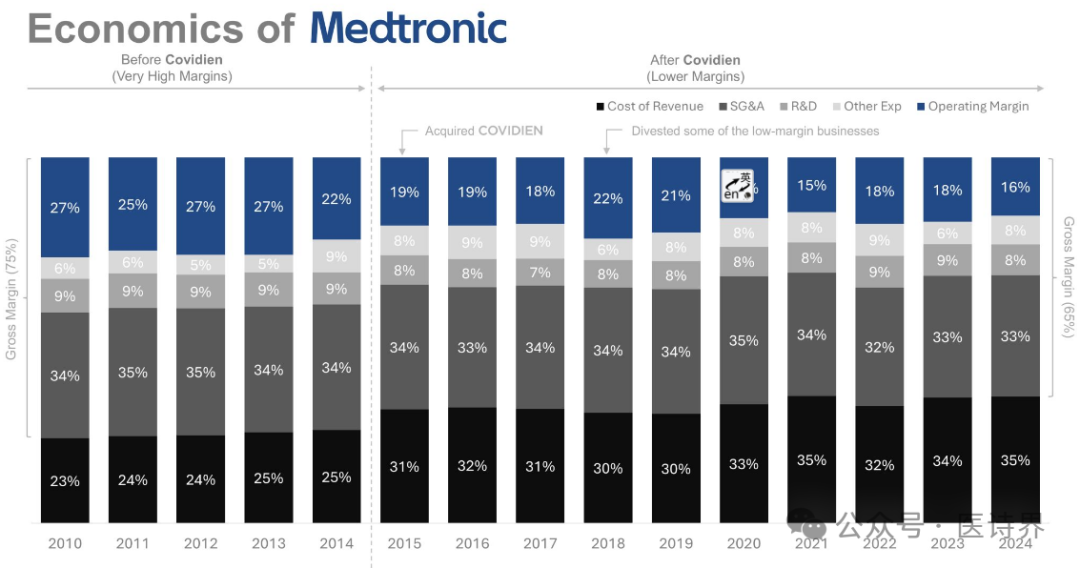

Ten years ago, inUnder Omar Ishrak's leadership, Medtronic completed the largest acquisition in the history of the medical device industry, with Medtronic acquiring Covidien for $43 billion.At the time of the transaction, Medtronic had 50,000 employees and an annual revenue of $18 billion, while Covidien had 40,000 employees and an annual revenue of $10 billion. This acquisition was essentially more like a merger of equals. Through this acquisition, Medtronic surpassed Johnson & Johnson to become the leading company in the medical device industry, a position it held for a decade.The "big brother" of medical devices, Glory, has brought countless honors to Medtronic, but it has also brought无形pressure to Medtronic. Before acquiring Covidien, Medtronic was the benchmark for profitability in the medical device industry. The company maintained an astonishing gross margin of nearly 75% and a robust operating margin of over 25%, thanks to its core business in high-value Class III medical devices. Its R&D investment also remained at a leading level in the industry (accounting for 9% of revenue), building a solid technological moat.AcquisitionAfter Coviden, Medtronic's profitability experienced a structural collapse, transforming from a high-tech, high value-added company into a "low profitability, low-value enterprise."

Before acquiring Covidien, Medtronic was the benchmark for profitability in the medical device industry. The company maintained an astonishing gross margin of nearly 75% and a robust operating margin of over 25%, thanks to its core business in high-value Class III medical devices. Its R&D investment also remained at a leading level in the industry (accounting for 9% of revenue), building a solid technological moat.AcquisitionAfter Coviden, Medtronic's profitability experienced a structural collapse, transforming from a high-tech, high value-added company into a "low profitability, low-value enterprise."

Because Coviden's product line mainly consists of Class I medical devices with lower profit margins. Despite its smaller revenue scale, this merger has caused a "dimensionality reduction blow" to Medtronic’s profitability structure:The proportion of sales cost jumped from 25% to 35%.

Gross margin fell from 75% to 65%

Operating Profit Margin Halved, Plunging from 27% to 17%

Even though revenue nearly doubled, the company’s operating profit has stagnated. The strategic adjustment in 2017 to divest some low-margin businesses for $6 billion to Cardinal Health also failed to reverse the long-term decline in profitability.

Due to long-termThe inability to improve profitability has also led to a decline in Medtronic's market value.Collapse, from a high of $150 billion to now $100 billion. It has also stepped down from the top spot in the medical device market capitalization, successively surpassed by Stryker,Intuitive, Boston Scientific surpassed. Even compared with the 180% increase of the S&P 500 Index in the same period, it pales, showing the disappointment of the capital market. Therefore, if Medtronic cannot change this situation quickly, it will face continuous pressure from capital and may even be split. For capital, a rise in the stock market means big money.

Medtronic and CEOGeoff Martha Faces Significant Pressure, Hoping Medtronic Can Return to a High-Growth, High-Profit State.