AI-Analyzed Pharma Annual Reports: Semaglutide Poised to Dethrone Keytruda as Global 'Blockbuster Drug'

DeepSeek

Large Language Model (LLM) and Related Technology Developers

Novo Nordisk

Insulin Developer and Manufacturer

The threshold for the title of "King of Medicines" is approaching 30 billion US dollars.

According to the latest released 2024 annual report, K drug Keytruda (Pembrolizumab) successfully defended its title as the global "top drug" with a revenue of $29.482 billion in 2024, while Semaglutide generated a revenue of $29.296 billion in 2024, with a difference of less than $2 billion between the two.

From double-digit sales to nearly $30 billion in annual revenue, Keytruda took 10 years, while semaglutide only took 5 years.

In terms of growth rate, Keytruda (K药), which has been on the market for nearly a decade, saw an 18% year-over-year increase in 2024. In contrast, the rapidly rising star semaglutide recorded a 38% year-over-year increase, demonstrating a clear advantage. As a result, the market believes that semaglutide is highly likely to claim the top spot in 2025. Both Keytruda and semaglutide will face the issue of a patent cliff, and how they address these challenges in the future will be crucial in their battle for the title of "best-selling drug."

VCBeat tries to interpret the changes in the market behind the competition for the title of "King of Drugs" through DeepSeek's analysis of annual corporate reports, to see how the most popular large AI models view this.

DeepSeek: Analysis of Merck's 2024 Annual Report

1. Core Financial Performance

1.Revenue Growth: Total annual sales of $64.2 billion, a year-on-year increase of 7% (excluding the impact of exchange rate changes, growth was 10%).

2.Product Highlights:

KEYTRUDA (anticancer drug): Full-year sales of $29.5 billion, a year-on-year increase of 18% (22% excluding exchange rate effects), accounting for 46% of the company's total revenue.

WINREVAIR (New Cardiovascular Drug): Q4 Sales $200 Million, Annual Sales $419 Million, Becoming a New Growth Engine.

Animal Health Business: Full-year sales of $5.9 billion, a year-on-year increase of 4% (8% excluding exchange rate effects).

GARDASIL/GARDASIL 9 (HPV Vaccine): Impacted by the Chinese market, total annual sales reached 8.6 billion USD, representing a year-on-year decrease of 3%.

3.Profit and Earnings Per Share

GAAP EPS: $6.74 for the full year (compared to a loss of $0.48 and a profit of $0.14 in the same period of 2023).

Non-GAAP EPS: $7.65 for the full year (compared to $0.03 and $1.51 in the same period of 2023).

Key adjustment items: Business development transaction-related expenses (full-year impact of $1.28 per share), tax reserve release (full-year contribution of $0.21 per share).

2. Regional Market Performance

Key Market Dynamics

China: GARDASIL: Due to the suspension of shipments (starting February 2025), sales are expected to face pressure in 2025. Approved in January 2025 for HPV prevention in males aged 9-26, which may drive future growth.

United States: Strong demand for KEYTRUDA in indications such as bladder cancer and endometrial cancer supports core business growth.

Europe and Japan: WELIREG and Lynparza Gain New Indications, Accelerating Market Penetration.

3. R&D and Strategic Progress

1.Key Clinical Trial Results

KEYTRUDA Subcutaneous Injection: Phase 3 Trial Shows Non-Inferiority to Intravenous Injection, Potential to Enhance Patient Convenience.

WINREVAIR: Phase 3 ZENITH Trial Stopped Early Due to Significant Efficacy, Approved for High-Risk Pulmonary Arterial Hypertension Patients.

RSV Monoclonal Antibody Clesrovimab: FDA Accepts BLA Application, Expected Approval by June 2025, Targeting Infant RSV Prevention Market.

2.Strategic Cooperation and Pipeline Expansion

LaNova Collaboration: Acquires Global Rights to PD-1/VEGF Bispecific Antibody MK-2010, Strengthening Oncology Pipeline.

Hansoh Collaboration: Introducing Oral GLP-1 Receptor Agonist MK-4082, Expanding into the Metabolic Disease Field.

HIV New Drug DOR/ISL: Phase 3 Trial Completed, Single-Tablet Regimen or Simplified Treatment Option.

