Why Every Surgical Robotics Company Is Fighting for Second Place Behind Intuitive

CMR Surgical

Surgical Robot Developer

Medtronic

Medical Device Manufacturer

Johnson & Johnson

Medical Device R&D and Manufacturer

Intuitive

Surgical Robot Developer

At the same time, let's add up all the systems from other companies; the total number of robots installed by all manufacturers is approximately 600.

So, our starting point in 2026 will be 11,600 surgical robots —IntuitiveWith 11,000 of them, accounting for 95% of the beautiful market share.

If we look at the number of surgeries completed to date, Intuitive Surgical will account for 99%. In terms of revenue — it will be 98%, and the profit is almost 100%. (Believe me, many companies suffer from heavy losses.)

Therefore, as the baseline;IntuitiveThe starting point is very strong. For now, we'll use a smaller figure, 95% of the installed base. We'll temporarily use this as the benchmark for market leadership.

Now, we need to examine what it mathematically means for a single company to capture more than 50% of the market share in a fantasy world.

Let's calculate.

In this fantasy scenario,IntuitiveSuddenly decided to stop selling any robots, with the installed base remaining at 11,000 units.

Moreover, all competitors have ceased operations... Only one other company remains in the surgical robot market, capturing 100% of the sales and achieving a total of 11,001 robotic systems installed, thereby becoming the "leader." All of this occurred within a span of five years.

Let's run this strange scenario:

AssumptionXThe company's starting base is the sale of 200 systems globally by the end of 2025. Then, XThe company needs to sell 10,801 brand-new systems within 5 years to reach the magical number of 11,001 units.

This means 2,160 systems per year, or a mere 41.5 systems per week — including holidays — every week for five years starting from January 1, 2026. Or broken down further, six robots per day. Every single day, without interruption, not one less.

I know it seems a bit "strange" for me to do this—but I keep receiving emails saying that Company X or Company Y will soon surpass.Intuitive. We all need to face reality.

Reality One:The annual production capacity of most companies ranges from 200 to 500 systems, which is five times smaller than the actual demand. If not within a few weeks, they will have backlogged orders within a few months.

Reality Two:This assumes that six systems are purchased globally every day. There will never be a day when hospitals don’t buy robots – never again. It’s insane.

Reality Three:In order to sell/deliver/implement and train each team – this means that for the next five years, six teams will need to work every day without interruption.

Can you see how absurd it is to think about the problem this way?

The reality is, ifIntuitiveIf they actually win 90% of the global bids/deals, they will add 1,000 robots to that target every year. Therefore, within 5 years, Company X will actually need to sell 16,001 systems to become the "market share leader."

This simple mathematical calculation shows that,IntuitiveIt is impossible to be pulled down from the top position—so please—all those who say emerging companies will defeat them… this is just a fantasy. Stop it. Stop torturing yourself by setting such lofty and unrealistic expectations.

So, what about using annual installation volume as an indicator?

Look, it doesn't work to measure by absolute installation volume — or absolute historical surgical completion volume. I mean, no one has a time machine to go back 25 years.

On the contrary, the focus should be on future business. In 2026 – you can start calculating the number of potential deals that could be closed and see how many deals the da Vinci system wins compared to its competitors (using the beginning of that year as the baseline). Historical installations are not counted.

Now, it's getting more interesting... but...

Let's assume Intuitive Surgical will sell 1,000 systems in 2026.

So far, the highest annual sales figure I've seen from any competitor is... well, it was from my previous time at...CMR SurgicalThe team sold more than 60 systems in a year. By the way, this is an impressive achievement.

So, this is 60 out of 1,000, or 6% of the installed base. It's still far from reaching 50%...

So, let's run this calculation for our super competitor, Company X.

To become the first, they need to achieve a sales volume of 1001 by 2026. Let's run this scenario.

1001 systems in 12 months = 83.5 systems per month

Or 19.25 systems per week

Or 2.75 systems per day.

Even if this number seems crazy — Intuitive Surgical is ready to do it and will achieve it by 2026. So, for a company that is large enough, with sufficient production capacity, enough training capability, and so on, it is absolutely possible.

But we must look at the gap from today. Assume that Company X (the best ever) has an operational rate of 100 systems per year by the end of 2025. On December 31, their operational rate is 1.9 systems per week — and this would need to increase tenfold within 24 hours to reach 19.25 systems per week. This is impossible — even for the largest and best company on Earth. Sorry, but that’s just the reality.

But if they double – reaching 200 systems per year – that’s now 16.6% – not bad.

Okay——now we're getting to the point!!!

I have been predicting for several years,IntuitiveThe next competitor will capture approximately 15% of the market share for new annual installations.

Let me clarify, this is not 15% of the global installed base (including historical installations). We need a better metric. For me, a better metric is "What percentage of new robots did Company X sell?"

If we use this metric - then I predict that the best companies can reach a level of selling 200 systems per year within 5 years. Moving from less than 100 to 200 sets implies a lot of things. But it is feasible and possible.

They still have to in the context ofIntuitive, and win 200 victories in the competition against all other competitors (bids and tenders). Not easy. But not impossible.

