Hansoh Pharma 2025 Interim Report: A Paradigm of Global Innovation Upgrade for Chinese Innovative Pharmaceutical Companies

Hansoh Pharma

Pharmaceutical Research, Production, and Sales

Note:This article does not constitute any investment opinions or suggestions; please refer to official/company announcements for accuracy.This article only introduces drugs related to medical health, not a recommendation of treatment options (if involved), and does not represent the platform's position.Any article reprinted needs to be authorized.

Hansoh Pharma delivers a robust interim report.

In the first half of 2025, the company achieved revenue of 7.434 billion yuan, representing a year-on-year increase of 14.3%; profit reached 3.135 billion yuan, marking a year-on-year growth of 15.0%. Meanwhile, the company announced an interim dividend of 23.16 Hong Kong cents per share, maintaining stable returns for shareholders.

But the growth figures are not the whole story of this earnings report.

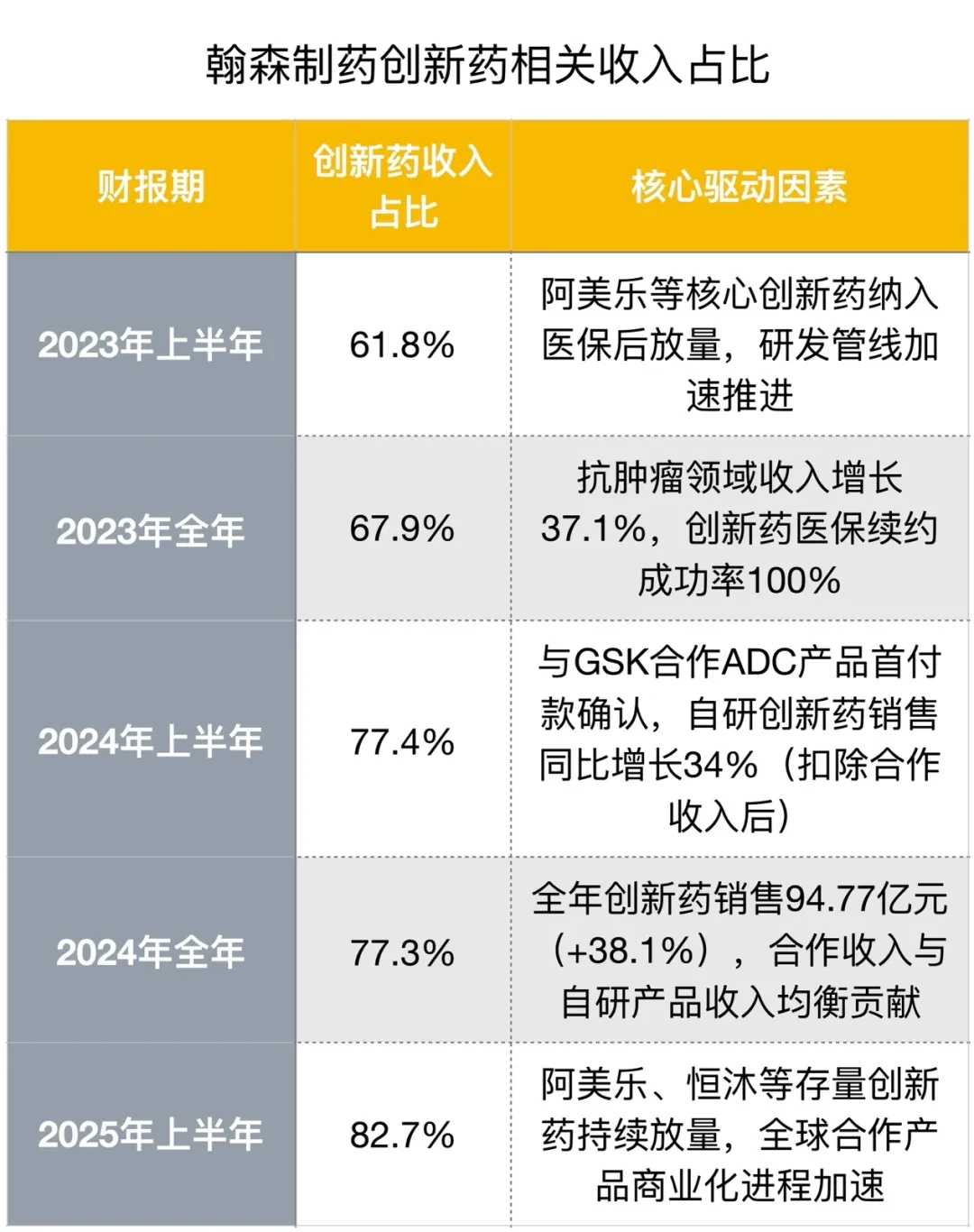

A key figure defines Hansoh's present and future: revenue from innovative drugs and collaborative products reached 6.145 billion yuan, increasing by 22.1% year-on-year, accounting for a whopping 82.7% of total revenue.

