Oral Healthcare Investment Maturing: Five Irreversible Trends and Insights from Six Leading Dental Chain Models

In recent years, capital has been continuously investing in dental clinics and hospitals, with five deals alone in the first half of 2018. While investor enthusiasm for consumer healthcare (such as dentistry and medical aesthetics) remains strong, a key premise is that the dental care industry remains time-driven.

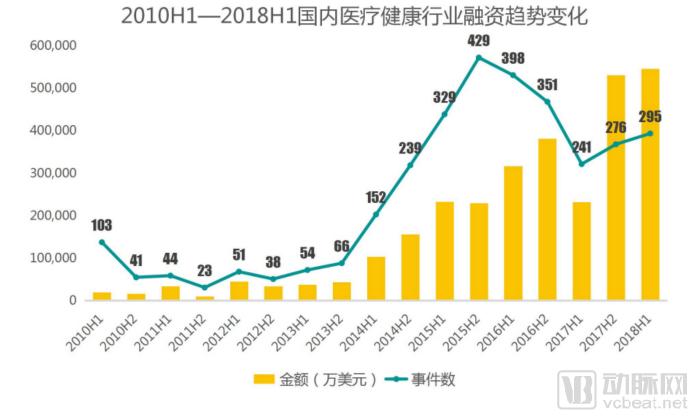

According to data from VCBeat (WeChat ID: vcbeat) and its research arm, VCBeat Institute, the domestic healthcare sector in China raised $5.46 billion in the first half of 2018, representing a substantial year-on-year increase of 135% and setting a new record for H1 fundraising in the industry. This growth was driven by seven mega-rounds exceeding RMB 1 billion each, spanning primary care, consumer healthcare, biotechnology, pharmaceuticals, and health tech. Notably, Taikang Life Insurance invested RMB 2.06236 billion to acquire a 51.56% equity stake in Bybo Medical.

Investment and Financing Trends from the First Half of 2010 to the First Half of 2018

From a capital perspective, 2015–2016 marked the peak of healthcare investment, characterized by a high volume of deals and elevated valuations of target companies. By 2017, the market gradually returned to more reasonable levels, a trend particularly evident in the dental sector.

An industry evolves from a stage where most people cannot access its offerings to a tipping point where products and services become affordable and readily available to many. At this stage, suppliers can remain competitive with minimal training. This transition generally requires three driving factors:

1. Technology-driven.Typically, the purpose of cutting-edge technology is to simplify problems by transforming empirical processes previously reliant on intuitive trial-and-error into standardized, efficient, and routine methodologies. Specifically in the field of dentistry, the adoption of digitalization is irreversible. Digital diagnostic technologies enable simpler and more efficient operations for clinicians while enhancing patient comfort, whereas the informatization of dental practices strengthens their capabilities in clinical care, management, and marketing.

2. Business Model Innovation.Deliver streamlined solutions to consumers in a profitable manner, ensuring they are both affordable and convenient. Although digitalization has been advocated in the dental field for many years, progress has not been as rapid as expected due to factors such as high equipment costs increasing clinic expenses and slow approval processes for medical devices. From a payment perspective, the integration of insurance with dental care in China is still in its early stages; orthodontics and dental implants tend to cater to mid-to-high-end users, while preventive dental care still faces significant challenges.

3. Ecological Network Collaboration.Establishing a comprehensive supply chain system to create a micro-commercial ecosystem, wherein all internal companies operate under economic models characterized by continuous innovation and mutual reinforcement. In the dental industry chain, the upstream sector—comprising equipment manufacturers, consumable suppliers, and dental laboratory processors—remains highly fragmented. Technologically, the market is still dominated by the United States (for consumables) and Germany (for devices), with domestic substitution progressing slowly. Brand building requires time, while dental laboratories are undergoing digital transformation. On the provider side, hospitals and clinics face challenges related to talent acquisition, cost management, patient shortages, and brand recognition. For many consumers, dental care is still not perceived as a medical necessity.

When an industry experiences sustained competition during its growth phase, the outcome is typically higher prices, as entrants flock to the high-end market to offer more profitable services. Historically, in efforts to improve healthcare accessibility and affordability, significant price reductions have almost invariably been driven by disruptive competition.

In summary, in terms of affordability and accessibility, while there have been some innovations in specific segments of the oral health sector, it has not yet reached the stage of disruptive innovation. Meanwhile, contradictions are more pronounced and direct within service providers such as hospitals and clinics.

