Spin-off of Siemens Healthineers: Industrial Giants and the Strategic Divergence in MedTech – A GPS Comparative Analysis

Siemens Healthineers

Integrated Healthcare Service Provider

GE Healthcare

Digital Solution Provider

On October 2, 2025, foreign media reported that Siemens AG is studying the divestiture of most of its shares in Siemens Healthineers. The specific method might be through a direct spinoff, where the parent company no longer retains shares but directly distributes them to all shareholders in the form of stock dividends according to their shareholding ratio.

Following the announcement, Siemens' stock price rose nearly 3% on the same day, and the market value of Siemens Healthineers stabilized at approximately 52 billion euros.

This is not a simple equity operation, but a major event that impacts the global medical technology industry landscape.

SiYu MedTech believes that this news is worth observing from two dimensions:

Horizontal Comparison of GPS:Similar to Siemens, Philips and GE have also undergone the "split and integration of group and healthcare business.", A comparison of the paths among the three can clearly reveal the industry logic.

Looking Back at the Development Process Longitudinally: Back to the historical context,Why did medical businesses initially emerge within large industrial groups? And why do they generally become independent today?

The medical technology industry is a sector with long-term stable growth, but for companies to grow bigger, they need to become"Friend of Time". This not only means patient capital investment, but also means making crucial decisions at key moments.Forward-looking strategic choices.

In this article, Siyu MedTech will focus on analyzing the "GPS" – the different paths of the three giants GE, Philips, and Siemens – and, combining their historical backgrounds and capital market logic, provide some references and insights for Chinese conglomerates in their medical business layouts.

The Similarities and Differences in the Tripartite Standoff:

Insights into the Current State of GPS Giants

In the global medical technology industry,Siemens Healthineers、GE HealthCareandPhilipsRegarded as the "GPS giants." Although all three companies originated from large industrial groups, they have now embarked on different strategic paths:Siemens Healthineers remains under the strong control of the group; GE HealthCare has completed its independent listing; Philips, through the long-term divestment of non-core businesses, has transformed into a pure medical technology enterprise.

As ofFiscal Year 2024, the scales of the three companies have all reached tens of billions of euros/dollars:

Siemens Healthineers: Revenue approximately22.36 billion eurosThe four major segments—Imaging, Diagnostics, Varian (Radiation Therapy), and Advanced Therapies (Interventional Treatments)—form a complete system.

GE HealthCare: Revenue approximately$19.7 billion, mainly covering imaging, ultrasound, patient monitoring/anesthesia and respiratory care, as well as the distinctive Pharmaceutical Diagnostics.

Philips: Sales approximately18 billion euros,with a focus on three major segments: Diagnosis & Treatment, Connected Care, and Personal Health.

At the group relationship level, the three companies are also at different stages:

Siemens Healthineers is still 71% owned by the group, but a possible spin-off is under discussion.

GE HealthCare Technologies, Inc. completed its full spin-off in 2023 and moved towards independent operation in the capital market.

Philips has undergone more than two decades of divestment, becoming thoroughly "medicalized."

Next, we will analyze the current status of the three companies one by one, comparing them from the perspectives of business structure, financial performance, market risks, and strategic direction.

