Global First CLDN18.2-Targeted Therapy Approved in China, Sparking Intense Competition from Domestic Players

Astellas

Pharmaceutical R&D Manufacturer

On the last day of 2024, Astellas'重磅药Zolbetuximab was officially approved for marketing in China.This is the world's first and currently only approved CLDN18.2-targeted drug: In October 2024, Zolbetuximab was the first to receive FDA approval, and subsequently successfully entered major markets such as Europe and Japan.。

As a popular target for global gastric cancer drug development following HER2, the competition for CLDN18.2 is quite intense globally. According to the VCBeat database, apart from the already approved zolbetuximab, there are more than 70 drugs worldwide in active status. Among these,Chinese-produced drugs take the dominant position, not only accounting for nearly 90% of 70 drugs, but also occupying all seven CLDN18.2-targeted drugs that have currently progressed to Phase III clinical trials.。

However, with the global approval of zolbetuximab as a pioneer, the original competitive landscape has been disrupted, and domestically produced drugs with "group advantages" are beginning to catch up.

Taking CARsgen Therapeutics as an example, its self-developed CLDN18.2-targeted autologous CAR-T therapy—Surugicel (generic name: oladencabtagene autoleucel) injection—has recently achieved significant breakthroughs in a pivotal Phase II clinical trial in China for the treatment of gastric cancer, with a disease control rate (DCR) as high as 91.8%. Innovent Biologics has also made substantial progress recently; its CLDN18.2 antibody IBI343 is currently in Phase III clinical trials in Japan and is expected to become the world’s first CLDN18.2 ADC new drug. Additionally, other CLDN18.2-targeted drugs, such as Mingji FG-M108, Aosaikang ASKB589, Hengrui SHR-A1904, and Connect Biopharma CMG901, have also seen major breakthroughs recently.

It can be said that,Chinese-produced drugs are currently accelerating rapidly and attempting to secure the first domestically approved drug targeting CLDN18.2, in order to break Astellas' dominant market position.。

"Magic" target, large BD continuously

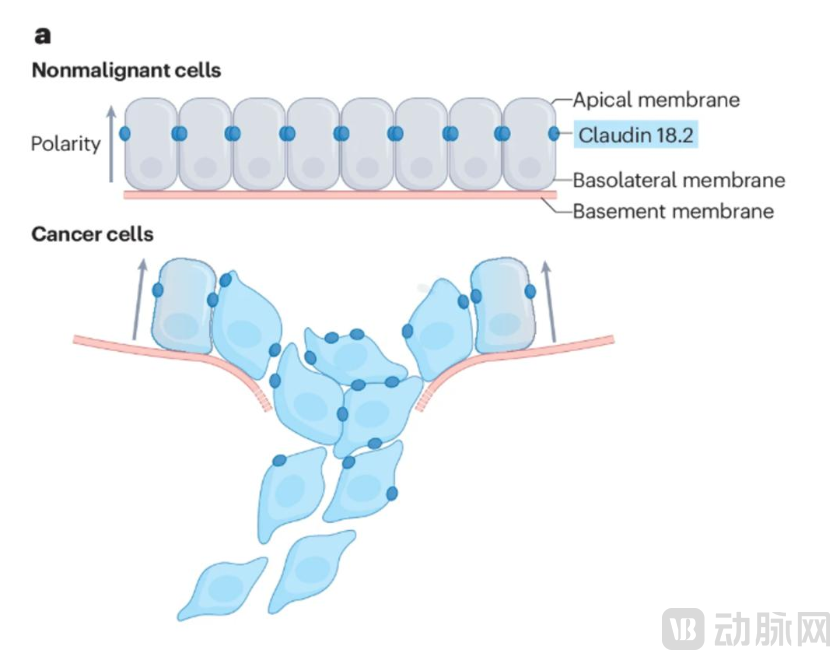

From the market response,CLDN-18.2 is the most focused target in the Claudin family so far., of course, this is mainly due to its high expression in various tumors such as gastric cancer, pancreatic cancer, esophageal cancer, and lung cancer.

Figure 1. Expression of CLDN18.2 in Tumor Tissues

It is reported that under normal circumstances, CLDN-18.2 is expressed at low levels in the differentiated epithelial cells of the gastric mucosa, mainly functioning to complete intercellular connections. However, when CLDN-18.2 is activated, it can damage cell membrane function, increase tissue permeability, and open a "convenient door" for tumor metastasis, indicating tumor proliferation, differentiation, and invasive metastasis. According to research findings,CLDN-18.2 is expressed in up to 60%-80% of gastric cancer cases, making it a "dark horse" in the field of gastric cancer treatment.。

This has also received positive feedback at the BD level. For example, the first approved drug, zolbetuximab, was acquired by Astellas in 2016 for $1.4 billion from Ganymed Pharmaceuticals.

