MNC M&A Strategy Shifts Create New Opportunities for Chinese Biotech Firms

Pfizer

Pharmaceutical R&D Developer

Seagen

Monoclonal Antibody Developer

Novartis

Drug Development and Manufacturing

MorphoSys

Biopharmaceutical Manufacturer

Johnson & Johnson

Healthcare Product Manufacturers, Health Service Providers

AstraZeneca

Biopharmaceutical Manufacturer

MSD

Pharmaceutical R&D and Manufacturer

Harpoon Therapeutics

Developer of Immuno-Oncology Therapeutics

Genmab

Differentiated Antibody Therapy Developer

Compared to 2023, the number of mega M&A deals by MNCs in 2024 has significantly decreased.

According to incomplete statistics, the total amount of M&A transactions in the pharmaceutical industry in 2023 was approximately 150 billion US dollars, including nine deals exceeding 5 billion US dollars, and the threshold for entering the TOP10 list was 4.1 billion US dollars.

The number of M&A transactions in the pharmaceutical sector increased in 2024 compared to 2023, but from a value perspective, there were not many mega-deals. Excluding Novo Nordisk's $16.5 billion acquisition of CDMO company Catalent, the remaining deals were all under $5 billion.

Major M&A Events in the Pharmaceutical Industry in 2024 (As of Early December), Compiled and Organized Based on Public Information

On the one hand, the U.S. Federal Trade Commission (FTC) has tightened transaction supervision that was relaxed during the pandemic and increased the filing fee for deals over $5 billion from $800,000 to $2.25 million this year. On the other hand, an increasing number of Biotech companies are opting to bring their drugs to market independently, which has also reduced the number of late-stage assets available for MNCs, naturally keeping deal prices low.

Moreover, the absence of heavyweight player Pfizer has made the M&A market in 2024 appear lackluster.

Perhaps because Pfizer's $43 billion acquisition of Seagen in 2023 consumed much of its "ammunition," it appeared unusually low-key in 2024. In contrast, Novo Nordisk and Eli Lilly, which have capitalized on the GLP-1 boom over the past two years, are now in a strong position for mergers and acquisitions.