Expanding into dental institutions remains a capital-intensive model that requires a certain growth period. Only through sustained strategic investments in talent, equipment, medical informatics, and management during the later stages can the quality and management standards of chain dental practices be ensured, enabling steady and robust development. The fundamental premise is that healthcare cannot be discussed in isolation from the scarcity of medical resources, regardless of whether it involves “+ digitalization,” “+ internet,” or big data. So, what constitutes an effective chain model in the dental services sector? What are the new strategic layouts and models adopted by leading enterprises? VCBeat (WeChat ID: vcbeat) has attempted to outline and interpret these questions.

During nationwide expansion, enterprises typically expand into new regions through a combination of acquisitions and organic growth, thereby complicating organizational relationships. The ability to successfully penetrate new markets depends on numerous factors, such as identifying geographic markets suitable for the types of services offered, understanding local consumer preferences, addressing competition in local markets, negotiating acceptable lease terms (including favorable rent levels), recruiting, training, and retaining medical staff, successfully integrating new facilities into existing control structures and operational systems (including information technology systems), and ensuring access to financing or maintaining sufficient capital required for investing in or acquiring new facilities.

Furthermore, managing growth and expansion to achieve and sustain profitability will continue to rely on management, physicians, administrative, operational, and financial personnel, as well as infrastructure. At times, it may not be possible to acquire ideal targets, or integrations may not be successfully executed. The choice of expansion model involves several key strategic positioning decisions.

Single-Brand and Multi-Brand Strategies

Both models have corresponding enterprises implementing strategic layouts. A single-brand strategy, as exemplified by Bybo Dental, leverages a direct-operation model to concentrate resources on building brand awareness for a single entity. This approach amplifies brand value and reduces promotional costs. Once brand recognition is established among consumers, subsequent marketing efforts benefit from first-mover advantages and cumulative effects, thereby fostering a loyal customer base.

Multi-brand strategies, as exemplified by Arrail Group and Happy Dentistry, enable differentiated positioning across various segments and regions. For instance, acquiring an existing clinic allows for the immediate retention of its established customer base, facilitating economies of scale, segmented and differentiated services, and reduced brand risk. Alternatively, companies can develop niche sub-brands; Happy Dentistry’s premium brand, Guya Orthodontics, capitalizes on the broader trend of digital dentistry by comprehensively promoting digital diagnostic technologies.

Meiwei aims to build a regional multi-brand chain, empowering its brands within specific regions to achieve personalized development and optimize their growth paths, thereby infusing the brand matrix with vitality and competitive advantage.

Currently, during clinic expansion, most enterprises opt for partnerships or joint ventures, as self-construction entails high costs and long lead times. In this context, managing multiple brands becomes inevitable. Moreover, some leading companies establish separate sub-brands targeting specific segments, such as cosmetic dentistry and pediatric dentistry, to better serve mid-to-high-end customers.

The crux of the issue lies in geographic expansion. Single-brand enterprises often fail to achieve effective synergies or maintain brand awareness in new regions, leaving them vulnerable to competition from established local brands. Conversely, a multi-brand strategy presents practical challenges, such as team integration and partner incentivization.

Generally, after acquiring a regional chain brand, companies typically refrain from forcibly changing the original brand name and strive to retain the existing organizational personnel. This approach facilitates greater emotional acceptance among founders, physicians, and patients, particularly for enterprise founders who have operated for many years, are approaching retirement, and lack suitable successors. However, in terms of marketing and resource integration, challenges inevitably arise during the adjustment period, especially regarding the balance between standardization and personalization. These issues require careful consideration and resolution as the company formulates its future strategy.

Expert IP and Chain Brand Models

The War for Talent: Intense Competition in the Dental Sector, Where Finding Suitable Dentists Is a Challenge Faced by All Dental Chains

If a physician with strong professional expertise and an established personal brand launches a startup and expands to two or three clinics, they can thrive by leveraging their accumulated reputation and resources. However, once the number of clinics exceeds five, especially when expanding across different regions beyond their geographic reach without effective resource integration, there is, to some extent, a diminishing return on their personal brand (IP).

When chain brands expand, whether to use physician IP as a promotional focus can be guided by a reference standard: the leading medical aesthetics chain brand, United LiGe, promotes its services through physician IP. It gathers renowned dermatologists across China, such as Zheng Quan, Zhou Zhanchao, and Zhao Xiaozhong, around specific technical fields like dermatology. By leveraging physician IP as a key attraction, it builds traffic and trust behind these branded labels.

Certainly, as healthcare providers, consumers vary in their cognitive perceptions when choosing medical services—whether they anchor on physician expertise, institutional brand reputation, or cost-effectiveness. By way of analogy, opting for unified chain clinic brands prioritizes service efficiency, whereas following individual physician IPs emphasizes service diversity. As information accessibility improves, it can awaken consumers’ innate demand for variety. Therefore, driven by the continuous enhancement of consumer cognition, the wave of diversity is poised to catch up with, and even surpass, the wave of efficiency.