In recent years, domestically produced drugs in China have also started to participate frequently. In May 2022, Turning Point acquired partial development and commercialization rights of LM-302 from Limin Pharmaceuticals for a total value exceeding 1 billion US dollars; In July 2022, Kelun Biotech reached a collaboration and exclusive licensing agreement with Merck for SKB315, with a total transaction value surpassing 900 million US dollars; In February 2023, Connaught and Lepu jointly announced the authorization of CMG901 to AstraZeneca for a total value exceeding 1.1 billion US dollars; In October 2023, Hengrui Medicine announced an exclusive licensing agreement with Merck for its self-developed SHR-A1904, with a potential total transaction value as high as 1.4 billion euros.

According to incomplete statistics from VCBeat,Over the past two years, there have been more than 25 BD collaborations on the CLDN-18.2 target, involving a total amount of nearly 15 billion US dollars, and leading MNCs have increased their investments.。

The Reasons Behind the "Cash Grab" in the Midst of a Severe Winter: Firstly, it Lies in the Market. CLDN-18.2 Mainly Targets Gastric Cancer, Which is Hard to Detect in Its Early Stages and Has an Extremely Low Five-year Average Survival Rate, Leading to a Huge Demand for Drugs. According to Frost & Sullivan's Forecast,The global gastric cancer drug market size has grown to USD 22.1 billion in 2024 and is expected to reach USD 36.4 billion by 2030.. The huge potential market undoubtedly provides more options for pharmaceutical companies urgently seeking new growth points.

Secondly, in terms of key efficacy, in recent years, targets such as HER2, PD-L1, MET, and FGFR-2 have successively shown promise, creating numerous possibilities for gastric cancer treatment. CLDN-18.2, as a new target, is not to be outdone and shows potential to surpass the others, with several significant drugs demonstrating breakthrough performance in clinical trials.

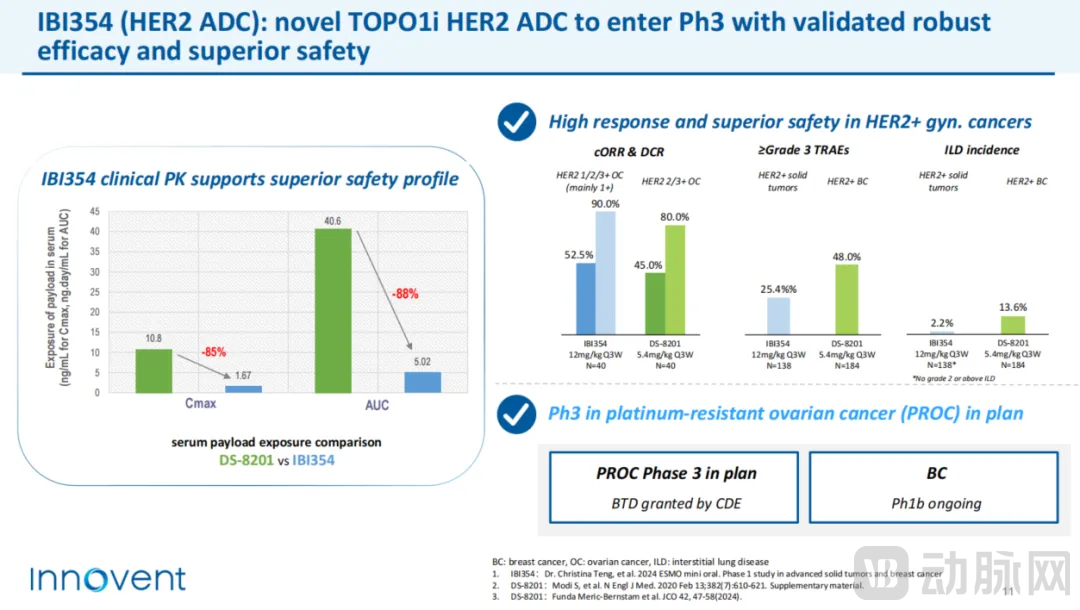

Figure 2. Key Clinical Data of IBI343 by Innovent (Source: Innovent JPM Conference Presentation PPT)

Figure 2. Key Clinical Data of IBI343 by Innovent (Source: Innovent JPM Conference Presentation PPT)

Taking IBI343 from Innovent Biologics as an example, it was recently officially included by the CDE as a breakthrough therapy drug candidate, which is an absolute affirmation of its efficacy. In June 2024, Innovent orally presented clinical data of IBI343 in the treatment of advanced gastric or gastroesophageal junction adenocarcinoma (G/GEJ AC), with an overall objective response rate of 32.3% and a disease control rate of 75.8%. Additionally, there is SHR-A1904 from Hengrui. According to its latest published data in G/GEJ AC treatment, its objective response rate and disease control rate were 55.6% and 88.9%, respectively.

