Recently, many medical technology companies have released their fourth-quarter and full-year financial reports, among which two updates are worth noting.

First,Becton, Dickinson and Company (BD)Announced a strategic decision,To spin off its biosciences and diagnostics units from the company’s operations.The department will become an independent company or be sold to another company. The purpose of doing so may be to focus on core business, improve operational efficiency, or release value for shareholders.SecondlyZimmer BiometAnnouncementAcquisition of Paragon 28 for $1.1 billionThisIs aA company specializing in orthopedic medical devices, this acquisition helps to expand Zimmer Biomet's product line, strengthen its competitiveness in the orthopedic field, and may achieve growth through the integration of resources and market channels.At the same time,Globus MedicalAlso announcedPlan to acquire spinal cord stimulation company Nevro for approximately $250 million.According to analysts, the leading enterprises in the medical technology fieldJohnson & Johnson, Abbott, Boston Scientific, Stryker, and Intuitive SurgicalRobust performance was reported this quarter.Apart from BD Medical and Zimmer Biomet, many other companies have made similar key decisions. Siyu has compiled them as follows for readers' reference.- Divest Life Sciences Business to Increase Investment in Medical Technology Field

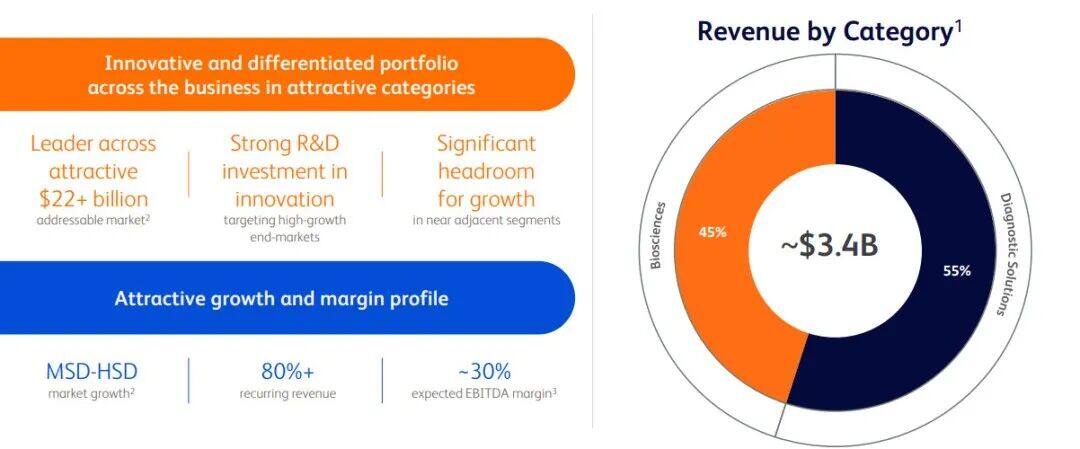

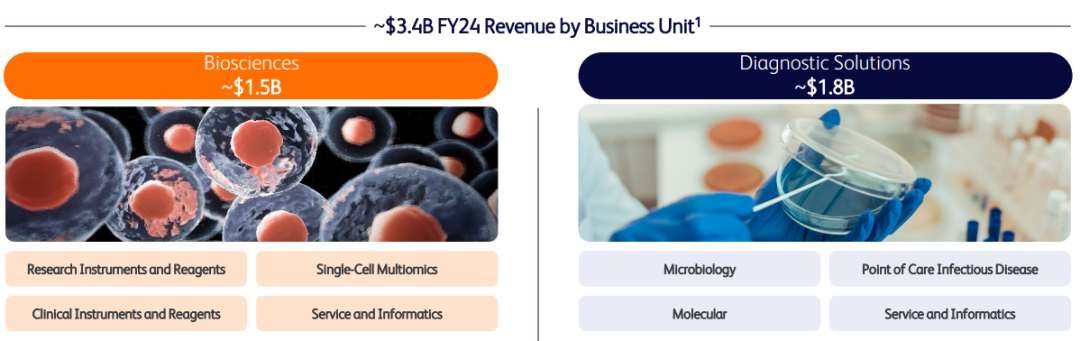

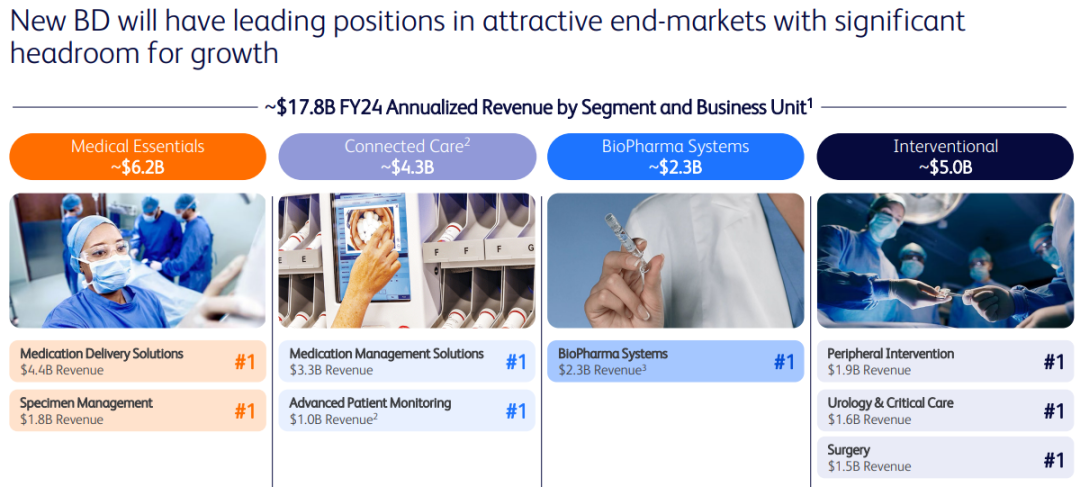

Company CEO Tom Polen stated that BD will "double down on shifting our portfolio towards higher growth, higher margin value-added areas through organic growth and tuck-in M&A."BD outlined the financial performance of its separation business and remaining business in its earnings report. In BD's fiscal year 2024,Biological Science and Diagnostics