Given that brick-and-mortar dental practices in China are still predominantly small, independent clinics and have not yet formed a landscape dominated by chain clinic brands, building physician IPs and teams may be a highly viable strategy.

National Chains and Regional Chains

The management and expansion risks arising from the unique artisanal nature of dental care have led dental hospitals to deeply cultivate regional markets, forming a business model that mitigates the risks associated with cross-regional expansion.

What model should be adopted for nationwide expansion? Options include greenfield development, acquisitions, and joint ventures. In fact, over the years of development in China’s private dental sector, various institutions have tried these approaches, either individually or in combination.

When acquiring a dental hospital or clinic, considerations should include the target institution’s location, its distance from major commercial districts, existing clinical departments, operational scale, the experience and track records of medical professionals and staff, the institution’s historical medical performance and professional reputation, as well as its compatibility with the acquirer’s corporate culture and existing dental practices.

Regulatory frameworks, market conditions, and audience perceptions vary across regions. Post-acquisition, the headquarters struggles to provide sufficient management capabilities, patient resources, and medical resources. Furthermore, to fund initial expansion and the ramp-up phase of newly acquired clinics, the headquarters has assumed a significant debt burden, resulting in elevated financial expenses.

Each model has its own advantages and limitations. Self-building is too slow and costly. Establishing a new dental institution generally involves many steps, including strategic planning, market research, site selection, feasibility studies, regulatory approval processes, facility construction and renovation, recruitment of necessary personnel, procurement of equipment and supplies, and commencement of operations. It typically takes 1–2 years to build a specialized dental hospital, while specialized dental outpatient departments or clinics require 6 months to 1 year. Moreover, newly established clinics need at least 6 months, and hospitals require a ramp-up period of at least 8 months.

However, the advantage of building from scratch lies in the ability to plan from the outset, ensuring strict quality control over staffing composition and service quality. Acquisitions and joint ventures are more efficient and faster but require addressing challenges such as team integration, incentive mechanisms, and differentiated positioning.

Currently, there are two mainstream approaches. One is the “1 (Flagship Store) + N (Regional Clinics)” model. However, this requires the flagship store to have exceptionally high brand recognition, service capabilities, and physicians’ technical expertise, so that regional clinics can be replicated in a relatively short period, share medical and brand resources, accumulate customer bases, and capture market share.

Another approach is to acquire a controlling stake in well-performing local chains, which requires robust capabilities in resource integration and capital strength, as well as the ability to formulate tailored development strategies and incentive policies based on their respective stages of growth.

There are still shortcomings in China’s dental education and public awareness of oral health care, while dental chain clinics face significant demand for customer acquisition. In the private healthcare market, the debate continues over whether to pursue short-term profits or to truly adopt a patient- and consumer-centric approach by returning to the essence of medical practice.

Traditional dental institutions typically prioritize high-value-added services such as dental implants, while paying insufficient attention to routine preventive care, teeth cleaning, and basic treatments. Whether this situation will change, whether the Kaiser model can be replicated in the dental sector to achieve cost control, and what factors might drive such changes remain uncertain. Encouragingly, however, several clear trends are still observable.

The Trends Toward Digitalization, Patient Comfort, and Precision Are Irreversible

The digitalization of the dental industry, in a general sense, refers to the adoption of CAD/CAM technology, intraoral scanners, and CBCT (Cone Beam Computed Tomography) to provide patients with more comprehensive treatment plans and an optimized clinical workflow, ultimately delivering better therapeutic outcomes, particularly in the fields of orthodontics and dental implantology.

However, the drive toward digitalization has not progressed as rapidly as envisioned, due to a variety of factors:

First, the habitual iteration among dentists will take some time, as it is related to overall educational approaches and clinic positioning;

Second, the acquisition of intraoral scanners, CBCT units, and 3D printers has increased clinic costs. While only large hospitals have sufficient capital to purchase high-end CBCT systems, it is inconceivable to perform subsequent orthodontic procedures without such equipment as intraoral scanners.

Third, policy requirements mandate that imported advanced medical devices obtain registration certificates and undergo a time-consuming approval process. For instance, Invisalign’s iTero intraoral scanner officially entered the Chinese market in April this year, while 3Shape currently offers only its second-generation products in China.

