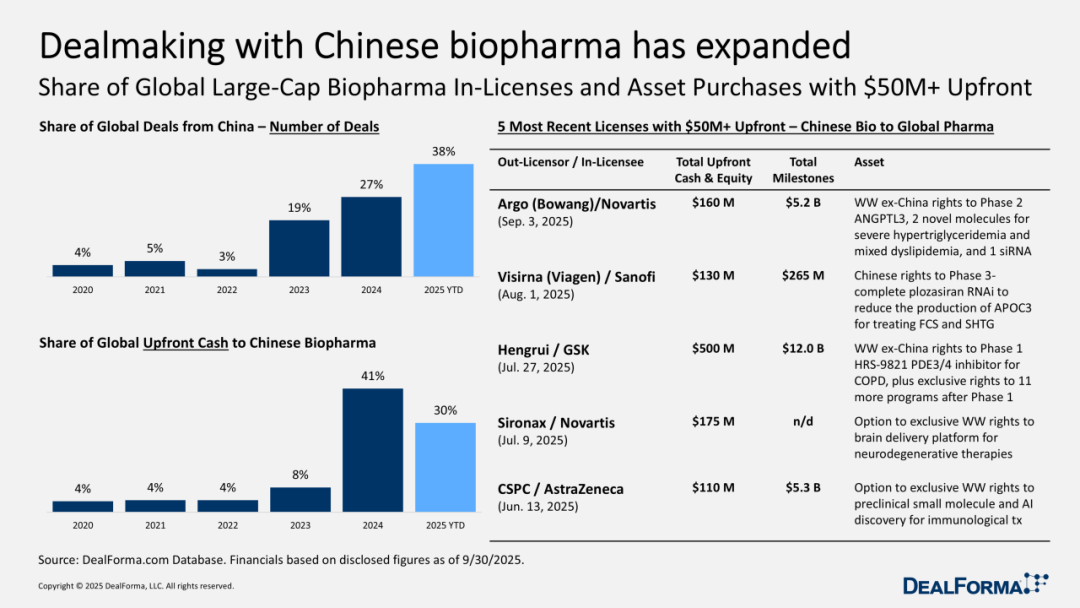

China's Innovative Drug BD Transactions Account for 38% of Global Total

Sanofi

Pharmaceutical Manufacturer

GSK

Pharmaceutical R&D Manufacturer

AstraZeneca

Pharmaceutical Technology Research and Development Provider

In the third quarter, the U.S. biotech industry saw a slight rebound along a series of key indicators: over the past six months, the Nasdaq Biotechnology Index (XBI) steadily increased, finally breaking through the 100 USD mark at the end of last month; The Federal Reserve announced a 25 basis point interest rate cut, andThe decline in borrowing costs is expected to inject momentum into the biotech industry in the coming months.

Amidst the joy, the U.S. market is also questioning: Is this a long-awaited sign of recovery, or another"Fake Move"?

InIn the view of Chris Dokomajilar, founder and CEO of DealForma,Signs in the third quarter give biotech companies reason to believe that the worst may be over.——

Based on the trend in the third quarter, pharmaceutical M&A and licensing deals are highly likely to continue growing this year; in the primary market, investors have started seeking returns from biotech companies in the late clinical stage, driving...The significant increase in the total amount of C-round and D-round financing also helped venture capital recover after a sluggish second quarter.

Based onDealForma’s 2025 Q3 Global Healthcare and Life Sciences Review: Endpoints News observed signs of recovery from three aspects—M&A, licensing deals, IPOs, and the primary market—particularly for drug developers holding late-stage clinical "potential winners."

Notably, China's innovative drugsThe continuous rise in BD transactions, along with the growing popularity of Hong Kong IPOs compared to Nasdaq, has also drawn significant attention, leading foreign media to conclude that "the global biotech landscape is shifting."