Hospitals (in some regions) must be willing and need to purchase more than 1,200 new systems that year. These are new installations, and if other companies also win some — then we might see about 1,500 new systems annually — Company X needs to secure 200 of these.

Is this reasonable? Is it worth it?

Okay, I need to do some other calculations here and take you on a "Is it worth it?" financial journey.

It's complicated, because it all depends on what "worth" means to your company. If you are an independent surgical robotics company that only relies on your own sales, then you need to look at the independent financial situation.

Independent Sales:

If we do this — we need to look at, say, $1 million (the price you might win if you're lucky enough to compete with Xi).

Then, just the capital expenditure — 200 x $100 million = $200 million in upfront revenue.

Adding approximately $2,800 per surgery (250 surgeries annually) = $700,000 per system each year.

200 systems (annual) = Additional $140 million

Adding service revenue of approximately USD 20 million (accounting for 10% of capital revenue)

That year, it might equal $360 million in revenue — not bad.

So, if I am the second-ranked independent robotics company — facing $360 million in revenue, with a 60% gross margin = $216 million in profit — that is not a small amount of income.

This assumes all capital equipment is sold as upfront cash sales. If part of the $200 million in capital is leased, paid over 7 years, and you're carrying a significant amount of costs on the books, then things look a little less certain.

But after more than 7 years, it’s generally a good deal. (You have surgical fee income every year!)

But...My small survey shows that Medtronic and Johnson & Johnson rank second and third, respectively. That's a different situation.

Sales Related to Business Defense:

As I've mentioned countless times — as laparoscopic and open surgeries shift toward robotic surgery, large surgical companies stand to lose the most. They lose access devices like trocars, staplers, and energy devices. These are high-margin and critical areas.

(Other companies will also lose imaging equipment, etc.) But these two giants are at the greatest risk.

Therefore, for every robot that can "defend a customer," its value is not just the value of the robot itself, but the value of that customer's business.

If that robot can even convert one customer... its value is even greater.

A single customer could represent millions of dollars in potential sales to defend or win. So, for a strategic corporation, each robot there is more valuable than it is for an independent robotics company.

When you look at it in this context, the situation starts to become very, very different.

Yes —— the company gains value from the robots —— but any company that defends or wins up to 200 major customers annually!! This is significant!!

Let’s assume the average value of a major customer is $4 million. If 200 customers are won, the added value would be $800 million.

Adding the $360 million from robotic sales, we're talking about a financial area worth billions of dollars within five years.

I want to emphasize that a 15%-20% market share of new installations is not equivalent to the market share of the installed base in many aspects. It is actually more valuable.

Look again — 200 units per year for five years equals 1,000 systems (after five years) out of over 16,000 total installed systems.

Accounting for an absolute 6% of the market share. This sounds terrible... but it’s not.

When I say the second and third competitors are far behind, I'm not exaggerating. You have to look at it from its own financial perspective.

Johnson & Johnson and Medtronic – if one of them achieves 15%-20% of the annual installations... it will add billions of dollars in value each year. And defend their crucial surgical product portfolios – so we must "view the second place within the specific context."

I hope this clarifies,IntuitiveStill number one by far — and leading by a wide margin. However, for any second or third place players, capturing their share of new installations is crucial to their own success — even ifIntuitiveIrrelevant.

What do I think of these results?

