Follow the official account and reply"Abstract"

Claim Now: Nearly 400 Abstracts from the 2025 European Congress of Interventional Cardiology + 2025 ESC Abstracts Excel

Note: This article has a total of 14,873 words and an estimated reading time of 38 minutes.In December 2025, China's intravascular imaging track witnessed intensive developments.On December 3, Acoustic Life Science Co., Ltd., a subsidiary of SonoScape, received NMPA approval for the official market release of its self-developed 60MHz high-frequency intravascular ultrasound (IVUS) catheter.[1]This is another 60MHz high imaging frequency IVUS approved for production in China after Acoustic Life Science Co., Ltd. Just a week later—on December 8, Horimed Technology Co., Ltd. announced the completion of nearly 100 million yuan in financing, bringing in investors such as Guanghua Open Source, Zhongtian Weiyi, and Chengdu Science and Technology Investment (MedDRA InvestGO).®Database). Within a short week, from nearly 100 million yuan of capital injection to another breakthrough in domestically produced 60MHz high-end consumables, industry benefits have been coming one after another. This is not just the accumulation of numbers and certificates, but more like a flare sent out to the entire industry: the competition in China's intravascular imaging market may have shifted from单纯的“国产替代”to “性能竞争”.Reviewing the industry development, since the first balloon angioplasty in 1977, coronary angiography (CAG) has long been the imaging standard for the diagnosis and treatment of coronary heart disease.[2]However, for complex situations such as left main lesions and chronic total occlusions, traditional angiography can only provide information on the lumen contour, without the ability to evaluate vascular wall structure, plaque characteristics, or stent apposition, making its limitations increasingly apparent.For this reason, intravascular ultrasound (IVUS) and optical coherence tomography (OCT) have gradually developed into important endovascular imaging tools, achieving a leap from "viewing the lumen" to "viewing the vessel wall." They complement angiography: angiography is responsible for vascular pathways and intraoperative navigation, while IVUS and OCT focus on cross-sectional imaging and quantitative assessment of the vessel wall, thereby optimizing percutaneous coronary intervention (PCI) strategies and improving patient outcomes. In recent years, hybrid imaging technologies that combine the penetration power of IVUS with the high resolution of OCT have also become a research hotspot, driving endovascular imaging towards a more three-dimensional and comprehensive direction.Against this backdrop, the successive approvals of high-performance products such as China-produced 60MHz high-frequency IVUS can be seen as a key strategic move by companies in the dimension of "performance competition." Then, in 2025, after the implementation of the centralized procurement policy, will the bidding and procurement data truly reflect the policy direction of "exchanging volume for price"? In the competition between the IVUS and OCT markets, which path will better break the long-term monopoly of imported products?This report is based onMedCube NextDevice®Medical Device DatabaseOfChina Marketed Device ModuleAndChina Device Bidding Module, starting from the technical principles and clinical evidence, combined with the latest market data, systematically review the development logic in the IVUS and OCT fields, and conduct an empirical discussion on the development logic and direction of China's intravascular imaging market.1. Sound Waves and Light Waves

![]()

![]()

Modern cardiovascular interventional diagnosis and treatment has broken through the single dependence on angiography, establishing a diversified evaluation system covering functional, histological, and morphological aspects. According to technical principles...Theory and Clinical PracticeDue to the different outputs, mainstream interventional diagnosis and treatment technologies can be divided into three major categories.Table 1-1: Mainstream Endovascular and Intracardiac Interventional Diagnostic and Treatment Technologies

Although the aforementioned technologies collectively constitute a variety of techniques in interventional diagnosis and treatment, FFR focuses on physiological indicators, NIRS emphasizes chemical analysis, and the application scenarios of ICE are mainly within cardiac structures (such as atrial fibrillation and valvular disease). In contrast, IVUS and OCT are high-precision morphological tools that focus on the interior of the vascular lumen.At the clinical application level, the clinical use of intravascular imaging technology mainly focuses on two core interventional fields: coronary and peripheral. In percutaneous coronary intervention (PCI), angiography and intravascular imaging complement each other to compensate for blind spots in angiography, such as those in the left main trunk and calcified lesions. In peripheral interventions (e.g., iliac vein compression and lower extremity arterial occlusion), intravascular imaging serves as a key decision-making tool for evaluating the true vascular diameter and stent apposition. However, due to the physical nature of IVUS and OCT, which are based on sound waves and light waves respectively, there are significant differences in imaging resolution, tissue penetration, and environmental requirements.

1.1 Intravascular Ultrasound (IVUS): Acoustic Deep Imaging

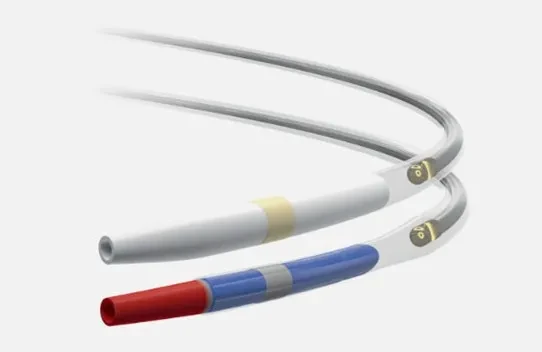

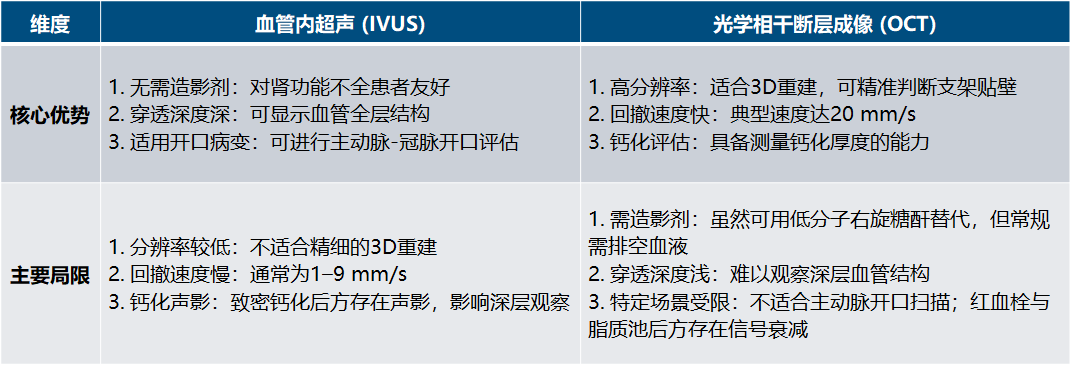

IVUS Technology is Rooted in the Principle of Ultrasound Echo. The system consists of a miniature ultrasound transducer at the catheter tip, a pullback device, and an imaging host. The transducer emits high-frequency ultrasound waves (20-60 MHz), which penetrate through blood into the vascular wall tissue, generating reflections at interfaces of different densities due to variations in acoustic impedance; receiving and processing the echo signals enables the reconstruction of grayscale cross-sectional images of the blood vessel.[3]。In terms of imaging mechanisms, IVUS is mainly divided into mechanical rotational and electronic phased-array types. The mechanical type achieves 360-degree scanning through the high-speed rotation of a single-crystal transducer, offering high resolution and uniform beam, but the rotating shaft may affect maneuverability and introduce image artifacts (e.g., non-uniform rotational distortion). The phased-array type uses an annular multi-element array for electronic scanning, without mechanical rotating parts, enhancing catheter flexibility, though earlier models were slightly inferior in resolution and dynamic range.The core advantage of IVUS lies in its excellent tissue penetration capability, routinely penetrating over 10 millimeters in depth. It not only clearly displays the intima but also penetrates thick plaques to accurately identify the external elastic membrane (EEM) of blood vessels. In coronary interventions, the EEM diameter is crucial for determining the true vessel size and guiding stent selection. Moreover, due to minimal attenuation of ultrasound in blood, IVUS imaging does not require the removal of blood from the lumen. This "contrast-agent-free" feature makes it a suitable choice for patients with renal insufficiency and demonstrates high safety in scenarios such as left main ostial lesions.Figure 1-1: Boston Scientific OptiCross HD IVUS Catheter