Endpoints News pointed out that the biopharmaceutical industry actually crossed a critical turning point in 2023: China leaped from being a "minor player" in the deal-making circle to becoming a pivotal "major player." In 2024, China further solidified this position; by 2025, China's status as a "key player" was essentially confirmed — a development that left many American biotech companies astonished.

Dokomajilar pointed out,China-related transactions have accounted for38%,Take it to the next level.The proportion of the down payment, although from last year's41% dropped to 30%,But still an impressive volume.

Novartis, Sanofi,GSK, AstraZeneca — these European pharmaceutical giants — have readily paid over 100 million USD in upfront payments and potentially billions of dollars in milestone payments amid the increasingly tense geopolitical atmosphere between China and the US. For AstraZeneca, this is the culmination of years of deep investment and strategic layout in China.

Endpoints News analyzed that, initially, multinational pharmaceutical companies in China were merely "curiosity-driven" bargain hunters. However, now, China has become the "first stop" for these pharmaceutical companies seeking shortcuts in drug development. With a solid scientific foundation and less regulatory intervention, Chinese biotech companies can initiate trials and obtain human data more quickly, far surpassing their counterparts in the US and Europe.

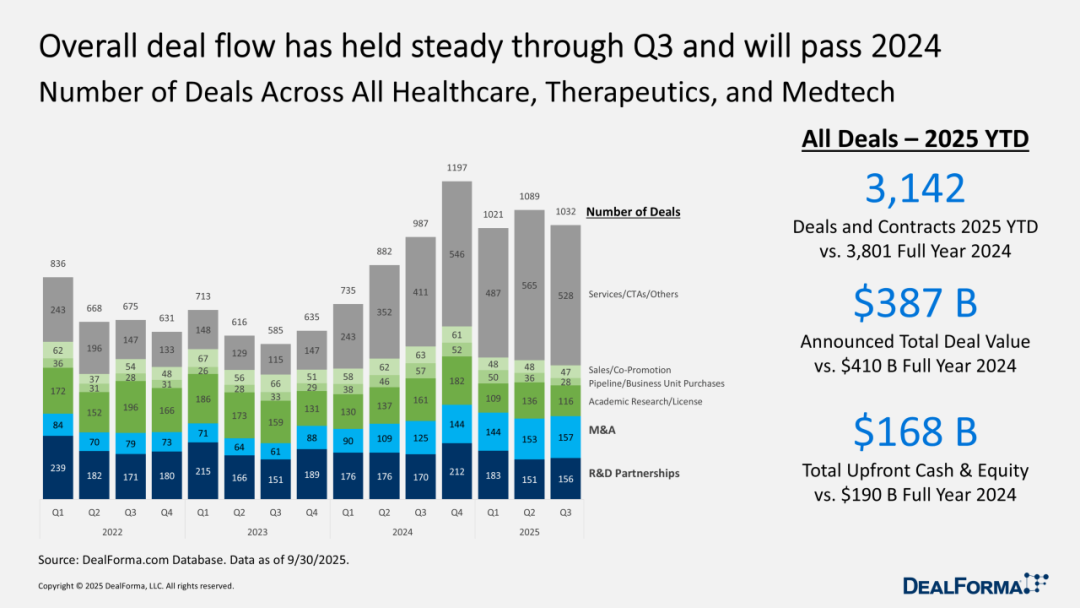

Overall, the global healthcare industry's licensing transactions are stable and improving:

The total volume of authorized transactions in healthcare, pharmaceuticals, and medical devices has grown steadily, although the pace slowed at the end of the third quarter; the total annual transactions are still expected to reach a new high.Record of 2024.

In terms of transaction value, the total value of all authorized transactions in the first nine months of this year has risen to$387 billion last year, with a total of $410 billion for the whole year. There is no doubt that annual growth will be achieved in 2025. Among this, upfront cash and equity have reached $168 billion, approaching last year's total of $190 billion.

