China's CRO Industry: From Emergence to Capital Market Frenzy

In 2018, WuXi AppTec’s initial public offering set off a capital frenzy in China’s pharmaceutical market. Prior to this, ChemPartner and Huawei Pharma had also accessed the A-share market through restructuring. Moreover, a host of leading companies, including Pharmaron, Medicilon, and Pharmsynthez (YaoShi Technology), submitted their IPO applications in 2017 and are on the verge of listing.

After nearly two decades of development, China’s CRO industry has undoubtedly grown from scratch and is now making robust strides toward the capital market on a large scale.

CROs are an essential infrastructure in the process of pharmaceutical innovation, providing specialized services to pharmaceutical companies and R&D institutions during drug development through contractual agreements.

This model originated in the United States. During the 1970s and 1980s, the U.S. healthcare payment system underwent reform, with fee-for-service gradually transitioning toward prospective payment systems and managed care. This shift impacted pharmaceutical companies, prompting them to place greater emphasis on investment in innovative R&D to address the increasingly challenging trends in drug consumption. To enhance efficiency and meet the substantial R&D demands of numerous enterprises, the contract research organization (CRO) model emerged.

These services include preclinical studies, clinical trials, technology transfer, and consulting, covering the entire process from new drug discovery and clinical development to regulatory registration. As the CRO market matures, diverse business models such as contract manufacturing and industry-academia collaborations have emerged, making CROs an increasingly vital segment of the pharmaceutical and biotechnology industries.

In 1996, MDS Pharma Services invested in China to establish the country’s first true contract research organization (CRO), primarily providing clinical research and development services for new drugs to pharmaceutical companies. In 1997, Quintiles, the world’s largest CRO, entered the Chinese market, followed by other multinational CROs such as Covance and Kendle, which subsequently established branches in China.

The entry of these multinational pharmaceutical companies sowed the seeds of the CRO industry in China. Despite some initial challenges in adapting to the local environment, their presence ultimately sparked the initial momentum that ignited the Chinese CRO market.

However, the true emergence of Chinese CROs dates back to 2000.

When the first company, Pharmacopeia, went public, Li Ge was only 28 years old. In 1999, while invited back to his alma mater to deliver a lecture, he observed a peculiar phenomenon in China’s pharmaceutical industry at the time: most innovative drugs were held by foreign enterprises, technological advancements remained confined to universities and laboratories, and the vast majority of commercial companies were engaged solely in the production of generic drugs. The entire domestic pharmaceutical market suffered from weak innovation capabilities, with a serious disconnect among industry, academia, and research.

Gaps in the market often signify opportunities.

In 2000, Li Ge gave up the achievements he had already made in the United States and decided to return to China to start a business again. At the end of that year, Li Ge, together with three other partners, founded WuXi AppTec in Waigaoqiao, Shanghai.

Starting with a 700-square-meter laboratory and four employees, the company became a legend in the history of China’s pharmaceutical industry within just a few years. It pioneered the localization of contract research organizations (CROs) in China, earning its founder, Li Ge, the title of “the first person in China’s pharmaceutical R&D outsourcing industry.”

The period after 2000 can be regarded as the nascent stage for domestic Chinese CRO companies. Apart from WuXi AppTec, the other members of the “Four Giants” of China’s pharmaceutical CRO industry were all established in succession during these years.

In 2002, Hui Xin started from scratch, launching his venture with five employees in a laboratory of just over ten square meters in Zhangjiang. The company he founded, Pharmaron (Shanghua Medicine), ultimately became a shining star in China’s CRO industry. In the same year, Wang Tingchun established Boji Medicine in Guangzhou. These two companies went public in 2010 and 2015, respectively; notably, Shanghua Medicine returned to the A-share market after completing its privatization in the United States in 2013.

The following year, Shanghua Medicine established a subsidiary, ChemPartner, which primarily provides preclinical research services to enterprises. In 2017, ChemPartner was acquired by Quantum Hi-Tech for RMB 2.38 billion.

Three years after the establishment of WuXi AppTec, China’s CRO industry has once again reached a milestone.