Of course, in the broader trend of domestic substitution for medical devices, several outstanding Chinese manufacturers have emerged, such as Meyer Optoelectronic (CBCT), Phison Technology (intraoral scanners, CBCT), and Langcheng (intraoral scanners), which have captured a certain market share through competitive pricing, service, and technology. Phison Technology already offers the Linying all-in-one CBCT system and the Linzhi intraoral scanner. Additionally, digital surgical guide companies such as Color Cube and GuideMia have also emerged.

Moreover, in addition to digitalization, comfort-oriented care, precision dentistry, and minimally invasive techniques are also trends shaping the future of the oral healthcare industry, necessitating continuous iteration of high-quality products and technologies.

Train More General Dentists

With a population of nearly 1.4 billion and only 200,000 registered dentists, coupled with the lengthy training period required for dentists, one can imagine the magnitude of the talent shortage. Dentistry is not an industry that allows for quick mastery; it demands long-term accumulation of expertise. The rapid training and replication of dentists is highly challenging, and much of the training is currently conducted by equipment manufacturers. From an industry-wide perspective, 15% of dentists should be specialists, while the remaining 85% should serve as general practitioners (GP dentists).

Most clinics in China must excel in general dentistry, which includes periodontics, root canal therapy, fillings, and crowns. General dentistry is the foundational competency of any dental clinic; issues are typically identified through general dental treatments, after which implantology or orthodontics are provided based on patient needs. Complex orthodontic cases and implant surgeries must be performed by senior specialists, while basic care and restorative procedures can be handled by general dentists.

Take dental implantology as an example. It requires clinicians to possess specialized knowledge, including bone quality, anatomy, implant characteristics, connection mechanisms, and the operation of implant systems. This field involves oral surgery, regional anatomy, physiology, and bone conditions, while also necessitating an understanding of complication prevention and risk management for implants over a 5- to 10-year period.

Certain digital technologies have indeed facilitated the professional development of dentists in training, education, and surgical procedures. By enabling simpler and more standardized treatment protocols, these technologies have, to some extent, reduced procedural complexity and enhanced efficiency. However, a comprehensive preventive care system within the oral health industry has yet to be fully established, and there remains considerable room for improvement in training mechanisms. Hospitals and clinics continue to prioritize high-ticket items such as dental implants and orthodontics. Consequently, digitalization currently tends to address the needs of a small segment of high-end patients, and widespread adoption of these technologies will require time.

Refined Operations Must Be Prioritized

Dental institutions face fierce market competition in terms of both patient and physician resources. The previous extensive growth model—such as aggressively opening new clinics within a short period and acquiring customers through price wars—has been proven unsustainable. Only high-quality medical service providers adhering to standardized operations can earn long-term consumer trust.

Dental chain clinics have, to varying degrees, accumulated brand recognition as well as medical and management teams during their development. The focus for the next stage is undoubtedly to explore innovations in management systems and operational mechanisms, while pursuing refined operations.

Particularly for some large chain institutions, years of offline advertising bombardment have generated a certain degree of brand exposure, enabling them to centrally capitalize on the abundant online traffic, such as young users on social media and e-commerce platforms. Refined operations encompass numerous elements, including information management systems, clinical care systems, training systems, procurement systems, customer service systems, and human resources systems, with the aim of enhancing control, service quality, and efficiency.

In terms of information management systems, clinics are increasingly demanding robust data capabilities and intelligent reporting. Operators seek to understand the efficiency of each stage—from patient acquisition to final word-of-mouth conversion—to make targeted decisions. They are also placing greater emphasis on patient communication and the clinical experience to deliver more personalized services. For instance, Lingjian’s e-Kanya software supports chain and group practice management within its system and offers a Social Customer Relationship Management (SCRM) platform deeply integrated with social media networks, helping healthcare institutions achieve intelligent marketing.

Clinic management software is a highly promising niche segment that enables integrated supply chain procurement; however, it faces the challenge that large-scale small clinics lack sufficient motivation for digital transformation.

In terms of the clinical and customer service system, clinics must provide patients with clear diagnoses and treatment plans to minimize patient attrition during initial consultations. Additionally, they should offer comfortable treatment options throughout the care process, implement effective patient management, and prioritize building a positive reputation on social media platforms such as Dianping.

Of course, the specific operational guidelines for refined management are too extensive and complex, requiring continuous exploration in practice.

The Preventive Healthcare System Has Significant Market Potential

There are several thought-provoking questions regarding the low-frequency nature of healthcare: First, given the many specialized segments within healthcare, is demand uniformly low-frequency across all of them, or are there high-frequency segments? Second, can this low-frequency attribute be transformed into a high-frequency one? Third, can multiple low-frequency services be aggregated to present as high-frequency engagement within a single platform? Fourth, since low frequency is difficult to alter, can it be leveraged directly instead?

