Recently, a global leading medical technology company with a market value of 149.5 billion US dollarsStryker (NYSE: SYK) Announces Completion of Large-Scale Debt Offering,Raised a total of 3 billion US dollars (approximately 21.9 billion RMB)。

According to InvestingPro data, the company has a moderate level of debt and a financial health rating of "very good," indicating that this new issuance has strong financial "appeal." Completed on Monday, the issuance includes four series of bonds with maturities ranging from 2027 to 2035 and interest rates between 4.550% and 5.200%.

Stryker's Strategic "Puzzle" of Large-scale Fundraising

Mention this, why does Stryker raise funds in a big way? According to foreign media reports,This financial move is part of Stryker's strategy to fund the upcoming acquisition of Inari Medical (TASE: PMCN). Right at the start of 2025, Stryker publicly announced its plan to acquire Inari Medical for $4.9 billion.

This transaction also becameThe First "Bomb" in the 2025 Medical Device M&A Field。

On January 7, Stryker, the world's second-largest orthopedic device manufacturer and fifth-largest medical device supplier, announced that it would acquire Inari Medical, an innovative company based in Irvine, California, focused on treatment solutions for venous diseases. The boards of both companies have unanimously approved the transaction, which is expected to be completed by the end of the first quarter of 2025.

For Stryker, this acquisition represents a significant enhancement to its neurovascular business, which focuses on developing products and technologies for vascular access, embolization, thrombectomy, angioplasty, and stent placement.

Why Choose Inari Medical?

Since its founding in Irvine, California in 2011, Inari Medical has quickly risen to become one of the most notable companies in the medical technology field and has been listed multiple times as one of the most attractive medtech acquisition targets.

Inari's product portfolio is highly complementary to Stryker's neurovascular business, including mechanical thrombectomy solutions for peripheral vascular diseases such as deep vein thrombosis and pulmonary embolism.

An analyst analyzed that this deal was not surprising because Stryker's management had discussed that peripheral vasculars were a potential area of interest.

Bright Earnings Report, Bonds Attract Significant Investment

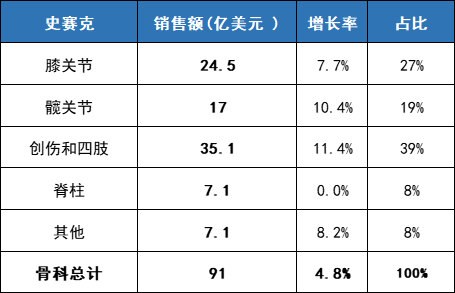

Stryker's completion of this large-scale bond issuance is inseparable from its excellent financial performance. It is reported that its full-year sales for 2024 were $22.6 billion, increasing by 10.23% compared to the previous year, while maintaining dividend payments for 35 consecutive years. Net income was $3 billion. Among this, orthopedic business sales reached $9.1 billion, accounting for 40%.

In orthopedic products, trauma and extremities account for the largest share, reaching $3.5 billion, which is close to 40% of the orthopedic business, with a growth rate exceeding 11%. Knee and hip joints also achieved steady growth.

CEO Lobo stated, "We have once again achieved double-digit organic sales growth for the year, while continuing to expand our adjusted operating margin and driving growth in adjusted earnings per share."

He also stated that over the past year, Stryker has launched many products and actively participated in mergers and acquisitions to further enhance its position in high-growth end markets.

However, this bond issuance also has preconditions. If the acquisition is not completed before the specified date or the merger agreement is terminated early, Stryker is obligated to redeem the 2030 and 2035 notes at a premium. It is understood that the proceeds from the 2030 and 2035 notes, along with other available funds, will be exclusively used for the tender offer related to the acquisition of Inari Medical and associated costs.

The proceeds from the 2027 and 2028 notes will be used for general corporate purposes, which may include repaying, redeeming, or refinancing other debt.

Mergers and Divestitures,

Will Still Be the Main Theme in the Medical Device Field in 2025

With the continuous advancement of medical technology and changes in market demand, the global orthopedic medical market is undergoing a profound transformation. Stryker has not been "spared" either, and needs to adopt a series of strategies such as mergers and acquisitions or selling businesses to always keep itself in a favorable position.

On January 28,Stryker Announces Signing of Final Agreement to Sell Its U.S. Spine Implants Business to Family Investment Firm Viscogliosi Brothers, the family investment company Viscogliosi Brothers taking over Stryker's U.S. spinal implant business is undoubtedly a bold strategic investment.Stryker has a relatively small market share in the U.S. spinal fusion market, approximately 9.1%, and its growth has been relatively slow since entering the market, while the shares of major manufacturers such as Medtronic and Globus Medical are about 37.5% and 23.9%, respectively.

