Source of the article: HeartFuture; Editor: SophiaReprint Requirements: If the source of the article is indicated at the beginning of the text, it can be reprinted directly.In the medical device field, as companies expand in scale and competition becomes increasingly fierce, it is becoming more difficult for companies to internally develop revolutionary original technologies. Moreover, the market size of niche segments within the medical device field is relatively small, with poor technical versatility. Many companiesChoose to directly acquire those technologies that have been clinically validated when the time is ripe., such as the giants in the global medical device industry,Johnson & Johnson, Medtronic, Abbott, Boston Scientificetc.

The Pioneer of Domestic M&A Belongs toMindray MedicalAndGIAN HealthcareThese two companies. Mindray, through self-research and mergers and acquisitions, has gradually become the leading medical device company in China and entered the global top thirty. Ginza Medical, on the other hand, has become a unicorn in minimally invasive surgery through acquisitions, licensing, agency, local product innovation, and production.

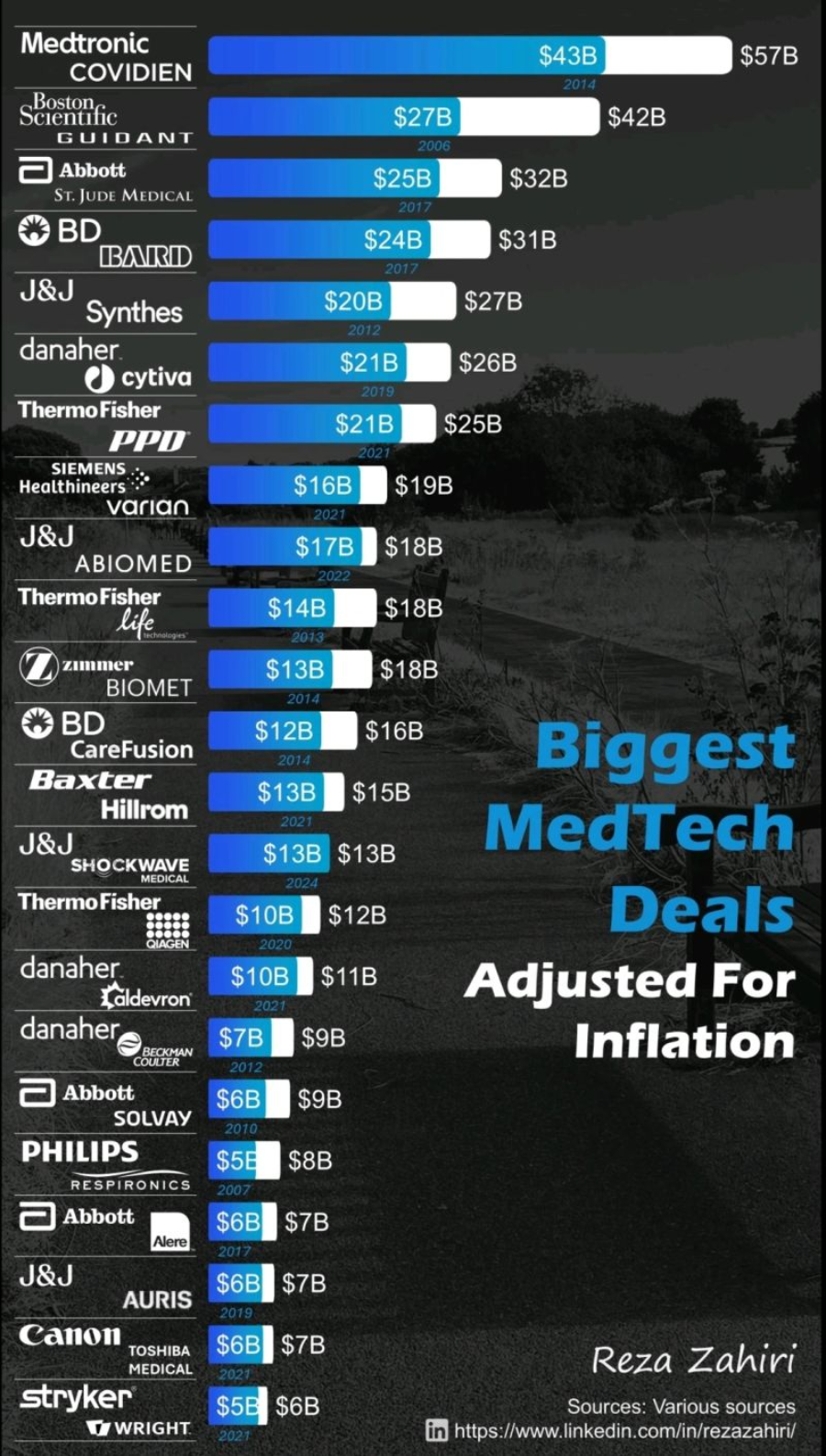

This phenomenon not only reflects the intrinsic demands of enterprises for seeking scale effects, technological advancements, and market expansion but also promotes the efficient allocation of resources and the rapid iteration of technology.In 2024 alone, there were 31 mergers and acquisitions in the medical device field at home and abroad, with a total acquisition amount exceeding 38 billion US dollars.。

