Gilead's $4.3 Billion Bet Pays Off: Seladelpar (Livdelzi) Approved for Primary Biliary Cholangitis

Cymabay Therapeutics

Drug Developer

Gilead Sciences

Antiviral Drug Developer

"Love to 'Gamble' Will Win."

This is perhaps a principle that every MNC has endorsed and practiced. Especially in recent years, with the rapid changes in fields such as cell and gene therapy, ADC, and drug delivery technology, the number of MNCs entering new fields through mergers and acquisitions has been increasing year by year. Looking at the major M&A cases in 2024, the technology has already completed its iteration.

For Gilead, which has long been known for its "high-stakes gambles," 2024 has not been a smooth year, with the repercussions of such gambles hitting back hard: At the end of May 2024, Gilead announced that its TROPiCS-04 study failed to meet its primary endpoint, marking another setback for Trodelvy in urothelial cancer. More regrettably, the goal of the TROPiCS-04 study was to secure full approval, and this failure means that Gilead’s Trodelvy for the treatment of urothelial cancer could face withdrawal from the market. Not only that, but earlier, Trodelvy’s Phase III clinical trial for non-small cell lung cancer also ended in failure.

The two drugs mentioned above were acquired by Gilead Sciences through the $21 billion acquisition of Immunomedics and the $4.9 billion acquisition of Forty Seven, respectively.

By March 2025, a turning point has arrived. Gilead Sciences'重磅新药Seladelpar (brand name: Livdelzi) has received conditional approval from the European Commission (EC) for marketing, indicated for the treatment of primary biliary cholangitis (PBC), marking a significant breakthrough in the field of PBC treatment.

One year ago, Gilead Sciences reached a definitive agreement with CymaBay Therapeutics (hereinafter referred to as CymaBay) to acquire CymaBay for $32.5 per share in cash, with a total equity value of approximately $4.3 billion.

CymaBay's main candidate product is Seladelpar, which was at the time in the pivotal Phase III RESPONSE study. The data showed that the Seladelpar treatment group achieved superior results compared to the placebo group in key secondary endpoints, including the primary composite endpoint of biochemical response (61.7% in the Seladelpar group vs. 20.0% in the placebo group, p<0.0001) and normalization of alkaline phosphatase at 12 months (25.0% in the Seladelpar group vs. 0% in the placebo group, p<0.0001). Additionally, for patients with moderate to severe pruritus lasting 12 months, significant improvement in pruritus symptoms was observed after six months of Seladelpar treatment.

PBC, previously known as primary biliary cirrhosis, is characterized by T lymphocyte-mediated attacks on small bile ducts within the liver lobules. Continuous attacks on bile duct epithelial cells lead to gradual destruction and eventual disappearance of the bile ducts. Persistent loss of bile ducts within the liver lobules causes symptoms and signs of cholestasis, potentially leading to cirrhosis and liver failure. The terminology for this disease changed from "primary biliary cirrhosis" to "primary biliary cholangitis" to more accurately describe the condition and its natural course. With the advent of ursodeoxycholic acid (UDCA) treatment, most patients now have a normal life expectancy, with only a small number progressing to cirrhosis.

Seladelpar is considered the first and only therapy to show statistically significant improvements over placebo in ALP normalization, key biomarkers, and pruritus.

Therefore, Seladelpar's unique mechanism of action and significant clinical efficacy make it a promising candidate to become one of the first-choice drugs for PBC treatment. Statistics show that 90%-95% of PBC patients are female, and the majority are diagnosed between the ages of 30 and 65. The global PBC treatment market size was $526 million in 2017 and is expected to grow to $8.593 billion by 2026.

In other words, Gilead, transitioning from a high-risk gambler to a prudent investor, has won a victory at the start of 2025.

Starting from the Snake Swallowing the Elephant

The venture capital background of Gilead founder Michael L. Riordan laid the groundwork for the company's risk-taking nature, making each key milestone in Gilead's development famous for its "high-stakes gambles."

For him, the first big gamble was Gilead's determination to innovate in drug development. As is well known, engaging in innovative drug development is itself a high-risk investment with high costs and long cycles. At that time, Gilead had just been established, and he was only 29 years old. However, it turned out that O'Day's gamble was highly successful, as the first drug went from research and development to market with only $93.3 million. Moreover, at that time, O'Day almost entirely bet the company’s future on HIV treatment.