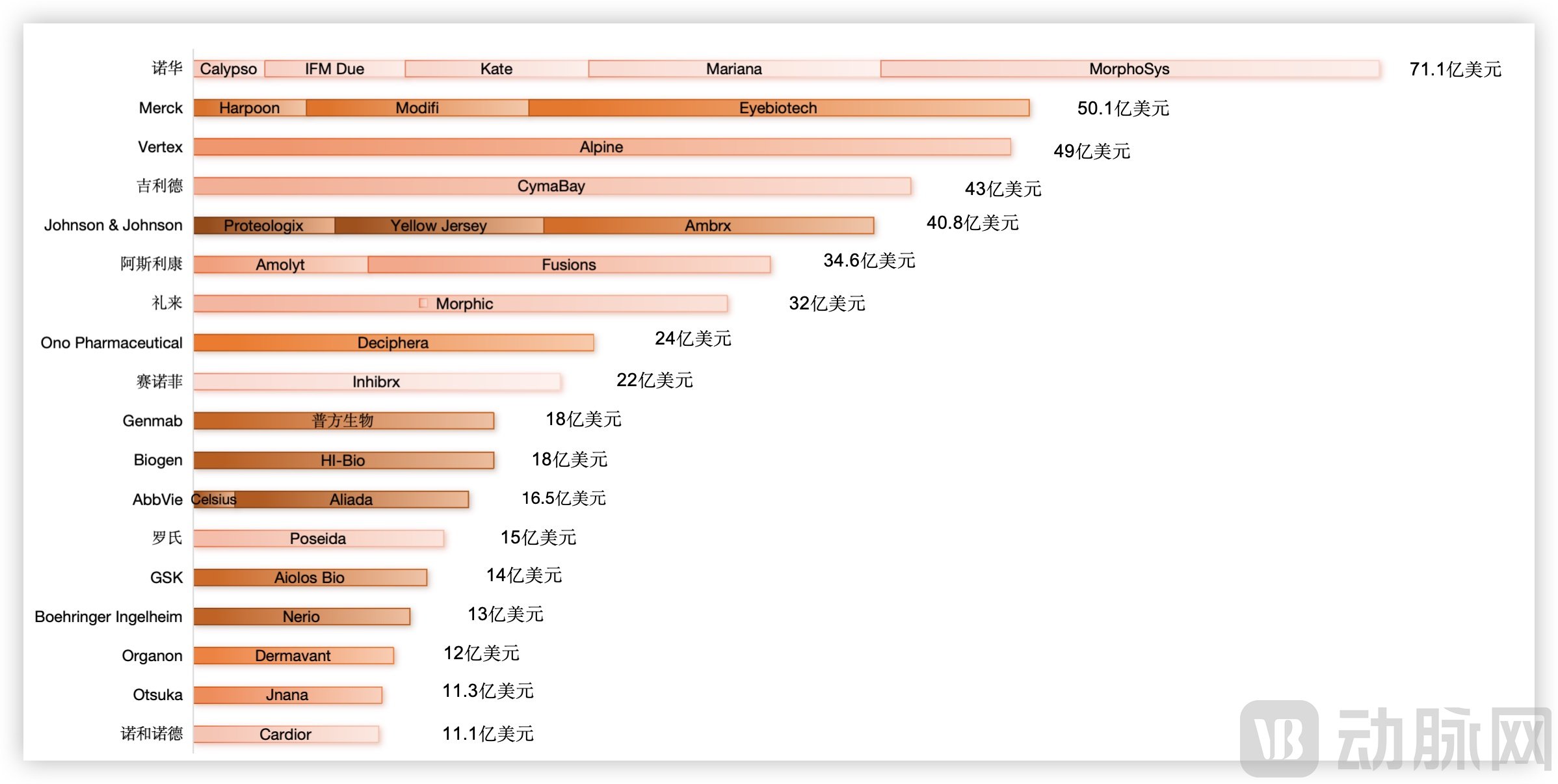

Despite Vertex's $49 billion acquisition of Alpine being the largest single biotech deal in 2024, Novartis completed five transactions totaling over $70 billion, and other multinational corporations (MNCs) also made moves to strengthen their positions based on their strategic development. However, the presence of Chinese biotech companies was minimal. From the mergers and acquisitions in 2024, we may be able to glimpse the industry’s development trends in the coming years and understand what types of biotech companies MNCs prefer to acquire.

Although the oncology field has slowed down, it remains the most important competitive track for MNCs.