Source: Boston Scientific Official Website

1.2 Optical Coherence Tomography (OCT): High-resolution Optical Imaging

OCT Technology Based on Low-Coherence Interferometry Principle[5]。The most significant feature of OCT lies in its extremely high axial resolution, which can reach 10–20 μm, approximately 10 times that of IVUS (100–150 μm). This improvement provides it with excellent recognition of fine structures, enabling clear visualization of high-risk plaque characteristics such as thin fibrous caps (TCFA, as thin as 65 μm), precise evaluation of endothelial coverage over stent struts, and differentiation between red and white thrombus morphology. OCT is of significant diagnostic value in assessing stent malapposition, tissue prolapse, and minor edge dissections.However, the physical properties of light waves also determine the limitations of OCT. Near-infrared light scatters and attenuates strongly in red blood cells, requiring the rapid injection of contrast agents or Ringer's solution to temporarily evacuate blood during imaging. This not only increases procedural steps but also limits its application in patients with renal insufficiency. Additionally, the shallow penetration depth of light waves, only 1–2 mm, makes it difficult to penetrate large lipid cores or heavily calcified plaques, usually unable to clearly display the EEM. Therefore, there are certain evaluation limitations in assessing vascular positive remodeling and selecting large-sized stents.It is worth mentioning that another mature application scenario for OCT is ophthalmic OCT, and subsequent research reports will separately analyze the development and landscape of ophthalmic OCT.Figure 1-2: Abbott Dragonfly Opstar™ OCT Imaging Catheter

Source: Abbott Official Website[6]

1.3 IVUS+OCT Synchronous Imaging

With the increasing demand for precise diagnosis and treatment of complex coronary artery diseases, imaging technologies that integrate the deep penetration of IVUS and the high resolution of OCT have emerged. This integration, based on the intrinsic complementarity of their principles, achieves synergistic effects in clinical practice, particularly aiding in the thorough evaluation of complex lesions and the optimization of interventional strategies.[7]。The technical core lies in the synchronous acquisition of the overall vascular structure and fine features through a single pullback, thereby compensating for the limitations of single imaging. IVUS, with its strong penetrability, clearly displays the EEM contour, accurately evaluates vessel dimensions and plaque burden, providing critical reference for stent selection. OCT, with micrometer-level resolution, presents the intimal surface and shallow details, precisely identifying thin-cap fibroatheroma, microthrombi, and calcification subtypes. After stent implantation, OCT can assess stent apposition, dissection, and intimal coverage, enabling full visualization from microscopic pathology to interventional outcomes.[8]。In severe calcified lesions, fusion technology demonstrates synergistic value: OCT precisely evaluates calcification morphology, IVUS determines deep distribution, providing a basis for plaque modification and treatment strategies. In chronic total occlusion interventions, IVUS confirms the true lumen position, while OCT assesses plaque characteristics. The synchronized imaging catheter allows operators to avoid equipment changes, enhancing procedural efficiency and safety.[9]。In addition, the synchronous imaging probe enables dual-mode synchronous acquisition, shortening operation time, reducing the risk of instrument exchange, and decreasing contrast agent dosage. This is particularly significant for patients with renal insufficiency or hemodynamic instability, highlighting the clinical practical value of "one retraction, double observation."2. Development Trends in China's Intravascular Imaging Equipment Market

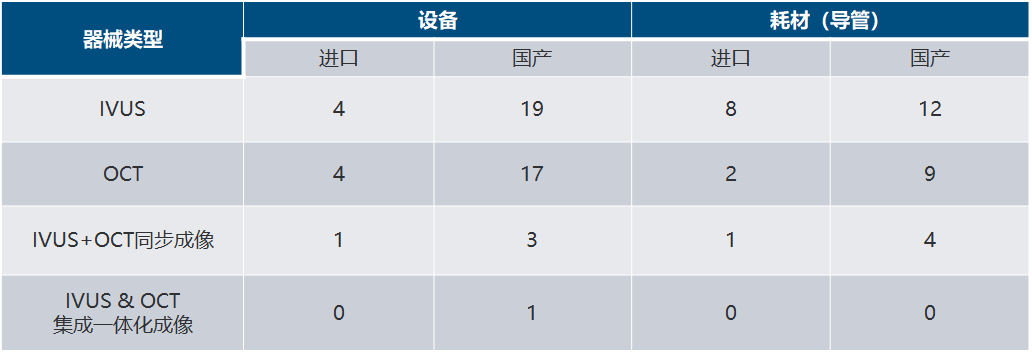

Chapter One: After elucidating the physical principles and application potential of intravascular imaging technology, it is necessary to further explore: What has been the process of introduction, digestion, and integration of these technologies in the Chinese market? What are the characteristics of the current market ecosystem? This chapter will analyze the overall development status of domestically marketed products, from the registration and approval process to the strategic layout of key enterprises, outlining the industrial transformation from import dominance to the rise of local companies, while analyzing the market logic and competitive landscape.Based on PharmaCube NextDevice®Screening Analysis of China's Marketed Device Module Data: By using the concept track "Intravascular Imaging Equipment" and classification tags such as "Ultrasonic Pulse Echo Imaging Equipment" or "Optical Coherence Tomography System (Non-Ophthalmic)," it is possible to comprehensively track the registration status of China's intravascular imaging equipment (IVUS and OCT) and catheter consumables. According to the query results, as of November 31, 2025, China currently has 85 registered certificates for "Intravascular Imaging Equipment." Among these, there are 49 device registration certificates and 36 consumable (catheter) registration certificates.Figure 2-1: NextDevice®Currently Listed and Approved Intravascular Imaging Devices (Equipment and Catheters) in China

2.1 Registration Quantity Trend: Transition from Import-Dominated to Growth in Localization

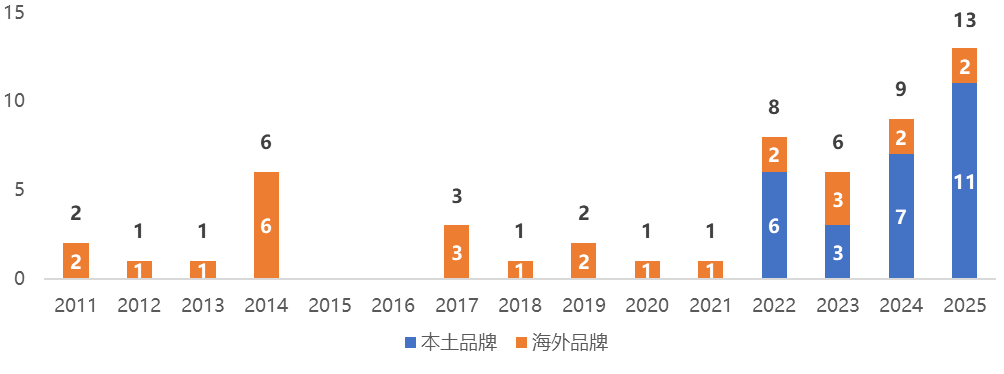

2.1.1 Approval Trends of IVUS SystemsIn the early stages of development, China's IVUS (intravascular ultrasound) market was long dominated by imported brands. From 2011 to 2019, imported IVUS devices were successively approved for marketing, while domestically produced devices were relatively scarce, resulting in a market landscape with clear dependence on imports.However, since 2022, domestically produced IVUS devices have gradually emerged, marking a significant improvement in local R&D and manufacturing capabilities. Looking ahead, this growth trend is expected to continue. By 2025, the cumulative number of approved domestically produced IVUS devices and consumables has reached 11, indicating that the localization process is accelerating.It should be noted that some overseas brands have products manufactured in factories established within China, which are approved in the form of a domestic medical device registration certificate. To more clearly distinguish the origin of these brands, this report uses "overseas brands" and "local brands" as classification criteria when analyzing approval statuses, in order to more accurately present the market competition landscape and development trends.Figure 2-1: NextDevice®First Approval Date of IVUS Devices and Consumables in the Database