GlobalData healthcare analyst Aidan Robertson commented: "Given Stryker's performance in the market, the decision to sell seems to be a logical next step, which could benefit the company in the long run as it continues to focus on interventional spine products. Although Stryker does not hold a large market share, its competitors are expected to seize this opportunity to expand their influence over the market share previously held by Stryker, which may pose challenges for the future development of VB Spine."

And before that,Stryker has always been known as the "King of M&A" with a high-profile and aggressive approach.。

Only in 2024,Stryker has conducted 7 acquisitions, covering areas such as joint replacement, foot and ankle care, soft tissue fixation techniques, breast cancer surgical care, AI virtual care, operating room ecosystem optimization, and minimally invasive neurotechnology solutions.

These acquisitions, although not large in scale, are of great significance to Stryker's business. They not only expand Stryker's product lines but also strengthen its presence in emerging technology fields.

It is not difficult to see that Stryker's series of measures are undoubtedly a vivid reflection of its adaptation to market adjustments and changes. Selling off its U.S. spinal implant business to optimize resource allocation, actively pursuing acquisitions, venturing into multiple emerging fields, expanding product lines, and strengthening the layout of emerging technologies.

Meanwhile, foreign media analysis suggests that mergers and acquisitions and spin-offs may still be the main theme in the medical device sector in 2025. In the first month of the year, several major companies have already made significant moves in mergers and acquisitions as well as business separations.

On January 28, Zimmer Biomet announced that it had reached a definitive agreement with Paragon 28, Inc. to acquire all outstanding common shares of Paragon 28 for $13.00 per share in cash upfront, representing an equity value of approximately $1.1 billion and an enterprise value of approximately $1.2 billion (approximately RMB 8.7 billion).

On January 30, GetingeIndicates,It will gradually phase out its surgical perfusion business and reallocate resources to higher-growth areas such as Extracorporeal Membrane Oxygenation (ECMO) and transplant care. Getinge CEO Mattias Perjos stated that surgical perfusion has been a struggling category since 2015, when the FDA consent decree forced the company to withdraw from the U.S. market by halting the production of certain devices.

On February 3, Reuters reported that Becton Dickinson, the leader in the U.S. medical device industry, is steadily preparing to spin off its highly valuable life sciences division, which is estimated to be worth approximately $30 billion.

On February 7, Globus Medical (NYSE: GMED), the global leader in orthopedic surgical robotics, announced the acquisition of all shares of chronic pain treatment company Nevro (NYSE: NVRO) at $5.85 per share, with a total equity value of $250 million (approximately 1.82 billion yuan).From Stryker's business adjustments, toZimmer Biomet, Getinge, BD Medical, Globus MedicalIndustry giants' mergers, acquisitions, and business changes by early 2025,This deeply reflects that the global medical device field is in an unprecedented wave of transformation.

In order to keep moving forward in this highly competitive and complex market, they have to acquire new technologies and businesses through mergers and acquisitions, or spin off underperforming business units to concentrate resources and optimize strategic layouts.

In the future, driven by both continuous innovation in medical technology and dynamic market changes, industry giants will face even more uncertainties. Only by constantly adapting to change and daring to achieve innovative breakthroughs can they establish a firm foothold in this challenging field and continue to write a new chapter in the industry’s development.

Nowadays, the development wave of China's medical device innovation companies is surging, and mergers and acquisitions (M&A) have become one of the best ways for companies to "reach the shore." However, how companies can accurately position themselves to find high-quality M&A targets, and how to ensure the smooth progress of the M&A process, have become pressing challenges. As a professional service platform in the industry, the Medical Device Innovation Network, relying on strong resources and a professional team, can provide companies with full-chain M&A service support.

For more details, please contact: Xiao Xin 18136127515

▲ Source of the article: Medical Device Innovation Network▲Please indicate the above source for reprint.Disclaimer: This article is intended solely for the purpose of information transmission and is for reference only. It does not constitute any advice on investment or treatment; please carefully verify. If it involves issues related to the content, copyright, or other aspects of the work, to protect the rights and interests of both parties, please contact us and we will handle it immediately. If this article is reprinted by other platforms, they must take responsibility for the content themselves. The Medical Device Innovation Network is not responsible for any secondary dissemination caused by reprints.