Endpoints News believes that the increase in licensing deals this year mainly revolves around new service agreements — the biotech industry is continuously ramping up its investment in AI. Executives are leveraging various collaboration deals to help companies navigate through the downturn in the biotech sector.

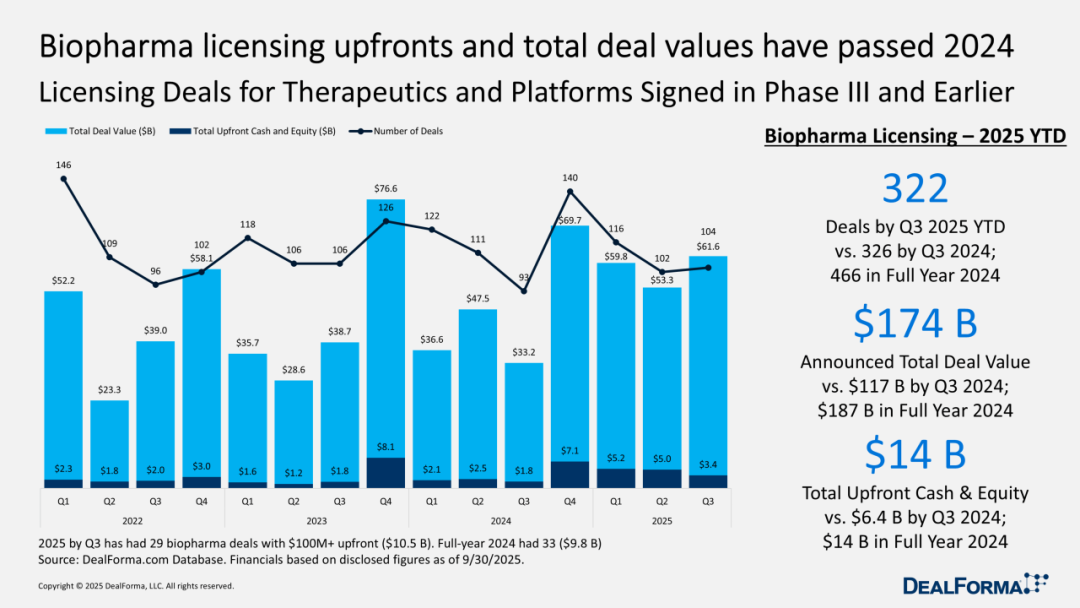

Focusing on the biopharmaceutical sector, the number of deals in the first nine months of this year has already matched the total for last year, while the total value of transactions has surged significantly.——By the third quarter of this year, it had reached US$174 billion, far higher than last year's US$117 billion.

From"Gold Content" in Upfront Payments: In the first nine months of this year, the total upfront payments in biopharmaceutical licensing deals have already matched the entire 2024 figure; the total for individual deals exceeding $100 million has even surpassed the whole of last year. Given that figures in the fourth quarter over the past few years have often far exceeded those of other quarters, the market generally expects 2025 to outperform the previous three years with ease.

However, for those biotech companies that are focusing on raising cashFor CEOs, licensing deals may have become slightly more challenging in the third quarter: although the total value of licensing deals increased, upfront payments were lower compared to previous quarters.

Overall, the fundamental logic of biotech company licensing deals remains solid: giants need biotech companies to provide innovative pipelines, especially after some companies divest their consumer businesses; biotech companies, on the other hand, rely on funding and endorsement from pharmaceutical giants to stay in the game. This relationship is often tense, but in this industry, demand always outweighs preference.

