Chinese Neurovascular Intervention Leaders Achieve Collective Profitability Three Years After Volume-Based Procurement

Zylox-Tonbridge

Innovative R&D, Production, and Sales of Medical Devices in the Vascular Intervention Field

Peijia Medical

Developer of Cardiac and Cerebrovascular Interventional Medical Devices

HeartCare

Neurointerventional Medical Device Developer

SINOMED

High-end interventional medical device R&D, production, and sales provider

Since 2021, the field of neurointervention has been included in the centralized procurement, and the industry pattern is rushing towards an unpredictable direction.

In the first centralized procurement of neurointerventional products, the average price of coils dropped from 12,000 yuan to around 6,400 yuan, with an average reduction of 46.82% and a maximum reduction of 66%. Subsequently, various provinces and cities or provincial alliances gradually included neurointerventional products in their centralized procurement programs. Currently, the lowest bid for coils is about 3,244 yuan, the average price of intracranial thrombectomy stents has decreased from 26,900 yuan to less than 4,000 yuan, and there have been significant price reductions for access products such as catheters and guidewires...

Intracranial covered stents, which have high technical barriers and fewer approvals, have been reduced from over 100,000 yuan to 78,600 yuan, and flow diverter stents have dropped to an average of 60,000 yuan (with a minimum of 49,000 yuan).

Moreover, unlike the high selection rate in the early stage of centralized procurement, the selection rate for neurointerventional centralized procurement has been continuously declining. For instance, the selection rate for the 2023 Beijing-Tianjin-Hebei "3+N" Alliance neurointerventional centralized procurement was only 20%, with most products being eliminated, and the gap between other companies and leading companies is widening. However, during the procurement of some high-barrier products, the selection rate remains relatively high (over 80%).

Since the centralized procurement of neurointerventional products, the industry landscape has undergone significant changes.: First, the market share of China-produced neurointerventional products surged from less than 10% to 26% (in 2024). Second, the industry has entered a phase of elimination, with market share concentrating among leading companies, and less competitive firms will face bankruptcy and liquidation one after another. Third, an increasing number of neurointerventional products are being included in centralized procurement, leading to a decline in the prices of related products and a shrinking domestic market space.

It should be noted that,Despite winning in terms of market share, leading companies in China's neurointervention field have long been in a state of financial loss.For example, Minimally Invasive Brain Science reported a net loss of 24.678 million yuan in 2022; Zylox-Tonbridge's loss attributable to equity holders was 78.734 million yuan in 2023; Peijia Medical's neurointervention business incurred a loss of approximately 60 million yuan in 2022; HeartCare reported a loss of 94 million yuan in 2023. SINOMED's parent company loss was 39.63 million yuan in 2023.

This is mainly because the products of the aforementioned leading companies were mostly launched around 2021, and they encountered centralized procurement (low end-user prices) soon after their launch, missing out on a period of high profitability. Coupled with substantial upfront investments in equipment and R&D, these leading companies have remained in a state of consecutive annual losses.

However, by 2024,Three Years After the Centralized Procurement, Leading Companies in the Neurointervention Field Finally Achieved ProfitabilityAmong them, Minimally Invasive Brain Science achieved a net profit of 249 million yuan (turning profitable in 2023); Zylox-Tonbridge reported a profit of approximately 100 million yuan, reversing the previous year's loss; Peijia Medical’s neurointervention business achieved a profit of 52.09 million yuan, turning profitable; SINOMED realized a parent company net profit of 1.4978 million yuan, reversing the loss; HeartCare’s pre-tax loss significantly narrowed from 103 million yuan to 12 million yuan in 2024, representing an 88.3% year-on-year reduction, and its operating cash flow is nearing balance.

From Years of Continuous Losses to Turning a Profit: What Have the Leading Neurointerventional Companies Done?

Turning Loss into Profit: From the Most Fundamental Perspective, It Means Revenue Exceeds Cost. This Requires Companies to Continuously Increase Revenue and Reduce Costs.