3.Regulatory Milestones

United States: Breakthrough Therapy Designation (Sac-TMT for EGFR-Mutant Lung Cancer).

Europe: CAPVAXIVE Pneumonia Vaccine Receives CHMP Recommendation for Approval.

4. Outlook for 2025

1.Financial Goals

Revenue: Estimated $64.1 billion to $65.6 billion (approximately 2% negative impact from exchange rates).

Non-GAAP EPS: $8.88-$9.03 (including a one-time milestone fee of $0.09 per share).

Profit Margin: Non-GAAP gross margin approximately 80.8%, with steady control of R&D and administrative expenses.

2.Risks and Challenges

China Market Volatility: GARDASIL Shipment Suspension May Impact Short-Term Revenue.

Exchange Rate Pressure: Strong US Dollar May Further Weigh on Overseas Revenue.

Pipeline Dependency: KEYTRUDA accounts for too high a proportion (46%), necessitating the acceleration of new drug commercialization to diversify risks.

3.Growth Drivers

WINREVAIR: Expansion of Pulmonary Arterial Hypertension Indications and Release of Long-term Efficacy Data.

RSV and HIV Pipeline: Clesrovimab and DOR/ISL Contribute to New Growth After Approval.

Animal Health: Acquisition of Elanco Aquaculture Business Drives Portfolio Diversification.

5. Conclusion

In 2024, Merck achieved steady growth driven by the continued strong performance of KEYTRUDA, the successful launch of WINREVAIR, and cost optimization. In 2025, the company needs to navigate market volatility in China and the risk of the patent cliff, while relying on subcutaneous KEYTRUDA, RSV monoclonal antibodies, and new drugs in the metabolic field to unlock growth potential. Strategic collaborations and pipeline diversification will be key to long-term competitiveness.

Brief Commentary

:Long-term competitiveness is considered by DeepSeek to be the key to MSD's development.

The field of oncology treatment has always been a fiercely competitive arena. Even GSK, which focuses on vaccines, achieved a 98% year-on-year sales growth in the oncology sector in 2024. GSK has also strengthened its ADC pipeline through BD deals. Pfizer has similarly excelled, with its oncology business revenue reaching $15.612 billion in 2024, marking a 25% year-on-year increase. The ADC drugs acquired from the $43 billion acquisition of Seagen in 2023 contributed over $3 billion in revenue in 2024.

Not only MNCs, but also local Biotechs hope to gain a share within the sphere of influence of K medicine.

With the success of K medicine, PD-1 has become a hot track. After years of domestic competition, products from several pharmaceutical companies such as Hengrui Medicine, BeiGene, Junshi Biosciences, and Innovent Biologics have been approved for marketing. Relying on price advantages and medical insurance coverage, these products will also erode part of the K medicine market.

In addition, China's Biotech is also accelerating innovation.

If Akeso's PD-1/VEGF bispecific antibody outperforms Keytruda in a head-to-head trial, it will become highly controversial. In January 2025, Innovent Biologics registered a Phase 2 clinical trial for its world-first PD-1/IL-2α-bias bispecific antibody fusion protein to be compared head-to-head with Keytruda. According to incomplete statistics, there are currently over 100 PD-1 multispecific antibodies and antibody fusion protein drugs under development globally.

More importantly, the patent for Keytruda will gradually expire starting from 2028, by which time the emergence of generic drugs will encroach on its market share. Currently, pharmaceutical companies such as Amgen and Sandoz are already gearing up to make significant moves. Amgen has registered a Phase 3 clinical trial for ABP 234, a biosimilar of Keytruda, on Clinicaltrials.gov, and will conduct a head-to-head comparison with Keytruda in non-small cell lung cancer.

With the upcoming expiration of Keytruda's patent and numerous competitors on the chase, how will Merck maintain its competitiveness in the coming years? At the 2025 JPM Conference, Merck disclosed some insights, as summarized by DeepSeek: pipeline diversification.