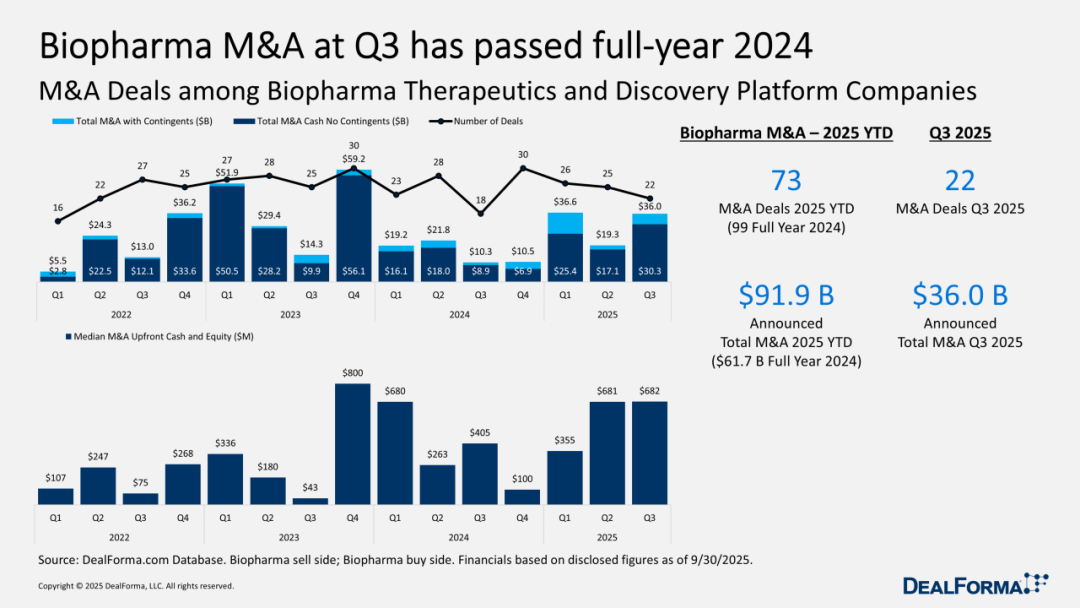

In order to prove to analysts itsAfter the expiration of Keytruda's patent in 2028 and the loss of most of its revenue, Merck still managed to stand firm by firing the "first shot" of the third-quarter M&A boom with a $10 billion acquisition of Verona. Following this, Pfizer also acquired Metsera for nearly $5 billion upfront, aiming to launch a competing obesity drug and enter this super market.

During this period, the industry also witnessed a series of smaller-scale mergers and acquisitions.——Dokomajilar Statistics Show 22 Cases in the Past Three Months——Biotech CEOs Who Predicted a Surge in Big Pharma M&A Driven by the 'Patent Cliff of Blockbuster Drugs' Are Feeling Triumphant.

According toAccording to DealForma statistics, the total M&A amount in just the third quarter is sufficient to allow 2025 to surpass the sluggish figures of 2024.If the fourth quarter can掀起一波高潮 like in previous years, the full-year data will be相当亮眼.

Not long ago,TCG Crossover Announces Successful Close of TCGX Fund III with $1.3 Billion in Commitments. In a public interview, TCGX founder Chen Yu attributed this achievement to the consecutive acquisitions of a group of late-stage biotech companies they selected, realizing their value.

It can be said that,For anyone who wants to achieve results within a relatively short period of timeFor LPs seeking to generate returns, market realities have made mergers and acquisitions a core strategy.IfWith the IPO channel blocked and the path to Nasdaq cut off, there are few places left to explore value at a discount.

This might beThe best window for pharmaceutical giants to "strike real gold" through mergers and acquisitions in the past 15 years. If the biotech industry enters an upcycle next year, waiting will only come at a higher cost, and the demand for mergers and acquisitions has never faded.

