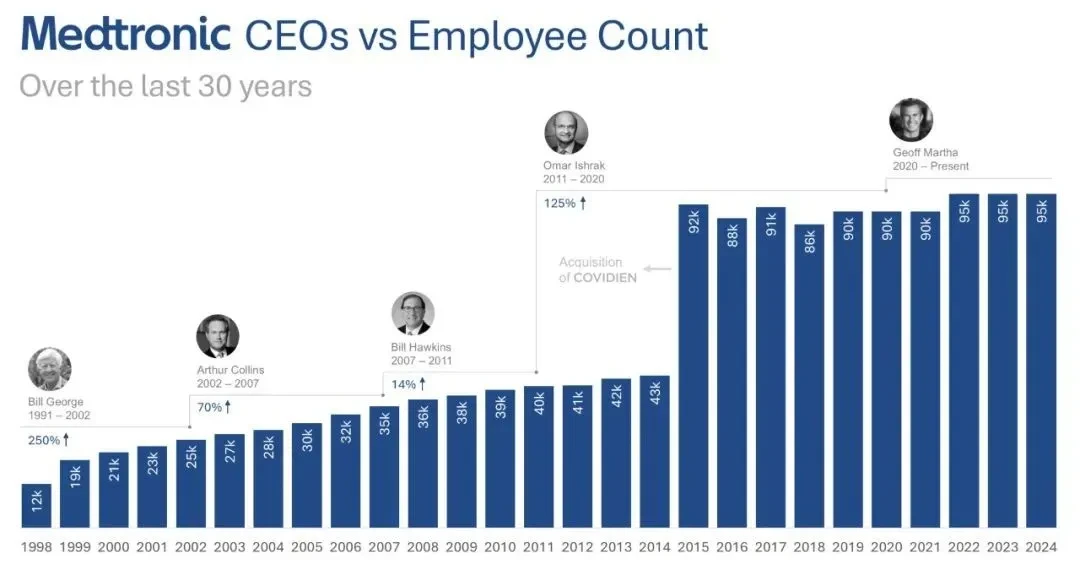

Ten years ago, Medtronic completed the largest acquisition in the history of the medical device industry ($43 Billion Acquisition of Covidien), this acquisition directly enabled Medtronic to surpass Johnson & Johnson, securing the top position in the medical device industry, and maintaining its leading position for a decade.Big Brother GloryTo make Medtronic the most renowned medical device company globally and become the goal in the hearts of countless medical device companies in China, aspiring to become a company like Medtronic.The halo of being the "big brother" of devices has brought Medtronic countless honors, but it has also become a heavy burden for the company. The number of employees has nearly doubled, yet profits have seen almost no growth over the past decade. More alarming is...The ability of "profit creation per capita" has plummeted from the top of the industry to the average level, which means Medtronic is no longer a top-tier company in the industry (but rather a large yet mediocre enterprise). ThereforeJeffAfter Martha took the stage, she began to reduce the burden by divesting or selling "non-promising" businesses, bringing Medtronic back to its pre-century merger profitability level. Recently, Medtronic announced the spin-off of its low-profitability diabetes business.Overseas bloggers analyze the changes after Medtronic's acquisition of Covidien from three aspects:Although the employee scale is an unconventional performance indicator, it profoundly reflects the growth trajectory of a company—because it is directly linked to labor costs (such as salaries and benefits, training investments, office expenses, etc.), often forming a core part of a company's operational expenditures.Looking back at history, Medtronic has continued to expand based on three core areas: cardiovascular, restorative therapies, and diabetes. Through a combination of organic growth and strategic acquisitions, the company maintained steady employee growth before 2015.The $43 billion acquisition of Covidien in 2015 marked a major turning point in strategic path. At that time, Medtronic had about 50,000 employees, and Covidien brought 40,000 new team members, making the acquisition essentially a merger. Covidien's differentiated product lines also gave rise to a new business unit - the Minimally Invasive Therapies Group.This acquisition has triggered multiple challenges: organizational restructuring, cultural integration, increased financial burden, and a sharp rise in operational complexity. The merger of the dual headquarters led to significant functional overlaps, ultimately resulting in a wave of executive departures (including layoffs and early retirements).After completing the largest acquisition in the history of the medical device industry, Medtronic has continued to integrate Covidien's operations, divesting low-margin businesses to restore financial health. In terms of workforce data, the total number of employees has remained basically unchanged after the acquisition.