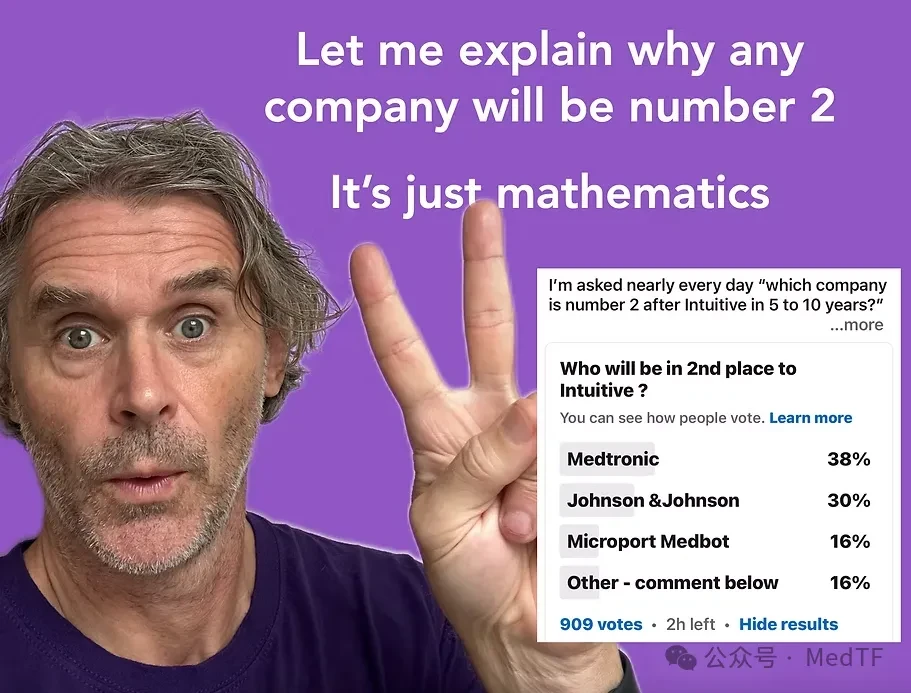

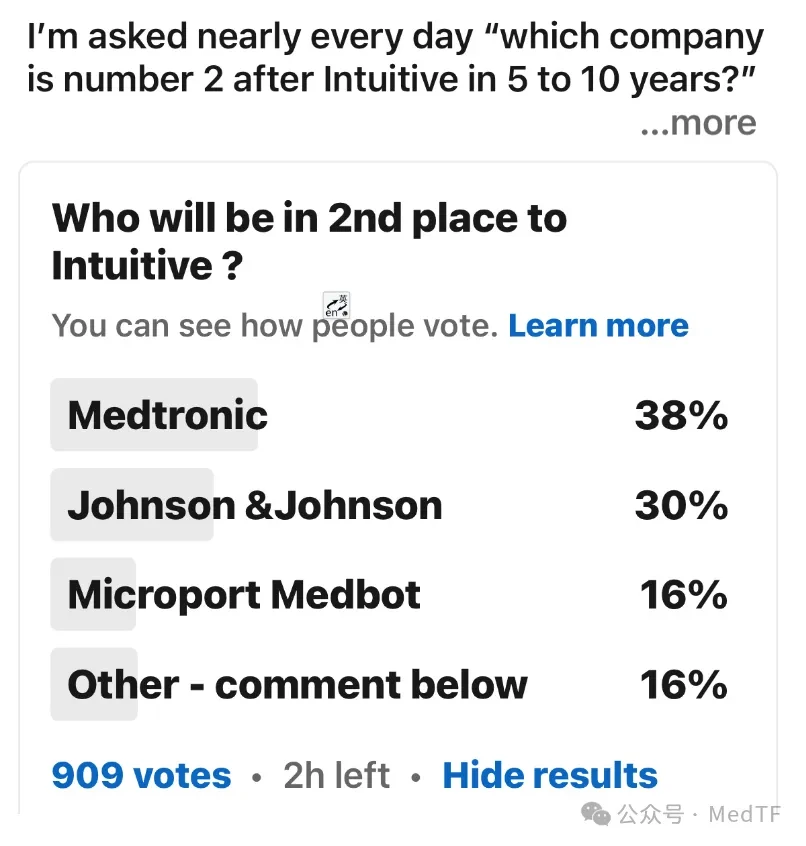

Which companies will becomeIntuitiveThe Second Place Afterwards

Don't take these surveys too seriously, but they indicate the zeitgeist of the market. Now, if I look at this list...

Second Place: Medtronic

Third Place: Johnson & Johnson

4th Place: Minimally Invasive

Other Participants:CMR Surgical, SS Innovationsi。

In my opinion, these three followers are large companies, which may be accurate. This is because I feel that "robots" alone do not have enough scale and influence to win. If a company uses distributors globally— with the changes in pricing and financing dynamics, it will eventually encounter difficulties in profit margins.

But this also involves the infrastructure costs of 360°, while large companies have open offices, operating finance departments, sufficient human resources teams, and so on. All these leveraged costs will determine success or failure. It’s not just about the robot itself. Building robotic infrastructure is expensive.

Therefore, on this basis, Medtronic is a giant company that can occupy a leading position. And they actually already have a robot on the market. Keep in mind, we're talking about 5 to 10 years in this discussion. Johnson & Johnson doesn't have Ottava available yet, so the third place is "if they get approval."

Their goal is to submit an application to the FDA in the first quarter of 2026 — then it will take at least 9 months to get approval. That will be 2027 — and only in the United States.

(But I suspect they are advancing the CE and Japan PMDA certifications in parallel.)

Nevertheless, nothing is certain until the approval is obtained. But the clock for securing second place is ticking every day.

But assuming approval is granted — by 2027 — they would become the second competitor. They have more than six years to catch up with Medtronic. This is no easy feat. So, can they miraculously surpass Medtronic within five years from now? I have my doubts. Therefore, third place feels about right.

Minimally invasive ranks fourth. With a solid foundation in China, and having personally seen their company — yes, they will continue to exist and are very likely to become a competitor after the top two or three.

For others... If any of them (CMR Surgical,SS Innovationsi) Being acquired by a large company - well, yes, they might also become competitors. But that important clock is ticking. The market space is being filled, and people are getting used to the existing systems. If the large companies want to enter, they need to act now.

So I think these results are credible - and I think if Medtronic can reach an annual installation volume of 200 sets... it will becomeIntuitiveA strong second place is definitely achievable.

As mentioned, for Johnson & Johnson and Medtronic, you can't look at their robots in isolation — you have to consider the bigger picture of their overall surgical product portfolios.

So, is this list credible in my opinion? ——"Yes"

Does this mean 49% of the market share? — "No"

Does this mean reaching an operational rate of 200 installations per year within 5 years? — "Yes," there is absolutely no reason why not.

Do I think small companies may be acquired and disrupt this landscape? — "Yes"