapies. Among Nimble's research achievements, the IL-23R inhibitor stands out in particular. This is a preclinical-stage oral therapy under investigation, designed to offer new treatment options for patients with psoriasis and inflammatory bowel disease (IBD). Notably, this target is the same as AbbVie’s existing blockbuster injectable drug, risankizumab, indicating that Nimble's research aligns synergistically with AbbVie's current product portfolio.

Nimble claims that its designed drug not only inherits the potent activity of injectable IL-23 drugs but also has an extended "half-life." In addition, Nimble disclosed two other candidate drugs for generalized myasthenia gravis and IBD, which are also in the preclinical testing stage.

Nimble R&D Pipeline

Through this acquisition, AbbVie will not only bring Nimble's product line under its wing but also gain access to the advanced technologies of this Madison, Wisconsin-based company in synthesizing, screening, and optimizing peptide drug candidates. This will provide AbbVie with strong technical support in the field of oral peptide therapies, accelerating its R&D progress in this emerging area.

In fact, AbbVie's acquisition of Nimble is its third major acquisition this year in the field of immunotherapy developers. This series of consecutive acquisitions not only highlights AbbVie's active layout in the immunotherapy sector but also reveals the company's sense of urgency to maintain its leading market position, especially against the backdrop of competitors like Johnson & Johnson making progress in the field of oral psoriasis drugs.

From the Needle Tip to the Tongue Tip

"Oral Peptide" Drugs Are Gaining Momentum

The polypeptide industry is currently in an unprecedented golden age of development.Compared with small-molecule chemical drugs, peptide drugs exhibit higher bioactivity and specificity;Compared with biologics, they stand out with advantages such as low immunogenicity, high purity, and lower production costs.Overall, peptide drugs are highly favored for their high activity, low dosage, and low toxicity.

Frost & Sullivan's forecast shows that the global peptide drug market size has grown from USD 60.7 billion in 2018 to USD 89.5 billion in 2023, and is expected to reach USD 189 billion by 2028.

When the efficacy generally reaches a certain level, oral medications often become the choice for patient treatment due to their advantages in medication adherence. However, due to the unique chemical and biological properties of peptide drugs, their oral delivery has remained one of the significant challenges in the pharmaceutical field.

Since the discovery of insulin, research on oral peptides has never ceased.

Due to the poor permeability of polypeptide drugs and their susceptibility to degradation by proteases in the gastrointestinal tract, most polypeptide drugs on the market are in injectable form. However, long-term repeated injections not only affect patients' quality of life but also increase the complexity of manufacturing and storage, ultimately leading to higher healthcare costs. Therefore, although the development of oral polypeptide drugs has always been a research hotspot in the pharmaceutical field, the successful transformation of such products is rare due to the numerous difficulties faced in the absorption of oral polypeptide drugs.

With the in-depth research on the oral absorption mechanism of peptides, innovative technologies developed by scientists are gradually breaking down the barriers to peptide absorption in the gastrointestinal tract, and some oral peptide drugs have successfully entered the market.

For example, semaglutide (Semaglutide), a GLP-1 peptide drug that has received much attention in recent years, is traditionally administered via subcutaneous injection. With the innovative technology of the "SNAC absorption enhancer," the semaglutide tablet (Rybelsus) successfully overcame technical barriers, achieving a historic breakthrough in administering GLP-1 drugs orally and becoming the first truly oral peptide drug.

The active pharmaceutical ingredient (API) of Rybelsus is identical to that of the injectable version, also featuring a fatty acid chain modification, with an additional 300mg of SNAC molecules. The addition of SNAC can transiently increase the stomach's pH and, at specific concentrations, promote transcellular absorption in the gastric mucosa. In the human NCI-N87 gastric epithelial cell model, the addition of SNAC increased the absorption capacity of gastric epithelial cells by 100 times.

After entering the market, Rybelsus has also shown remarkable performance. The demand for these products is so high that there is a shortage of supply. In the first half of 2024, the sales of Rybelsus reached 1.587 billion US dollars, increasing by 32% year-on-year.

Equally noteworthy is the Israeli pharmaceutical company Chiasma Inc., which successfully developed the oral capsule Mycapssa through an innovative formulation and launched it in the U.S. in 2020 via the 505(b)(2) regulatory pathway. Mycapssa is the first and only approved oral somatostatin analog capsule for the treatment of acromegaly, offering patients a new therapeutic option. The Transient Permeability Enhancer (TPE™) technology adopted by Chiasma provides critical technical support for the development of oral peptide drugs.

MSD Also Focuses on the Oral Peptide Trend. In January 2024, MSD signed a $220 million collaboration agreement with Unnatural Products. Through this partnership, MSD began leveraging Unnatural Products' technology to develop macrocyclic peptide drug candidates, primarily targeting the challenging field of oncology. MSD has likened macrocyclic peptides to "Goldilocks" because their molecular size falls between small molecules and biologics, offering many unique advantages.

Previously, Merck had launched the Phase III clinical program for MK-0616, a macrocyclic peptide that binds to PCSK9. Currently, PCSK9-targeted therapies can only be administered via injection, and the cost-effectiveness issue of using biologics to lower cholesterol has yet to be effectively resolved. The development of an oral PCSK9 inhibitor has been a goal in this field, and the research and development of MK-0616 macrocyclic peptide is expected to achieve a significant breakthrough.

According to the research report by MARKET MONITOR GLOBAL, INC (MMG), the global market size for oral peptide therapeutic drugs was approximately USD 1,886.4 million in 2023. It is projected to have a compound annual growth rate (CAGR) of 15.8% over the next six years, reaching USD 7,843.2 million by 2030.

Industry perspectives generally believe that the treatment market for autoimmune diseases is experiencing rapid growth. With continuous breakthroughs in oral peptide therapy technology and the rapid expansion of the market, AbbVie has consolidated its R&D position in the oral peptide field by acquiring Nimble Therapeutics. Whether AbbVie can reclaim the title of "King of Immunology" and continue to lead innovation in the field of autoimmune disease treatment remains to be seen. The Pharmaceutical Economy Newspaper will keep a close watch on future developments.

Editor: Wanwan

www.yyjjb.com.cn

Insight into Industry Trends

"Pharmaceutical Economy Herald"

Academic Official Account

Focusing on the Frontiers of Oncology Academia

Terminal Official Account