Johnson & Johnson Tops Q1 Pharma Sales with Over $20B, Lilly Surges 45%, Top 3 Oncology Drugs Generate $12.7B

Johnson & Johnson

Medical Device R&D and Manufacturer

Wonderful Content

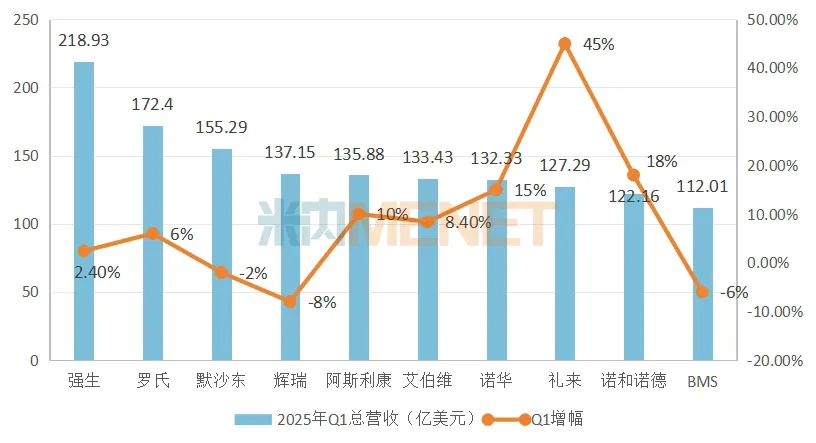

Recently, major multinational pharmaceutical companies have successively released their Q1 2025 financial reports. Based on each company's revenue performance, the top ten rankings for Q1 are as follows: Johnson & Johnson, Roche, Merck, Pfizer, AstraZeneca, AbbVie, Novartis, Eli Lilly, Novo Nordisk, and BMS. Sanofi narrowly missed the list. Meanwhile, the oncology field has always been a "must-compete territory" for multinational pharmaceutical companies. Merck's Keytruda remains firmly in the top position, generating over $70 billion in revenue, with Johnson & Johnson's Darzalex (daratumumab) following closely behind. The weight loss sector is gaining significant momentum, with the competition between Eli Lilly and Novo Nordisk becoming increasingly intense...

Johnson & Johnson surpasses $20 billion to claim the "sales champion" throne, while Eli Lilly surges 45% into the rankings

Multiple multinational pharmaceutical companies have released their Q1 2025 financial reports. In terms of total revenue, the top five are Johnson & Johnson, Roche, Merck, Pfizer, and AstraZeneca. When ranked solely by pharmaceutical business revenue, the top five are Johnson & Johnson ($13.872 billion, +2.3%), Pfizer ($13.715 billion, -8%), Merck ($13.638 billion, -3%), AstraZeneca ($13.588 billion, +10%), and AbbVie ($13.343 billion, +8.4%).

Figure 1: TOP10 pharmaceutical companies' Q1 2025 performance

As the TOP1 in comprehensive strength,Johnson & JohnsonWith the revenue from two major sectors — Innovative Pharmaceuticals ($13.872 billion, +2.3%) and Medical Technology ($8.020 billion, +2.5%) — firmly securing the top position;RocheRelying on pharmaceutical business revenue (USD 13.342 billion, +8%) and diagnostic business revenue (USD 3.898 billion, +8%) to rank second; holding the ace product Keytruda,Merck & Co.Also ranked third.

Notably, 2025 Q1SanofiRevenue of $10.457 billion, a year-on-year increase of 9.7%, was $7.44 billion behind BMS, which ranked 10th, missing out on a spot in the TOP10 list.

In Q1 2025, the year-over-year total revenue growth showed polarization. Companies like Eli Lilly, Novartis, Novo Nordisk, and AstraZeneca experienced rapid growth, with Eli Lilly’s growth reaching as high as 45%. In contrast, Merck, Pfizer, and BMS reported negative growth, while other multinational corporations (MNCs) showed single-digit growth.

Eli LillyThe rapid growth in performance is attributed to the GLP-1/GIP dual agonist tirzepatide. Specifically, the diabetes version of tirzepatide, Mounjaro, achieved sales of $3.84 billion in Q1 this year, representing a 113% year-over-year increase; the weight loss version of tirzepatide, Zepbound...Q1 revenue was $2.31 billion, compared to just $517.4 million in the same period last year. Tirzepatide contributed $6.15 billion in revenue for Eli Lilly, accounting for 48% of the total Q1 2025 revenue, driven by its two major indications.

NovartisThe rapid growth is backed by the steady increase in its four core areas: cardiovascular-renal-metabolic, immunology, neuroscience, and oncology, along with the boost from multiple innovative drugs such as Entresto (sacubitril/valsartan), Cosentyx (secukinumab), and Kisqali (ribociclib), achieving a year-on-year growth rate of 15%.