The last point is about market competition. Currently, the CLDN-18.2 target has only one approved drug, zolbetuximab, making the market landscape very open with plenty of opportunities for "latecomers."

Who Can Obtain the First Approved Drug in China?

In fact, as domestically produced drugs continue to gain momentum, a question is becoming increasingly prominent:Who can be the first to cross the finish line and become the first China-produced drug approved for the CLDN18.2 target?

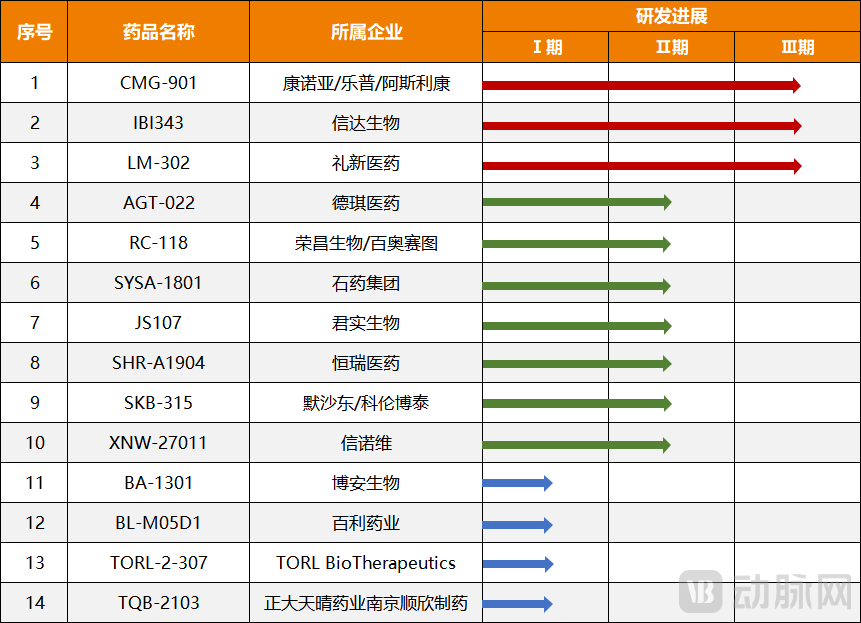

Figure 3. Seven CLDN18.2-targeted drugs in Phase III clinical trials (Data source: Public information)

Figure 3. Seven CLDN18.2-targeted drugs in Phase III clinical trials (Data source: Public information)

Currently, the seven targeted drugs that have progressed to Phase III clinical trials clearly have a better chance. These include three monoclonal antibody drugs (Mingji FG-M108, Aosaikang ASKB589, Chansyn Osemitamab) and four ADC drugs (Limin TPX-4589, Hengrui SHR-A1904, Konnua CMG901, Innovent IBI343).

It is reported that in the CLDN18.2 target, various forms such as monoclonal antibodies, bispecific antibodies, ADCs, and CAR-T are flourishing.But in terms of clinical manifestations and the number of layouts, the status of monoclonal antibodies remains unshakable.For example, Astellas' zolbetuximab, which was the first to emerge, belongs to the monoclonal antibody drug class. The same is true for domestically produced monoclonal antibody drugs, with generally rapid research and development progress. Three monoclonal antibody drugs all began Phase III clinical trials in September-October 2023, significantly earlier than the four ADC drugs also in Phase III.

Of course, this is mainly due to its morphological characteristics, as monoclonal antibodies are antibodies produced by a single B-cell clone. Coupled with their mature technical route and relatively low research and development costs, clinical progress has been rapid. Additionally, in terms of critical efficacy data, monoclonal antibodies also have a say. Among the currently disclosed CLDN18.2 monoclonal antibody drugs for treating advanced gastric or gastroesophageal junction adenocarcinoma, the disease control rate exceeds 80%. It is precisely because of this that, apart from Mingji, Aosaikang, and Transcenta, leading pharmaceutical companies such as CSPC, Junshi, Qilu, and Zai Lab have all increased their investments, and they all stand a good chance of securing the first batch of approvals in China.