This article will delve into the field of medical devices.TOP 3 in the Global Top 20 Acquisition Cases, analyzing the strategic intentions, market impact, and long-term influence on the industry landscape behind these mergers and acquisitions, providing referable experiences for those enterprises eager to grow.

Top 20 Global Acquisition Cases# Top1 Medtronic AcquisitionCovidien

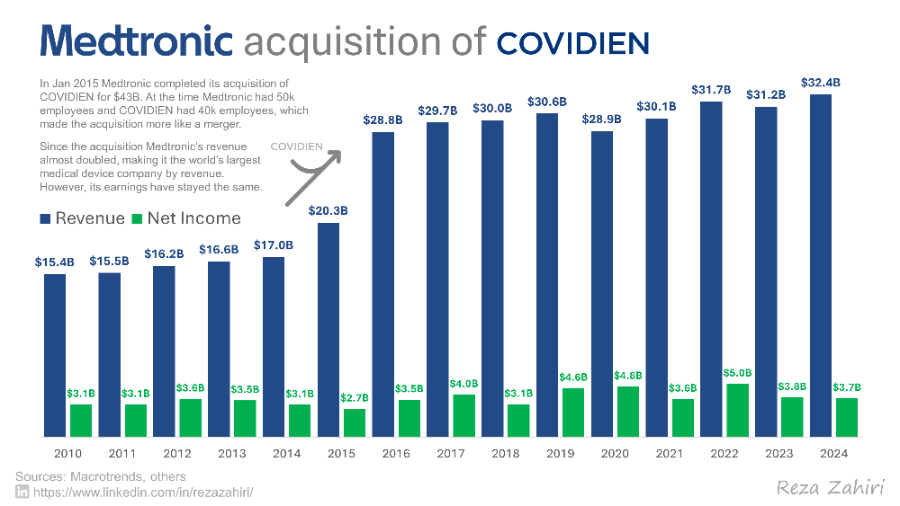

Top 20 Global Acquisition Cases# Top1 Medtronic AcquisitionCovidienIn June 2014, Medtronic announced$429 billionThe price to acquire Covidien, this is so farThe World's Largest Medical Device M&A Case。

Covidien, as a global leading supplier of clinical and home medical devices,Its product line and market channels form a strong complement to Medtronic,After the acquisition, Medtronic relocated its headquarters to Dublin, Ireland, paving the way for the diversification and expansion of its global business.Building on this, Medtronic established the Minimally Invasive Therapies Group (MITG), which focuses on pulmonary, pelvic, renal, gastrointestinal diseases, and obesity, further solidifying its leadership position in the field of minimally invasive therapies.At the same time,Covidien's neurovascular business merges with Medtronic's Restorative Therapies Group (RTG),Jointly provide comprehensive solutions for brain and pericranial vascular diseases,This integration undoubtedly strengthens Medtronic's market competitiveness in the neurovascular field.After the merger, Medtronic has more than 85,000 employees in 160 countries, and its business in emerging markets has nearly doubled.

