Three Years of Price Wars Haven't Killed Innovation in China's Oral Care Industry

Medgen Life Sciences

Orthopedic Sports Medicine Product Developer

DeepCare

Developer of AI-Powered Dental Imaging Analysis Systems

Fortune Capital

Venture Capital Institution

Recently, the Guangdong Private Dental Association released an initiative on "addressing low-price and disorderly competition" through its official WeChat account, with its content repeatedly mentioning"No dumping below cost price," "No诱导ing patients with low-price引流," "Reject false discounts and price traps," "Reject transferring cost pressure by squeezing upstream suppliers."Words like these directly point to the negative effects of the "bleeding price cuts" in the dental industry in recent years.

According to data from Good Teeth DataLab,In the first half of 2024, 2,401 oral medical service institutions in China were "deregistered + revoked," doubling the total number for the entire year of 2023.This directly leads to an exacerbation of industry chaos, with founders absconding, employee wages being delayed, patients unable to get refunds, and an increasing number of malicious incidents such as medical complaints. A trust crisis is rapidly spreading throughout the dental industry.

As a result, oral enterprises that previously enjoyed exorbitant profits and high growth now have to face the harsh reality of shrinking performance and narrowing profit margins. According to the latest semi-annual reports, not only have revenues of numerous oral enterprises declined, but net profits have also fallen to the million-yuan red line. Even though some companies can maintain growth, their growth rates are significantly lower than before, generally around 10%-20%, a substantial slowdown from their peak periods.

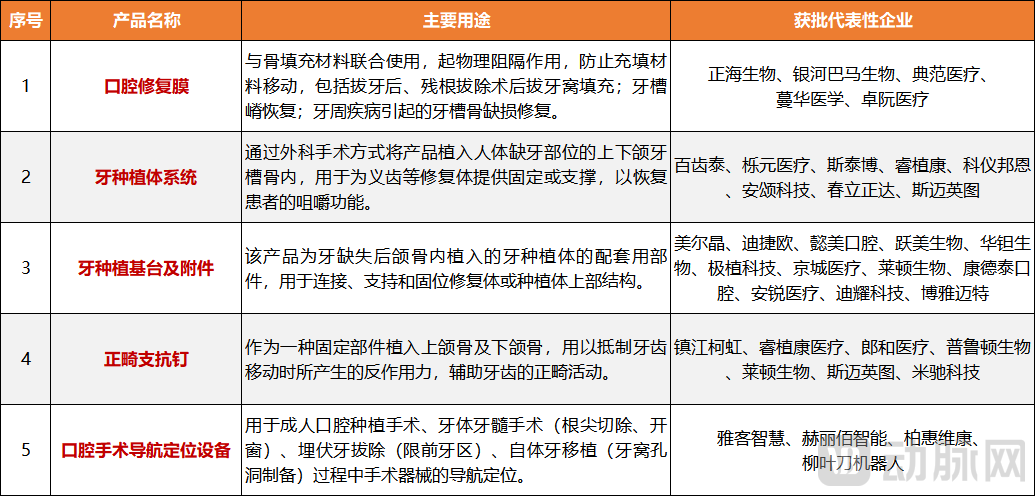

Figure 1. Representative dental products and their affiliated companies approved for Class III certificates in the first half of 2025

Figure 1. Representative dental products and their affiliated companies approved for Class III certificates in the first half of 2025

However, on the other side, the innovation process of China-produced oral enterprises is unexpectedly accelerating. According to VCBeat's collation and statistics,In the first half of 2025, the National Medical Products Administration approved the registration of 157 dental medical device products, including 110 Class III medical devices produced in China, ranking among the top in various subfields.Among these, several heavyweight products have emerged. For instance, the "Caries Oral Panoramic Image Auxiliary Detection Software" independently developed by Beijing Feather Medical Cabbage Information Technology Co., Ltd., which is the first Class III certificate approved in the field of oral artificial intelligence in China. Additionally, "Beigebone," the latest product launched by Medgen Life Sciences, was approved for marketing in March this year and is China's first porcine bone oral bone filling material.

The dental industry in 2025 seems to stand at a crossroads, with one side being the market downturn caused by price wars in dental services, and the other side seeing the successive approval and market launch of cutting-edge innovative products. These two starkly contrasting conditions seem to be proving to us that:Only innovation is the true way to break through the current disordered competition in the dental industry.。

Three Years of Price Wars in Dentistry: No Winners!