BusinessCreated$3.4 billionIncome. Among them, the diagnostic business sold products such as rapid infectious disease tests, contributing to$1.8 BillionIncome.Medical technology business has created$17.8 billionThe income. Medical products and interventional treatments are the two main businesses of the department, contributing approximately$6.2 billionAnd$5 billionIncome.Analysts have presented their expectations for how BD will develop its medical technology business after spinning off its bioscience and diagnostics operations. "We hope to see management build on this to drive business growth. For example,Expand into some high-growth supply markets, orLeverage existing cardiac or urology platforms,Add some early-stage or small-scale innovative growth assets。”- Acquisition of Nevro for $250 Million

Globus Medical Announces Plan to Acquire Spinal Stimulation Company Nevro for Approximately $250 Million. Globus will complete the acquisition through an all-cash transaction at $5.85 per share, which represents a 27% premium over Nevro's volume-weighted average price in the past 90 days.Nevro sells spinal cord stimulation devices for the treatment of back pain and diabetic painful neuropathy. After acquiring Vyrsa Technologies in 2023, the company also provides sacroiliac joint fusion devices for the treatment of lower back pain.BTIG analyst Ryan Zimmerman wrote in a research report,This acquisition may come as a surprise to investors, as Globus Medical just acquired NuVasive for $3.1 billion in 2023.But Nevro's valuation is "lower," and the cash amount paid by Globus is relatively small, so this acquisition can be seen as a very low-risk investment. However, Nevro's spinal cord stimulation business can benefit from Globus Medical's scale and position in the orthopedics field.- Acquisition of Paragon 28 Highlights Opportunities in Ambulatory Surgery Centers (ASC)