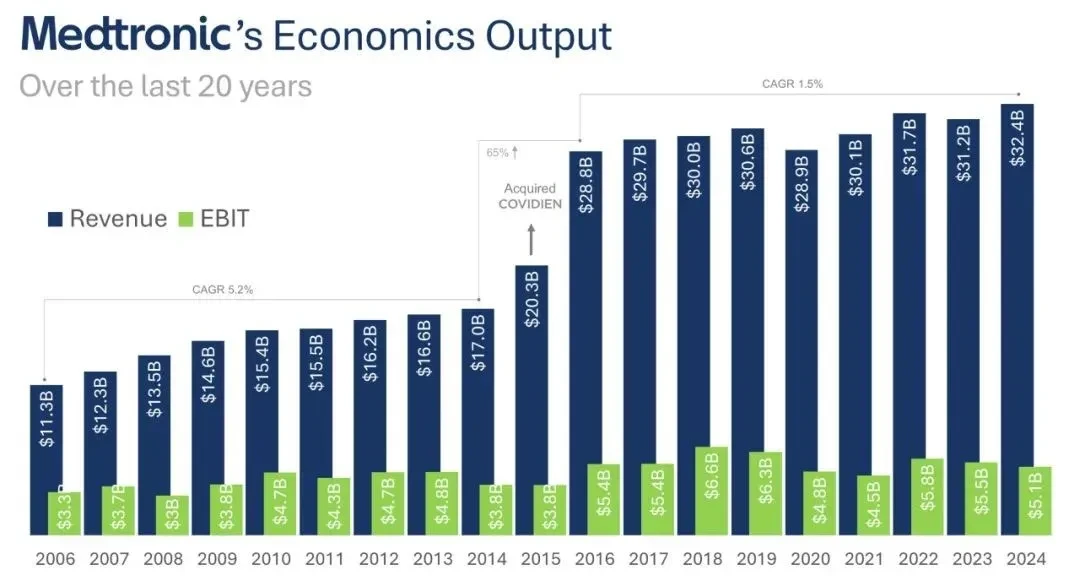

- Changes in Revenue and Profit

Before the acquisition, Medtronic achieved steady revenue and profit growth through organic expansion in its core markets and a series of strategic bolt-on acquisitions.

Despite the seemingly promising blueprint for mergers and acquisitions, challenges lurked beneath the surface. Before acquiring Covidien, Medtronic maintained an annual compound revenue growth rate of over 5%, reaching $17 billion in 2014; after the acquisition, its revenue surged to $29 billion in 2016, making it the top medical device company globally by revenue. However, following this brief surge, growth nearly stagnated—with a compound annual growth rate of only 1.5% over the next eight years, resulting in a cumulative increase of just 10% by 2024, with revenue settling at $32 billion.

More critically, despite both revenue and employee size doubling, operating profit has remained stagnant at around $5 billion. This completely deviates from management's promise that "mergers and acquisitions will create significant synergies," and instead reveals a further decline in organizational efficiency, ultimately eroding the foundation of profitability.

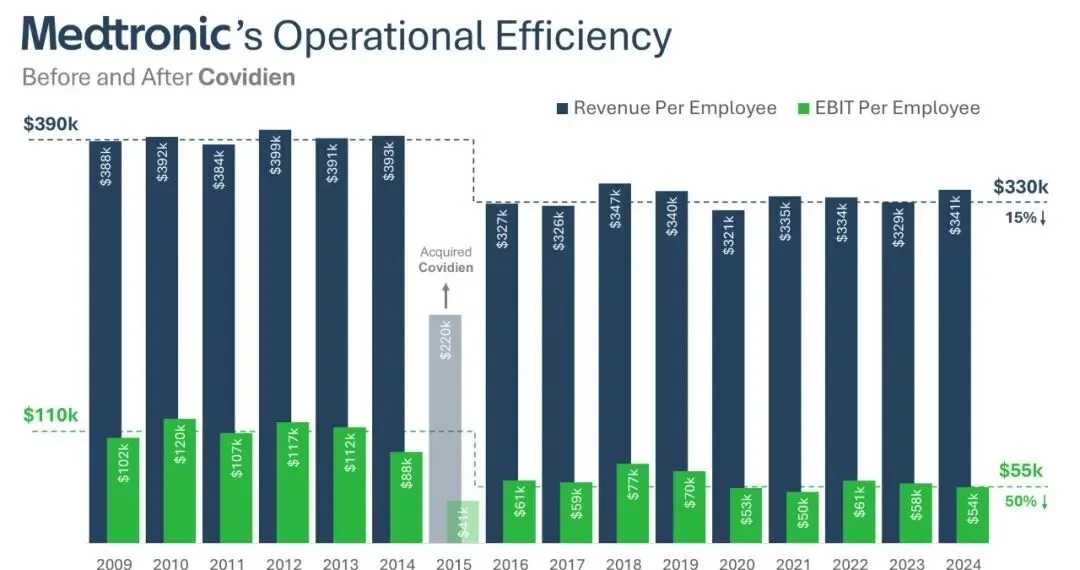

The core indicators for measuring operational efficiency are "Revenue per Employee" and "Profit per Employee." These two metrics quantify the effectiveness of a company's use of human capital to create value: an upward trend usually indicates improved productivity, economies of scale, or optimized cost control; conversely, it may suggest inefficiency, profit pressure, or overcapacity.

Historically, Medtronic once led the medical technology industry with approximately $400,000 in "revenue per employee." However, after acquiring Covidien, this figure dropped sharply by 15% to $330,000, bringing it closer to the industry average.

More critically, before the acquisition, Medtronic's "profit per employee" exceeded $100,000, firmly placing it at the top of the industry. After the acquisition, this figure was halved, slipping to the industry average. This indicates that the merger caused Medtronic to lose its competitive edge in operational efficiency and financial performance, falling from the top tier to mediocrity. Surprisingly, ongoing restructuring and asset divestitures have failed to reverse this trend.