In December 2022, the proposed winning results of the centralized volume-based procurement of orthodontic bracket consumables for the alliance of 16 provinces (autonomous regions, corps) led by Shaanxi Provincial Medical Insurance Bureau, including Shaanxi, Shanxi, Inner Mongolia, and Liaoning, were announced. A total of 572 products from 32 companies were selected, with an average price reduction of 43.23% and a maximum reduction of 88%. One month later, the inter-provincial alliance procurement of dental implant systems, guided by the National Healthcare Security Administration and led by Sichuan Provincial Medical Insurance Bureau, was held in Chengdu, Sichuan. A total of 39 companies were selected, with the average winning price as low as over 900 yuan, and the average price reduction reached 55%.

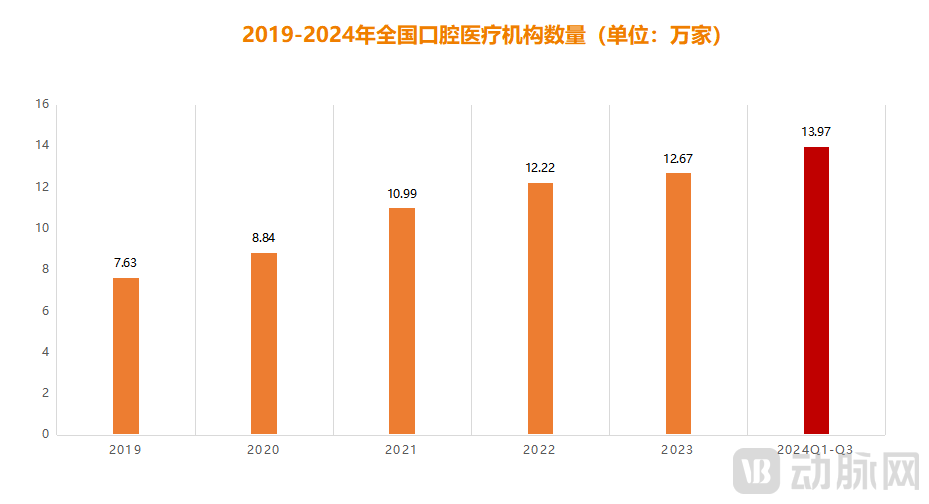

Figure 2. Number of oral medical institutions in China from 2019 to 2024 (Data source: CICC Research Institute)

Figure 2. Number of oral medical institutions in China from 2019 to 2024 (Data source: CICC Research Institute)

As two of the highest-profit projects in the dental industry, dental implants and orthodontics once enjoyed immense popularity and were considered shortcuts to financial freedom. There was even a saying: "Break-even in one year, comfortable living in two years, and immense wealth in three years." However, with the successive implementation of centralized procurement policies, the "easy money era" of the dental industry has officially come to an end. To maintain performance, many dental institutions have been forced into large-scale competition. Meanwhile, the explosive growth of new entrants driven by capital fever has further intensified the situation.In 2023, the number of dental medical institutions in China has soared to 126,700, increasing by more than 60% in four years, further intensifying the survival pressure in the dental industry.Force.

As a result, a "price war" that engulfs the entire market ensues.

At first, everyone could still repeatedly probe within a rational price range, but the good times didn’t last long—soon, the market was swept by an almost frenzied ultra-low price trend:"99-yuan orthodontic trial package," "1-yuan group-buying dental implant," "9.9-yuan resin tooth filling," and "free teeth cleaning" are among the endless low-price bombardment advertisements.。

But this did not yield the desired results. From a corporate perspective, extremely low profits or even loss-leading marketing, while attracting some customers to a certain extent, resulted in a very low conversion rate afterward. The vast majority only stayed at the "freebie-grabbing" stage.This kind of "burning money to gain market" behavior not only failed to make profits for the companies but also significantly increased the medical burden on dental institutions."A dentist commented on this, 'Generally, during such promotional events, we are busy from morning till nine or ten at night. Most of the visitors are middle-aged and elderly people, and they basically won't make repeat purchases.'"

Figure 3. Some dental companies with revenue declines in the first half of 2025 (Data source: Annual reports of enterprises)

Figure 3. Some dental companies with revenue declines in the first half of 2025 (Data source: Annual reports of enterprises)

Moreover, the low price will significantly diminish the brand influence of dental enterprises and institutions, causing some consumers to question their professionalism and reliability, thereby weakening their market competitiveness—a situation that is not worth the loss.