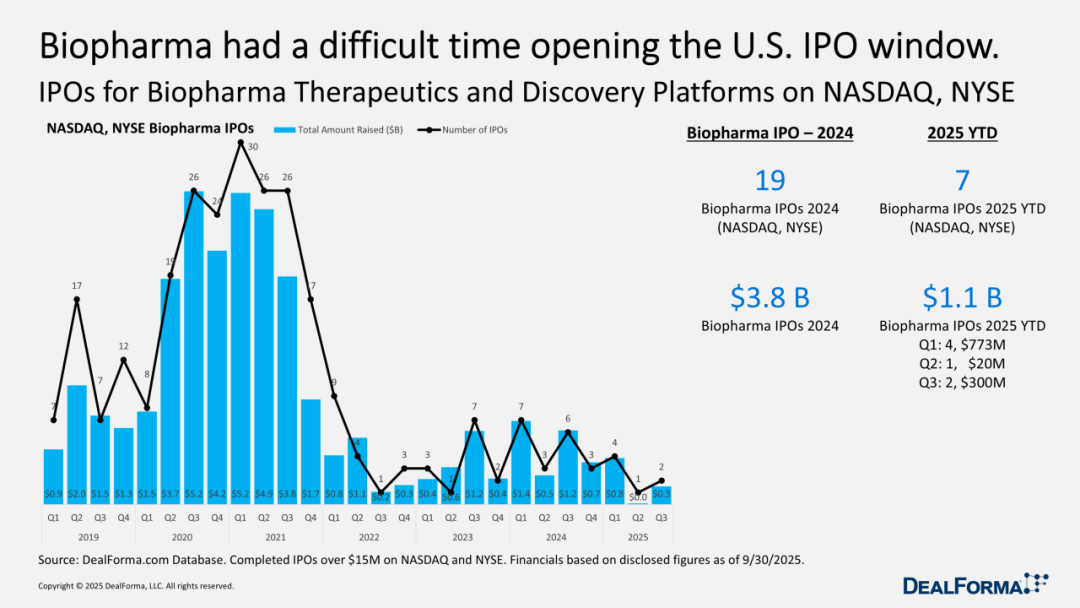

This Year's U.S. BiotechnologyIPO Data Shows Little Bright Spots. However, after a "zero IPO" second quarter, there was a glimmer of hope in the third quarter — a star company successfully landed on NASDAQ.

Industry experience is: best in"Money is no object" when financing. If a company with weak cash reserves forces its way to NASDAQ, it will often be overwhelmed by market skepticism. However, this "ideal state" is obviously not applicable when the IPO window is closed.

LB Pharmaceuticals Successfully Avoids Pitfalls: By Entrusting Pricing Power to the Market, It Raises $285 Million at the Median Price of $15 Per Share, Drawing Widespread Attention.

At present, a large number of applications for listingThe S-1 filing is still gathering dust in the corner. One exception is not enough to trigger an IPO boom, but if a few more break the ice, the trend may get underway.CurrentlyThe IPO market has only upward potential.If interest rates continue to fall, this potential turning point is worth close attention.

It should be noted that,When NasdaqIPOs Fall Into a Deep Freeze, but the Hong Kong Stock Market is Warm and Welcoming, Recently Continuously Welcoming New Listings. Endpoints News Believes That Behind This is the Overall Continued Favor of Large Pharmaceutical Companies Towards China's Biotech Firms, Which Have Established a Reputation for "Fast Clinical Progress and Quick Successful Returns."