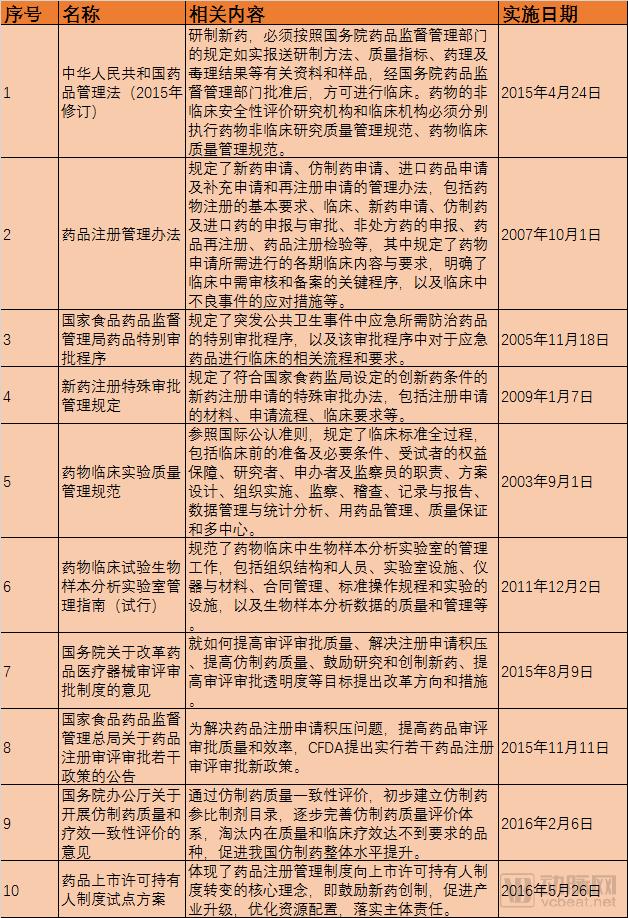

In 2003, the Good Clinical Practice for Drug Clinical Trials (hereinafter referred to as the "GCP") was officially promulgated in June after being reviewed and approved by the executive meeting of the National Medical Products Administration.

According to the provisions of the “Good Clinical Practice” (GCP), sponsors of clinical trials may entrust contract research organizations (CROs) with certain tasks and responsibilities in the conduct of clinical trials, thereby legally affirming the role and status of CRO companies in new drug development. The GCP officially came into effect in September of the same year, laying the foundation for the development of China’s CRO industry.

Leading companies such as Pharmaron, ChemPartner, Medicilon, Rundo Pharma, and Porton Pharma Solutions emerged during this period. China’s CRO industry officially transitioned from its nascent stage into a phase of rapid development.

In 2004, Lou Boliang returned to China from San Diego, where he had spent eight years in the biotech sector, to launch a startup. He founded Pharmaron in Beijing, focusing on chemical synthesis. At the time, Pharmaron consisted of just five employees and a small laboratory. Within three years, the company grew to become one of the top three players in the industry, securing major international pharmaceutical companies such as Merck and Pfizer as clients.

Also established during the same period were Tigermed and Medicilon, both of which subsequently grew into leading enterprises in the CRO sector. Notably, Tigermed listed on the Shenzhen ChiNext Market in 2012. With service networks across 50 major cities in China, as well as in Canada, the United States, South Korea, Japan, Australia, Malaysia, and Singapore, the company has successfully delivered over 400 clinical trial services to more than 300 clients worldwide.

If the entry of foreign CROs before 2000 offered Chinese pharmaceutical companies a kaleidoscopic view, then after 2000, with the establishment of representative firms such as WuXi AppTec and the promulgation of Good Clinical Practice (GCP) regulations, China’s CRO industry began to grow from scratch into a robust sector, entering a period of rapid development.

In 2007, after several years of development, WuXi AppTec had grown into an industry giant with a research team of over 2,100 employees and more than 80 clients, including nine of the top ten global pharmaceutical companies. That year, WuXi AppTec successfully listed on the New York Stock Exchange and ranked 14th worldwide in its industry.

One year after its IPO, WuXi AppTec acquired the U.S. laboratory testing services company AppTec for $151 million.

By acquiring AppTec, WuXi AppTec was able to further expand its global business and broaden its customer base. It has gradually evolved into a new global pharmaceutical research and development outsourcing service company with world-leading technologies, covering both small-molecule and large-molecule drug R&D.

In the same year, Sandia Pharma also established a CRO alliance with Shanghai Lianyou Pharmaceutical and Shanghai BGI Tianyuan, aiming to achieve complementary advantages in the field of drug research and development.

However, this alliance is essentially regional in nature. In Beijing, the China Biotech Outsourcing Alliance (ABO) has been established. Comprising 16 contract research and manufacturing organizations, the alliance provides one-stop collaborative R&D services—ranging from new drug development, preclinical studies, and clinical trials to registration and contracted manufacturing—through brand sharing and marketing collaboration.

From 2006 to 2010, the domestic CRO industry did not experience the explosive growth seen in 2004. During this period, these enterprises (particularly several representative companies established around 2002) began to develop and expand, driving rapid growth in China’s CRO industry and giving rise to emerging industry giants.

It is worth noting that in April 2010, Charles River offered $1.6 billion to acquire WuXi AppTec. However, four months later, the acquisition fell through due to opposition from major shareholders.