Compared with dental enterprises, consumers seem to have benefited from the "price war," but in fact, they have not.On the one hand, it is the overall decline in the quality of medical treatment brought about by low prices.According to data from the Shanghai Consulting Group, there were 15,000 complaints related to dental medical services in 2022, marking a 25% year-on-year increase and ranking first among medical-related complaints. This is actually due to the influx of low-quality consumables and "quick-trained" doctors into the market as a result of price-cutting trends, leading to frequent dental medical accidents.On the other hand, there is a significant increase in hidden consumption.Some dental institutions first attract customers with low prices, and then increase charges layer by layer during the treatment process by switching projects, breaking down fees, overcharging for additional items, or creating their own similar services, trapping consumers in the "low-price attraction followed by high-price exploitation" scheme.

In this regard, an investor in the dental field stated, "An obsessive focus on undercutting prices is definitely not the way forward for the dental industry. This extreme form of malicious competition will only lead everyone to fixate on price, completely ignoring the essence of healthcare. The ultimate outcome will be that dental companies won’t make money, frontline institutions can’t sustain themselves, and patients won’t receive quality treatment—there will be no winners from top to bottom. Therefore, in the long run..."The current 'Pinduoduo' model in the dental industry is far more aggressive than bulk procurement. It not only squeezes profits but also destroys the entire value system.。”

Fortunately, this disorderly competition is coming to an end, and everyone is currently trying to find ways to break out of the "price war" cycle.

After the Price War, Is a New Round of Innovation on the Way?

Everything has two sides. The "price war" in the dental industry is not only a crisis for survival but also an opportunity for transformation and upgrading. How to seize the opportunity lies in innovation. The industry has reached a consensus on this. Although the "price war" has led to a decline in revenue and profits, the commitment to investing in innovation has never been stronger.

From the previously mentioned approved volume, in the first half of this year, there were over a hundred products in the dental field that obtained Class III certificates, accounting for almost one-fifth of the total number of Class III certificates for medical devices approved during the same period. Secondly, in terms of R&D investment, according to an analysis of the semi-annual reports this year,The R&D investment of oral enterprises generally increased by 5% to 10%, a figure that is even higher than the average investment during the industry's peak period.Taking Invisalign, the pioneer of invisible orthodontics, as an example, it invests over 300 million US dollars in R&D annually, a figure that is close to 10% of its annual revenue.

Figure 4. Innovation investment cases in China's dental field in the past one and a half years (Data source: VCBeat)

Figure 4. Innovation investment cases in China's dental field in the past one and a half years (Data source: VCBeat)

Finally, from the perspective of the capital market, investment in the dental field began to gradually recover starting from 2024, with a focus on innovative products and breakthrough technologies in the dental sector. According to incomplete statistics from the VCBeat database,In the past one and a half years, innovation investment in China's dental field has exceeded 2 billion yuan。

So, what are the core breakthroughs in this wave of innovation in the dental industry? Which cutting-edge products are reshaping the market landscape?

This needs to be viewed from two aspects,On one hand, the focus is on innovation in dental materials, primarily through cutting-edge technologies to make the materials more compatible with the oral environment. This enhances their biocompatibility, durability, and aesthetics, thereby improving treatment outcomes and patient experience.。