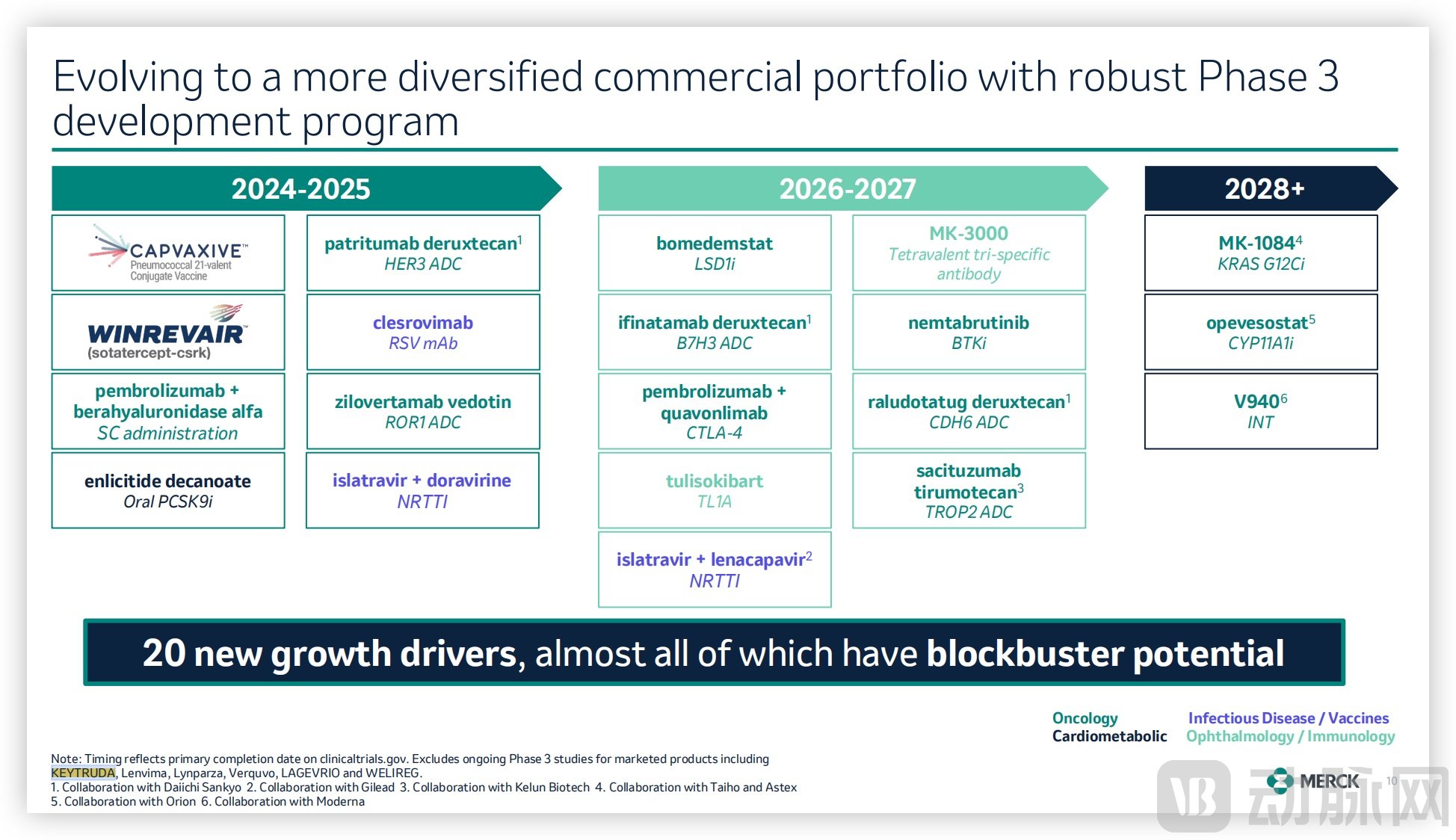

Product Layout of Merck for the Next Three Years, Source: Corporate Official Website

In simple terms, Merck has already started to lay out multiple directions, including HER3 ADC, ROR1 ADC, B7-H3 ADC, Trop2 ADC, and combination therapies with Keytruda. In November 2024, Merck also acquired the global license for LM-299, a PD-1/VEGF bispecific antibody under development by LaNova Medicines, for an upfront payment of $588 million and potential milestone payments of up to $2.7 billion. Additionally, Merck acquired Abceutics, an ADC rising star, for a potential consideration of $208 million.