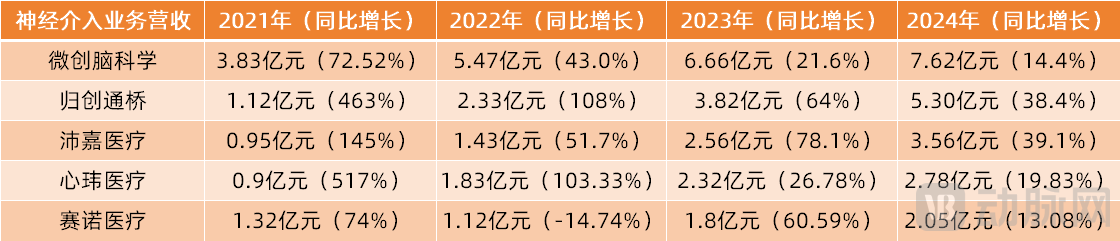

From 2021 to 2024, the revenue growth of leading companies in the neurointerventional sector has been extremely rapid. For example, the revenue from Zylox-Tonbridge's neurointerventional business increased by 463%, 108%, 64%, and 38.4% year-on-year respectively; Peijia Medical's neurointerventional business grew by 145%, 51.7%, 78.1%, and 39.1% year-on-year respectively… Although the annual growth rates of various enterprises fluctuated, they generally remained at a high level, demonstrating that the industry-leading companies maintained a relatively high year-on-year growth rate during these years.

Revenue Surge Attributed to Multiple Factors: Detailed Analysis Below

First, the number of commercialized products increases.In 2021, leading neurointerventional companies in China had fewer products approved and commercialized domestically. For instance, Minimally Invasive Brain Science had only 8 approved products, Zylox-Tonbridge had 10, Peijia Medical and HeartCare each had 11, while SINOMED had 3.

(Number of products approved and commercialized by leading domestic neurointervention companies in 2021/2024)

By 2024, the number of neurointerventional products approved and commercialized by leading companies has significantly increased. Minimally Invasive Brain Science has 25 neurointerventional products approved and commercialized in China, Zylox-Tonbridge has 23, Peijia Medical has 17, HeartCare has 22, and SINOMED has 14.

Among them, Peijia Medical specifically mentioned in its 2024 annual report: In August 2024, the company reached a cooperation with NuYang Medical to obtain the exclusive distribution rights for the Greater China region of NuYang Medical's self-developed YonFlow flow diverter stent, completing the final piece of the company’s bleeding product line.

These leading companies have almost all achieved a full-range product layout in the three细分 markets of "ischemic, hemorrhagic, and access" within the neurointervention field.A rich product line and the launch of key products have laid the foundation for leading domestic neurointerventional companies to rapidly increase their revenue.。

In addition, the platform-based layout and a rich product line will enhance the company's market competitiveness, enabling it to adopt flexible pricing strategies and achieve revenue and profit growth by selling complementary products, thereby delivering a competitive blow to single-product companies.

Second, centralized procurement has driven a significant increase in the sales volume of leading companies' products, helping them boost revenue.Typically, after medical device products are approved, they still need to go through processes such as listing on procurement platforms and entering hospitals, which can take a considerable amount of time. However, the centralized procurement of neurointerventional products has accelerated the commercialization speed of related companies' products.

For example, Minimally Invasive Brain Science's NUMEN coils, leveraging the opportunity of centralized procurement, gained access to approximately 520 new hospitals in 2024, with cumulative clinical application in nearly 1,450 hospitals.

Several months after the execution of the centralized procurement project that selected Zylox-Tonbridge's SilverSnake intracranial support catheter, the product's sales volume in most provinces...An average increase of approximately 2.5 times。

Peijia Medical's coil products have also been stimulated by volume-based procurement. It is reported that Peijia Medical's coil products were previously selected in projects such as the Jilin Province-led provincial alliance coil procurement and the Beijing-Tianjin-Hebei "3+N" alliance coil procurement. To date, the selected regions for its coil products have covered over 90% of provinces and municipalities in China. Based on this, in 2024, the revenue from Peijia Medical's Jasper intracranial electrically detachable coil increased by 18.5 million yuan.

HeartCare's multiple neurointerventional products have won first place or the highest bid price in several alliance procurement projects, accelerating the expansion of their market share. Affected by centralized procurement, the implantation volume of HeartCare's neurointerventional products exceeded 180,000 units in 2024.