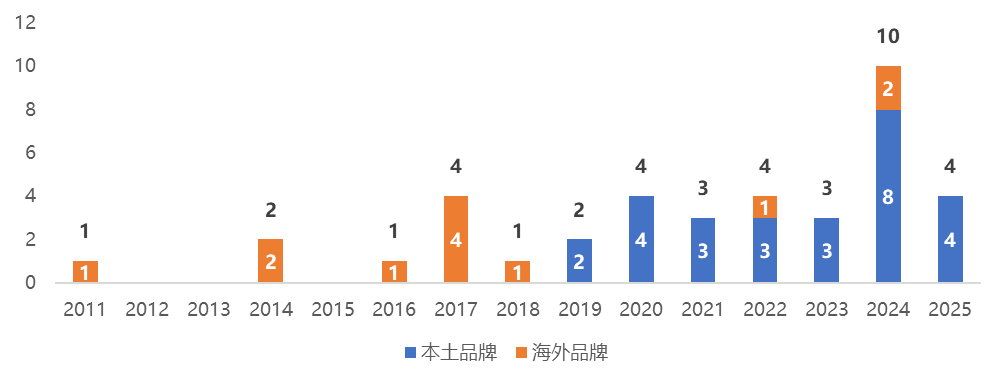

2.1.2 Approval Trends of OCT SystemsThe OCT field follows a similar trajectory. From 2014 to 2019, the market was characterized by the slow growth of imported products, but after 2020, the registration of domestically produced OCT devices/consumables increased rapidly, with six domestic devices approved in 2024 alone. This shift not only highlights breakthroughs by local enterprises in technology development but also signifies that China's intravascular imaging market has transitioned from sole reliance on imports to a diversified competitive landscape where domestic and imported products coexist, offering broader clinical options.Figure 2-2: NextDevice®First Approval Date of OCT Equipment in the Database

2.2 Analysis of Market Participant Landscape: Differentiated Competition Based on Technical Routes

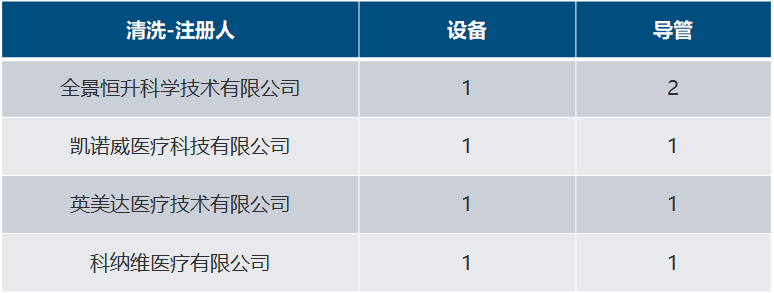

Although the number of registration certificates cannot be directly equated with market share or commercial competitiveness, it is an important indicator for measuring a company's R&D activity, product line diversity, and technical maturity. By comparing the registration status of different technical approaches horizontally, the competitive landscape of the current intravascular imaging market can be clearly depicted.2.2.1 IVUS Track: Intense Competition in a Crowded Market, Breakthrough of Domestic Production under Import DominanceIn the field of interventional therapy, IVUS has long been recognized as the gold standard for imaging, and market competition is becoming increasingly fierce. The current market reflects a situation where multiple companies are fiercely competing. Among imported brands, Volcano Corporation holds two device registration certificates and five catheter certificates thanks to its mature product portfolio. Boston Scientific, on the other hand, has demonstrated flexible localization strategies. Since 2022, its IVUS devices have been manufactured in local factories in China, with four domestically produced registration certificates approved as of November 31. However, the core consumable, the catheter, remains imported, with three registration certificates held. This combination of "locally produced equipment and imported consumables" reflects how multinational corporations are optimizing their cost structures through localized production to consolidate their market positions. Compared to imported registration certificates, domestically produced certificates offer significant policy and price advantages during the bidding process. They not only eliminate the cumbersome import justification procedures but also align with the domestic priority quota, while leveraging cost resilience to gain an advantage in centralized procurement bidding.At the same time, although domestic companies started relatively late, they have gradually broken through key technologies. Companies such as SonoScape, Acoustic Life Science Co., Ltd., and Horimed Technology Co., Ltd. have all achieved the supporting certification for equipment and consumables, continuously catching up in terms of the number of registration certificates. This marks that domestically produced IVUS products have reached the technical standards required for clinical applications, and the process of domestic substitution is advancing from the initial "availability" issue towards a deeper phase that focuses more on performance and optimization.Table 2-2: IVUS Market Participants in China

2.2.2 OCT Track: A Differentiated Battlefield Led by Chinese ProductionCompared to the fierce competition in the IVUS market, the OCT market presents a completely different competitive landscape: Chinese-produced products have gained an overwhelming advantage over imported brands in terms of the number of approved products, forming a new trend of "Chinese production taking the lead."Among imported products, Abbott stands out as the dominant player with four registered devices and two catheter certificates. Other imported brands, such as St. Jude Medical (which has been acquired by Abbott), are gradually fading from the market. This indicates that multinational giants have relatively concentrated investments in the OCT field, with fewer competitors.Chinese enterprises have experienced explosive growth. The data performance of Zhongke Micro-Light in the OCT field is particularly impressive, with 10 registered devices and 3 registered catheters. The richness of its product line far exceeds that of similar competitors, demonstrating its deep cultivation strategy in this niche market. In addition, Panorama Hengsheng, Micro-Light Medical, and Wofuman, among other Chinese enterprises, are also making their moves. This pattern indicates that compared to ultrasound technology, domestic companies in China have a faster R&D response speed in the optical coherence tomography (OCT) imaging field, with products receiving approval more frequently. OCT may become a key area where Chinese manufacturers can "overtake on a curve."It is worth mentioning that, through its subsidiaries Acoustic Life Science Co., Ltd. (IVUS) and Argus (OCT), MicroPort has achieved a dual-track approach, which allows it to cover a wider range of clinical indications and reduce the risks associated with a single technological pathway.Table 2-3: The Pattern of Participants in China's OCT Track

2.3 The Rise of Multimodal Imaging Systems

2.3.1 IVUS/OCT Synchronized ImagingWith the increasing demand for precision diagnosis and treatment in clinical practice, the limitations of single-modality imaging have given rise to a new direction of technological integration. Registration data shows that IVUS/OCT synchronous imaging devices, as an emerging category, began receiving regulatory approval starting from 2022. This trend stems from innovative attempts to combine the deep penetration advantage of IVUS with the high-resolution strength of OCT within a single console or even a single catheter, aiming to address the operational pain point of frequently switching catheters during traditional procedures. Currently, there are nine registered certificates for IVUS/OCT synchronous imaging devices in China, four for equipment and five for catheters. Nearly 80% of these registered certificates are for domestically produced products. In the future, intravascular imaging may evolve towards a more efficient and integrated synchronous imaging approach. Given the current market landscape, this is also one of the better breakthrough points for achieving domestic innovation.Table 2-4: Participants in China's IVUS/OCT Synchronized Imaging Sector

2.3.2 Horimed: IVUS & OCT Integrated Imaging DeviceHorimed recently launched the innovative intravascular imaging system HSD100 (China Medical Device Registration No. 20233061754). Unlike synchronous imaging, this system integrates IVUS and OCT physically at the hardware level, rather than through single-catheter synchronous imaging. It provides clinicians with an efficient "one-stop" intraluminal imaging solution, eliminating the hassle of switching hosts during procedures and reducing operation time. It also alleviates, to a certain extent, the spatial pressure caused by crowded equipment in catheterization labs.Figure 2-3: Horimed Intravascular Imaging System HSD100

Source: Horimed Official Website[10]

III. Clinical Evidence-Based Medicine: Building the Pyramid of Value

If the industrialization process of technology depicts its growth trajectory in the Chinese market, then a series of milestone clinical studies have laid the foundation for the clinical use of intravascular ultrasound (IVUS) and optical coherence tomography (OCT). Over the past decade, evidence-based medical data has accumulated from quantitative to qualitative changes, driving these two technologies to undergo a role transition: evolving from "optional aids" that improve angiographic outcomes to "decision cores" that directly enhance patient survival and quality of life.