Semaglutide Becomes a Global BestsellerNovo NordiskA Key Driver of Revenue Growth: Semaglutide (Combined Sales of Three Products) Reached $80.11 Billion in Q1 2025, a Year-on-Year Increase of 31%, Accounting for Nearly Two-Thirds of Novo Nordisk's Total Revenue.

AstraZenecaDriven by double-digit growth in both oncology and biopharmaceutical businesses, the total revenue for Q1 2025 is expected to grow by no less than double digits.

Blockbuster Tumor Drugs Go Head-to-Head, Top 3 Rake in $127 Billion

The oncology field has always been a "must-contest territory" for multinational pharmaceutical companies. Amidst various pressures and a constantly changing market landscape, the oncology sector remains a crucial domain for most multinational pharmaceutical enterprises.

According to the published financial report data, in the oncology field by 2025The top three drugs in Q1 sales are all monoclonal antibody drugs, namely Merck's Keytruda (Pembrolizumab), Johnson & Johnson's Darzalex (Daratumumab), and BMS's Opdivo (Nivolumab). The Q1 sales of these three drugs in 2025 have all successfully broken through the threshold of 2 billion US dollars. Among them, Keytruda this year...Q1 sales reached $7.205 billion, a year-on-year increase of 4%, firmly maintaining its position as the top-selling oncology drug.

Table 1: Partial Sales of Oncology Drugs Exceeding $1 Billion in Q1 2025

Merck & Co.Global sales in Q1 this year dropped by 3%, but the oncology sector achieved positive growth, with the core product PD-1 inhibitor Keytruda (Pembrolizumab) continuing to shine.K drug's sales in Q1 this year were $7.205 billion, a year-on-year increase of 4%.Accounting for 53% of the entire pharmaceutical business. In other oncology drugs, Lynparza (olaparib), a PARP inhibitor jointly developed by Merck and AstraZeneca, generated $321 million in revenue for Merck.

Johnson & JohnsonTumors account for half of the market, and in Q1 2025, the oncology sector achieved revenue of $5.678 billion, a year-on-year increase of 17.9%. Oncology drugsDarzalex (daratumumab) generated revenue of $3.237 billion, representing a year-over-year increase of more than 20%.The growth rate of CAR-T drugs is the fastest. Carvykti (Cilta-cel), the CAR-T therapy for treating multiple myeloma developed through the collaboration between Johnson & Johnson and Legend Biotech, achieved $369 million in sales in Q1 2025, representing a year-over-year increase of 135%.

BMSMature Products in the Oncology SectorOpdivo (Nivolumab) generated revenue of $2.265 billion, a year-on-year increase of 9%.Yervoy (Ipilimumab) and Opdualag (Nivolumab + Relatlimab) generated revenues of $624 million and $252 million respectively. The global second KRAS G12C inhibitor, Krazati (Adagrasib), achieved a Q1 revenue of $48 million in 2025, with growth surging over 100%.

AstraZenecaOncology business remains the strongest growth point in Q1 2025. Specifically,Tagrisso (Osimertinib)Remains the best-selling product in a single quarterSales reached $1.679 billion, an 8% increase year-over-year.;Imfinzi (Durvalumab) sales reached $1.261 billion, a year-on-year increase of 16%, mainly due to strong demand in HCC and BTC as well as further increases in early-stage NSCLC and limited-stage SCLC patients. Other oncology products Calquence (Acalabrutinib), Lynparza (Olaparib), and Enhertu (Trastuzumab Deruxtecan) all showed growth across the board.

Besides, in Q1 2025, AbbVie's oncology sector achieved revenue of $1.633 billion, increasing by 5.8% year-on-year; Novartis' oncology sector revenue reached $3.906 billion, growing by 24% year-on-year, and Sanofi's oncology sector revenue was $1.402 billion.

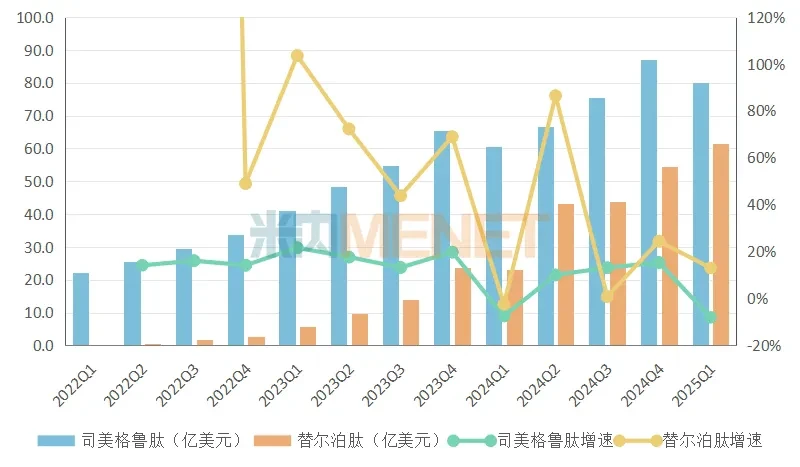

Weight Loss Giants Battle! Two Major Blockbuster Products Only $1.8 Billion Apart in Q1, More Weight Loss Products on the Way