It can be seen that, driven by the centralized procurement, the terminal prices of products from leading companies have decreased, but their sales volume has grown significantly, leading to a rapid increase in the overall revenue of the companies. Meanwhile, the centralized procurement products of these leading companies, such as coils, have gradually achieved a good effect of trading volume for price due to product performance and brand reputation, with market share steadily increasing.

As a result, companies continue to actively participate in the centralized procurement of neuro-interventional products. For instance, in the 2025 provincial alliance volume-based procurement project led by Hebei, Minimally Invasive Brain Science (Suzhou) Co., Ltd. actively participated, with its Tubridge flow diverter, the next-generation fully visible Tubridge Plus flow diverter, and intracranial balloon dilation catheter all successfully winning bids.

Zylox-Tonbridge succeeded in the bidding for its Kylin Flow Diverter, Baiju Intracranial PTA Balloon Dilatation Catheter (Rx), and three peripheral balloon products during the relevant product procurement process in early 2025, paving the way for a significant increase in sales.

Peijia Medical's SacSpeed Balloon Dilation Catheter and Fastunnel Delivery Balloon Dilation Catheter were both selected under Rule A of Group 1 in the January 2025 provincial alliance procurement for vascular interventional consumables. After the official implementation of the procurement, sales are expected to increase significantly.

Third, leading neurointerventional companies are accelerating their overseas expansion, opening up a second growth curve in the market.After centralized procurement, the domestic neurointervention market space has been affected. Against this backdrop, leading neurointervention companies have turned their attention to the vast overseas markets, hoping to break through market limitations.

Among them, Minimally Invasive Brain Science conducted more than 50 overseas surgical training sessions and academic exchange conferences in 2024, inviting multiple overseas clinical doctors and partners to visit the company, receive product training, and engage in discussions. At the same time, Minimally Invasive Brain Science also transitioned its distribution model in the U.S. market to a direct sales model starting from the first quarter of 2024, and has since entered nearly 50 hospitals. The direct sales model not only aligns better with local marketing practices but has also significantly improved operational efficiency and profit levels.

Under various initiatives, Minimally Invasive Brain Science's overseas business has made significant progress: in 2024, its overseas revenue increased by 137.9% year-on-year; the Numen Silk Coil Embolization System received FDA and CE registration approvals; the Numen Coil Embolization System expanded into 10 additional countries and broke into the South Asian market for the first time; products such as the Tubridge Flow Diverter, Neurohawk Thrombectomy Stent, and X-track Distal Catheter achieved their first commercial use in Brazil and Argentina.

Zylox-Tonbridge, Peijia Medical, HeartCare, SINOMED, and other leading neurointervention companies are also accelerating their expansion overseas. For instance, Zylox-Tonbridge's international business revenue reached 22.6 million yuan in 2024, representing a year-on-year increase of 58.2%, mainly from Europe and Asia.

Currently, Zylox-Tonbridge has sold 20 products in 24 overseas countries and regions. In addition to traditional sales and marketing activities, Zylox-Tonbridge also conducts post-market clinical follow-up trials to demonstrate the clinical value of its products overseas, further gaining market recognition. According to its annual report, Zylox-Tonbridge is engaging with various partners in Europe and plans to accelerate its development through a broader cooperation strategy.

HeartCare's overseas revenue reached 8.395 million yuan in 2024, marking a year-on-year increase of 684%. Its products, including intracranial thrombectomy stents, occlusion balloon catheters, and distal access catheters, have obtained CE or FDA certification, along with 26 registration certificates from other countries and regions. Currently, HeartCare is in the process of registering over 40 products across 10 countries and regions while expanding sales channels to lay the foundation for achieving long-term overseas sales goals.

SINOMED officially kicked off the overseas expansion of its neurointerventional products starting in 2024. The company has reached cooperation intentions with distributors across multiple overseas markets and swiftly initiated the overseas registration process for its neurointervention-related products. To date, SINOMED has completed the submission for CE certification of its intracranial thrombectomy stent and self-expanding intracranial stent, with applications already accepted, and registration work in several countries is progressively commencing.

Fourth, adopt targeted marketing strategies to boost product sales.Market promotion is also an indispensable and crucial factor in market activities. In the promotion of neurointerventional products, leading companies have adopted different measures.