This proportion has increased by 5.3 percentage points from 77.4% in the first half of 2024, and surged nearly 21 percentage points from 61.8% in the same period of 2023. This marks that the business structure transformation of Hansoh Pharma has passed a critical turning point, and its growth momentum has completely shifted.

Driving this profound transformation are two major engines: continuously intensified internal R&D and a series of fruitful external collaborations. During the reporting period, Hansoh Pharma's R&D expenditure reached 1.441 billion yuan, increasing by 20.4% year-on-year, with R&D investment intensity approaching 20%. As of the interim report, the company held cash and bank deposits amounting to 27.104 billion yuan, providing more possibilities for the future thanks to its robust cash flow.

In terms of external cooperation (BD), following significant deals with GSK and Merck (MSD), in the first half of 2025, Hansoh Pharma once again reached an overseas licensing agreement with global giant Regeneron for its self-developed GLP-1/GIP dual-target agonist HS-20094.

Now, Hansoh's identity has changed. It is no longer a company in transition.Pharma, but a Biopharma dominated by innovation.

Breaking down the revenue composition of Hansoh Pharma, its growth is not driven by a single product or field but exhibits a healthy trend of diversified development. The four major sectors—oncology, metabolism, central nervous system, and anti-infectives—jointly form a solid business foundation.

The anti-tumor field remains the absolute cornerstone of Hansoh Pharma.

In the first half of the year, this segment achieved revenue of 4.531 billion yuan, accounting for over 60% of total revenue, reaching 60.9%.

The core driving force comes from China's first domestically developed third-generation EGFR-TKI, Amelie (Ameile).®(Aumetinib). During the reporting period, Ameile®Two new indications have been approved in China, covering consolidation treatment for patients with unresectable locally advanced NSCLC and adjuvant treatment for postoperative patients with stage II-IIIB NSCLC, bringing the total number of approved indications in China to four.

At the same time, Ameile®Approved for marketing by the UK Medicines and Healthcare products Regulatory Agency (MHRA) in June 2025, achieving a milestone for China-originated EGFR-TKI to reach overseas markets.

Hansoh Pharma's Amelie®The lifecycle management strategy is clear and long-term. In the short term, rapidly cover the newly added adjuvant treatment population; in the medium term, further consolidate the market position through combination therapies (e.g., first-line combination chemotherapy with a PFS of 28.9 months); in the long term, establish new mechanisms such as ADC and c-MET small molecule combinations to build a strong competitive moat.

The metabolic and other diseases segment was the fastest-growing sector in the first half of the year, generating revenue of 1.40 billion yuan, accounting for 18.8%.

This growth was mainly driven by the value realization of BD collaboration projects. During the reporting period, Hansoh Pharma confirmed the receipt of a $112 million upfront payment from Merck for their GLP-1 small molecule collaboration project. This revenue demonstrated to the market the external recognition of the value of its R&D pipeline, while the BD strategy also brought direct financial contributions to the company.

This model creates a self-reinforcing positive cycle: strong sales of core products provide ample cash flow for R&D, while the high-value pipeline generated by R&D brings in substantial returns through BD licensing, further strengthening the company's finances and laying the foundation for higher levels of R&D investment.

In the two traditional areas of strength for Hansoh—central nervous system (CNS) and anti-infectives—the company has also maintained steady growth through the iteration of innovative products.

In the first half of the year, the revenue in the CNS field was 7.68 billion yuan, and the revenue in the anti-infective field was 7.35 billion yuan, both achieving a year-on-year growth of approximately 4.8%. The growth was driven by the innovative drug Sinuva.®(Inebilizumab) and Hengmu®Driven by the continued increase in (Amitinofovir Tablets).

The steady performance of these two sectors has provided the company with valuable cash flow and a market foundation during the overall transition period, serving as an important guarantee for achieving a "soft landing."

The confidence behind Hansoh's transformation ultimately comes from the depth and breadth of its R&D pipeline. Currently, the company is advancing more than 40 innovative drug candidates and conducting over 70 clinical trials. Its pipeline fully covers the most cutting-edge and popular fields in the global biopharmaceutical industry.

Antibody-drug conjugates (ADCs) are the most prominent part of Hansoh Pharma's pipeline, forming a sizable "ADC army."