Siemens Healthineers

1. Relationship with the Group

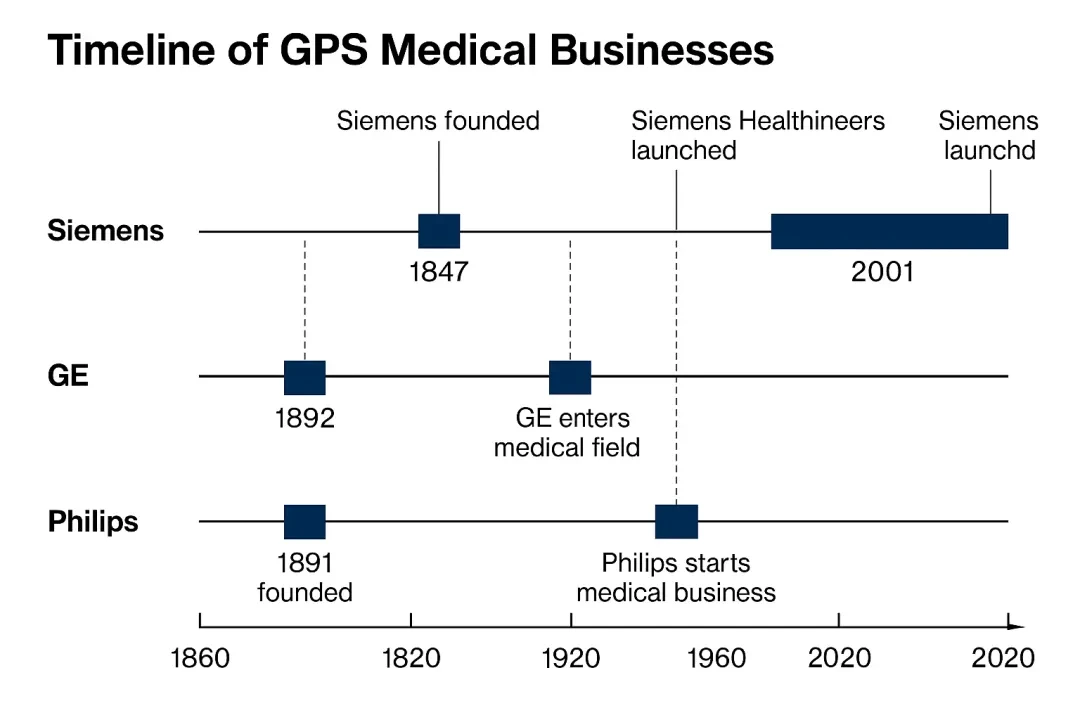

Siemens Healthineers originated earliest from1896The development of X-ray equipment marks one of the earliest entries into the medical imaging field globally. In 2018, it was spun off and listed from Siemens Group (Frankfurt Stock Exchange), but the parent company still retains absolute controlling status.

As of 2025, Siemens Group holds approximately71% Shares, remains the controlling shareholder of Siemens Healthineers. This year, foreign media reported that Siemens is studying a "direct spin-off" and considering distributing its shares to shareholders, which could mean the parent company might gradually exit its controlling stake.

2. Business Structure

Siemens Healthineers has currently established the most comprehensive medical technology product system globally, primarily divided into four major segments:

Imaging (Medical Imaging):MRI, CT, ultrasound, and X-ray are the core sources of income.

Diagnostics (In Vitro Diagnostics): Including laboratory diagnostics and rapid testing, which once contributed to explosive growth during the pandemic.

Varian (Radiation Therapy): Invested in 202013.9 billion eurosAcquisition of Varian Establishes Leadership in Radiation Oncology Equipment.

Advanced Therapies (Advanced Interventions): Focusing on catheterization lab imaging and minimally invasive surgical navigation, strengthening the interventional treatment layout.

This combination of "imaging + diagnostics + radiotherapy + intervention" enables Siemens Healthineers to cover the entire chain from diagnosis to treatment, creating a differentiated competitive edge against GE Healthcare and Philips.

3. Financial Performance (FY 2024)

Revenue Scale: ApproximatelyEUR 22.36 billion, a slight increase year-on-year.

Division Contribution:

Imaging About13.2 billion euros, remains the mainstay of revenue.

Diagnostics Approximately4.7 billion euros, due to the withdrawal from antigen testing, revenue declined.

Varian Approximately4.1 billion euros, the integration effect is gradually becoming apparent.

Advanced Therapies ApproximatelyMore than 3 billion euros, maintaining stability.

Profit Margin: The overall gross margin declined due to the drag from the diagnostics business, but the quality of profitability gradually improved as the business base recovered after the pandemic.

4. Current Highlights and Risks

Refinancing Pressure: Siemens Healthineers currently has approximately€13.9 billion in debtOf which approximately 9.4 billion euros are internal loans provided by the parent company, and if the holding structure changes, this portion will need to be refinanced or repriced. Investment banks estimate an annual increase of approximately70 to 125 million eurosFinancial expenses.

Market Volatility: From 2024 to 2025, China's market demand will be affected by the policy environment and the high base after the pandemic, leading to a slowdown in growth. However, in the medium to long term, it will remain the core growth engine.

Strategic ValueIf Siemens Group completely exits its controlling stake, Siemens Healthineers may achieve a higher capital market valuation, but it will also face challenges such as rising financing costs and independent operation.