In 2010, following WuXi AppTec, PharmaFrontiers also successfully listed in the United States, marking a new chapter for Chinese CROs going public.

Between 2010 and 2017, a total of 17 companies went public. Shanghua Medicine was the first to list in the United States. Among the remaining enterprises, three listed on the New Third Board, two on the Hong Kong Stock Exchange, and one in Taiwan; the rest were listed on either the Shanghai Stock Exchange or the Shenzhen Stock Exchange.

As can be seen, 2015 and 2016 were a dormant period for the IPOs of these companies, with only six going public over the two years. In 2017, however, the wave of CRO company IPOs began to surge: five companies successfully listed that year (notably, two of the companies that went public in 2016 did so after November), and two additional companies filed their prospectuses during the year.

Not only that, but an interesting phenomenon has emerged in recent years. The first two companies to list in the United States have both delisted, eventually returning to the A-share market through restructuring, spin-offs, and other methods.

Among them, Shanghua Pharmaceutical voluntarily delisted from the U.S. stock market through privatization in 2013. At that time, the company’s annual profit was $60 million, and its market capitalization at the time of delisting was $11.4 billion.

Shanghua Medicine injected its entire CRO and CMO businesses into its subsidiary, ChemPartner, and then injected 90% of ChemPartner’s equity into Quantum Hi-Tech, creating a joint platform for Shanghua Medicine and Quantum Hi-Tech, ultimately leading to a listing on the A-share market.

WuXi AppTec was privatized in 2015 at a market capitalization of $3.3 billion, embarking on its journey to split into three entities and return to the domestic market.

In April 2015, WuXi AppTec spun off its subsidiary, PharmaBlock, which was listed on the New Third Board. PharmaBlock is primarily responsible for providing CRO services to multinational pharmaceutical companies, focusing on small-molecule drug intermediates, active pharmaceutical ingredients (APIs), and formulations.

In June 2017, its subsidiary, WuXi Biologics, was officially listed on the Hong Kong Stock Exchange. This segment is positioned as an “open-access biologics technology platform,” primarily providing services for the discovery, development, and manufacturing of biologic drugs.

In May 2018, WuXi AppTec listed on the A-share market, marking the successful completion of its “one-into-three” listing on the capital markets.

As of now, WuXi AppTec has a market capitalization of nearly RMB 90 billion, WuXi Biologics HK$101.9 billion, and STA Pharmaceutical approximately RMB 20 billion, bringing the combined market cap of the three WuXi-affiliated companies to nearly RMB 200 billion. As WuXi AppTec’s new shares continue to attract strong investor demand, the market valuations of the three listed companies in the WuXi group are expected to keep rising.

CROs serve as the infrastructure for pharmaceutical innovation. To some extent, policy and market guidance toward pharmaceutical innovation have also promoted the development of CRO enterprises.

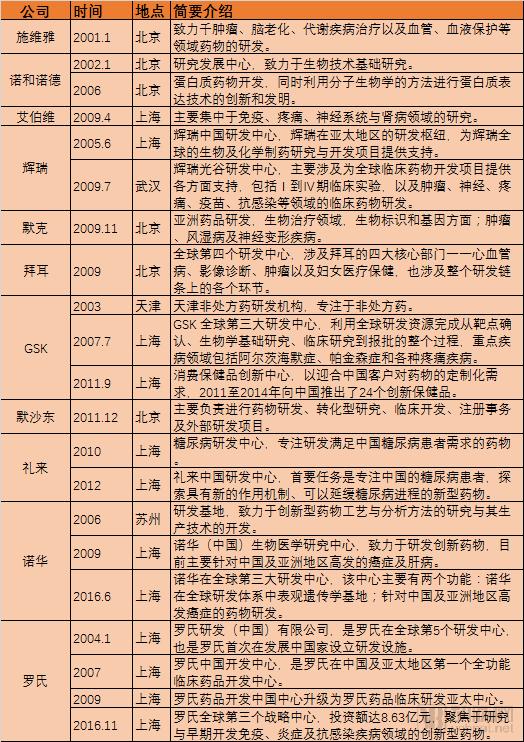

Pharmaceutical innovation in China initially took root with the entry of multinational corporations. According to statistics from Qianzhan Industry Research Institute, since 2000, multinational pharmaceutical companies have invested over RMB 10 billion in China and established dozens of new R&D centers.

Data Source: Qianzhan Research Institute

Subsequently, policy guidance steered Chinese pharmaceutical companies from generic manufacturing toward innovation, leading to the rise of numerous innovative drug enterprises. Domestic regulatory reforms, such as the consistency evaluation, further provided a fertile ground for innovation among local companies.