3.1 From "Optimizing Operations" to "Improving Prognosis"

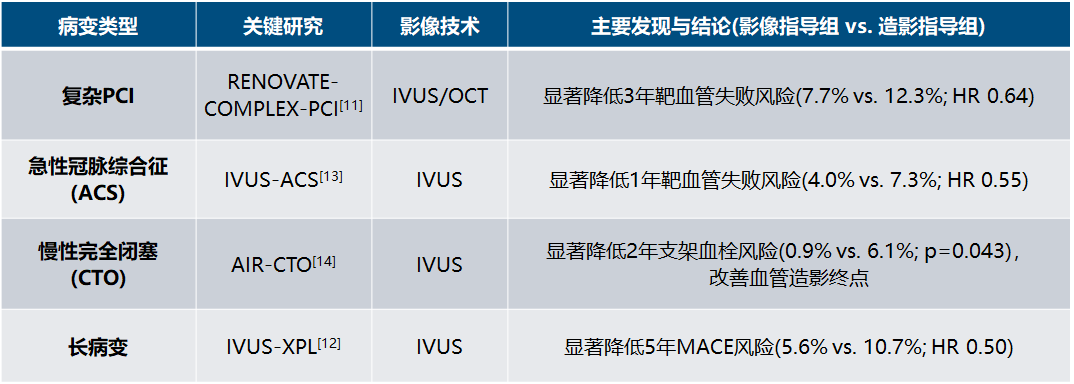

Early research primarily focused on the immediate radiological optimization of stent implantation. In recent years, several large-scale, rigorously designed randomized controlled trials (RCTs) have provided definitive evidence: compared to angiography alone, angiography combined with intravascular imaging guidance significantly reduces the risk of "hard endpoint" events (such as death, myocardial infarction, and repeat revascularization) in patients. For instance, the RENOVATE-COMPLEX-PCI trial demonstrated that in complex lesion interventions, IVUS or OCT guidance can relatively reduce the 3-year target vessel failure risk by 36%.[11]The five-year follow-up of the IVUS-XPL trial further demonstrated that the reduction in major adverse cardiovascular events (MACE) risk persists and the advantage expands.[12]. These studies collectively establish an indisputable conclusion: precision interventions based on imaging can translate into tangible improvements in patients' long-term outcomes.Table 3-1:Key Clinical Research Evidence of Intravascular Imaging in Specific High-Risk Lesions

3.2 Complementary Positioning of IVUS and OCT

IVUS and OCT, as the two major pathways of intravascular imaging, what are their respective positions, advantages, and disadvantages? The 2023 OCTIVUS trial provided a key answer: in improving 1-year clinical outcomes for patients, OCT guidance is non-inferior to IVUS guidance, establishing the equivalence of both in terms of clinical benefits.[15]However, "equivalent" does not mean "identical." Due to their distinct physical principles, the two have formed clear and complementary clinical roles. IVUS, with its powerful tissue penetration, is indispensable for evaluating the true size of blood vessels (especially the left main trunk) and determining guidewire positioning in chronic total occlusion lesions. On the other hand, OCT, with a resolution ten times higher than IVUS, is irreplaceable for precisely assessing calcification, meticulously analyzing stent implantation outcomes, and identifying the microstructure of vulnerable plaques.Table 3-2:Comparison of Core Technical Features and Advantage Scenarios Between IVUS and OCT[16]3.3 The Future: Synchronous Imaging Technology Moving from Clinical Evidence to Application

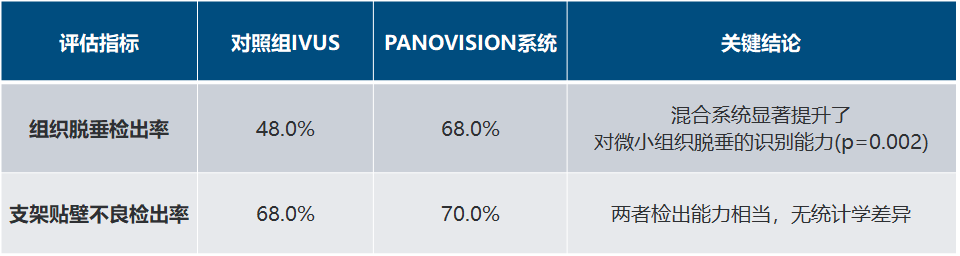

The clinical value of synchronized imaging technology has moved beyond the theoretical conception phase, gaining evidence-based support from rigorous clinical trials. The landmark PANOVISION trial, a large-scale, multi-center, first-in-human clinical study targeting a novel IVUS-OCT synchronized imaging system, has established a solid evidence foundation for the application of this technology.[17]。The research results confirmed that the IVUS and OCT modes of the integrated system demonstrated non-inferior performance compared to standalone control devices in core imaging quality metrics (clear stent capture rate), establishing its position as a reliable imaging tool. More significantly, the study revealed the synergistic value of the system: benefiting from the improved acoustic window due to contrast flushing, its IVUS mode showed a significantly higher detection rate of tissue prolapse than traditional IVUS (68.0% vs. 48.0%). Therefore, this integrated system is not merely a simple functional overlay but can inversely enhance the diagnostic efficacy of a single modality. Additionally, the system’s 40mm/s pullback speed and 150mm imaging length significantly optimize surgical workflow and efficiency while ensuring safety.[17]。However, the study also prudently pointed out unresolved challenges, including its deliverability in complex lesions, the ability to precisely characterize culprit lesion plaques, and how to effectively integrate dual-modal information to reduce the cognitive load on operators. These issues are not only obstacles that synchronous imaging technology needs to overcome in moving from clinical validation to widespread application, but also establish a clear direction for the development of next-generation medical devices.Table 3-3:Comparison of IVUS+OCT Synchronous Imaging System with IVUS[17]

4. Centralized Bulk Procurement: Can It Bring Opportunities for Domestic Substitution?

4.1 Policy Background and the Evolution of Centralized Procurement

Intravascular Imaging Catheters: The End of an Era and the Dawn of a New Phase

4.2 Zhejiang Provincial Alliance Centralized Procurement: Rules, Results, and Market Impact

The alliance procurement organized by Zhejiang Province covers the entire country, making it the largest and most influential specialized procurement event in this category currently, which has had a profound impact on the industry's development.[18]。

The design of the centralized procurement rules emphasizes the balance between price control and technological development. The core rule is to categorize intravascular ultrasound catheters into "mainstream application group below 60MHz" and "high-end technology group at or above 60MHz" based on technical parameters and clinical application scenarios, and determine the ranking of selected enterprises and the agreed procurement volume based on the bidding of products below 60MHz. Meanwhile, a price cap management (the winning bid price of low-frequency products from the same enterprise plus 650 yuan) was implemented for high-end products ≥60MHz, creating an effect of "one product bidding, full range linkage."

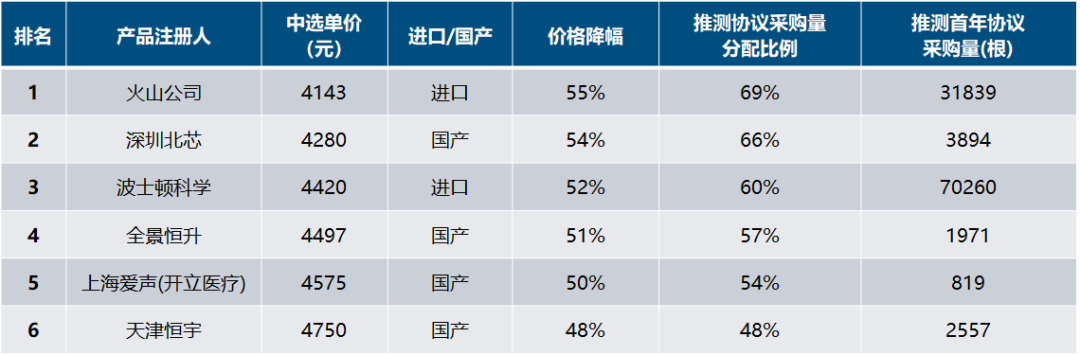

The winning bid results significantly reshaped the product pricing system. The 2024 selection results revealed a substantial drop in the end-user prices of intravascular ultrasound catheters, with an average reduction of approximately 53% (based on a reference price of 9,208 yuan). Some mainstream products that were originally priced above 10,000 yuan have now dropped to around 4,000 yuan.[18]Based on the publicly announced first-year demand volume and the rules of this centralized procurement, we have speculated on the distribution ratio and the agreed procurement volume of this centralized procurement agreement.