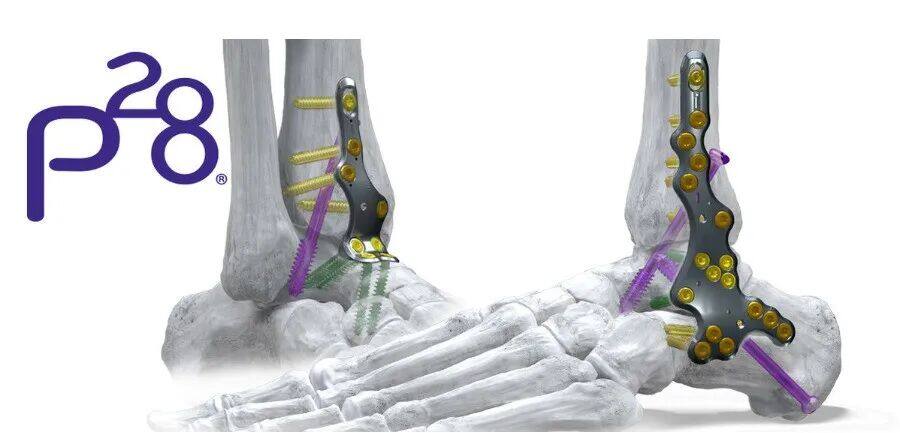

Zimmer Biomet's Q4 2024 sales were $2.02 billion, with a net income of $239.4 million; annual sales reached $7.68 billion, with a net income of$903.8 million. At the same time,CompanyAnnouncement Passed$1.1 billionAcquisition of Paragon 28.Paragon 28 is a company focused on orthopedic medical devices, dedicated to providing innovative solutions for foot and ankle surgeons. The company specializes in developing and producing medical devices for the treatment of foot and ankle diseases and injuries, including implants, surgical tools, and related accessories.Zimmer Biomet CFO Suky Upadhyay told investors that, combined with Paragon 28's business, the company’s sports medicine, extremities, and trauma division will grow in scale.Exceeding $2 billionThe hip joint business, and the growth rate will exceed its hip and knee departments.Upadhyay added that the acquisition is expected to immediately drive revenue growth but could dilute adjusted earnings per share by approximately this year.3%。Zimmer Biomet CEO Ivan Tornos said that this acquisition will provide more opportunities for Ambulatory Surgery Centers (ASCs), "In ASCs, reimbursement for foot and ankle surgeries is more common, and we are currently not fully taking advantage of this opportunity."As more surgeries performed in ASCs are increasingly covered by insurance, orthopedic companies have regarded ASCs as a key to future growth. Zimmer Biomet predicts that within the next three to five years,40%-60%Orthopedic surgeries will be transferred to ASCs. Tornos stated that currently, nearly20%From ASCs.- PFA Products Perform Well and Will Continue to Expand Indications

Boston Scientific's sales in the fourth quarter of 2024 were $4.56 billion, with annual sales of $16.75 billion. Sales from its electrophysiology business in the fourth quarter were$649 million, with total annual sales of$1.9 billion, respectively increasing by nearly171%And138%。The rapid growth of the electrophysiology business is mainly attributed to Farapulse, a technology that is transforming traditional ablation procedures into pulsed field ablation (PFA) procedures.Boston Scientific hopes to expand the indications for Farapulse to include patients with persistent atrial fibrillation (AFib), whose irregular heart rhythms last more than seven days and who do not respond well to medication. The company stated that persistent AFib accounts for approximately 25% of all AFib cases. The company anticipates that the indication expansion will be completed by the end of this year.- 23andMe Considers Sale Due to Insufficient Cash Reserves

This genetic testing company had a cash reserve of $79.4 million at the end of last year and has told investors it needs to raise funds to support its operations and financial commitments.CEO Anne Wojcicki attempted to take the company private last year, but the board rejected the proposal. Independent directors subsequently resigned, citing disagreements with Anne Wojcicki over the company's future direction. The company also recently laid off more than 200 employees through restructuring, terminating its therapeutics division and the development of all therapeutic programs.23andMe gained fame by selling consumer DNA testing services and established a genetic information database. These tests provide customers with information about their ancestry and health traits, enabling 23andMe to study the connections between genes and human diseases.The U.S. FDA issued a warning letter in 2013 regarding health claims in 23andMe's DNA testing, but the company...In 2017, received the first authorization for 10 genetic health risk tests.. The valuation of 23andMe at its IPO in 2021 was$3.5 billion。According to Yahoo Finance, as of last Wednesday, 23andMe's market value was close to$92 million。Due to growing concerns about the company's finances, its stock price has fallen from a year ago.$14.86Dropped to approximately$3.39As of the end of September, 23andMe's cumulative deficit was$2.3 billion。At the time, the company warned that it lacked sufficient funds to sustain operations for the next 12 months. In the following three months, 23andMe's cash reservesReduced by approximately 47 million US dollars, leading to its year-end cash reservesReduced to less than 80 million US dollars.Despite the company's confirmation ofPharmaceutical company GSKIn the transaction$19.3 millionResearch service revenue, but its cash reserves are still declining.As cash reserves dwindle, the board has begun seeking deals.Opportunity.Overall, 23andMe is facing severe financial pressure and is responding to the crisis by laying off staff, terminating projects, and seeking a sale, but itsGene database and listing status may still become key assets to attract potential buyers.- Quarterly Report Released, Spinal Implant Business Sold

Stryker's Q4 2024 Revenue Reaches $6.4 BillionIn USD, the net income was 546 million USD; the total revenue for 2024 was 22.6 billion USD, with an annual net profit of 2.99 billion USD.Stryker's spine implant business achieved sales of $707 million and reported $818 million in goodwill and other impairment losses related to the spine business in the fourth quarter.

In addition, on February 19, 2025, StrykerAnnounced the completion of the previously announced acquisition of Inari Medical. The company announced last month that it had reached an agreement,In$80 per shareCash AcquisitionInari Medical, with a total transaction value of approximately$4.9 billion(Contract 36 billion RMB)。

Stryker and Family Investment CompanyViscogliosi BrothersReach an agreement to sell its U.S. spinal implant business for an undisclosed amount.The newly established company will be named VB Spine, focusing on neuromusculoskeletal products.