Before the acquisition, Covidien's annual revenue in 2013 was $10.2 billion, and Medtronic's was $16.6 billion.After the acquisition, Medtronic's revenue reached $29 billion in 2016, making it the world's highest-revenue medical device company.

In FY2024, Medtronic achieved revenue of $32.364 billion, representing a year-over-year increase of 3.6%. All business segments performed well.Cardiovascular business revenue reached 11.831 billion US dollars, increasing by 2.7% year-on-year.; Surgical and Critical Care business revenue was $8.417 billion, a year-on-year increase of 5.4%; Neuroscience business revenue was $9.406 billion, a year-on-year increase of 5.0%; Diabetes business revenue was $2.488 billion, a year-on-year increase of 10.0%.Medtronic has rapidly expanded its scale through the acquisition of Covidien.Despite some challenges faced by Covidien in recent years, overall, Medtronic has achieved its strategic goals through this acquisition and maintained its leadership position in the global medical device market.# Top 2 Boston Scientific Acquires Guidant

Boston Scientific in 2006 with$27 billionAcquired Guidant, becomingChinaThe World's Largest Cardiovascular DeviceMedical Device Manufacturer。This deal sparked widespread controversy at the time, with the media even calling it historic.UpThe Second DumbestThe acquisition case, second only to the merger of Time Warner and AOL. But is this really the case?

Guidant, the medical device division of pharmaceutical giant Eli Lilly, was spun off and became an independent listed company in 1994. At that time, Guidant ranked second only to Medtronic in the business field of implantable defibrillators and pacemaker series.

At that time, both Johnson & Johnson and Boston Scientific responded to the acquisition of Guidant, and finally,Boston Scientific Acquires Guidant's Implantable Defibrillator and Pacemaker Series Product Business for $3 Billion More Than Johnson & JohnsonAfter the acquisition, its scale once surpassed that of Medtronic, making it the world's largest cardiovascular device manufacturer.

Boston Scientific's AcquisitionNot only did they pay a high price, but they also had to pay Johnson & Johnson a $700 million breakup fee, as Johnson & Johnson had previously reached a preliminary acquisition agreement with Guidant.In addition,Guidant's core products - implantable defibrillators and pacemakers - have faced multiple lawsuits due to product defects that led to patient deaths.For BostonScience has brought countless legal troubles.

Since both Boston Scientific and Guidant have cardiovascular stent businesses, Boston Scientific, as the market leader, had to sell Guidant's related business to Abbott to avoid antitrust scrutiny hindering the merger. This has cultivated a strong competitor for itself in the future.Hand,In 2006, Abbott launched a new generation of drug-eluting stentsLaunch Xience V, subsequently joining the fray with Boston Scientific, Johnson & Johnson, and Medtronic.

Since then, Johnson & Johnson's cardiovascular business has been on the decline, with Cordis failing to launch any products that are competitive in the market. In May 2015, Johnson & Johnson sold Cordis for $2 billion to Cardinal Health, a leading American pharmaceutical commercial company. Since then, Johnson & Johnson announced its withdrawal from the cardiovascular stent market.As of now, the global cardiovascular stent field is led by Boston Scientific, Abbott, and Medtronic.

Looking back,The leaders of Boston Scientific were not unaware of the cost of acquiring Guidant and the subsequent troubles. At the time, Boston Scientific was the global leader in cardiovascular stents, but companies with stronger backgrounds and more capital, such as Medtronic and Abbott, were all eyeing the market hungrily.The market share of Boston Scientific's cardiovascular stents will gradually be caught up with or even surpassed. Therefore, it is necessary to find another sufficiently large market sector that can diversify the company’s business without incurring excessive risk.。

Today's Boston Scientific has achieved a rebirth, revitalizing the company through corporate acquisitions and launching new products. Strategically, Boston Scientific’s acquisitions have focused more on peripheral interventions, cardiac electrophysiology, and heart valve fields, with relatively smaller scale. Through these acquisitions, the company has established itself in surgical MedSurg, cardiac rhythm, and neuromodulation (Rhythm andNeuro), cardiovascular, and three major business lines, among whichCardiovascular intervention business still accounts for more than 25% of Boston Scientific's revenue.。