For example, Minimally Invasive Brain Science has focused on grassroots hospitals as the key market for its acute ischemic stroke products. Targeting the grassroots market, Minimally Invasive Brain Science provides clinical training, post-operative consultation, and routine guidance to doctors in lower-tier cities and county-level hospitals, helping grassroots hospitals enhance their stroke treatment capabilities. As a result, the sales of its acute ischemic stroke products surged significantly, with revenue from this segment reaching 46.74 million yuan in 2024, marking an 82% year-on-year increase. In 2023, this segment experienced a year-on-year growth of 394.2%.

In terms of access products, Minimally Invasive Brain Science's market promotion strategy is to sell them in conjunction with therapeutic products, fully leveraging competitive advantages such as high clinical compatibility and well-established marketing channels. In 2024, the U-track support catheter, a key accessory in aneurysm treatment surgeries, achieved rapid growth in clinical usage driven by the increased sales volume of related therapeutic products.

Peijia Medical, on the other hand, focuses on strengthening market promotion through differentiated marketing strategies such as innovative surgical techniques. For instance, Peijia Medical promotes innovative procedures like BASIS, COSIS, TRUST, REST, ATTACH, Zero Exchange, FAST ICAS, and ANSWER to drive the sales growth of its thrombectomy stents, intermediate guiding catheters, and delivery balloon dilation catheters.

Through the above measures and conventional promotional activities, the revenue of leading neurointervention companies in China has skyrocketed.

Turning losses into profits, another key point is to cut costs.

According to the annual reports of leading enterprises,Improving operational efficiency is its main means of reducing costs.。

For example, through refined management, Peijia Medical achieved a 20.3% year-on-year decrease in sales expense ratio and a 7.6% year-on-year decrease in administrative expense ratio in 2024.

Zylox-Tonbridge improved operational efficiency by strengthening its team, reducing the proportion of sales and distribution expenses to total revenue from 31% in 2023 to 22.3% in 2024, while administrative expenses decreased from 114 million yuan to 91 million yuan.

HeartCare is no exception. Its administrative expenses decreased from 74.6 million yuan to 58.2 million yuan, while sales and distribution expenses remained balanced (despite a significant increase in sales).

In addition, leading neurointerventional companies also reduce costs by optimizing the supply chain and promoting intelligent and lean production.

For example, in 2024, SINOMED improved product stability and yield rate while reducing unit cost and increasing product gross margin through measures such as improving product processes, optimizing equipment performance, and utilizing AI intelligent tools. Specifically, it completed the optimization of key processes such as heat treatment, sandblasting, and electrochemical polishing for its metal stent platform; redesigned spraying equipment and tooling for the drug-coating process platform and optimized process parameters; and optimized existing processes for the access catheter platform by introducing new materials and techniques.

Minimally Invasive Brain Science completed over 60 supply chain improvement and upgrade projects in 2023, significantly reducing production costs. By the end of 2023, the localization rate of raw materials for products under Minimally Invasive Brain Science had reached over 90%, with the localization rate of key materials exceeding 85%.

HeartCare continues to improve processes such as stainless steel and nitinol welding, ultra-smooth coating technology, and multi-strand winding technology, while reducing costs through intelligent production and other measures. At the same time, the localization rate of the more than 2,000 materials required for HeartCare's products exceeds 95%.

In addition, the sales volume of products under each leading company has surged in recent years, spreading out their initial R&D and equipment investments, thereby reducing this portion of costs.。

Overall, leading neurointervention companies in China have reduced overall costs through refined management and optimized supply chains. The revenue growth far outpaced the increase in costs, enabling these leading neurointervention companies to finally turn a profit.

It is worth mentioning that, due to the decline in the rate of centralized procurement bids and the competitive pressure from leading companies expanding their product lines, some backward small and medium-sized enterprises will face bankruptcy liquidation. The neurointervention market will further concentrate, and with the promotion by domestic companies, the localization rate will also accelerate.

According to the annual reports of various companies, in the future, leading enterprises in the neurointerventional field will continue to enhance operational and production efficiency, reduce overall costs, and optimize the supply chain system; actively expand their international presence to break through market ceilings; participate in domestic collective procurement to increase market share; strengthen the research and development of innovative technologies, and focus on emerging therapeutic fields with high growth potential by developing innovative medical devices, thereby creating new business lines.It is expected that under these initiatives, leading neurointerventional companies will earn more profits thereafter.