However, when it comes to major mergers and acquisitions, it was in 1999 that Gilead Sciences acquired NeXstar Pharmaceuticals (hereinafter referred to as NeXstar) for $550 million. NeXstar's revenue was three times that of Gilead, while Gilead's total assets at the time were only $1 billion. This "snake swallowing an elephant" acquisition brought Gilead two liposome products, AmBisome and DaunoXome, enabling the company to achieve revenue of $169 million the following year, breaking the $100 million mark for the first time. This acquisition not only helped Gilead transform from a company reliant on outsourced project income into a genuine pharmaceutical enterprise but also laid the foundation for its subsequent development.

In 2003, Gilead Sciences acquired Triangle Pharmaceuticals for $464 million. This deal nearly exhausted all of Gilead's revenue from the previous three years. Through this acquisition, Gilead obtained the key ingredient emtricitabine for anti-AIDS drugs, establishing its leading position in the HIV treatment field. Emtricitabine became one of the core components of Gilead’s subsequent “cash cow,” Truvada. The launch of Truvada solidified Gilead's dominant position in the anti-AIDS field.

In 2011, Gilead Sciences acquired Pharmasset for $11 billion. At the time, Pharmasset had only 82 employees and was operating at a loss. Undoubtedly, the $11 billion price tag made this deal a widely acknowledged "high-stakes gamble." However, the acquisition brought Gilead drugs such as Sofosbuvir (Sovaldi) and Ledipasvir/Sofosbuvir (Harvoni) for the treatment of hepatitis C. The launch of Sovaldi and Harvoni completely transformed the landscape of hepatitis C treatment, quickly becoming "blockbuster" drugs and generating hundreds of billions of dollars in returns for Gilead.

Subsequent mergers and acquisitions were carried out at the level of tens of billions of dollars.

In 2017, Gilead Sciences acquired Kite Pharma for $11.9 billion, marking the company's official entry into the field of cancer treatment. Through this acquisition, Gilead obtained the CAR-T cell therapies Yescarta and Tecartus.

Gilead Sciences' Major Acquisition, Chart Prepared by VCBeat

At this point, the revenue concerns of Gilead Sciences have become apparent. The company's performance growth has been driven by its revolutionary yet expensive hepatitis C drugs. However, with a decrease in the number of patients and intensifying competition, revenue has started to decline. Gilead’s hepatitis C drugs—Sovaldi, Harvoni, and Epclusa—generated a total revenue of $2.9 billion in the second quarter of 2017, down from $4 billion during the same period in 2016.

The reason is simple: Gilead Sciences has successively launched four generations of drugs in the hepatitis C field, raising the cure rate for hepatitis C to nearly 100%. With the explosive growth in the hepatitis C sector, the company's highest annual revenue reached $30.4 billion, securing its place among the top ten global pharmaceutical enterprises. However, due to the high cure rate, by 2019, the hepatitis C market had shrunk to half of its size in 2015.

Against this backdrop, turning attention to CAR-T therapy is an inevitable move.

Subsequently, in 2020, Gilead Sciences acquired Immunomedics for $21 billion, obtaining the Trop2 ADC drug Trodelvy. In the same year, Gilead Sciences spent $4.9 billion to acquire Forty Seven, focusing on the CD47-targeted drug Magrolimab. However, the clinical trial of this drug was terminated due to safety concerns.

Gambler Hits a Wall

The blow focused on the outbreak in 2024.

By the end of 2024, Gilead Sciences had ventured into various technological pathways such as ADC, monoclonal antibodies, bispecific antibodies, and CAR-T. However, the revenue from the oncology sector in 2024 was far behind that of the antiviral sector, especially the HIV business, which accounted for nearly 70% of the total revenue.