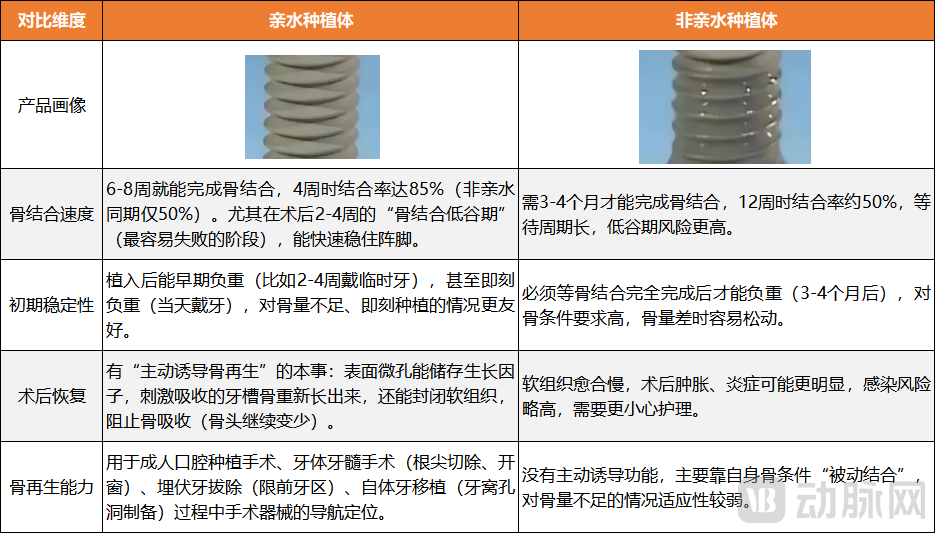

Figure 5. Comparison of hydrophilic and non-hydrophilic implant performance

Figure 5. Comparison of hydrophilic and non-hydrophilic implant performance

Taking dental implants as an example, the most popular and industry-focused option currently is undoubtedly hydrophilic implants. These achieve a transformation from "hydrophobic" to "super-hydrophilic" through special chemical or physical methods. This change attracts proteins and osteoblasts from the blood and significantly accelerates the speed of osseointegration, reducing the healing period from the traditional 3-6 months to just 3-4 weeks. Additionally, the hydrophilic surface reduces fibrinogen adsorption, thereby minimizing postoperative swelling and inflammatory responses, allowing patients to recover more comfortably.

In the view of many industry experts, high-end titanium implants are currently trending towards "super-hydrophilic" development, which is considered a new trend in modern implantology. At present, several dental companies in China are deploying this new technology. Among them, the "SLApro Super-Hydrophilic Implant," independently developed by Wuxi Shuiqing Medical, was mass-produced and launched in May 2025. It is capable of increasing bone healing speed by 25%, with an expected annual production capacity of over one million sets.

Focusing further on the orthodontics field, the continuously evolving SmartTrack material is undoubtedly the current highlight. As one of the core technological breakthroughs of the Invisalign system, it features excellent elasticity and toughness. While consistently applying gentle and constant corrective forces, it precisely conforms to the tooth surface, enabling refined control over complex tooth movements and significantly enhancing wearing comfort. At present, SmartTrack has become the "gold standard" material in the invisible orthodontics field.

On the other hand, innovation is embodied in the comprehensive optimization and enhancement of digital technology in the field of dentistry.Firstly, in the examination process, taking YOFO's Hirox-O (Xin CT) as an example, this is the world's first spiral oral CBCT with a maximum spatial resolution of up to 28lp/cm. It can accurately capture every detail inside the mouth and obtain CT, 3D panoramic, and 3D lateral views in one shot. Additionally, it can generate 3D and TMJ views, which significantly enhances the operational efficiency and accuracy of oral examinations.

Figure 6. YOFO Medical Hirox-O (CT) Product GIF (Source: Company Official Website)

Secondly, in the treatment process, taking dental implant surgery as an example, current digital technologies can precisely plan the position, depth, and diameter of implants. With the help of 3D-printed surgical guides or dynamic navigation systems, millimeter-level virtual plans can be accurately "transferred" to the patient's oral cavity, achieving minimally invasive, flapless, and one-step implant placement. Orthodontic treatments have also achieved qualitative breakthroughs through digital technology. Taking the critical step of impression-taking as an example, traditional methods mainly relied on silicone impressions, which were not only less accurate but also caused significant discomfort. However, digital technology has greatly improved this aspect. For instance, the "iTero Lumina™ Pro" digital intraoral scanner introduced by Align Technology offers a smaller scanning head while providing a wider field of view and deeper capture range, achieving a triple upgrade in precision, comfort, and efficiency.

Finally, in the post-diagnosis and rehabilitation stages, whether it is for implants or orthodontics, this is a rather lengthy treatment process, making follow-up visits particularly crucial.The integration of digital technology can help doctors achieve full-cycle precise tracking and personalized intervention for patients, thereby building a complete closed loop of "data collection - intelligent analysis - dynamic adjustment - continuous feedback," further ensuring the treatment effectiveness.。

This shows that digital technology is reshaping the value system of the entire dental field, driving it towards a more precise, efficient, and personalized direction. A senior investor expressed agreement, stating, "Digital technology will undoubtedly be the key driving force for continuous innovation in the dental field in the future. In the past few years, we have already seen some innovative results in the market, but this is far from enough. Potential scenarios such as bioprinters growing live gum tissue chairside or using a patient's digital twin to simulate occlusal wear ten years from now still need to be realized through digital technology."Therefore, the integration and innovation of digital technology in dentistry have only just begun.。”