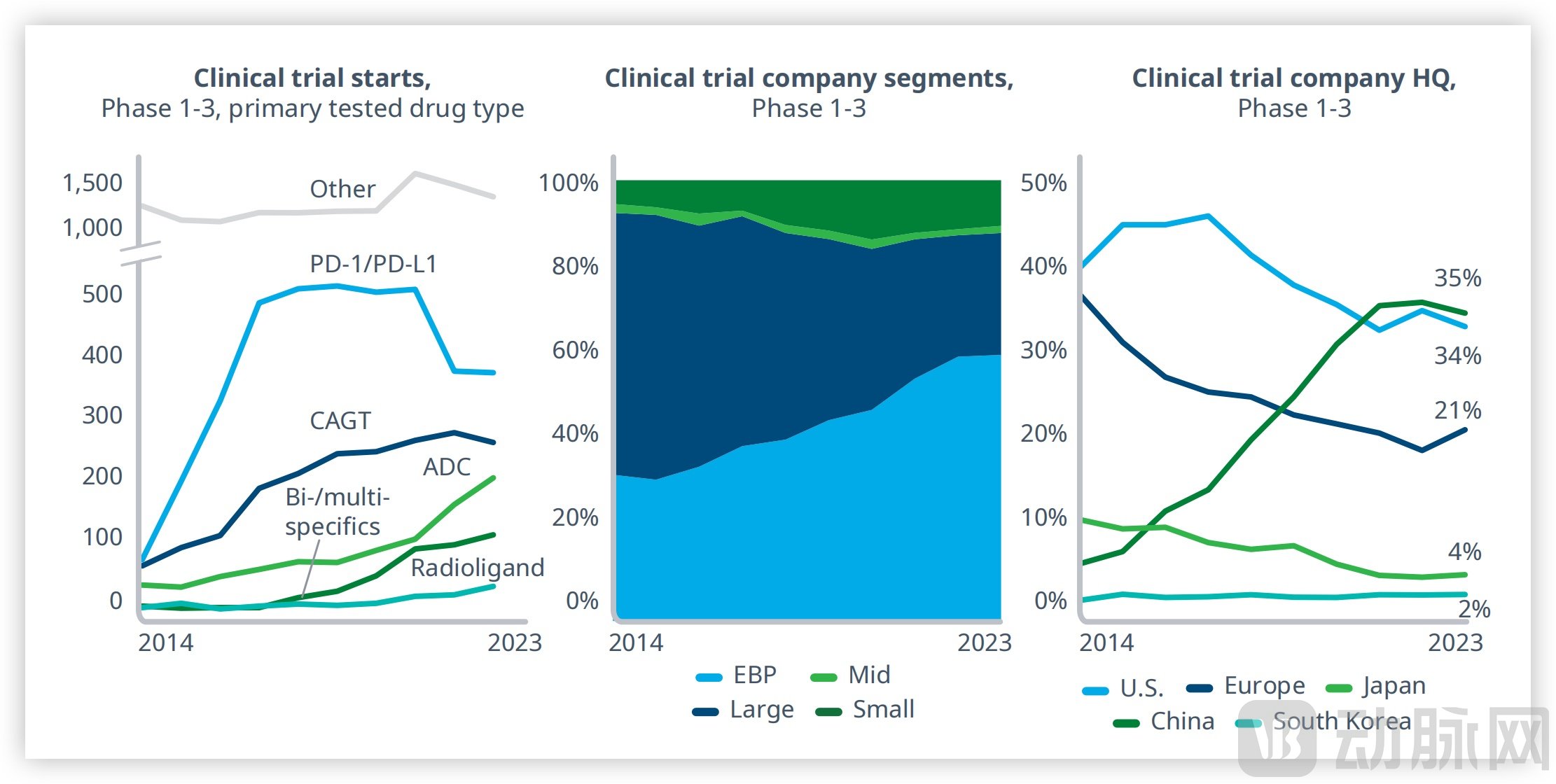

Clinical trials do not lie.

Cancer Clinical Trials in the Past Decade, Source: IQVIA

The oncology track remains a hotbed for innovative drugs, with various new therapies continuing to emerge. It can be observed that as the frenzy surrounding PD-1/PD-L1 in previous years has led to a recent decline in related clinical trials, new therapies are rapidly taking the spotlight. These include a sharp increase in clinical trial activities for CGT, ADC, bispecific and multispecific antibodies, as well as radioligand therapies.

In this process, emerging biopharmaceutical companies have become the backbone of conducting oncology clinical trials, with their share increasing from 33% to 60% over a decade, while the proportion of MNCs has dropped from 59% to 28%. Naturally, some MNCs with less comprehensive layouts are unwilling to fall behind and are strengthening their positions through acquisitions.

Taking Johnson & Johnson as an example, with the validation of ADC drugs, the company has started to make significant efforts in recent years. From previous technology platform collaborations with Mersana and DuoXi Bio, to BD transactions with LegoChem, and up to this nearly $2 billion full acquisition of Ambrx, all these moves demonstrate Johnson & Johnson's emphasis on ADC.

Although Ambrx's core pipeline ARX517 is still in the early stages of clinical trials, it is currently the only prostate-specific membrane antigen (PSMA)-targeted ADC new drug. Clinical data for the treatment of metastatic castration-resistant prostate cancer has shown promising safety and efficacy, with the potential to be the best in its class.