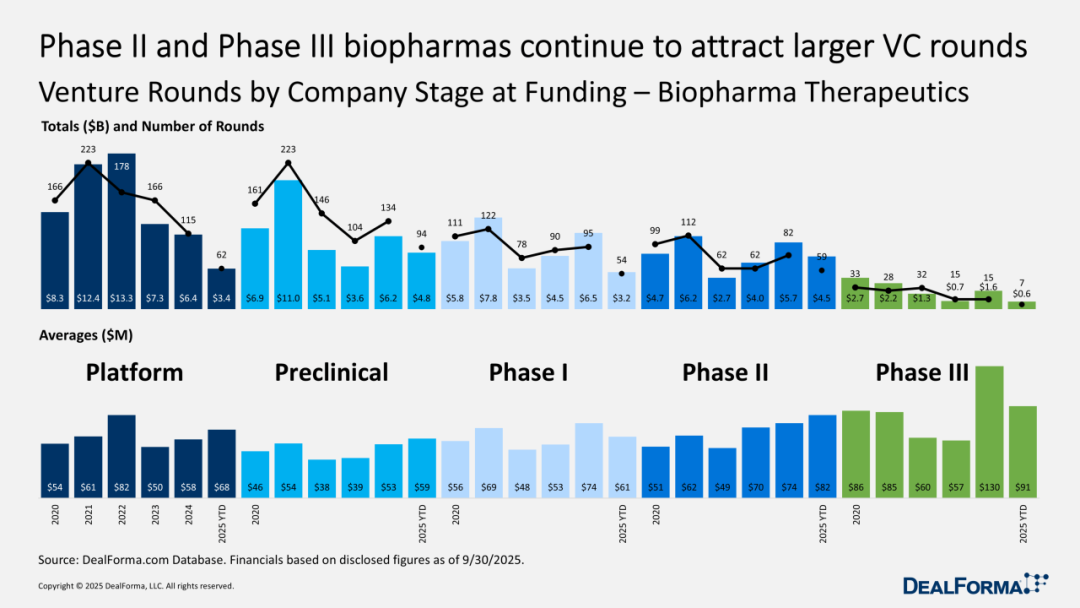

For US biopharmaceutical venture capital,The freeze of IPOs implies a "crisis of confidence." With no exit options available, the flow of capital has also shifted significantly: moving from an emphasis on startups at their peak a few years ago to betting on solid clinical data.

DealForma noted that venture capital is flowing into Phase II and Phase III clinical projects.The preclinical stage financing is particularly challenging. If a company needs to go through a long journey before entering human trials, investors become even more conservative.

And as the pendulum of the industry cycle swings from the early stageAs Series A shifts to later stages, biotech companies are chasing the "make-or-break" human data—data that either brings substantial returns or sends projects straight to the "failure graveyard." In an environment lacking comprehensive fund support for IPOs, VCs can only continue to double down on their most promising projects, pushing them all the way into later funding rounds.