GE Healthcare

1. Relationship with the Group

GE Healthcare is one of the oldest businesses under General Electric (GE), with origins dating back toEarly 20th CenturyGE produced early X-ray machines in the 1900s.

In January 2023, GE fully spun off its healthcare business, and GE HealthCare became an independent publicly listed company (NASDAQ: GEHC), ending over a century of "parent-subsidiary" relationship. This spin-off is one of the most significant strategic adjustments in GE's history, with the group itself transitioning to focus on...Aviation (GE Aerospace)andEnergy (GE Vernova)。

GE HealthCare is now completely independent, with its management, capital structure, and debt arrangements fully separated from the parent company.

2. Business Structure

GE HealthCare currently has four major business segments:

Imaging (Medical Imaging): Including MRI, CT, PET/CT, and X-ray, it is the largest segment.

Ultrasound (Ultrasonic): Global leader, covering cardiology, obstetrics and gynecology, whole-body imaging, etc.

Patient Care Solutions (Monitoring and Treatment): Includes anesthesia machines, ventilators, and monitoring systems, and is an important equipment supplier for ICUs and operating rooms.

Pharmaceutical Diagnostics (Drug Diagnostics/Nuclear Medicine): Mainly produces contrast agents and radiopharmaceuticals for nuclear medicine, a business that is uniquely characterized among the three giants, bringing GEHC dual growth in equipment + consumables.

3. Financial Performance (FY 2024)

Revenue Scale: Approximately$19.7 billion, a slight year-on-year increase (+1% approximately).

Division Contribution:

Imaging: Exceeding$10 billion, maintaining a core position.

Ultrasound: Approximately$3.5 billion, with stable growth.

Patient Care Solutions: Approximately$4 billion, driven by the demand for ICU/anesthesia monitoring.

Pharmaceutical Diagnostics: Approximately$2 billion, increasing by more than 10% year-on-year, becoming the fastest-growing sector.

Profitability: Revenue for the fourth quarter of 2024$5.3 billion, up 2% year-on-year, with significant improvements in net profit and EPS. The overall operating profit margin has been increasing quarter by quarter, and cash flow remains robust.

4. Current Highlights and Risks

Fluctuations in the Chinese Market: In early 2024, weakened demand in China pressured quarterly results, with a gradual recovery anticipated in the second half. For GEHC, China remains the second-largest market globally, and the pace of recovery will have a significant impact overall.

Product Highlights:

Omni Legend PET/CTSecuring Major Orders in the U.S. to Strengthen Imaging Competitiveness.

The pharmaceutical diagnostics business has performed outstandingly, particularly driven by the steady growth of PET radiopharmaceuticals (such as Vizamyl and Cerianna).

Long-term Strategy:

After becoming independent, its valuation is more transparent, and the capital market highly recognizes its "equipment + consumables" combination model.

The company emphasizes enhancing clinical workflows through a digital imaging platform and AI tools to maintain competitiveness.

Philips

1. Relationship with the Group

Philips was founded in1891, initially a light bulb manufacturer. Starting from the mid-20th century, Philips leveraged its strengths in optics, electronics, and vacuum tubes to enter the X-ray and medical imaging equipment fields. In the following decades, Philips continued to expand into medical areas such as ECG monitoring, ventilators, and ultrasound.

Over the past two decades, Philips has undergone a complete "de-multification" transformation:

In 2011, the television business was sold.

In 2016, the lighting business (Signify) was spun off.

In 2021, the home appliance business was sold.

Now Philips is almost entirely focused on medical technology and has become aPure Healthcare Technology Company, which is the most thorough transformation case among the three giants.

2. Business Structure

Philips' business is mainly composed of three major segments:

Diagnosis & Treatment (Diagnosis and Treatment): Including imaging diagnostics (MRI, CT, ultrasound), interventional treatment, and radiotherapy solutions, it is the largest segment.

Connected Care: Covering patient monitoring, sleep respiratory management, emergency and information solutions.

Personal Health (Individual Health): Including consumer health products such as oral care and electric shavers, the scale is relatively small but maintains a stable cash flow.