The other side that DeepSeek didn't see is that, despite numerous competitors, Keytruda still has a deep moat, such as its continuously expanding indications. According to incomplete statistics, by the end of 2024, Keytruda has been approved for more than 40 indications in the United States, over 30 in Europe, and nearly 20 in China. It covers multiple cancer types, including non-small cell lung cancer, esophageal cancer, colorectal cancer, head and neck cancer, gastric cancer, liver cancer, and melanoma. In 2024, Keytruda maintained steady sales growth in the Chinese market, mainly due to its widespread application in several indications such as NSCLC.

At the same time, Merck & Co. has also increased its investment in Keytruda within the fields of combination therapies and early-stage cancer treatment, which can effectively consolidate its market position. Additionally, in November 2024, the successful Phase 3 clinical trial of Keytruda's subcutaneous formulation significantly reduced the average administration time, further boosting Keytruda's sales.

Despite the encircling competition, K drug's growth momentum will continue before its patent expires. However, against rivals outside the oncology field, K drug is powerless.

DeepSeek: Analysis of Novo Nordisk's 2024 Annual Report

1. Core Financial Performance

1.Sales and Profit

Total Sales: 290.403 billion Danish Kroner (DKK), a year-on-year increase of 25% (26% at constant exchange rates, CER), primarily driven by diabetes and obesity medications.

Operating Profit: 128.339 billion DKK, a year-on-year increase of 25% (CER 26%), with a stable gross margin of 84.7%.

Net Profit: 100.988 billion DKK, a year-on-year increase of 21%, with diluted earnings per share at 22.63 DKK (+22%).

Dividend: Total annual dividend of 11.40 DKK/share (including interim dividend of 3.50 DKK), a year-on-year increase of 21%, with a payout ratio of 50.2%.

2. Cost and Cash Flow

R&D expenses: 48.062 billion DKK (+48%), mainly used for late-stage clinical trials and early-stage research.

Free Cash Flow: -14.707 billion DKK, primarily due to the expenditure of 11.7 billion USD (approximately 82 billion DKK) on the acquisition of Catalent's production base.

Capital Expenditure: 47.164 billion DKK (+83%), for the expansion of Active Pharmaceutical Ingredients (API) and filling capacity.

2. Regional Market Performance

1.North American Market(Sales accounted for 61%)

Sales increased by 30% (CER 30%), reaching 178.172 billion DKK.

Core Drivers: GLP-1 Diabetes Drug (Ozempic® Grew 26%); Obesity Drug Wegovy® Sales Increased 86%, Accounting for 74% of Global Obesity Revenue.

Insulin sales grew by 52%, benefiting from channel and payer structure adjustments.

2. International Business(Sales accounted for 39%)

Sales increased by 19% (CER 19%), reaching DKK 112.231 billion.

Highlights: Obesity drug growth of 107% (Wegovy® newly entered 15 countries); GLP-1 drug sales in China increased by 19%, but rare disease business dropped by 30%.

3. Product Line Performance

Diabetes and Obesity: Total sales of 271.764 billion DKK (+27% CER), accounting for 94% of the company's revenue. GLP-1 drugs (Ozempic®, Rybelsus®) contributed 149.125 billion DKK (+22% CER). Obesity drugs (Wegovy®, Saxenda®) generated sales of 65.146 billion DKK (+57% CER).

Rare Diseases: Sales of 18.639 billion DKK (+9% CER), with rare endocrine disorders growing by 31%.

3. R&D and Strategic Progress

1. Core R&D Achievements

CagriSema (GLP-1/Amylin Dual Agonist): REDEFINE 1 Trial Shows 22.7% Weight Loss, Regulatory Submission Planned for 2026.

Semaglutide 7.2 mg: 20.7% weight loss in the STEP UP trial, outperforming existing doses.

Oral Semaglutide 25 mg (OASIS 4 Trial): 13.6% Weight Loss, Planned FDA Submission in 2025.

2.Strategic Acquisition

Catalent Production Base: Completion of Acquisition in December 2024 to Enhance Filling and Packaging Capacity, Addressing Supply Chain Bottlenecks.