Prostate cancer is a key focus area for Johnson & Johnson, which already has best-selling drugs such as Zytiga, Erleada, and Akeega, along with numerous early-stage clinical pipelines, including PSMA/CD28 bispecific antibodies, KLK2-targeted radioligand therapy, and CD3/KLK2 bispecific T-cell engagers. This acquisition not only strengthens its R&D capabilities in the ADC field but also further solidifies its market position in the prostate cancer sector.

MNCs like Johnson & Johnson often pursue mergers and acquisitions that create synergy between the acquired assets and their own products, achieving a 1+1>2 effect.

For instance, Novartis acquired MorphoSys for nearly $3 billion, eyeing its BET inhibitor pelabresib (CPI-0610) to be used in combination with its own ruxolitinib for treating patients with myelofibrosis (MF). In a Phase 3 clinical trial targeting MF patients who did not respond to JAK inhibitors, the combination therapy achieved the primary endpoint of spleen volume reduction. Additionally, all four clinical disease markers of MF—splenomegaly, disease-related symptoms, anemia, and bone marrow fibrosis—showed improvement after the combination treatment.

BI's $1.3 Billion Acquisition of Nerio Is the Same: Nerio’s Small-Molecule PTPN1/N2 Inhibitor Has FIC Potential, Not Only as a Monotherapy but Also in Combination with Various Cancer Therapies Developed Internally by BI to Create New Cancer Treatments.