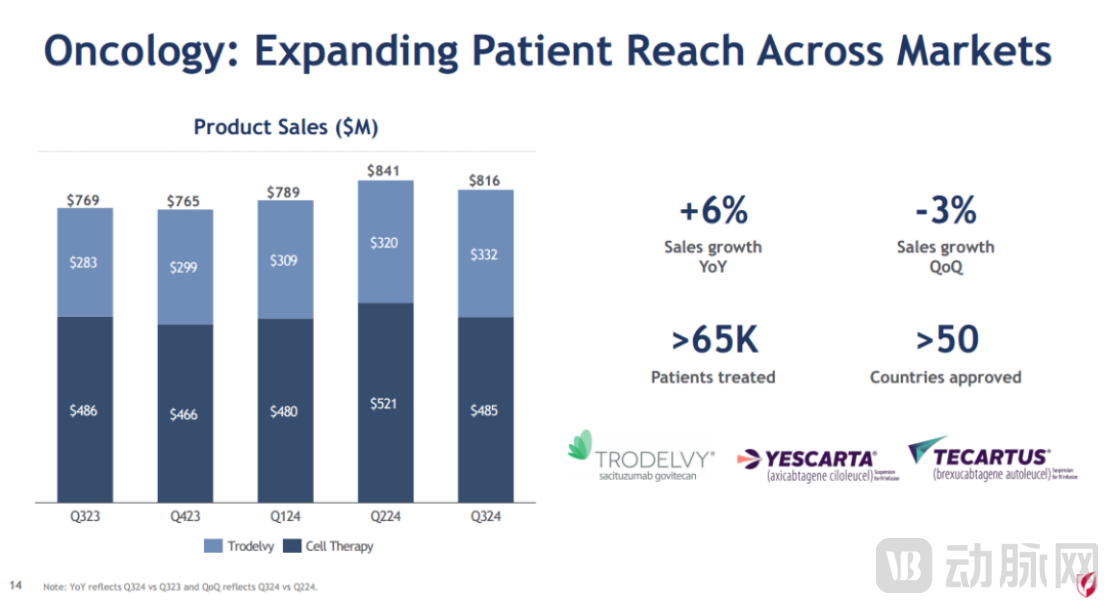

On November 6, 2024, Gilead Sciences announced its Q3 financial report for 2024. The Q3 revenue was $7.515 billion, a year-on-year increase of 7%. The oncology segment generated $816 million in revenue, marking a year-on-year growth of 6%, but a nearly 3% decrease quarter-on-quarter.

When the oncology sector has yet to meet expectations, Gilead Sciences' three main products are already showing signs of fatigue. According to financial reports, the total sales of Gilead's CAR-T cell therapies in 2024 amounted to $1.973 billion. Among them, Yescarta generated $1.570 billion in sales, a year-on-year increase of 5%; CD19 CAR-T therapy Tecartus achieved $403 million in sales, marking a year-on-year increase of 9%.

In contrast, BMS's CD19 CAR-T therapy Breyanzi was launched a year later than Tecartus. In 2024, its sales grew to $747 million, a year-on-year increase of 105%, effectively doubling.

As for Trodelvy, its sales once reached $1.065 billion in 2023, but subsequently, sales growth slowed down due to clinical trial issues and market competition.

In May 2024, Gilead Sciences announced that Trodelvy failed to meet the expected goals in the TROPiCS-04 study, which was conducted as a confirmatory trial for conditional approval in bladder cancer. This TROP2-targeted antibody-drug conjugate did not outperform chemotherapy in extending the lives of bladder cancer patients who had previously received PD-1/L1 treatment and chemotherapy.

This outcome is truly regrettable, as the purpose of the TROPiCS-04 study was precisely to secure full approval for Trodelvy. The failure of this trial means that Gilead Sciences' Trodelvy for the treatment of urothelial cancer could face withdrawal from the market. Moreover, earlier in January 2024, Trodelvy’s Phase III clinical trial for non-small cell lung cancer also failed.

This outcome made Trodelvy's $1.315 billion sales achievement in 2024, representing a 24% year-over-year increase, seem lackluster.

Misfortunes never come singly.

At the 2024 European Hematology Association (EHA) conference, Gilead Sciences presented the Phase III study data of Magrolimab, which not only failed to demonstrate efficacy but also showed persistently high safety risks.

In Gilead's Q1 financial report released at the end of April 2024, six clinical trials related to Magrolimab for solid tumors and hematological malignancies were marked as "Removed from pipeline." The CD47 antibody Magrolimab, which once led Gilead to spend $4.9 billion to acquire, has ultimately been shelved.