As Eli Lilly and Novo Nordisk announce their Q1 2025 earnings reports, competition in the GLP-1 space is reaching a fever pitch, with the weight loss market landscape undergoing significant changes.

From the generic name,Novo Nordisk's SemaglutideTotal revenue for Q1 2025 reached $8.011 billion, representing a 31% year-over-year increase.Eli Lilly's TirzepatideSlightly ahead. Eli Lilly's tirzepatide total revenue for Q1 2025 is $6.15 billion.

In terms of individual product names, Novo Nordisk's semaglutide injection for blood sugar control (Ozempic), semaglutide tablets (Rybelsus), and semaglutide weight-loss injection (Wegovy) generated revenues of $4.79 billion, $830 million, and $2.54 billion, respectively.

Lilly's diabetes version of tirzepatide (Mounjaro) and weight-loss version of tirzepatide (Zepound) generated revenues of $3.84 billion and $2.31 billion respectively in Q1 2025.

From the sales gap perspective, in the second half of 2024, the gap between semaglutide and tirzepatide exceeded $3 billion, while in Q1 of 2025, the gap between semaglutide and tirzepatide had narrowed to $1.8 billion.

Figure 2: Sales comparison of Semaglutide and Tirzepatide from Q1 2022 to 2025

In the Chinese market, the popularity of semaglutide is quite high. Semaglutide injection for blood sugar control (brand name: NovoTide), oral semaglutide tablets for blood sugar control (brand name: NovoSin), and semaglutide injection for weight loss (brand name: NovoWin) were approved for marketing in China in 2021, January 2024, and June 2024, respectively. In May and July 2024, tirzepatide received approval from the National Medical Products Administration, with the brand name MuFengDa, applicable to both diabetes patients and those seeking weight loss. To date, both indications have been commercially launched in China.

Figure 3: Tirzepatide Injection Related Approval Documents

(Click on the image to enlarge)

(Click on the image to enlarge)The competition for market sales is still ongoing, and further research is needed to determine who will be the true weight-loss champion in the future.

On May 12, 2025, Eli Lilly announced the detailed results of the head-to-head study (SURMOUNT-5) comparing tirzepatide and semaglutide. SURMOUNT-5 is a multicenter, randomized, open-label Phase IIIb trial. The trial aims to evaluate the efficacy and safety of tirzepatide versus semaglutide in overweight adults with obesity or at least one comorbidity (such as hypertension, dyslipidemia, obstructive sleep apnea, cardiovascular disease) who do not have diabetes. The data shows that tirzepatide surpasses semaglutide with a 1.47-fold relative advantage in weight loss effects, and tirzepatide outperforms semaglutide in all key secondary endpoints related to weight loss and waist circumference reduction.

Besides tirzepatide and semaglutide, Lilly and Novo Nordisk are also secretly competing in other pipelines within the weight-loss track.

Novo Nordisk's CagriSema is considered an "upgraded version" of semaglutide. The company announced the Phase III clinical trial data for this product by the end of 2024. The data shows that CagriSema has better weight loss effects than semaglutide, but the degree of weight loss fell short of market expectations. Nevertheless, Novo Nordisk has not lost hope in CagriSema and plans to release the results of the second pivotal Phase III trial, REDEFINE 2, in the first half of 2025. This trial targets adult patients with type 2 diabetes who are obese or overweight.

Another weight-loss drug being developed by Eli Lilly, Retatrutide, simultaneously activates three major receptors: GLP-1R (suppresses appetite), GIPR (regulates insulin), and GCGR (glucagon receptor). The addition of GCGR makes "accelerated fat burning" possible. Currently, Retatrutide has entered Phase III clinical trials, covering a broader population including obesity combined with diabetes and cardiovascular diseases. If the Phase III data meets expectations, it is expected to be launched in 2027.

To counter Eli Lilly's triple receptor agonist, in March this year Novo Nordisk announced a collaboration with United Biotech on the rights outside Greater China for a long-acting GLP-1R/GIPR/GCGR triple agonist (UBT251). According to the agreement, United Biotech will receive a $200 million upfront payment, up to $1.8 billion in potential milestone payments, and tiered sales royalties in the licensed region.

Source: Company financial reports,MENET Databaseetc.