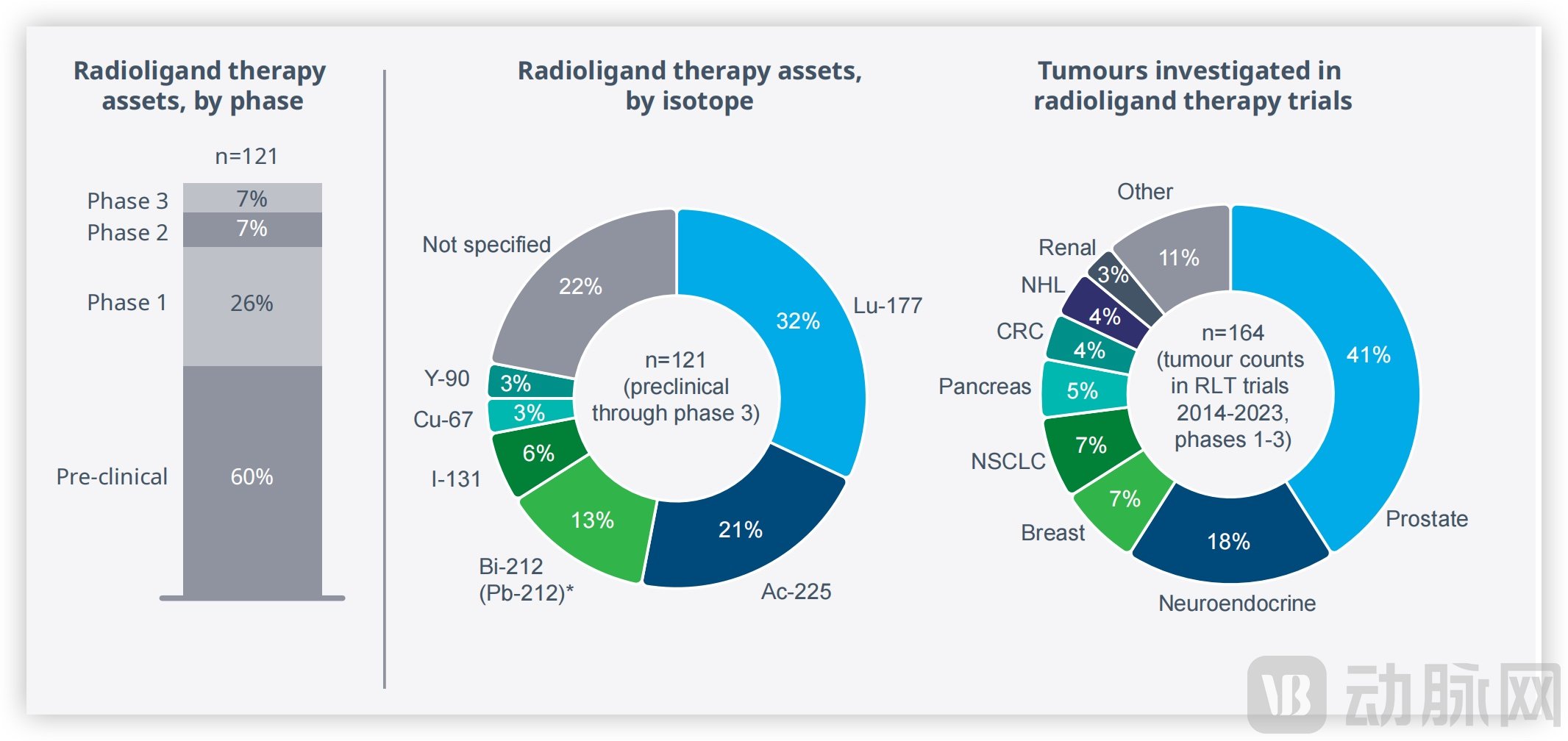

In addition to ADC, the field of radioligand therapy (RLT) is also thriving.

With the success of Novartis' Lutathera and Pluvicto, two nuclear medicines, the industry's interest in nuclear medicines is growing daily. A large amount of funding has started to flow in, and pipelines are continuously expanding. According to IQVIA data, as of July 2024, approximately 40 companies worldwide are developing about 121 nuclear medicine pipelines, with 40% of the projects already in the clinical stage and the remaining 60% still in the early stages.

Moreover, in terms of isotope classification, although the Lu-177 isotope, which emits β-rays, still accounts for the highest proportion (32%) of RLT under development, the current trend shows that the focus of research and industry investment is gradually shifting towards α-radioisotopes (accounting for 21%). Compared with β particles, α particles have greater energy and limited penetration distance, enabling high-intensity destruction of tumor tissues while avoiding damage to nearby healthy cells.

Global Pipeline of Radioligand Therapy, Source: IQVIA

Facing such a situation, AstraZeneca didn't hesitate to act in Q1 2024. The target was Fusion, a company it had already collaborated with back in 2020, which focuses on the development of targeted alpha-particle therapy. As interest in this field heats up, AstraZeneca's decision to fully acquire a well-known partner like Fusion seemed only natural. Not only does Fusion have multiple nuclear medicine pipelines under development, but it also possesses the capability to produce clinical GMP doses of radiopharmaceuticals. This is highly attractive for AstraZeneca as a newcomer to the field.

Novartis' acquisition of Mariana includes a series of RLT projects from hit compound optimization to early development, covering various solid tumor indications such as breast cancer, prostate cancer, and lung cancer. It also includes MC-339, an actinium-based RLT candidate being studied for small cell lung cancer. This acquisition further enriches Novartis' RLT pipeline.

In addition, the application of bispecific/multispecific antibodies in the field of oncology is also a key focus for MNCs.

MSD Acquires Harpoon for $680 Million, Double Harpoon's Closing Price on the Day. This acquisition not only grants MSD access to the highly promising DLL3/CD3 antibody currently in clinical trials but also provides it with multiple tri-specific antibody platforms from Harpoon, particularly the next-generation ProTriTAC and TriTAC-XR platforms that can be specifically activated in the tumor microenvironment, allowing MSD to quickly enter the TCE field.

It is worth mentioning that MSD has submitted a clinical application in China for the acquired tri-specific antibody in early December, ranking alongside Roche's RO7616789 and Zelgen Biologics' ZG006 as the globally leading DLL3-targeted tri-specific antibodies. With the previous involvement of Sanofi and Roche, the competition for bispecific/multi-specific antibodies in the oncology field will become even more intense in the future.