The failure of two key clinical products has caused Gilead's stock price to continue falling since 2024, with its market value evaporating by nearly 20 billion US dollars.

It should be noted that both Trodelvy and Magrolimab are key bets made by Gilead Sciences to expand its oncology portfolio and build new growth channels. The two acquisitions behind these products cost Gilead nearly $26 billion. Notably, Gilead's total product sales for the entire year of 2023 amounted to $26.9 billion.

Indeed, drug development is inherently a high-risk, high-investment endeavor, and the "tough nut to crack" nature of the CD47 target is an industry consensus. It’s not surprising that many companies have stumbled in this space. R&D pipelines acquired through external mergers and acquisitions may face additional uncertainties, such as technical challenges and market acceptance, all of which could impact the smooth progress of the R&D projects.

However, these two acquisitions not only failed to boost Gilead but even undermined Gilead's previous M&A myth.

In fact, Gilead Sciences has been highly regarded in the industry for its forward-looking and precise mergers and acquisitions. Trodelvy, the world's first Trop-2 ADC product, was globally leading at the time in terms of the two core elements of ADCs: the Linker and the antibody.

However, the above praise mainly reflects Gilead's success in the antiviral field, which is due to its systematic construction and iterative strategy. Through several key "snake swallowing elephant" acquisitions, Gilead not only gained underlying technology but also formed a strong scale effect and R&D efficiency.

However, its layout in the anti-tumor field has failed to replicate this model. The reason lies in the fact that antiviral and anti-tumor are two completely different fields, and Gilead Sciences overlooked this core issue in its anti-tumor strategy.

First, there are differences in disease mechanisms. The development of antiviral drugs mainly focuses on inhibiting viral replication and transmission, with relatively clear targets. For instance, the treatment of HIV and hepatitis C largely relies on direct-acting antiviral agents (DAAs), and the technological pathway is relatively straightforward.

Anti-tumor treatment involves complex biological mechanisms, including cell proliferation, apoptosis, immune regulation, and more. For instance, the development of CAR-T cell therapy and ADC drugs needs to address various issues such as immune response, targeting specificity, and toxic side effects.

Secondly, there are differences in the R&D pathways. The development of antiviral drugs is relatively linear, with a clear path from laboratory to clinical application. For example, the development of Sofosbuvir was based on known mechanisms of viral replication, making the R&D process relatively efficient. The R&D pathway for anticancer drugs is more complex, involving multidisciplinary integration. For instance, CAR-T cell therapy needs to address complex issues such as cell preparation, immune response, and patient variability.

In addition, there are differences in marketing. The marketing of anti-tumor drugs is more complex, as it needs to address a wide range of cancer types and patient needs. For example, the promotion of CAR-T cell therapy requires solving issues such as high costs and personalized treatment.

The Rise of Liver Disease Drugs: Returning to the Comfort Zone

Multiple "snake swallowing elephant"-style mergers and acquisitions have placed Gilead under tremendous financial pressure.

Although external collaborations can quickly supplement one's own pipeline, the projects acquired by large pharmaceutical companies through initial investments of hundreds of millions or even billions of dollars face uncertainties akin to "drawing water with a bamboo basket"—such as clinical trial failures, changes in market competition dynamics, shifts in project R&D priorities, or termination of cooperation and development.

Gilead Sciences' M&A Strategy Has Played a Key Role in Its Development. Through a Series of Bold M&A Moves, Gilead Successfully Rose in the Antiviral Field and Gradually Expanded into the Tumor Immunotherapy Sector. However, in Recent Years, Its M&A Efforts in the Oncology Field Have Not Achieved the Expected Success, Reflecting the High Risks Associated with M&A Strategies.

Therefore, after experiencing the glory in the antiviral field and the ups and downs in the oncology field, Gilead Sciences has gradually adjusted its M&A strategy in recent years, shifting from large-scale "high-risk" acquisitions to a more stable layout. This transformation is not only reflected in the adjustment of acquisition scale but also in the precise selection of acquisition targets and the grasp of market opportunities, with greater emphasis on the technical potential and market prospects of the acquisition targets.