Figure 4. Clinical progress of representative drugs for CLDN18.2 ADC (Data source: Insight)

Figure 4. Clinical progress of representative drugs for CLDN18.2 ADC (Data source: Insight)

Beyond monoclonal antibodies, ADCs are next in line.In terms of drug mechanism, ADC can be considered as a combination of monoclonal antibody and chemotherapy, with the only difference being the chemotherapeutic agents. However, in terms of mechanism and composition, ADC drugs may be superior to the combination regimen of monoclonal antibody and chemotherapy. For instance, CMG901, a CLDN18.2 ADC drug jointly developed by Connaught and Lepu, consists of a CLDN18.2 monoclonal antibody, a cleavable linker, and a cytotoxic small molecule monomethyl auristatin E (MMAE). According to clinical data, it shows an objective response rate of 75% in treating advanced gastric or gastroesophageal junction adenocarcinoma, demonstrating excellent performance.

In terms of safety, since ADCs use antibodies as "guides" to precisely deliver chemotherapy drugs into tumor cells, they can reduce damage to normal cells, making the treatment process milder and more effective. This has also been validated in IBI343 developed by Innovent Biologics, which, in non-head-to-head comparisons, showed lower incidence rates of gastrointestinal adverse events, hypoalbuminemia, and discontinuation due to adverse events. Therefore, it is considered a strong contender as the world's first CLDN18.2 ADC to embark on commercialization.

Next, focus on CAR-T, which is also worth paying attention to.According to the VCBeat database, there are currently 21 CLDN18.2 ADCs in development globally, but most are concentrated in Phase I and Phase II trials. Among these, the most advanced is CARsgen's CT041, which as early as 2021 announced preliminary clinical efficacy data. The results showed that in GC/GEJ patients with mainly medium to high expression of CLDN18.2, the ORR reached 61.1%, comparable to some ADC drugs.

However, as research continues to deepen, the drawbacks of CAR-T have gradually emerged. On one hand, there is a slight decline reflected in key clinical data; on the other hand, it lies in the cost and affordability. The high expenses and development costs of CAR-T therapy stand in stark contrast to the current payment environment in China and the financial capacity of patients.

Lastly, bispecific antibodies (bsAbs) must be mentioned. In fact, with monoclonal antibodies (mAbs) preceding them, antibody-drug conjugates (ADCs) following them, and chimeric antigen receptor T-cell (CAR-T) therapies alongside them in the market landscape, bsAbs have not garnered much attention for the CLDN18.2 target. The reason mainly lies in their relatively lagging clinical development, and from the currently published clinical data of CLDN18.2 bsAb drugs, there is nothing particularly remarkable. Nevertheless, they remain an undeniable force for the future, primarily because they can exert anti-tumor effects through multiple mechanisms while also demonstrating significant advantages in terms of safety.

It is not difficult to see that the existing CLDN18.2-targeted drugs each have their own advantages and disadvantages. As for who will take the lead, there is currently no standard answer, but the rigid conditions are gradually becoming clear.

In this regard, a senior insider told VCBeat, "An ideal CLDN18.2-targeted drug should possess two key characteristics: one is high safety, which depends on the selectivity of the molecule—insufficient selectivity can lead to erroneous binding with CLDN18.1, affecting the drug's therapeutic efficacy while causing significant side effects in the human body; the other is high affinity, where, in most cases, the higher the affinity, the stronger the drug’s expression capability, resulting in more pronounced anti-tumor effects.". Of course, the speed of realization and choices at the clinical progress level are also crucial.

With Precious Gems Ahead, Will Commercialization Turn Left or Right?

Currently, CLDN18.2 is primarily targeted at gastric cancer, which is a market with tremendous potential. The market size has already exceeded tens of billions of US dollars and is still growing rapidly. However, in this disease area, HER2 has already achieved commercialization first. Representative drugs include Roche's Trastuzumab, Merck's Pembrolizumab, Hengrui's Apatinib, and RemeGen's Vidotuximab.