As the most important细分赛道 in the pharmaceuticals industry, mergers and acquisitions in the oncology field seem to have little connection with Chinese Biotech. This may not be good news for Chinese Biotech companies currently facing a寒流. However, perhaps we can discern from the limited transactions what kind of Chinese Biotech meets the aesthetic standards of multinational corporations (MNCs).

Looking at the acquired Biotech companies, their value is approximately equal to the value of their core pipelines, with a technological platform being a bonus. Simply put, small and beautiful Biotech companies are more likely to be favored by MNCs.

However, there are not many Chinese Biotechs that truly meet the definition of "small and beautiful."

It can be seen that in the M&A deals of multinational corporations (MNCs) in 2024, Chinese Biotechs were hardly present, with the only two acquired companies being bought by BioPharmas like Genmab and BioNTech. However, this gives us a glimpse into what kind of Chinese Biotechs are more likely to be chosen by multinational pharmaceutical companies.

Genmab Acquires Protheon Biotech for $1.8 Billion: A Leading Chinese Biotech in the ADC Drug Field

The disclosed R&D pipeline of Propharm Biotech includes three projects that have entered clinical trials: Rina-S (PRO1184, an ADC targeting FRα), PRO1160 (an ADC targeting CD70), and PRO1107 (an ADC targeting PTK7); as well as multiple preclinical projects, including PRO1286 (a bispecific ADC targeting EGFR and cMET).

Several projects entering clinical trials have shown considerable potential, especially Rina-S. Since FRα is minimally expressed in normal tissues but overexpressed in various solid tumors such as non-small cell lung cancer, mesothelioma, and endometrial cancer, it has the potential to become an ideal target. Prior to the transaction, Rina-S had already been granted Fast Track designation by the FDA for treating patients with FRα-expressing high-grade serous or endometrioid platinum-resistant ovarian cancer.

As the acquirer, Genmab's strengths lie in the field of antibody development, particularly in enhancing efficacy and reducing toxicity in the development of monoclonal antibodies and bispecific antibodies. Protheon’s ADC technology platform improves drug hydrophilicity by introducing hydrophilic molecular fragments based on Seagen's technological approach, significantly enhancing the compatibility of lipophilic payloads with antibodies. The addition of Protheon allows Genmab to explore more possibilities in ADC drug development.

If the "small" of Provention Bio lies in its scale and the "beauty" in its deep cultivation of the ADC track, then another company that has been acquired, Prime Medicine, represents a different kind of "small but beautiful."

The story of BioNTech and Promab began a year before the acquisition. At that time, BioNTech obtained the rights to Promab's PM8002, a PD-L1/VEGF bispecific antibody in Phase 3 clinical trials, for markets outside Greater China, at a total cost of $1 billion (with an upfront payment of $55 million).

Although PD-L1/VEGF are both conventional targets, which may not appear to be highly innovative, this year Akeso Biopharma's PD-L1/VEGF bispecific antibody AK112 outperformed Keytruda in a head-to-head clinical trial for one of its indications, instantly igniting market enthusiasm.

Summit, which obtained the overseas rights to AK112, saw its stock price double in just a few days. Another Chinese biotech company, Immune-Onc Therapeutics, also licensed out its PD-L1/VEGF bispecific antibody for a total amount of $2 billion. Meanwhile, PM8002 from Primus has already laid out 9 indications and entered the clinical stage, with clinical data presented at ESMO showing positive results, indicating significant potential.

With its own potential and the "teammates" carrying the sedan, BioNTech has decided to further strengthen its ties. However, the final transaction method is worth pondering. The price of the PM8002 pipeline alone has reached $1 billion, while the acquisition of the entire company only cost $800 million (upfront payment) + $150 million (milestone).

The company's value is less than its core pipeline.

To know that, apart from PM8002, Primus Bio has more than 10 pipelines, seven of which have entered the clinical stage, and one is already in Phase 3 clinical trials. Additionally, with production bases and an integrated antibody development platform, these assets are almost given away for free. However, for Primus, this is still a good deal. After all, securing 1 billion US dollars is not easy and involves significant risks.