3. Financial Performance (FY 2024)

Overall Scale: Sales approximately18 billion euros, Adjusted EBITA Margin11.5%。

Division Contribution:

Diagnosis & Treatment: Approximately8.5 billion euros, Comparable Sales Growth +1%, Adjusted EBITA11.6%。

Connected Care: About5 billion euros, an increase of +2%, adjusted EBITA9.6%。

Personal Health: Approximately4.5 billion euros, maintaining stability in the global consumer health market.

Profit and Cash Flow: Although the overall recovery trend is evident, it is still hampered by one-off events, making execution a critical factor.

4. Current Highlights and Risks

Market Fluctuations in ChinaIn the fourth quarter of 2024, the Chinese market experienced a double-digit decline, putting pressure on the Diagnosis & Treatment and Personal Health segments; the company anticipates a mid-to-high single-digit decline in 2025.

External Disturbance: US-EU Tariff Policies May BringEUR 150-200 millionThe additional cost pressure.

Compliance and Cash Flow: In the first quarter of 2025, the company will have a one-time cash outflow due to settlements for U.S. custody and personal injury.Approximately 1.025 billion euros. Meanwhile, the three-year period€2.5 Billion Efficiency Enhancement ProgramProceed continuously.

Strategic Positioning: Philips no longer has the support of a corporate "parent," relying entirely on the market competitiveness of its healthcare technology. This signifies both strategic focus and the challenge of growth bottlenecks.

A Century in Retrospect: Healthcare Born from Industry

Independence Driven by Capital

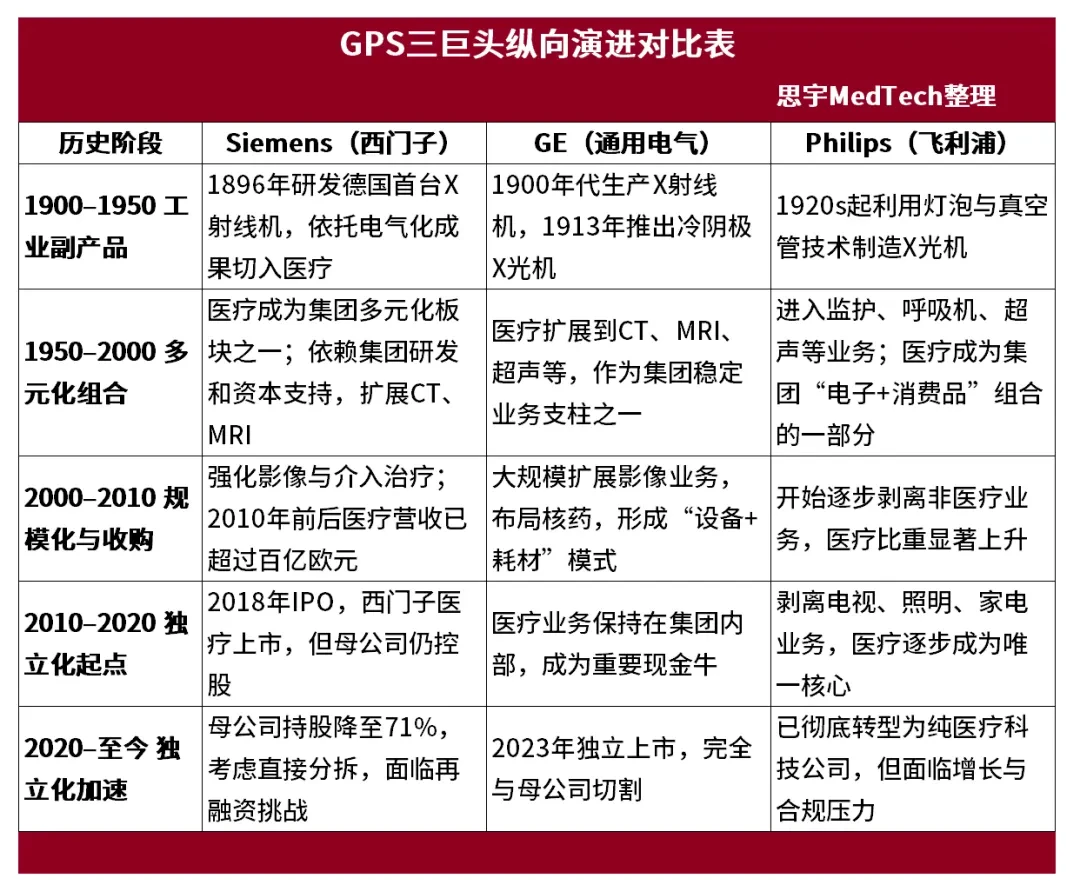

1. By-products of industrialization (1900–1950)

In the early 20th century, breakthroughs in electrification and physics gave birth to modern medical imaging.