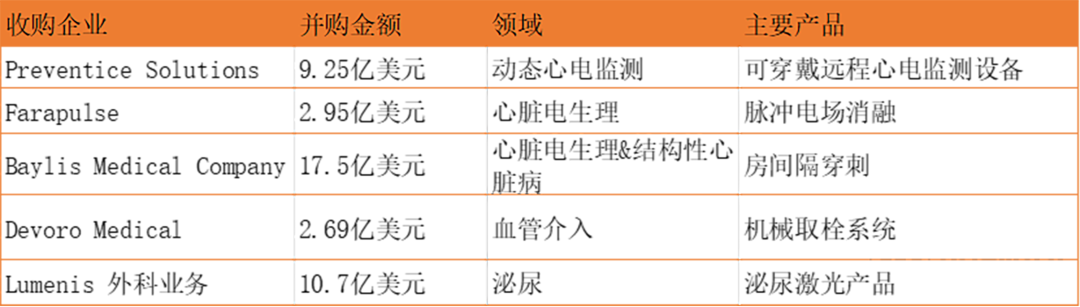

In 2021 alone, Boston Scientific launched 145 clinical trials, introduced 90 innovative products, and acquired five companies (Preventice Solutions, Farapulse, Baylis Medical Company, Devoro Medical, and Lumenis LTD's surgical business) to complement its existing product portfolio.

In the third quarter of 2024, Boston Scientific's revenue increased to $4.21 billion, a year-on-year increase of 19.4%, far exceeding market expectations. Among this,Cardiovascular business is the core driver of Boston Scientific, with net sales in the third quarter increasing by 29.2% year-over-year.。

TotalIn general, Boston Scientific CorporationGuidant'sCollectPurchase AlthoughPlagued by product defects and legal issues, but in the long run, it became...A turning point for the company's rapid development.

# Top 3 Abbott Acquires St. Jude MedicalAbbott in 2017 with$25 billionThe acquisition of St. Jude Medical greatlyStrengthens Abbott's Competitiveness in the Cardiovascular Business Field。After the acquisition was completed, Abbott's stock price and market response were positive, showing the market's favorable evaluation of this acquisition.

Strengthening in the business field:St. Jude focuses on multiple fields such as heart failure, arrhythmia, vascular disease, and structural heart disease.Through the acquisition of St. Jude Medical,Abbott has acquired key products such as heart failure treatment devices, catheters, and defibrillators, which complement its existing coronary intervention and valve repair products., making YaMedtronic gains a competitive advantage in several important细分领域 of the cardiovascular market.

Enhancement of Market Position:After acquiring St. Jude Medical, Abbott is capable ofCardiovascular drug-eluting stents, Cardiac Rhythm Management devices (CRM), Arrhythmia and Atrial Fibrillation devices, Structural Heart Disease devices (Occluders), Heart Valve devices, etc.Full Range of Cardiovascular Medical Device FieldsCompeting with Medtronic significantly elevated Abbott's ranking in the global cardiovascular market, establishing it as a leading player in the cardiovascular field.

Launch of Innovative Products:After the acquisition, Abbott has gained broader channels in the cardiovascular and neuromodulation fields, providing patients with next-generation innovative medical technologies and enhancing the efficiency of healthcare systems worldwide.

Abbott's cumulative revenue in the first three quarters of the 2024 fiscal year was $30.976 billion, a year-on-year increase of 3.71%.Global sales in the third quarter reached $4.7 billion, with an organic growth of 13.3% year over year. Among them,Sales of diabetes, structural heart disease, heart failure, and electrophysiology businesses all achieved double-digit growth.。

Overall, Abbott's acquisition of St. Jude Medical was a successful strategic move, which not only strengthened Abbott's product portfolio and market position in the cardiovascular field but also brought long-term growth potential and innovation momentum to the company.