Table 4-1:Zhejiang Provincial Alliance Intravascular Ultrasound Volume-based Procurement Selected Results (Below 60MHz)[28]Table 4-2:Zhejiang Provincial Alliance Intravascular Ultrasound Volume-based Procurement Results (60MHz and Above)[28]New Characteristics Emerge in Market Competition During the Centralized Procurement Process. In mainstream application groups, a "price inversion" phenomenon has occurred where imported brands offered lower prices than domestically produced brands, reflecting the aggressive pricing strategies adopted by import manufacturers to maintain their market share. In technical groups of 60MHz and above, the market is initially showing a pattern dominated by two companies: Boston Scientific and Shenzhen Beixins, with relatively stable price levels.

4.3 Regional Implementation and Policy Coordination of Centralized Procurement Results

After the centralized procurement results were announced, provinces and cities across China successively issued implementation documents to ensure the policy was enforced. For example, regions such as the Beijing-Tianjin-Hebei "3+N" Alliance quickly followed up with implementation.[19]. Guangdong Province, with its large base of market demand, has effectively driven the implementation of the centralized procurement results.[20]In addition, the "pending allocation" mechanism has been introduced in this centralized procurement rule, which ensures the basic procurement volume for the selected enterprises while granting medical institutions certain secondary choice rights to better match clinical needs and encourage technological advancement.

4.4 Analysis of Market Landscape Changes Based on the First-Year Procurement Demand

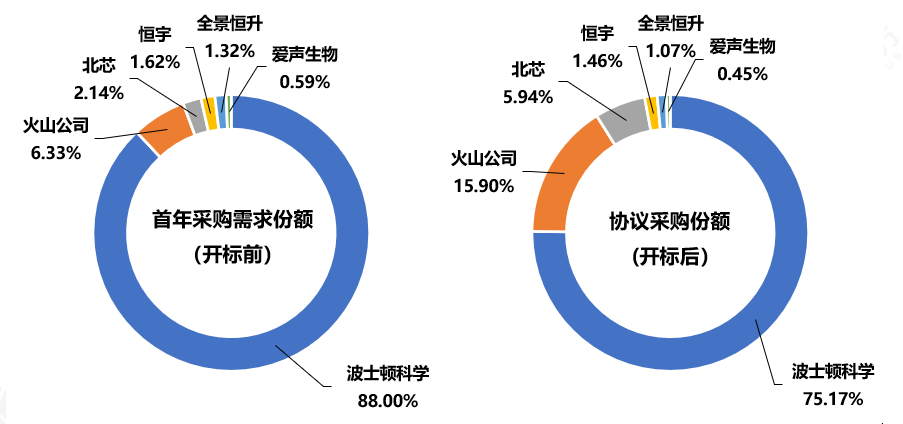

By comparing the estimated procurement volume before the centralized procurement based on publicly available data with the final agreed procurement volume determined by the centralized procurement, one can intuitively observe the structural changes in the intravascular ultrasound market before and after policy intervention. Although the overall market still maintains a pattern dominated by imported brands, significant differentiation has emerged in internal competitive dynamics and brand concentration.

In the first year of public procurement demand, the market showed a very high concentration. Boston Scientific, with its large installed base of main equipment, accounted for about 88.00% of the market share, holding a significant leading position. In contrast, Volcano Corporation, as part of the second tier of imported brands, holds a share of approximately 6.33%. Domestic brands, represented by Shenzhen Beixing, have made technological breakthroughs but still hold a relatively low combined share, with Shenzhen Beixing accounting for about 2.14%. This disparity in market structure mainly stems from the unique "main unit + consumables" strong binding model in this field. Intravascular ultrasound catheters must be used in conjunction with specific main equipment, and this closed technical barrier makes it difficult for medical institutions to switch brands simply by changing consumables without updating the main equipment, thus solidifying the brand landscape in the existing market.

Figure 4-1:The First-Year Procurement Demand Share Before Centralized Procurement (Left) and the Agreement Procurement Share After Centralized Procurement (Right)

After the publication of the centralized procurement results, the allocation of contracted procurement volumes not only revealed a rebalancing of the market landscape but also validated the effectiveness of the aforementioned barriers. Although imported brands still dominate, internal shifts in market share occurred due to varying bidding strategies adopted by different companies. Volcano Corporation adopted an aggressive pricing strategy, with its mainstream group’s bid price falling below that of some leading domestic firms. This approach significantly increased its contracted procurement share from 6.33% before the procurement process to 15.90%, making it the company with the most notable market share growth under this procurement scheme. Meanwhile, Boston Scientific retained 75.17% of the contracted procurement share, maintaining its top position in the market, but this figure represents a noticeable decline compared to its pre-procurement levels. While the centralized procurement successfully reduced the end-user prices of medical consumables through competitive bidding, its regulatory impact primarily focused on operational costs and did not directly address the allocation of main equipment categorized as fixed asset investments. For medical institutions, the high cost and long replacement cycle of main equipment make it difficult to immediately discard existing imported devices solely based on the price advantage of domestically produced catheters. The high switching costs at the equipment level contribute to the strong rigidity of the current market share distribution.Therefore, this round of centralized procurement did not immediately lead to the anticipated explosive growth of domestically produced alternatives. Data shows that the share of Chinese brands in the contracted procurement volume did not increase significantly; Shenzhen NorthX's share rose to 5.94%, while other domestic manufacturers saw their shares squeezed to a certain extent. This phenomenon indicates that as long as the stock advantage of imported brands' main equipment remains undiluted, domestically produced catheters, despite having a price advantage, will struggle to enter markets lacking hardware support. Additionally, the "price inversion" phenomenon observed among imported brands during the procurement process has, to some extent, weakened the cost-performance advantage of domestic brands. In summary, while the centralized procurement has effectively ended the era of high profit margins in the pricing system, it faces structural issues of "equipment anchoring" in reshaping market share. A single round of consumables procurement cannot disrupt the fundamental competitive landscape determined by installed equipment in the short term. The future progress of domestic substitution will depend more on the clinical adoption rate of domestically produced main equipment and performance in the secondary competition within the "undistributed volume" market.5. From NextDevice®Outlook on the Path and Progress of China's Domestic Substitution in the Medical Device Bidding Module

The preceding text thoroughly discusses the reshaping impact of centralized bulk procurement policies on the price system and competitive rules within the intravascular ultrasound imaging industry, exploring the theoretical possibility of breaking import monopolies through a "volume-for-price" mechanism. However, the intravascular imaging sector follows a strict "main unit + consumables" commercial closed-loop model. Against the backdrop of differentiated policies where IVUS catheters have been included in bulk procurement while OCT catheters remain primarily in market-driven competition, whether the pricing dynamics in the consumables market can influence purchasing decisions for equipment (main units) and thereby drive domestic substitution at the equipment level needs to be verified through actual performance in the end-user market. This chapter will be based on PharmaCube NextDevice.®Data Statistics of China's Medical Device Bidding Module: An Analysis Based on the Actual Equipment Bidding Performance in the 2025 Market

5.1 Panorama of China's Intravascular Imaging Equipment Bidding in 2025

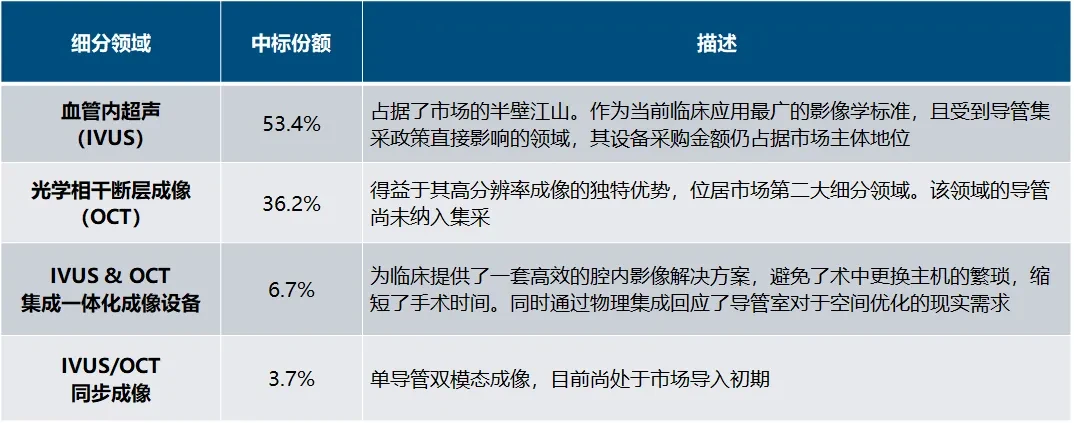

According to NextDevice®Data Statistics of China's Medical Device Bidding Module (Best-Selling Product Tag "Intravascular Imaging Equipment"): As of December 15, 2025, China's intravascular imaging equipment market has demonstrated a distribution pattern dominated by single-modality technology, with multi-modality fusion technology gradually penetrating. It should be noted that although the publicly announced bidding amounts do not directly equate to enterprises' final revenue, as a direct reflection of end-user hospital procurement intentions, this data is sufficient to objectively represent the current market热度 and competitive landscape.