3. Layout in Emerging Fields

Cardiovascular Disease: Initiation of GIP/GLP-1 Dual Agonist Phase 2 Trial for Chronic Kidney Disease;

Rare Disease: New Hemophilia Drug Alhemo® (Concizumab) Approved in Europe and the US.

4. Outlook and Challenges for 2025

1.Growth Expectations

Sales: Expected to grow 16-24% (CER), with an additional 3 percentage points higher when reported in Danish kroner.

Operating Profit: Expected to increase by 19-27% (CER), with reported growth in Danish kroner up by an additional 5 percentage points.

Capital Expenditure: Approximately 65 billion DKK, focusing on expanding API and injectable production capacity.

2.Core Driving Factors

GLP-1 Drug Demand Continues: Increased Market Penetration in Diabetes and Obesity, Enhanced Supply Capacity for Ozempic® and Wegovy®.

Emerging Market Expansion: Obesity Drugs Gradually Launched in China, Middle East and Other Regions.

3.Potential Risks

Supply Chain Pressure: Some products still face the risk of shortage and require continuous investment in production capacity.

Increased Competition: More Competitors in the GLP-1 Space (e.g., Lilly's Zepbound), Rising Price Pressure.

Exchange Rate Fluctuations: A Stronger US Dollar May Negatively Impact Profits Denominated in DKK.

5. Conclusion

Novo Nordisk Achieves Rapid Growth in 2024 Driven by Strong Demand for Diabetes and Obesity Drugs, with GLP-1 Drugs Remaining the Core Engine. In 2025, the Company Will Continue to Expand Production Capacity, Advance Pipeline Innovation, and Strengthen Its Production Advantages Through Strategic Acquisitions. Despite Supply Chain and Competitive Pressures, Its Leading Position in the Metabolic Disease Field Is Expected to Remain Solid.

Brief Comment:

DeepSeek believes that ensuring production capacity, semaglutide can continue to soar.

In 2024, Novo Nordisk made significant efforts to enhance its production capacity. These included acquiring Catalent, a leading CDMO, and gaining ownership of three of its plants located in Italy, the United States, and Belgium; investing 8.5 billion Danish kroner to establish a brand-new manufacturing facility in Odense, Denmark; and spending $4.1 billion to expand its manufacturing capacity in the U.S. Of course, Novo Nordisk's competitors are doing the same—Lilly invested an additional $5.3 billion in 2024 to expand the capacity of its manufacturing base in Indiana.

Notably, the Chinese market is expected to become a battleground for head-to-head competition between the two giants in the future.

In early January 2025, Eli Lilly announced the official launch of tirzepatide in China, including its weight loss indication. Around the same time, Novo Nordisk announced the official launch of oral semaglutide in China. Compared to injections, oral administration significantly enhances patient experience and effectively boosts product sales.

By the end of January 2025, the U.S. government announced that Novo Nordisk's weight-loss drug Wegovy and diabetes drug Ozempic, among 15 other drugs, have been included in the Medicare drug negotiation list. This means that the self-paid weight-loss drug market in China has become particularly important for these two companies.

To this end, both companies have increased their production capacity in China. For instance, Novo Nordisk invested approximately 4 billion RMB in Tianjin for the expansion of its sterile formulation project, while Eli Lilly invested about 1.5 billion RMB to upgrade the production capacity of its Suzhou plant, aiming to expand the production scale of innovative drugs for type 2 diabetes and obesity.

In addition, as the core patent of Semaglutide in China is set to expire in March 2026, a large number of domestically produced GLP-1 products are waiting to enter the market. According to incomplete statistics, there are currently more than 20 similar products in China that have entered the clinical stage. Companies such as Jiuyuan Gene, Livzon Group, United Laboratories, and Qilu Pharmaceutical have already submitted their applications for market approval.

Like K drug, semaglutide is also continuously expanding its indications. Currently, there are over a hundred clinical trials of semaglutide underway, including complications from diabetes and obesity, cardiovascular diseases, as well as chronic kidney disease, heart failure, non-alcoholic steatohepatitis, and cardiovascular diseases. Semaglutide is even broadening its indications to include Alzheimer's disease (Phase 3 clinical trials), ischemic stroke, Parkinson's disease, polycystic ovary syndrome, and peripheral artery disease.