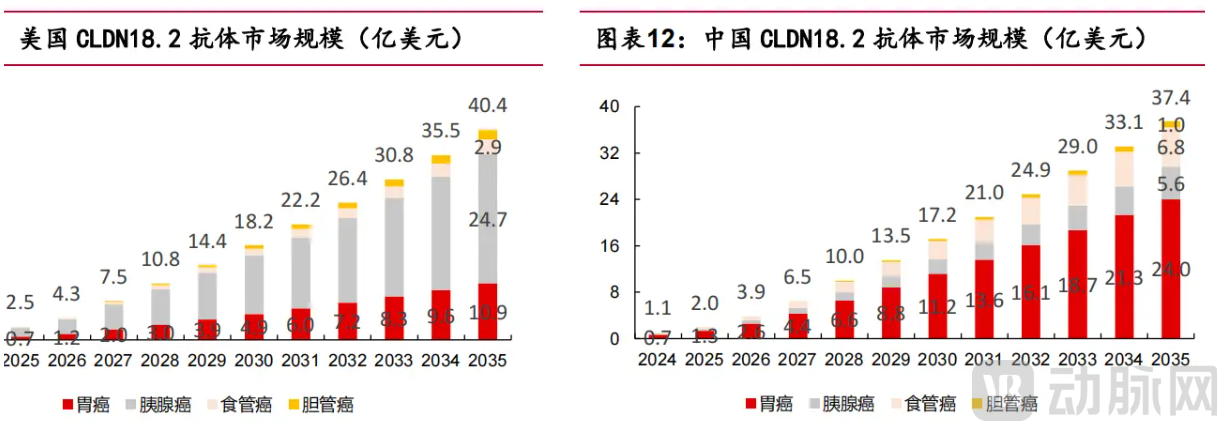

Figure 5. Market Size of Different Indications for CLDN18.2 Antibodies in China and the US (Source: Zheshang Securities)

Figure 5. Market Size of Different Indications for CLDN18.2 Antibodies in China and the US (Source: Zheshang Securities)

Among these, Roche's trastuzumab has shown the strongest performance, with sales in the first three quarters of 2024 reaching 1.244 billion Swiss francs, a year-on-year increase of 58%, dominating the global market. In China, Hengrui's self-developed drug apatinib has stood out, with global sales in 2023 surpassing the 10 billion yuan mark, reaching 10.8 billion yuan.

Therefore, with predecessors setting high standards, CLDN18.2 needs to demonstrate more solid strength while also learning to take an alternative path to rise above.

The first point is to speed up the approval process, accelerate the pace of market entry, and seize the first-mover advantage."This point is particularly important. In this regard, a senior investor emphasized, 'Because the disease area of CLDN18.2 is far less extensive than PD-1, latecomers won't have a diverse range of indications to choose from, so they need to win in speed and seize the market opportunity.'"

The second is to expand as many indications as possible and摆脱单一市场性依赖.It is reported that, in addition to high expression in gastric cancer, CLDN18.2 can also be highly expressed in various other tumors such as pancreatic cancer, esophageal cancer, and lung cancer, all of which present potential opportunities for CLDN18.2-targeted drugs. For instance, IBI343 developed by Innovent Biologics was officially granted Fast Track Designation (FTD) by the FDA in June 2024. It is intended for use in patients with advanced pancreatic ductal adenocarcinoma who are CLDN18.2-positive and have received at least one prior systemic therapy.

Finally, it is important to seize more monetization opportunities, including but not limited to going overseas, business development (BD), mergers and acquisitions, etc.In the current market environment, innovative drugs are also seeking more monetization opportunities. In the past year or two, methods such as going overseas and business development (BD) have been highly favored, with quite a few successful cases already. CLDN18.2-targeted drugs can completely follow suit; for example, in terms of going overseas, IBI343 has taken the lead—its clinical research in Japan has now entered Phase III, with the market launch imminent. Additionally, regarding BD, apart from existing cases, numerous large-scale collaborations are in the pipeline, primarily focusing on Phase II targeted drugs, all of which are expected to materialize in the first half of this year.

In this regard, a senior insider commented, "As the overall market tightens, the competition in innovative drugs is not only reflected in technology and clinical performance but also in monetization capabilities, which are equally crucial. Especially for emerging targets like CLDN18.2, there is currently a particular emphasis on commercialization capabilities. Therefore,Seizing all means of monetization to promptly obtain cash flow and investing it into the development of more indications is evidently a more ideal choice.。”

In fact, with the widespread global approval of zolbetuximab, CLDN18.2, after years of development, has rapidly shifted from competition in drug modality and speed to a commercial showdown of clinical value. In this already unfolding battle, numerous domestically produced innovative drugs are launching fierce attacks on zolbetuximab, poised to challenge Astellas' current dominant position.

1. "CLDN18.2: The Crucible of China-produced Innovative Drugs" —— VBInsight Database;

2. "The Never-Ending War, Claudin18.2 Target Creates New Waves" —— Gazelle Society;

3. "Market Trend Analysis of Gastric Cancer: Accelerated R&D of CLDN18.2-targeted Drugs, Pharmaceutical Companies Rush to Strategize" —— MoEntropy Pharma.