The agreement also includes a binding proposal to acquire Stryker's spinal products in France. Stryker CEO Kevin Lobo told investors that the business has been difficult to meet the company’s expectations.Stryker stated that it remains interested in interventional spine products, including its Q Navigation System for surgical planning and navigation.And the Mako Spine Robot. Stryker received FDA approval for the Mako Spine Robot in August 2024.

VB Spine to Gain Exclusive Rights to Mako Spine Robot and Copilot for Use with VB Spine Implants in Spinal Surgeries. Copilot is a feature that assists with screw placement during surgery and automatically stops when the predetermined depth is reached. Additionally, Stryker plans to sell its spinal implant business in other international markets.

# Getinge

Getinge Announces Gradual Exit from Surgical Perfusion Business to Redirect Resources to Faster-Growing Areas such as Extracorporeal Membrane Oxygenation (ECMO) and Transplant Care

Analysts from Needham and Stifel viewed this news asLivanovaBenefitsGetinge's business value in this field in 2024 is approximately450 million Swedish kronor (approximately 41 million US dollars)Getinge's exit from the surgical perfusion market provides LivaNova with an opportunity to capture market share and increase sales.CEO Mattias Perjos said on the earnings call that the business has been unsustainable since a consent decree forced Getinge to exit the U.S. surgical perfusion market in 2015.。Getinge signed a consent decree with the U.S. FDA in 2015, agreeing to temporarily suspend the production of certain devices at a factory in New Hampshire while working to strengthen its quality management system.Ten years have passed, this SwedishMedical technology companies have yet to reintroduce these devices to the U.S. market. According to data from Getinge, its market share outside the United States has dropped from 15% in 2018 to 7% in 2023.

As the company exits the market, CEO Mattias Perjos expects surgical perfusion sales to drop to approximately $27 million by 2025. The company highlighted extracorporeal life support (ECLS), another term for ECMO-provided support, as the driver behind acute care therapies, which saw nearly 12% year-over-year growth in the fourth quarter.

# Intuitive Medical

Revenue in the fourth quarter of 2024 was $2.41 billion, and revenue in 2024 was$8.35 billion, Net Income$2.32 billionYuanIntuitive MedicalCompany executives said,Evaluating the impact of potential tariffs that may be imposed by the Trump administration on its business, as well as the possible countermeasures the company might adopt.

The U.S. President has stated,Impose a 10% Tariff on Imports from ChinaAnd impose a 25% tariff on goods from Mexico and Canada.

However, Intuitive Medical did not include the new tariff in its 2025 profit margin forecast. The company expects this year's non-GAAPThe gross margin will be between 67% and 68% of net revenue.Below 69.1% in 2024.

# Abbott

Sales in the fourth quarter of 2024 were $10.97 billion, an increase of 7.2%; sales in 2024 were$42 billion,Increased by 4.6%, net income reached$13.4 billion。

The company's electrophysiology department achieved sales of $2.47 billion in 2024, representing a year-on-year increase of 12.3%.AbbottCEO of the company Robert Ford "High single-digit" growth is expected in 2025.

Robert Ford told investors,Expected to launch its first pulsed field ablation (PFA) device outside the United States in 2025.Abbott expects to obtain the CE mark in the first half of 2025 and FDA approval in 2026, according to a company spokesperson.

# Johnson & Johnson

Johnson & Johnson Medical Technology Business Fourth Quarter Sales Were $8.19 Billion, A Year-Over-Year Increase Of 6.7%; 2024 Sales Were$31.86 billion, an increase of 4.8%; Sales brought by Abiomed in 2024 reached$1.5 billion, an increase of 14.5%.

A Johnson & Johnson Medical Technology executive said,The company is currently collaborating with the U.S. FDA on the safety risks of its Varipulse pulsed field ablation device.Following the success of Johnson & Johnson's cardiovascular product portfolio, PFA encountered setbacks. The acquisition related to this business exceeded $30 billion and was realized in 2024.$7.71 billionRevenue, year-on-year growth21.4%。

The combined sales of Abiomed and Shockwave Medical, the two acquired companies, last yearMore than 2 billion USYuan,Among whichShockwave contributed$564 millionIncome.Tim Schmid, Global Chairman of J&J's MedTech, believes that Johnson & Johnson is strengthening its competitiveness in the cardiovascular medical field by acquiring companies such as Abiomed and Shockwave Medical. He is confident that these businesses will bring long-term strategic value and financial returns to Johnson & Johnson.

# Conclusion

As major medical companies continue to expand their presence in technology, market, and product portfolios, the industry landscape is set to undergo profound changes in the coming years. Despite market volatility and cost pressures, companies that can accurately grasp market trends, enhance product innovation, and strengthen mergers and acquisitions will stand out in this industry reshuffle, becoming core forces leading future development. Siyu will continue to monitor the situation.