Table 5-1:NextDevice®Market Share of Intravascular Imaging Devices in China's 2025 Bidding by Sub-Segments

5.2 Localization Process: Nonlinear Correlation Between Policy Impact and Market Choice

Based on the 2025 equipment bidding data, a comparison of market performance between the IVUS (already included in centralized procurement) and OCT (not yet included in centralized procurement) fields reveals that the progress of domestic substitution in the equipment sector shows significant structural differences and does not entirely follow the linear logic of "centralized procurement-driven substitution."

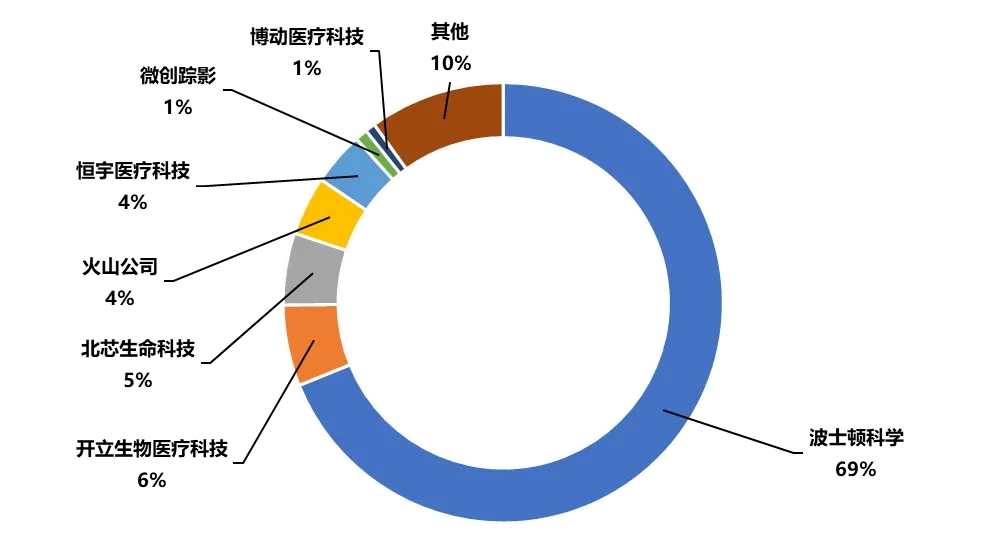

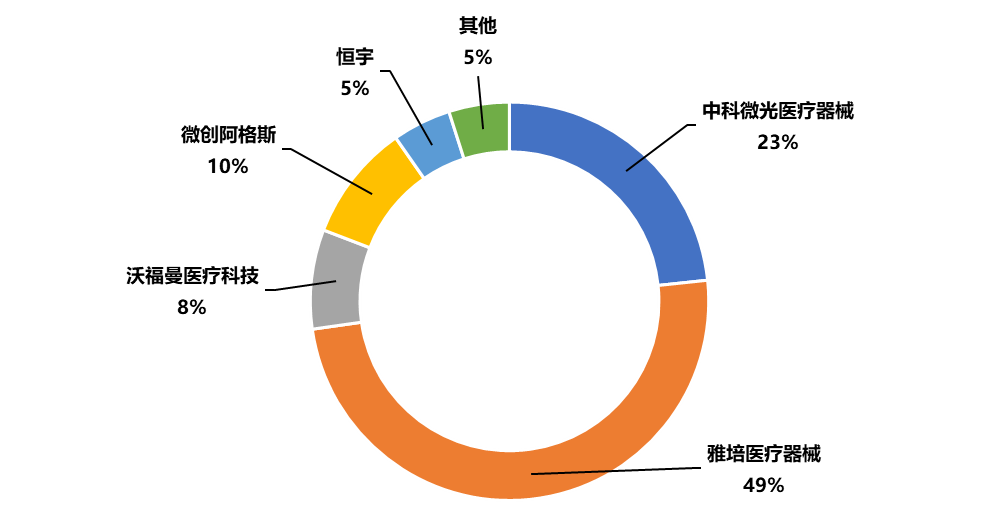

5.2.1 IVUS Equipment Bid Data for 2025In the Intravascular Ultrasound (IVUS) field, despite its dedicated consumables (catheters) having undergone provincial alliance centralized procurement in 2024 with an average price reduction of approximately 53%, the 2025 equipment bidding results show that imported brands still maintain a high level of monopoly. Data indicates that Boston Scientific accounts for about 69% of the winning bid amount, and together with Volcano Corporation at 4%, imported brands collectively occupy approximately 73% of the market share. This phenomenon suggests that the centralized procurement of consumables has not triggered a wave of domestic substitution on the equipment side in the short term. One reason is the high conversion cost posed by the large installed base of imported brands; another reason is that the decline in consumable prices has reduced the per-use operating cost of imported equipment for hospitals, which to some extent reinforces the usage stickiness of imported mainframes. Therefore, in the IVUS sector, domestically produced equipment still faces significant market barriers, and the substitution process remains relatively slow.Figure 5-1:NextDevice®Market Share of IVUS Devices in China's Tendering Module for Medical Devices in 20255.2.2 2025 OCT Equipment Bidding DataIn the field of Anterior Optical Coherence Tomography (OCT), its consumables have not yet been included in large-scale centralized procurement, and it operates entirely within a market-driven competitive environment. However, the substitution rate of domestically produced equipment is significantly higher than in the IVUS field. Although Abbott holds the top position with a 49% share, the combined market share of domestic manufacturers has surpassed Abbott’s at 51%. Among them, Zhongke Micro-Light holds 23% of the market, ranking first among domestic brands, while MicroPort Argus accounts for 10%. This phenomenon, where "the substitution rate is higher in fields without centralized procurement," indicates that domestic companies can effectively break through import barriers through rapid technological iteration (such as frequent product registration approvals) and differentiated market strategies, even without administrative intervention. It also reflects that, as a relatively new track, OCT technology does not have the same historical depth or exclusive barriers as the IVUS field, offering greater access space for domestically produced equipment.Figure 5-2:NextDevice® China Medical Device Bidding Module: 2025 OCT Equipment Market Share by Company

5.3 Market Validation of Technical Routes: Differentiation Path Analysis Based on Best-Selling Models

Facing the first-mover advantage and existing barriers of imported brands in the single-modality imaging field, have Chinese-produced enterprises explored effective market entry pathways? The 2025 equipment model bidding data provides critical empirical evidence.