Primus Bio's R&D Pipeline, Image Source: Company Official Website

The deal was also worthwhile for BioNTech. The day after the announcement, Lemz Therapeutics declared that it had granted MSD global rights to its PD-1/VEGF bispecific antibody for a total amount of $2.7 billion (with an upfront payment of $588 million).

After nearly a decade of development, many enterprises in China's Biotech industry have developed product pipelines covering multiple tracks, with core assets being relatively less focused. This is not favorable for multinational corporations (MNCs) interested in mergers and acquisitions. Perhaps the 2024 Sanofi-Inhibrx acquisition deal can offer some insights.

After completing the acquisition, Sanofi only incorporated one of Inhibrx's core rare disease pipelines into its own R&D sequence. The remaining pipelines, along with the employees, continued to operate independently under the new Inhibrx entity, while Sanofi holds a partial equity stake. This approach to acquisition deals offers some reference value for China's Biotech companies with multiple pipelines.

As the Oncology Field Cools Down, Biotech Acquisitions in 2024AmountThe laurel was won by the autoimmune track.

In the past five years, M&A activities in the autoimmune field have started to continuously heat up. The demand for innovative therapies in the market, strategic layout adjustments by companies, and support from the capital markets are all driving forces behind the development of this field. During this period, there were large-scale M&A events such as AstraZeneca's $39 billion acquisition of Alexion Pharmaceuticals.

Back to 2024, M&A events related to autoimmune diseases have been emerging endlessly, and M&A activities have been unusually active. In January, Novartis acquired Calypso for $250 million. The core asset, CALY-002, targets IL-15 and is used to treat celiac disease and eosinophilic esophagitis. By April, Regeneron had acquired the oncology and autoimmune assets of 2seventy Bio and established a new R&D department, Regeneron Cell Medicine.

In May, the autoimmune field witnessed a wave of mergers and acquisitions. Johnson & Johnson spent over $2 billion in total to acquire two autoimmune biotech companies, gaining two core bispecific antibody assets. Japanese company Ashahi Kasei also announced the acquisition of Swedish biotechnology company Calliditas Therapeutics for $1.06 billion, obtaining a pipeline for the treatment of IgA nephropathy.

In the second half of the year, TCE added fuel to the fire for the autoimmune field.

Candid Therapeutics, founded only a few months ago, has reached TCE collaborations with three companies—Nona Biotech, EpimAb Biotherapeutics, and Ab Studio—in a short period after acquiring two domestic TCE innovative drug companies. Considering that Candid is a NewCo Biotech specifically established for the purpose of selling, and given that its founder’s previous company was sold to BMS for $4.1 billion, it may create astonishing transaction events in the future.

Interestingly, TCE asset transactions are also a popular BD direction this year.

Including MNCs such as GSK and MSD, which have reached cooperation with Chinese Biotechs regarding TCE products. For instance, MSD paid $700 million upfront for acquiring the TCE pipeline from Tongrun Bio.

It is worth noting that, although most of the TCE pipelines in China are focused on oncology indications, after MNCs have invested substantial funds to acquire them, they have unanimously expressed intentions to use these TCE pipelines, originally developed for cancer indications, to pursue autoimmune clinical trials.

This also highlights the difference in mindset between MNCs and local Biotechs.

For domestic Biotech companies, applying new therapies to oncology is instinct-driven. However, in the view of multinational corporations (MNCs), the competition for TCE bispecific antibodies in the oncology field has already become crowded. By using T cells as effectors to kill B cells — which play a key role in autoimmune diseases — bispecific antibodies have the potential to cover dozens of indications in the autoimmune space. On the other hand, although TCE products have been clinically validated across various autoimmune diseases, overall development is still in its early stages, with results expected only years later, giving MNCs sufficient time to advance.

For Chinese Biotech, learning to grasp the aesthetic of MNCs can reflect real value in BD transactions by optimizing the R&D pipeline strategy, and provide an additional "path to success" for corporate development amidst the current downturn.