On the other hand, due to setbacks in the oncology field, risk diversification has become particularly important. Therefore, the next step is to expand into multiple areas to mitigate the risks associated with a single project, which has also become one of the product selection strategies. For instance, in addition to the liver disease sector, Gilead Sciences is also conducting research and development in niche areas such as non-alcoholic steatohepatitis (MASH) and chronic kidney disease.

After conducting over $26 billion in M&A activities in 2020 (including the $21 billion acquisition of Immunomedics, the $4.9 billion acquisition of Forty Seven, and a $2 billion commercial collaboration with Arcus), Gilead Sciences did not engage in any significant M&A activities in 2021.

In 2022, Gilead Sciences acquired MiroBio Ltd. for $405 million. MiroBio's lead investigational antibody, MB272, is a selective agonist of the immune inhibitory receptor B- and T-lymphocyte attenuator (BTLA) and has entered Phase I clinical trials. MB272 targets T cells, B cells, and dendritic cells, suppressing or blunting activation and inhibiting inflammatory immune responses.

In 2023, Gilead Sciences acquired XinThera for an expected transaction value of approximately $2 billion. At the time, XinThera's pipeline mainly included the PARP1 inhibitor for oncology and the MK2 inhibitor for immunology, with all five assets at the IND stage.

This was followed by the acquisition of CymaBay Therapeutics, Inc. for $4.3 billion in 2024, a quintessential example of this prudent strategy.

Globally, there are over 20 new drugs for PBC that have entered the clinical stage, most of which are in Phase 2 clinical trials. The current types of new drugs mainly include PPAR agonists, FXR agonists, and IBAT inhibitors, with FXR agonists and PPAR agonists being the most extensively developed. Elafibranor, a PPARα/δ agonist developed by Genfit, has now been accepted by the U.S. FDA for its New Drug Application for the treatment of PBC.

GSK's Linerixibat is an oral ileal bile acid transporter selective inhibitor designed to treat PBC-related cholestatic pruritus. Findings from the phase 2 study indicate that it effectively alleviated cholestatic pruritus without triggering serious adverse events.

Chinese companies are also investing in the development of PBC indications, with the highest progress reaching phase 2 clinical trials. ASC42, independently developed by Ascletis Pharma, is a novel, highly efficient, selective non-steroidal FXR agonist. According to phase 1 clinical trial data, in healthy subjects, whether given a single dose as high as 100 mg or multiple doses up to 15 mg per day over 14 days, ASC42 demonstrated overall good safety and excellent human tolerability.

In addition, Zelgen's self-developed Obeticholic Acid Magnesium Tablets (ZG5266) is also an FXR agonist, currently in Phase 1/2 clinical trials for the treatment of primary biliary cholangitis.

Gilead's bet on Seladelpar not only boasts the fastest progress but is also the "first-in-class" oral PPARδ agonist, filling a market gap.

This precisely demonstrates the importance of focusing on small details. Forward-looking drug discovery doesn’t necessarily require blockbuster deals. Take the heavy-hitting cancer drug Opdivo as an example. In 2009, BMS acquired Medarex for $2.4 billion, gaining access to this technology. Such "bolstering" deals are still what Gilead continues to pursue.

Back to Seladelpar. The development of Seladelpar has not been smooth sailing. Initially, it was developed for the treatment of Metabolic Dysfunction-Associated Steatohepatitis (MASH), but it performed poorly in Phase 2 clinical trials and even showed potential safety issues. As a result, CymaBay Therapeutics decided to halt the drug's development in the MASH field.

As its mechanism of action has been further explored, Gilead Sciences recognized its therapeutic potential in the PBC field and acquired CymaBay Therapeutics for $4.3 billion in February 2024, bringing Seladelpar into its portfolio, and successfully driving its approval for the PBC indication.

Gilead's Comeback in the Liver Disease Field May Provide Valuable Experience for Its Future Prudent M&A Strategy: By building on its comfort zone, and through precise target selection, controlling the scale of acquisitions, and diversifying risks, Gilead may be able to replicate this model in other therapeutic areas.

Shifting to double down on investment in advantageous business directions may create a new opportunity for Gilead Sciences to regain momentum.