SiemensIn 1896, Wilhelm Röntgen discovered X-rays, and Siemens quickly applied this to healthcare by developing Germany's first X-ray machine. This is a typical example of "industrial achievements applied to medical use."

GE: Also entered the X-ray equipment field in the 1900s, developing a cold cathode X-ray machine in 1913. As an extension of Edison Electric, GE naturally possessed electrical and vacuum tube technology.

Philips: Starting from light bulbs and vacuum tubes, entered the manufacturing of X-ray machines in the 1920s–1930s.

At this stage,Healthcare business is a byproduct of the industrial group.: Relying on the achievements of fundamental sciences such as electrical engineering, optics, and materials, they were transformed into medical imaging equipment. Independent medical companies were almost impossible at that time.

2. A Part of Diversified Portfolio (1950–2000)

After World War II, medical devices gradually entered the commercialization phase. At this time, the importance of medical business to the group increased, but it was still part of a "combination strategy":

Technical Dependence: The development of CT, MRI, and ultrasound relies on strong electronics, computer, and material research and development, which are precisely within the R&D systems of large corporations.

Capital Dependence: Large imaging equipment requires substantial investment, which can only be supported by the group's cash flow and channel network.

Industry LogicAgainst the backdrop of the Cold War and post-war industrial expansion, healthcare was regarded as an important component of corporate diversification rather than an independent core.

During this period, the medical businesses of Siemens, GE, and Philips continued to grow, but they remained closely tied to their parent groups.

3. Capital Market Drives Independence (2000–Present)

Entering the 21st century, the industrial attributes of medical technology have undergone a qualitative change:

Industry Scale: The global medical technology industry has reached an annual revenue scale of hundreds of billions of dollars, becoming a sufficiently independent and large-scale industry.

Profitability Characteristics: The medical business has high profit margins and stable growth, showing significant differences from the cyclicality of industrial manufacturing.

Capital Logic: The capital market has started to emphasize that "focused companies" have more valuation advantages, while "conglomerates" are at a discount.

This drives the three giants to pursue different paths towards independence:

Philips: The most thorough transformation, over 20 years divested lighting, home appliances and other businesses, fully transitioning into a medical technology company.

GE: Due to group debt and the burden of diversification, it was forced to split, and GE HealthCare was independently listed in 2023.

Siemens: Relatively conservative, Siemens Healthineers' IPO was only pushed forward in 2018, with the company still maintaining control, but now there are discussions about a potential spin-off.

4. Summary of Historical Logic

Starting Point: Technology spillover from industrial groups → Entering healthcare.

Mid-term: Group diversification expansion → Healthcare as a stable growth sector.

At this stage: The medical industry is large enough in scale → Independence can further unlock valuation and strategic flexibility.

SiYu MedTech Observation:

Friends of Time and Strategic Choices

1. Insights from the Global Triad: The Fork in the Strategic Path

As can be seen from the horizontal and vertical analysis, Siemens, GE, and Philips, although starting similarly, ultimately chose different strategic paths:

Philips: Actively transforming, over 20 years continuously divesting non-medical businesses, eventually becoming a "pure medical technology company." This is the most thorough choice, but it also means Philips has lost the buffer of industrial diversification.Fully exposed to the fluctuations of the medical technology market.

GE: Forced to spin off its healthcare business due to debt and diversification challenges. After GE HealthCare's independent listing, it gained higher recognition in the capital market, with a clearer valuation logic.GE itself focuses on aviation and energy, returning to its traditional strengths in heavy industry.

Siemens: It has consistently maintained a "dual-track" model of "industry + healthcare." The healthcare segment provides a stable cash flow, supporting the parent company's strategic investments in software and industrial digitalization. However, now,The pressure from the capital market and the need for financing have forced Siemens to consider further spin-offs.