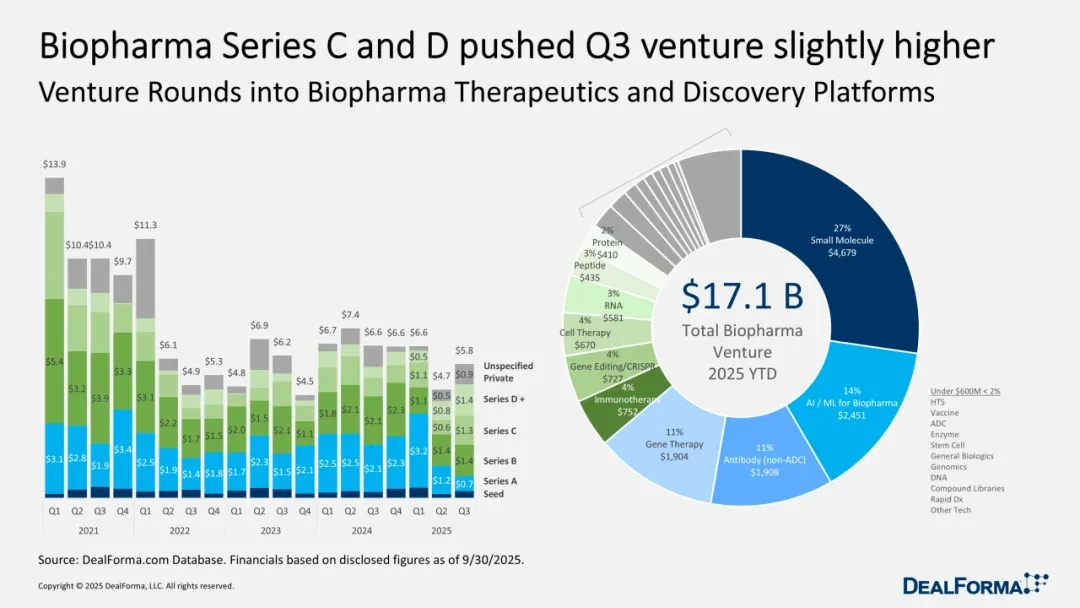

Therefore, it can be seen that,Series A financing has now fallen to a multi-year low; although the overall financing amount has slightly recovered from the bottom of the second quarter, it is mainly driven by significant growth in later-stage Series C and D rounds. Compared with the prosperous period of smooth exit channels in previous years, the current figures pale in comparison.

With a few exceptions, whenWhen the IPO door has basically closed, mainstream biotech investors rarely pay for “breakthrough science” and its distant returns. Their goal is to find drug candidates that can generate eye-catching profits and thereby attract big pharmaceutical companies. As a result, biotech CEOs have to make tough choices: concentrate resources and hold on tightly to the most promising products in the pipeline. Consequently, the wave of layoffs continues, and may even occur in the most unexpected companies.

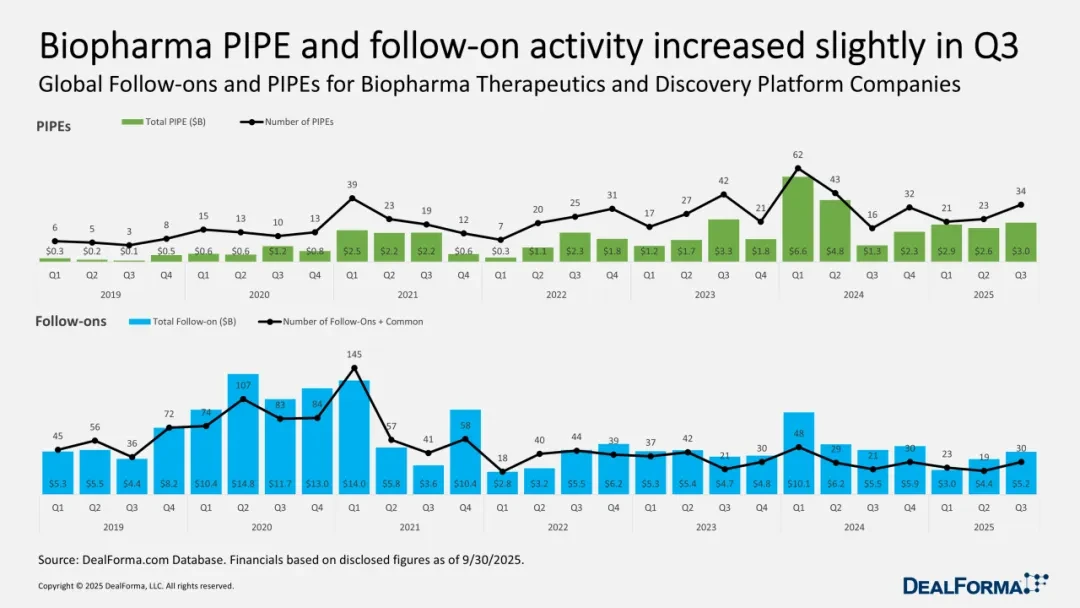

Two sides of the same coin,PIPE and refinancing have improved slightly. The pandemic has left a large number of listed biotech companies struggling in a market where high-risk stocks face difficulties in financing. For investors betting on positive human data readouts, this has instead become an attractive hunting ground.

According toAccording to DealForma statistics, PIPE investments have stabilized so far this year, with the number and value of deals in the third quarter rising significantly compared to the previous quarter. Refinancing has also started to climb after bottoming out in the first quarter.: The third quarter has a total of30 Follow-on Financings Bring $5.2 Billion to Innovative Drug Developers and Platform Companies.

Recommended Reading