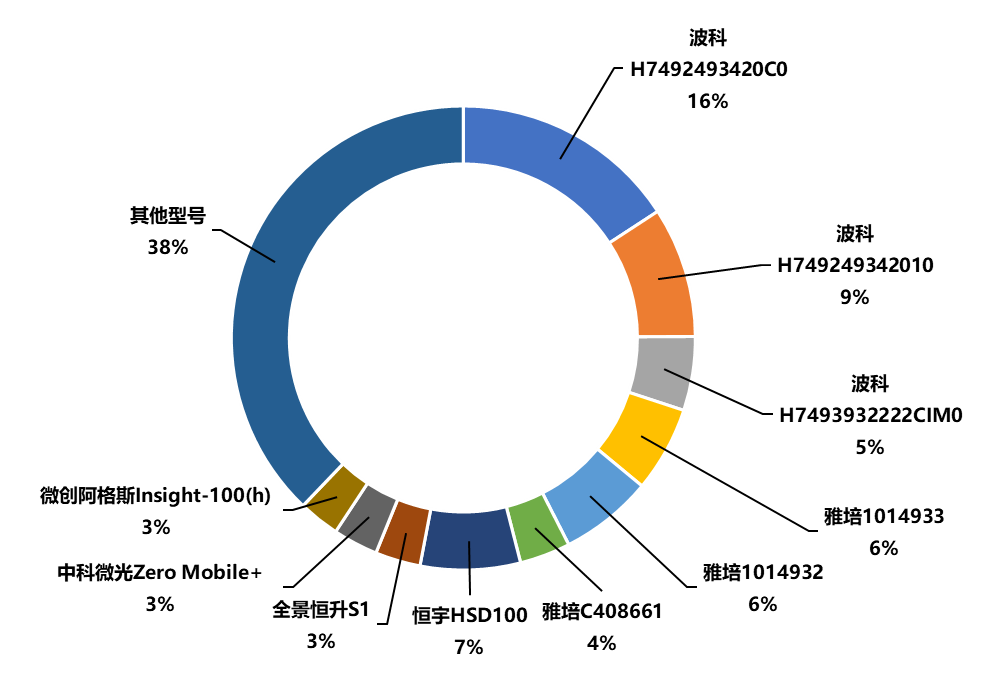

Figure 5-3:NextDevice®Top 10 Models by Bid Amount for Intravascular Imaging Devices in China's Equipment Bidding Module in 2025Data shows that the intravascular imaging equipment field exhibits a high level of market concentration. Boston Scientific maintains a significant market-leading position with its mature product portfolio, as its three IVUS console models combined account for approximately 30% of the market share. Notably, a single model, H7492493420C0, holds a market share as high as 16%, firmly ranking first. This highly concentrated distribution pattern indicates that in the traditional single-modality IVUS track, imported brands have built substantial replacement costs and user stickiness through long-term clinical application accumulation and a large installed base. For domestically produced enterprises in China, homogeneous competition within a single technological dimension is unlikely to effectively disrupt the existing market landscape.However, against this competitive backdrop, domestically produced equipment has demonstrated differentiated competitive advantages in the field of multimodal fusion. Horimed's HSD100 system, an integrated IVUS and OCT device, ranks third on the single-model list with a 7% market share, making it the domestically produced model with the highest market share currently. The standout performance of this data validates the market value of the "engineering integration" approach: solving the problem of limited catheter lab space through physical integration while reducing the comprehensive cost for hospitals purchasing multiple standalone units. The market success of HSD100 demonstrates that providing solutions to meet clinical demands for space optimization and cost control is a viable path for domestically produced equipment to bypass the core strengths of imported brands and achieve effective market penetration.At the same time, the S1 system from Acoustic Life Science Co., Ltd. represents a breakthrough in another technological dimension — IVUS/OCT synchronous imaging. Although this model currently holds a 3% market share and has not yet entered the top tier, it dominates the bidding amount in the synchronous imaging niche for 2025. Unlike integrated devices that focus on physical consolidation, synchronous imaging technology aims to enhance the dimensions and efficiency of clinical diagnosis, achieving both deep penetration and high-resolution images in a single pullback. Due to the relatively late layout of imported brands in this technology field, domestically produced enterprises have gained a valuable technical window period.In summary, the 2025 model bid data reveals a profound shift in the logic behind domestic substitution. Amidst the landscape dominated by multinational corporations like Boston Scientific in single-modality markets, leading Chinese manufacturers are gradually moving away from pure price competition and instead building differentiated competitiveness through multi-modality fusion technologies. Whether it is Horimed's success in engineering integration or Panoramic Hengsheng’s exploration of synchronous imaging technology, it demonstrates that "technological elevation" has become the core driving force for domestically produced devices to break through existing barriers and reshape the market structure.6. Reshaping the Future: The Wave of Technological Innovation and New Starting Points

With the normalization of centralized procurement, intravascular imaging technology has officially bid farewell to the era of "high premium optional" and moved towards a new cycle of "universal must-have." Market data in Chapter Five shows that pure price competition can hardly shake the stock barriers of imported brands, and only technological innovation can build new competitive moats. Looking ahead, industry competition will focus on three-dimensional competition across three key dimensions: deep integration of multimodal technologies, continuous race towards extreme high-definition, and AI-driven decision empowerment throughout the entire process.

6.1 Multimodal Imaging: From Physical Integration to Clinical Deep Fusion

The approval and market launch of the IVUS/OCT synchronous imaging system marks the initial engineering integration of multimodal imaging technology. However, in clinical practice, the simple side-by-side display of dual images often leads to information redundancy, increasing the burden on operators for image interpretation. Therefore, the development direction of this technology is shifting from basic physical superposition towards deep clinical information fusion.

First, the catheter design needs to focus on optimizing its passage performance. Due to the integration of dual sensors, early synchronous imaging catheters generally have problems such as larger outer diameters and higher tip rigidity, which limits their application in tortuous vessels and complex lesions. The future R&D focus is on further miniaturization and improving the flexibility of the catheter. For example, the catheter developed by Terumo with an outer diameter of only 2.6Fr reflects this trend, aiming to expand the application of synchronous imaging technology from specific high-risk lesions to more routine clinical scenarios. It also received FDA 510(k) approval on October 24, 2025, and officially launched in the United States.[21]。

Figure 6-1:Terumo OPUSWAVE®Imaging SystemSource:Terumo Official Website[21]Secondly, the core task of the software algorithm is to achieve precise registration and fusion of images. An ideal system should be able to use artificial intelligence algorithms to spatiotemporally register the microscopic intima structure information (such as thin-cap fibroatheroma) obtained by OCT with the full-layer vessel contour data provided by IVUS, and generate a unified fused image. This technology is expected to automatically identify and label key pathological features, thereby significantly reducing the cognitive load on physicians and shortening the time for image analysis.Finally, multimodal imaging will further expand to integrated assessment of structure and function. For example, MicroLight Medical (ZK MicroLight) is exploring a multimodal OCT system that integrates blood flow assessment functionality, which has successfully received FDA approval, marking another breakthrough for China's high-end medical equipment in the vascular intervention field.[22]### TranslationPulse Medical's image-based computation of Fractional Flow Reserve (UFR/OFR) offers another technical pathway. Relevant clinical studies have confirmed that UFR, computed from IVUS images, shows a high degree of consistency with the gold standard FFR (diagnostic accuracy rate of 92%), and its diagnostic performance (AUC 0.97) is significantly superior to traditional minimum lumen area assessment. This verifies the feasibility of achieving rapid and precise functional evaluation without the need for pressure wires. Future systems are expected to simultaneously obtain vascular anatomical structure, micro-pathological morphology, and functional parameters through a single catheter pullback, thereby reshaping the decision-making model for interventional diagnosis and treatment of coronary heart disease.[23]。Figure 6-2:The Multimodal Intravascular Imaging System by CAS MicroLightSource:MicroLight Official Website[22]

6.2 High-Definition Imaging: Frequency Enhancement and Image Quality Optimization

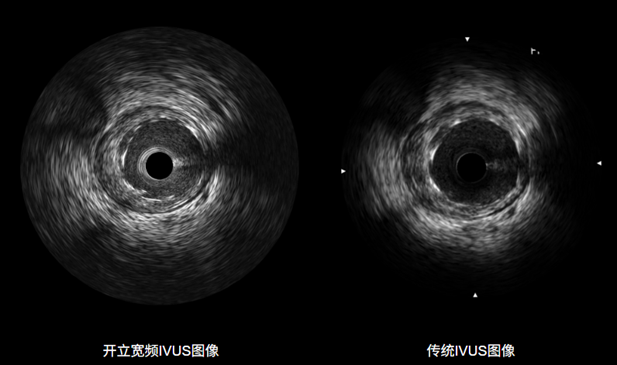

In the single-modality IVUS field, as the 40MHz probe has become the clinical standard configuration after centralized procurement, the industry is entering a high-resolution development phase represented by 60MHz. Companies such as Acoustic Life Science Co., Ltd., Boston Scientific, and SonoScape have successively launched related products. However, the increase in ultrasound frequency is constrained by the physical limit of attenuation in penetration power, making it difficult to meet the imaging needs of deep tissues solely by raising the frequency. Therefore, the focus of technical competition is shifting towards systematic optimization of image quality.