Previously, pharmaceutical R&D enterprises in China focused primarily on generic drugs, resulting in limited demand for pharmacological and toxicological services and a relatively small preclinical CRO market. Following national top-level design mandates that emphasized new drug innovation and gradual alignment with international standards, pharmaceutical companies increased their investment in innovative drug R&D, directly driving growth in the CRO industry.

Since 2016, China’s pharmaceutical industry has been in a golden period of rapid development, and the incremental market space has provided substantial market support for the growth of pharmaceutical R&D services.

Currently, based on the scope of services provided, CRO companies in China can be categorized into three types: First, CRO companies specializing in preclinical research. These firms are primarily engaged in activities related to new drug development, such as chemical synthesis, compound screening, process and quality standard studies, as well as pharmacological and toxicological experiments. Second, CRO companies focused on clinical research for new drugs. These firms mainly handle the design of clinical trial protocols, monitoring of study processes, management of research data, and statistical analysis. Third, CRO companies providing consulting services for new drug development and acting as agents for new drug registration applications. Although there is a large number of CRO companies across these categories, the number of firms capable of offering comprehensive, end-to-end R&D outsourcing services remains very limited.

As industry giants go public one after another, sparking a wave of IPOs, and with the Hong Kong Stock Exchange opening its doors to biotechnology companies, Chinese CRO firms will have greater opportunities.

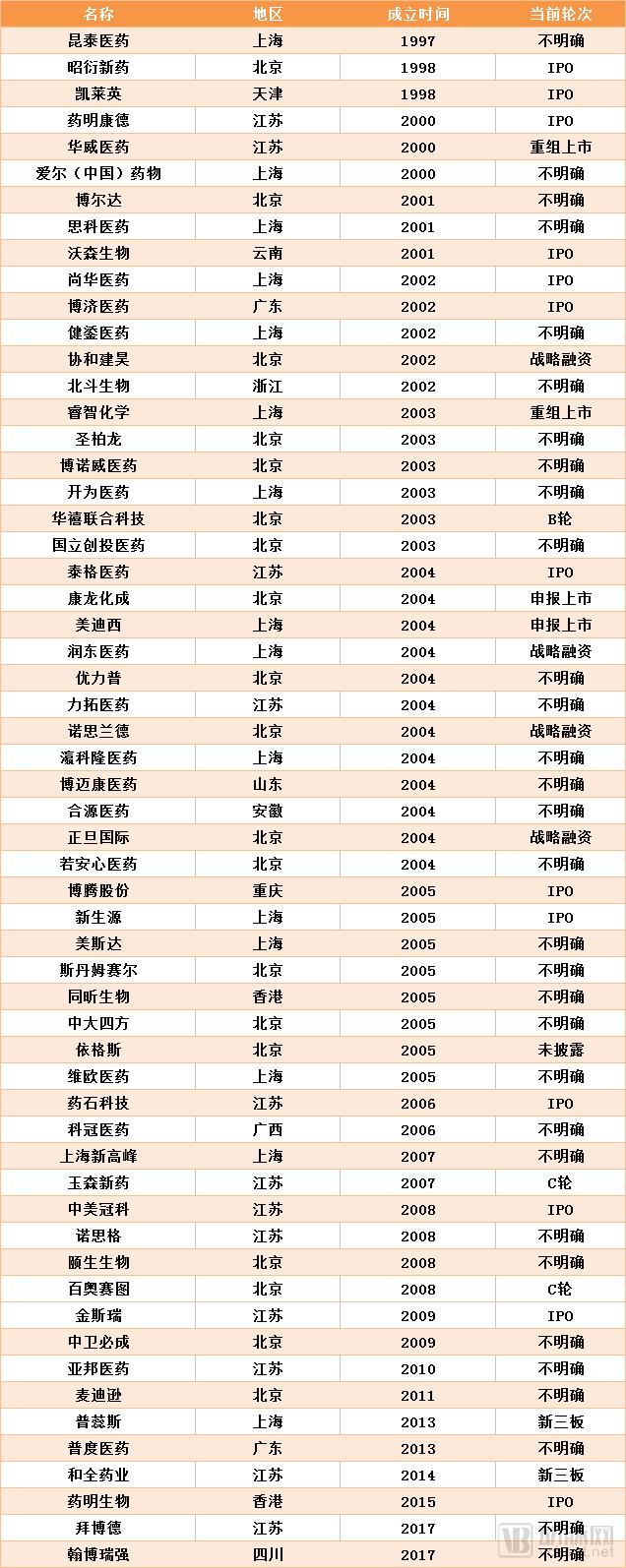

Attached is the list of companies for this inventory.