The Billion-Dollar Dental Market: Still Brewing Undercurrents

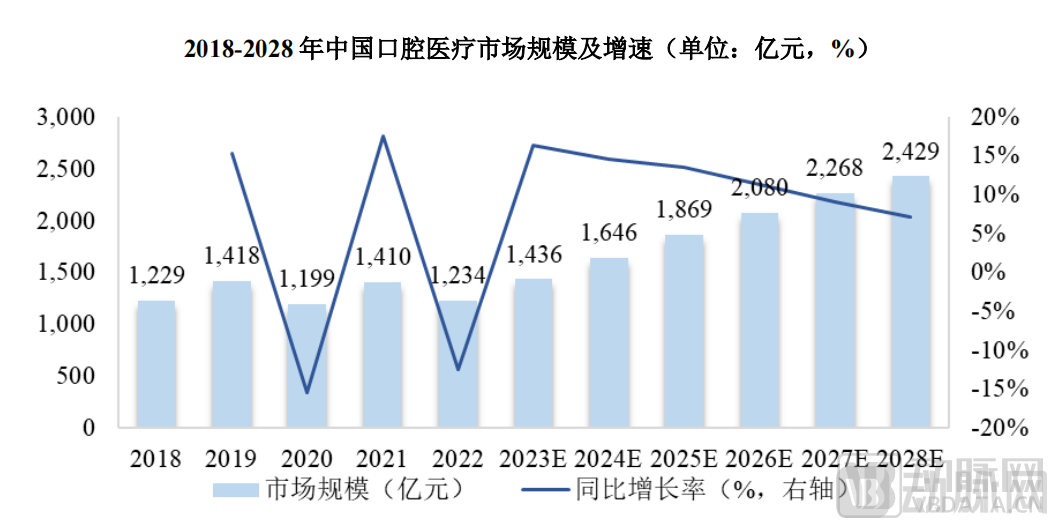

Figure 7. The Scale and Growth Rate of China's Dental Medical Market from 2018 to 2028 (Source: Frost & Sullivan)

Figure 7. The Scale and Growth Rate of China's Dental Medical Market from 2018 to 2028 (Source: Frost & Sullivan)

According to data from Sullivan and Zhongtai Securities Research Institute,From 2018 to 2028, the market size of China's dental medical industry will grow from 122.9 billion yuan to 242.9 billion yuan, with a compound annual growth rate of 7.1%.Undoubtedly, this is still a market full of imagination, but in the process of rapid growth, the dental industry has also undergone some structural changes.

For example, in market demand,The current dental industry is showing a distinct "bimodal structure.": On the one hand, the accelerating aging population has led to a surge in the demand for dental restoration among people over 65 years old. It is expected that by 2030, this group will account for 39.2% of the market. On the other hand, the "Generation Z" is gradually becoming the main consumer force, driving the invisible orthodontics market to grow at an annual rate of 25%. Among them, the 25-34 age group contributes more than 60% of orthodontic consumption.

Secondly, in the application process,At this stage, the dental industry has transitioned from disease treatment to functional enhancement and aesthetic improvement, giving the dental market a high degree of consumer attributes.Therefore, the vast majority of patients, while pursuing higher quality medical care, also have high demands for the medical experience, such as reducing treatment pain, shortening the lengthy medical cycle, and decreasing the frequency of visits. These have now become key factors in choosing a dental institution.

Finally, at the market level,Third- and fourth-tier cities, as well as county-level regions, have become the "main battleground" for future growth.Currently, the regional differences in the dental healthcare market are becoming increasingly evident. In first-tier cities where capital has been quick to establish a presence, there are already 8.2 clinics per 100,000 people, leading to intense industry competition and customer acquisition costs as high as 2,000 yuan per person. In contrast, the density of clinics in third- and fourth-tier cities, as well as county-level markets, is generally only one-fifth that of first-tier cities. However, the market growth rate reaches 18%, significantly higher than the average level. This indicates that the potential in these lower-tier markets is enormous and will be a crucial battleground for the dental industry’s future growth trajectory.

Different market demands, of course, require different products and business strategies. In this regard, the founder of a certain dental enterprise mentioned, "The future growth momentum of the dental industry will mainly come from three dimensions: efficiency improvement driven by technological innovation, new value created by service innovation, and incremental space brought by market expansion.”

Thus, an industrial innovation revolution in the dental field is taking place, and to break through, there are only two key points:One aspect lies in the products, where technological innovation is pursued to achieve higher quality while also creating differentiation and developing truly groundbreaking products with technical barriers; the other aspect focuses on the enhancement of oral care services, embedding and integrating digital technology more deeply to realize a full-chain upgrade from prevention, diagnosis, treatment to aesthetics.。

This is a new round of innovative challenges in the dental industry, as well as an unprecedented market opportunity.

1. "2025 Dental Industry Survival Guide: 30% Clinics Closing, How Will Institutions Survive?" —— Fan Mou You Dao;

2. "Overview of Dental Instrument Industry Approvals and Listings in the First Half of 2025" — CAMDI Dental Committee;

3. "Dental Implant Gross Profit Halved, How Can Dental Chains Still Make Money?" — Taurus Research Institute;

4. "Crazy Price Wars Are Not the Way Out for the Dental Industry" — VCBeat.