# M&A-Driven Transformation

Reviewing 2024, the medical technology M&A market was exceptionally active, with major companies enhancing their capabilities and expanding business areas through acquisitions. However, upon closer reflection,The Arrival of the Medical Device Industry's M&A Era Comes with a Sense of HelplessnessOn the one hand, there is the seller's fear and regret, and the eagerness to board the "Noah's Ark" of mergers and acquisitions; on the other hand, there is the buyer's greed and caution, the calmness of holding cash and observing, and the meticulous selection of "targets."

The background of the increase in M&A activities includesThe exit demands of investment institutions, the obstruction of IPO channels, and the investment term pressure faced by enterprises. EspeciallyWhen the IPO channel is no longer smooth, being acquired becomes another option for enterprises., and the certainty of the transaction also increases - the buyer's advantage is further strengthened, and the seller has to make compromises in the valuation negotiations, enterprise creationThe original team and the investors behind them usually also have to give up a portion of their interests in order to successfully complete the acquisition transaction.

Since entering 2024, IPO regulatory policies have continued to tighten, with successive issuances of documents by the CSRC, the State Council, the Ministry of Justice, and other departments. These documents systematically standardize the coaching supervision of companies listed on the NEEQ, targeting the quality of enterprises' listing applications, while strictly cracking down on market chaos such as fraudulent issuance and financial fraud on the STAR Market.Going public becomes a destination that only a few enterprises can reach, while other startups have to turn to mergers and acquisitions to seek a way out.

Moreover, not all companies are qualified to sit at the negotiating table.The buyer selects the target either for its advanced technical advantages, unique business model, or healthy financial performance. Even if the profit is not high, at least there should not be a huge amount of losses.. Although these companies with decent performance can also hibernate until the end of the winter by relying on their own self-sustaining capabilities, the investment institutions behind them may not necessarily wait until spring comes. When the exit deadline stipulated in the investment terms arrives, the investors may not...If they can exit smoothly and receive their deserved returns, the repurchase clause signed initially will be triggered, and at this point, no one is a winner.

Under various external influencing factors,NoWhether Active or Passive, Investors and Entrepreneurs Can Only Take the Path of Mergers and Acquisitions。

For the sellerWhen IPOs are smooth, they will not consider mergers and acquisitions as the only option. Even if negotiations fail, there is still a chance to continue applying for an IPO. Nowadays, with no other options available to sellers, the certainty of transactions has increased.

For the buyer, The purpose of mergers and acquisitions is nothing more than to grow bigger or stronger, expanding market share and enhancing influence through acquiring companies, filling in the missing parts of their own business sectors, achieving a more diversified layout, in order to gain or maintain their dominant position in the market.For instance, Mindray's 6.65 billion yuan controlling acquisition of Huitai Medical is aimed at quickly entering the cardiovascular sector. Moreover, as a listed company on the A-share market, Huitai Medical does not face the pressure of investor exit that startups in the primary market do, thus having moreA large bargaining space, with an acquisition price of 471.12 yuan per share, representing a premium rate as high as 30.67%.

Although the era of medical device mergers and acquisitions in China is gradually beginning, it must be acknowledged that, due to the unique industrial environment in China,Medical Device M&A in China Is Unlikely to Fully Replicate the Acquisition Models of Global Giants, a group of major domestic device manufacturers in China need to accelerate their exploratory efforts, figuring out a merger and acquisition model suitable for the domestic industrial environment. MoreoverDomestic device manufacturers suffer from severe asset homogeneity, low differentiation, and relatively few original products, meaning there may not be many high-quality assets available for mergers and acquisitions.

However, opportunities are also hidden in the crisis,We should actively search for relevant technologies, product pipelines, and channel sales targets.。Are the valuations of medical device assets in A-shares, Hong Kong stocks, and Chinese概念股 approaching the bottom? Has the valuation bubble been completely squeezed out? Whether the optimal acquisition price is at the top, middle, or bottom needs to be determined based on specific赛道and negotiation agreements.Require the acquirer to have extremely strong judgment.。

But it can be foreseen that the number of companies seeking M&A transactions will increase until the market reaches a mature, rational, and new balance.In the complex business world, it is better to board the "Noah's Ark" before sinking, so as to preserve the halo of a hero. By the time everything collapses like a house of cards,Has become a tragic symbol.