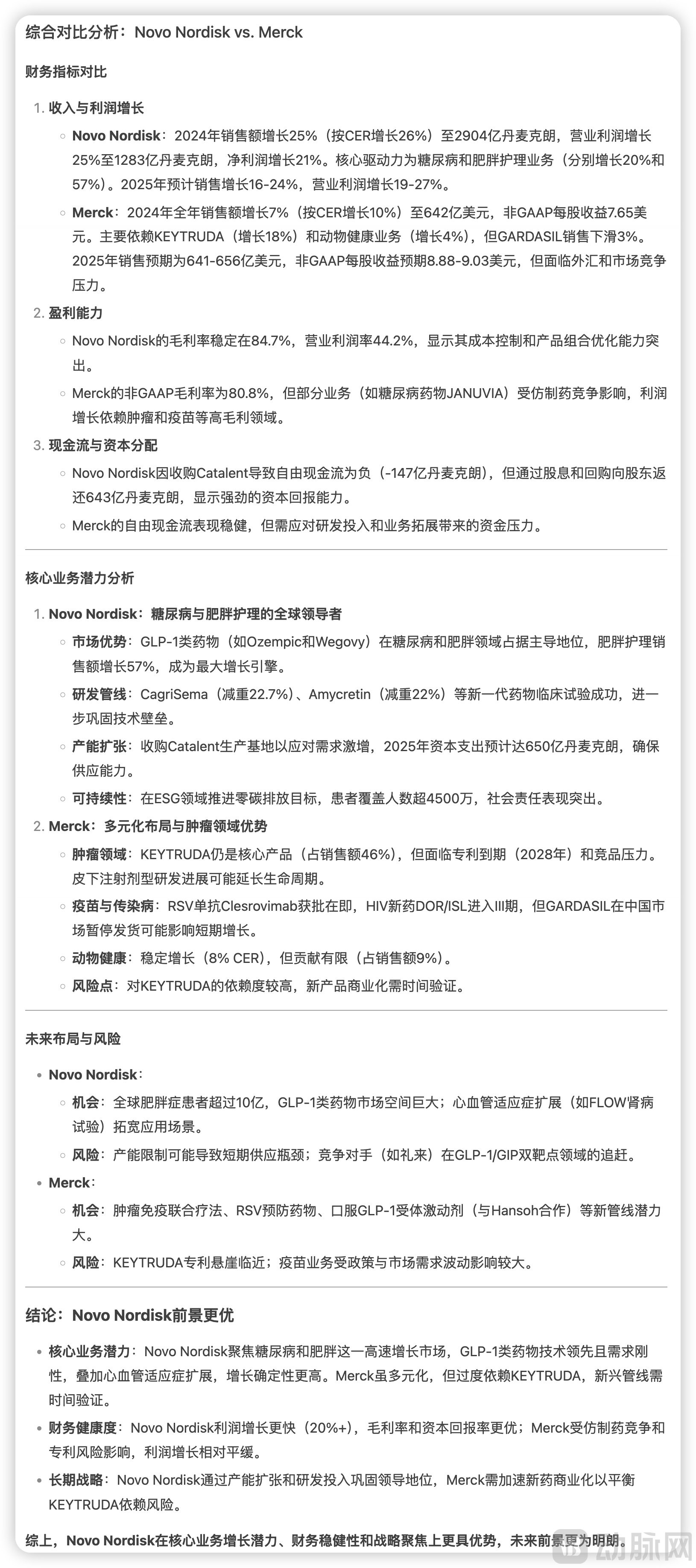

Deepseek Comparison of Merck and Novo Nordisk, Image Source: Deepseek

Overall, before the patent expiration, the competition in the GLP-1 field is still mainly between Novo Nordisk and Eli Lilly. It is precisely because of Eli Lilly's lagging behind that semaglutide has a great chance to ascend to the top as the "king of drugs" by 2025. After analyzing the annual reports of Novo Nordisk and Merck, DeepSeek concluded that Novo Nordisk has better prospects based on operating indicators, core business potential, and future strategies and risks. As for how things will actually develop, let us wait and see.