Notably, the self-developed B7-H3-targeting ADC (HS-20093) stands out, with its development progress ranking among the global leaders. It has already entered Phase III clinical research in China for two major indications: small cell lung cancer and bone and soft tissue sarcoma. Through collaboration with GSK, the global development of HS-20093 is advancing rapidly, with plans to enter global Phase III trials by 2025 and initiate combination therapy studies with PD-1 inhibitors.

Another self-developed B7-H4-targeted ADC (HS-20089) is also progressing rapidly, with a Phase III clinical trial for ovarian cancer already initiated.

In addition, new-generation ADC projects, such as the bispecific antibody ADC targeting EGFR/c-Met (HS-20122) and HS-20108, were approved for clinical research for the first time in the first half of the year, demonstrating the company's continuous iterative capability on the ADC technology platform.

In the globally most-watched weight-loss drug sector, Hansoh Pharma has also secured a favorable position.

HS-20094, a self-developed GLP-1/GIP dual receptor agonist by Hansoh Pharma, is currently advancing Phase III clinical trials for obesity or overweight indications, with over a thousand subjects having been dosed in the related studies.

In June 2025, Hansoh Pharma and Regeneron reached an exclusive overseas licensing agreement for HS-20094. Hansoh received an upfront payment of $80 million in July and is eligible to receive up to $1.93 billion in milestone payments as well as future sales royalties.

Securing such a significant deal with top global pharmaceutical companies not only brings substantial non-dilutive funding to Hansoh Pharma but also serves as an authoritative endorsement of the product's "best-in-class" potential. This move also cleverly addresses the challenges Hansoh faces in conducting large-scale Phase III clinical trials and commercialization in overseas markets. As competition in the weight-loss pipeline intensifies, obtaining definitive cash flow early on is becoming increasingly crucial.

Beyond oncology and metabolism, Hansoh is systematically building its third growth pillar in the field of autoimmune diseases.

The company has adopted a strategy of "introduction + self-research". The HS-20137, an IL-23p19 targeted monoclonal antibody drug introduced from Quanxin Biologics for the treatment of moderate to severe plaque psoriasis, has entered Phase III clinical trials during the reporting period. Meanwhile, the self-developed HS-10374, a TYK2 selective allosteric inhibitor and a potential next-generation oral autoimmune blockbuster drug, is also actively advancing in Phase III clinical trials for the same indication.

The most commendable aspect of Hansoh's transformation lies in its smooth process.

While the business structure has undergone fundamental changes, the company's overall revenue scale has not experienced sharp fluctuations or declines but instead maintained robust double-digit growth.

The key to achieving this lies in the company's clear planning and precise execution regarding the lifecycle of both new and old businesses.

The growth of innovative drugs has fully and more than covered the expected contraction of the generic drug business. According to the latest disclosed interim report, in the first half of 2025, the sales revenue of innovative drugs and collaborative products accounted for 82.7% of the total revenue. In the future, with the continuous commercialization of innovative drugs and collaborative products, the company's growth will enter a new phase, and the revenue scale of the generic drug sector will shift smoothly.

Hansoh's growth engine has completely "decoupled" from the policy risks associated with its generic drug business.

Hansoh Pharma has successfully pioneered a transformation path for Chinese pharmaceutical enterprises: utilizing the substantial cash flow generated by mature businesses to continuously fund the high investment and high-risk R&D of innovative drugs, while closely following the rapid development of the innovative drug business, and precisely completing the transition between old and new growth drivers.

In the 2025 interim report, from financial data, business structure to R&D pipeline, Hansoh Pharma has demonstrated all the core characteristics of a mature Biopharma: innovative products as the absolute revenue pillar, a late-stage pipeline with global competitiveness, a sustainable R&D platform, and the ability to maximize pipeline value through BD transactions.

Its success provides a clear and validated evolutionary path for numerous large traditional pharmaceutical enterprises in China. In the future, more companies in China's pharmaceutical industry will attempt and achieve this leap, while Hansoh Pharma has already set a new benchmark on this journey.

Rooted in Shanghai and radiating globally, PharmaCircle, as a biopharmaceutical industry-level strategic platform, is committed to the mission of "enabling the unrestricted flow of intelligence and connections." It builds a comprehensive industrial chain empowerment system covering drug research and development, production, distribution, and commercialization. Through four core engines—intelligent cloud services, precise resource linking, an industry think tank, and ecosystem communities—it creates the infrastructure for value flow in China's pharmaceutical sector.

Under the dual waves of globalization and digitalization, PharmaCircle is redefining the circulation paradigm of pharmaceutical resources — it is not only a hub for information and networking but also a catalyst for industrial transformation. With China as the origin, we are weaving a global network of pharmaceutical intelligence, making every precise connection a catalyst for leapfrog growth of enterprises.