These three pathways illustrate,Medical businesses, even if born within industrial groups, will eventually move towards a strategic choice of "independence.". The independent rhythm and approach merely depend on the strategic orientation and financial status of the parent group.

2. Special Attributes of the Medical Industry: A Friend of Time

The biggest difference between medical technology and industries such as consumer electronics, energy, and automotive lies in:

Stable Growth: The aging of the global population and the increasing burden of chronic diseases make healthcare demand inherently rigid. Even with economic cycle fluctuations and policy changes, the demand for medical devices and consumables remains relatively stable.

Long innovation cycle: It often takes more than a decade to translate basic research into clinical applications, and companies must possess "patient capital."

High Regulatory Barriers: The strict approval of medical devices forms a high barrier to entry in the industry.

This means that medical technology is a "race against time":No immediate explosion in sight, but long-term growth is bound to materialize.。

The transformation of Philips and GE is precisely because the capital market hopes that the medical business can be better valued as an "independent entity" rather than being overshadowed by the group's cyclical businesses.

3. Reference Significance for Chinese Enterprises

In China, many large groups are also entering the healthcare sector:

Home Appliance Enterprises:Midea, Haier, and others enter the fields of medical imaging and smart healthcare;

IT/Telecommunications Enterprises:Huawei and Lenovo Both Enter AI Healthcare and Device Ecosystem via "Technology Empowerment + Investment" Approach;

Traditional Manufacturing and Materials Enterprises: Some enter the high-end consumables, implants, etc.

These layouts often rely on the group's R&D, supply chain, and channel capabilities, which are very similar to the early paths of Siemens, GE, and Philips.

But from the experience of the global top three giants, there are a few points worth considering for the future:

1. Can the medical business rely on the parent group in the long term?

In the early stages, the group's capital and R&D system are indeed necessary. However, as the business grows, healthcare may "weigh down" the group's capital operations due to different valuation logic.

2. Does Independence Unlock More Value?

Just like GE HealthCare gained recognition from the capital market after becoming independent, in the future, if China's medical business reachesA certain scale, spinning off might achieve a higher valuation and strategic space.

3. The Importance of Patience and Strategic Vision

The medical business is hard to achieve "quick success," requiring more than a decade of investment and market cultivation. The ability to endure a long return cycle is key to determining whether a Chinese conglomerate can succeed in the healthcare sector.

4. Future Trends and Possible Patterns

Global: The competitive landscape of the three giants will become clearer. If Siemens Healthineers becomes independent, the future of the global medical technology field will see a tripartite stand-off among GPS., each finding different differentiated niche advantages.

China:

In the next decade, a group of "new medical technology giants" may emerge, starting from large industrial/home appliance/IT groups, but eventually becoming independent through spin-offs and entering the capital market.

Policies are also promoting "specialized, refined, novel" and locally produced medical device innovations. Under this trend, the independence and specialization of medical services are worth planning ahead.

The history of the medical technology industry tells us:Industry nurtures healthcare, capital drives independence。

Philips' proactive focus, GE's passive split, and Siemens' hesitation and balancing all indicateThe medical business is a "slow but steady" asset.

For Chinese conglomerates that are accelerating their expansion in the healthcare sector,What matters is not only the entry at this moment, but also whether it possesses patient capital and a forward-looking strategy, becoming "a friend of time."Seize the Opportunity for Independence in Future Industrial Transformation.

Recent Articles

The Era of Chinese-Made Medical Devices Has Arrived!

New Health Insurance Policy! Could It Become the "Second Ticket" for Innovative Medical Devices?

Global Medical Device Watch

▌Capital Radar|Money Flow

Overseas Financing Events| Financing Events in China Overseas Acquisition Cases| M&A Cases in China

Foreign Enterprise IPO | Chinese Companies' IPOForeign Enterprise Earnings Reports | Earnings Reports of Domestic Companies

Exhibition Preview/Review/Roundup

Si Yu Annual Event Review:The First Global Ophthalmology Conference | The First Global Orthopedics Conference | First Global Cardiovascular Conference| The First Global Medical Aesthetics Technology Conference |The 2nd Global Medical Technology Conference|The 3rd Global Surgical Robotics Conference