Intelligent frequency conversion and broadband technology provide a feasible solution to balance the contradiction between resolution and penetration. For instance, the 20–90MHz ultra-wideband technology proposed by SonoScape theoretically allows the system to dynamically adjust the transmission frequency based on imaging depth: using high frequency in the near-field area to capture fine structures of the tube wall, and switching to low frequency in the far-field area to ensure sufficient penetration depth, thereby achieving clear imaging across the entire depth range.[24]In addition, image enhancement technology based on deep learning has become an important supplement to hardware optimization. Through advanced signal denoising and processing algorithms, the system can effectively improve the image signal-to-noise ratio on the basis of existing hardware, more accurately delineate tissue boundaries, suppress artifacts, and achieve multi-dimensional optimization of image quality.Figure 6-3:Comparison of SonoScape Broadband IVUS and Traditional IVUS ImagesSource: SonoScape Official Website[24]

6.3 Artificial Intelligence Applications: Evolution from Automated Measurements to Full-Process Decision Support

The application of artificial intelligence in intravascular imaging is undergoing a profound transformation from an auxiliary tool to a core decision support system. This evolution can be roughly divided into three stages: automated measurement, intelligent diagnosis, and integrated decision support.

Currently, mature platforms such as Abbott's Ultreon and Philips' IntraSight have achieved automated contouring and measurement of the lumen and stent, enhancing the standardization and efficiency of measurements. The current technological frontier is moving towards intelligent diagnosis and risk prediction. Through deep learning algorithms, systems can quantify and identify vulnerable plaque characteristics and integrate clinical risk models to predict the risk of future cardiovascular adverse events in patients.[25][26]The AI large model released by Pulse Medical aims to generate structured reports containing such risk warning information.[27]。

The future development direction lies in building an intelligent decision-making navigation system that covers the entire process of interventional treatment. This system will integrate virtual functional assessments (such as UFR/OFR) to complete physiological evaluations without relying on pressure wires. Furthermore, artificial intelligence can fuse preoperative coronary angiography with intraoperative intravascular imaging data to construct a digital model of the coronary arteries, enabling virtual stent implantation simulation, real-time intraoperative navigation, and automatic postoperative effect evaluation, ultimately forming a closed-loop decision support system for interventional treatment.7. Conclusion

This report, based on market empirical data from 2025, systematically reviews and recaps the development logic and analytical framework of China's intravascular imaging industry under the intersection of normalized centralized bulk procurement and rapid technological iteration. The full text follows an analytical path that moves from technical principles to policy impacts, and then to market performance: starting with the analysis of the physical mechanisms of sound waves and light waves, passing through multiple rounds of implementation and impact of centralized bulk procurement policies, and finally focusing on terminal market bidding results and cutting-edge technological advancements. This complete logical deduction process not only reveals the underlying dynamics beneath the surface phenomena of the industry but also provides a multi-dimensional evidence-based answer to the core question raised at the beginning of the report — "Can centralized procurement directly drive domestic substitution?"Logical review shows that the development of China's intravascular imaging market has moved away from a simple linear substitution model. Although the centralized procurement policy has significantly compressed the price space for consumables through a "volume-for-price" mechanism and increased clinical penetration, the 2025 bidding data reveals a more complex phenomenon: In the intravascular ultrasound (IVUS) sector, imported manufacturers have built a resilient market barrier by relying on a strong "main unit + consumables" binding business model and a large base of existing equipment; a single consumable price advantage did not lead to systematic substitution at the equipment level in the short term. In contrast, in the optical coherence tomography (OCT) field, which has not yet been deeply covered by centralized procurement, and in emerging multimodal imaging, domestic companies have achieved higher market share through rapid R&D iteration and differentiated product strategies. This comparison clearly indicates that while administrative regulation can break price barriers, it alone cannot dismantle the commercial moats constructed by long-term technological accumulation and closed-loop ecosystems.Therefore, regarding the core issue of "the path to domestic substitution," the conclusion of this report is: Centralized procurement merely provides an entry opportunity for domestic companies to enter the mainstream market, rather than being the decisive factor in determining the final competitive outcome. The true reshaping of the market structure is shifting from low-dimensional homogeneous price competition to high-dimensional differentiated value competition. As multinational corporations like Boston Scientific advance localized production, their cost structures have gradually converged with domestic brands; under this new normal, technological upgrading has become the key variable for breaking through. Whether it is Horimed's engineering breakthroughs in IVUS/OCT integrated devices, Acoustic Life Science Co., Ltd.'s clinical innovations in synchronous imaging technology, or Northcore Life’s performance improvements in 60MHz high-frequency imaging, all indicate that only by providing comprehensive solutions that surpass the clinical value of existing imported equipment can one truly break through the established market landscape.Looking ahead to the next five years, China's intravascular imaging industry will enter a new stage of development defined by "technology-driven markets." As multimodal fusion technology evolves from physical integration to deep clinical collaboration, and artificial intelligence progresses from auxiliary measurement to full-process decision support, intravascular imaging will no longer merely serve as a "validation tool" for coronary intervention but is expected to become a "navigation system" for guiding precision interventions. During this transformation from "following innovation" to "independent innovation," companies that can lead the shift from single consumables suppliers to providers of intelligent, multimodal diagnosis and treatment solutions will gain a competitive edge in the fierce market competition, thereby driving China's medical device industry to achieve a historic leap from "China-made substitution" to "global competition."

NextDevice Medical Device Database

![]()

![]()

NextDevice®Is a full-life-cycle database of medical devices built by PharmaCube, covering the field of devices “Product、Sales、R&D、Investment"Four core scenarios. Through the method of 'AI big data monitoring and collection + professional data analyst review and cleaning,' Mofang has built a high-precision structured data system. It conducts in-depth cleaning and standardization processing on information such as the classification of device products, technological generations, medical service items, indications, popular tracks, performance features, and online listing/bidding results. At the same time, it further integrates and connects the global device labeling system, fully synchronizes information on devices under research and investment dynamics from various sources, spans the entire life cycle of medical devices, and achieves multi-dimensional competitive landscape analysis and decision support for devices."

1 https://finance.sina.com.cn/stock/med/2025-12-05/doc-infztyiy8315374.shtml2. https://eurointervention.pcronline.com/article/his-masters-art-andreas-gruntzigs-approach-to-performing-and-teaching-coronary-angioplasty3. https://clinicalgate.com/intravascular-ultrasound-principles-and-clinical-applications/4. https://www.bostonscientific.com/us/en/healthcare-professionals/products/intravascular-ultrasound-devices/catheters-and-guidewires/coronary-catheters/opticross-hd-coronary-imaging-catheters/fp00000330.html#marketingContent5. 10.4244/EIJ-D-21-000896. https://www.cardiovascular.abbott/us/en/hcp/products/percutaneous-coronary-intervention/dragonfly-opstar-imaging-catheter/overview.html7. 10.3389/fcvm.2020.001198. 10.3389/fcvm.2025.15958899. 10.1016/j.jcin.2024.06.03010. https://horimedtech.com/products/60.html11. 10.1056/NEJMoa221660712. 10.1016/j.jcin.2019.09.03313. 10.1016/S0140-6736(24)00282-414. 10.4244/EIJV10I12A24515. 10.1161/CIRCULATIONAHA.123.06642916. 10.1016/j.iccl.2022.12.00217. 10.4244/EIJ-D-22-0105818. https://zjjcmspublic.oss-cn-hangzhou-zwynet-d01-a.internet.cloud.zj.gov.cn/jcms_files/jcms1/web3190/site/attach/0/f04093ca5dac4ea0a2a7e6368fe82f2e.pdf19. https://ylbz.tj.gov.cn/xxgk/zcfg/ybjwj/202405/t20240530_6638454.html20. https://hsa.gd.gov.cn/zwgk/zfxxgkml/bmwj/qtwj/content/post_4438419.html21. https://www.terumo.com/newsrelease/detail/20251024/676622. https://www.vivolight.cn/index/news/detail.html?id=14323. 10.1161/CIRCINTERVENTIONS.120.00984024. https://www.sonoscape.com.cn/html/2023/IVUS_0228/118.html25. https://www.cardiovascular.abbott/int/en/hcp/products/percutaneous-coronary-intervention/intravascular-imaging/ultreon-software/ultreon-1-0.html26. https://www.philips.com.tw/healthcare/resources/landing/intrasight27. https://www.pulse-imaging.com/col.jsp?id=13728. https://ylbzj.wuxi.gov.cn/doc/2024/05/30/4319848.shtml