The above logic can be distilled into four key points: in healthcare-related behaviors, identifying high-frequency activities, creating high-frequency engagement, aggregating low-frequency activities into high-frequency patterns, and leveraging low-frequency activities to generate commercial value are critical to building a successful business model.

Consumers generally do not visit the dentist frequently, resulting in low-frequency demand. Therefore, driving engagement through the concepts of health management and prevention may be an effective way to stimulate higher-frequency demand. Comparing this with European and American markets, taking the most severe dental condition as an example—missing teeth requiring implants—the cost is typically around $2,000–$2,800, with premium options such as Nobel Active reaching up to $5,000. If consumers prioritize routine oral care, including professional cleaning, examinations, and basic treatments, the overall cost of treating dental diseases can be reduced. For instance, in many overseas dental chains, revenue from professional cleaning accounts for over 40%, while dental implants contribute only 5%. In contrast, the situation in China is reversed: in some mid-to-high-end clinics, implants and orthodontics account for more than 40% of revenue, prosthodontics another 40%, with general dentistry making up the remaining 20%.

As patients’ awareness of oral hygiene increases, the focus is shifting from “cure” to “prevention.” Coupled with the impetus provided by insurance coverage and mobile tools for oral health management—covering all stages from prevention and basic treatment to complex procedures—the market may undergo transformation by enhancing the capabilities of medical networks in terms of coverage, cost control, and service delivery.

Promising Subspecialties

Across the dental industry, leading brands in adult dentistry have already emerged, creating a highly competitive "red ocean" market nationwide. Currently, the focus is primarily on two niche segments: pediatric dentistry and orthodontics. Topchoice Medical completed its foundational layout in these two areas many years ago, with brands such as Sanye Children's Dentistry, Hibeauty Yinxiu, and Ortholink Youling.

In the field of pediatric dentistry, a decisive key factor is consumer health awareness. Enhancing consumers’ information literacy produces two opposing effects: on one hand, improved information literacy drives sales growth; on the other, effective competition leads to declining profit margins, with both phenomena coexisting. When consumer awareness surpasses a specific threshold, overall profit margins decline, becoming the primary driver of market evolution. The pediatric oral care market has still not reached this critical tipping point.

Children and adults have different service needs, with parental education being the most critical aspect. This sector remains a blue ocean market. Representative companies include Sanye Children's Dentistry under Topchoice Medical, Qingmiao Children's Dentistry, Jicheng Children's Dentistry, Xidun Children's Dentistry, Jiuwen Dental, DuangDuang Pediatric Dentistry, Duole Children's Dentistry, and Chunya Baby.

Due to parents' insufficient attention to children's oral health, many believe that pediatric dental treatment should be less expensive than adult care. The reality is quite the opposite. Treating children's oral conditions requires substantial time for behavior guidance and communication with parents. Moreover, pediatric dental procedures carry higher medical risks, demand longer chair time from dentists, and incur higher clinic operational costs. Additionally, anesthesia is often unavoidable in pediatric dental treatments, meaning that risks are always present.

At this juncture, there is a need for high-quality treatment models, medical devices, and consumables. For instance, Romu Occlusal Guidance, which entered the Chinese market in 2011, prioritizes the safety of its core products and therapeutic services. In the future, it will further serve healthcare institutions and physicians through its training system and centralized service platform.

Since its inception, Qingmiao Children's Dental has consistently promoted the philosophy of "prevention first, treatment second." To maintain strict quality control, it has not opened any franchising channels and operates exclusively through company-owned clinics. By introducing child behavior guidance and a "gamified" dental care strategy, Jicheng Children's Dentistry planned to establish multiple clinics in 2018, with Shanghai and Tianjin as its core markets.

Taking DuangDuang Pediatric Dentistry as an example, it is specially tailored for children aged 0–18. It advocates an American-style medical service philosophy that emphasizes both “prevention and treatment” and gives equal importance to “physiological and psychological” well-being. Its engaging environment and experience, along with psychological counseling, help eliminate children’s fear. The flagship offering of pediatric oral health management represents a currently popular model.

The development of cosmetic dentistry and orthodontics is driven by several factors. Consumer demand for aesthetics, particularly among residents in first- and second-tier cities, provides a solid customer base. From a technological perspective, digitalization and clear aligner technologies demonstrate superior performance in terms of efficiency, efficacy, and aesthetics. Due to the generally high average transaction value, clinics are also inclined to offer cosmetic dental services, gaining advantages in products, technology, pricing, and target demographics. However, it must be acknowledged that domestic aesthetic restorations are constrained by the skill level of local dental technicians, resulting in a significant gap in aesthetic quality compared to foreign products.

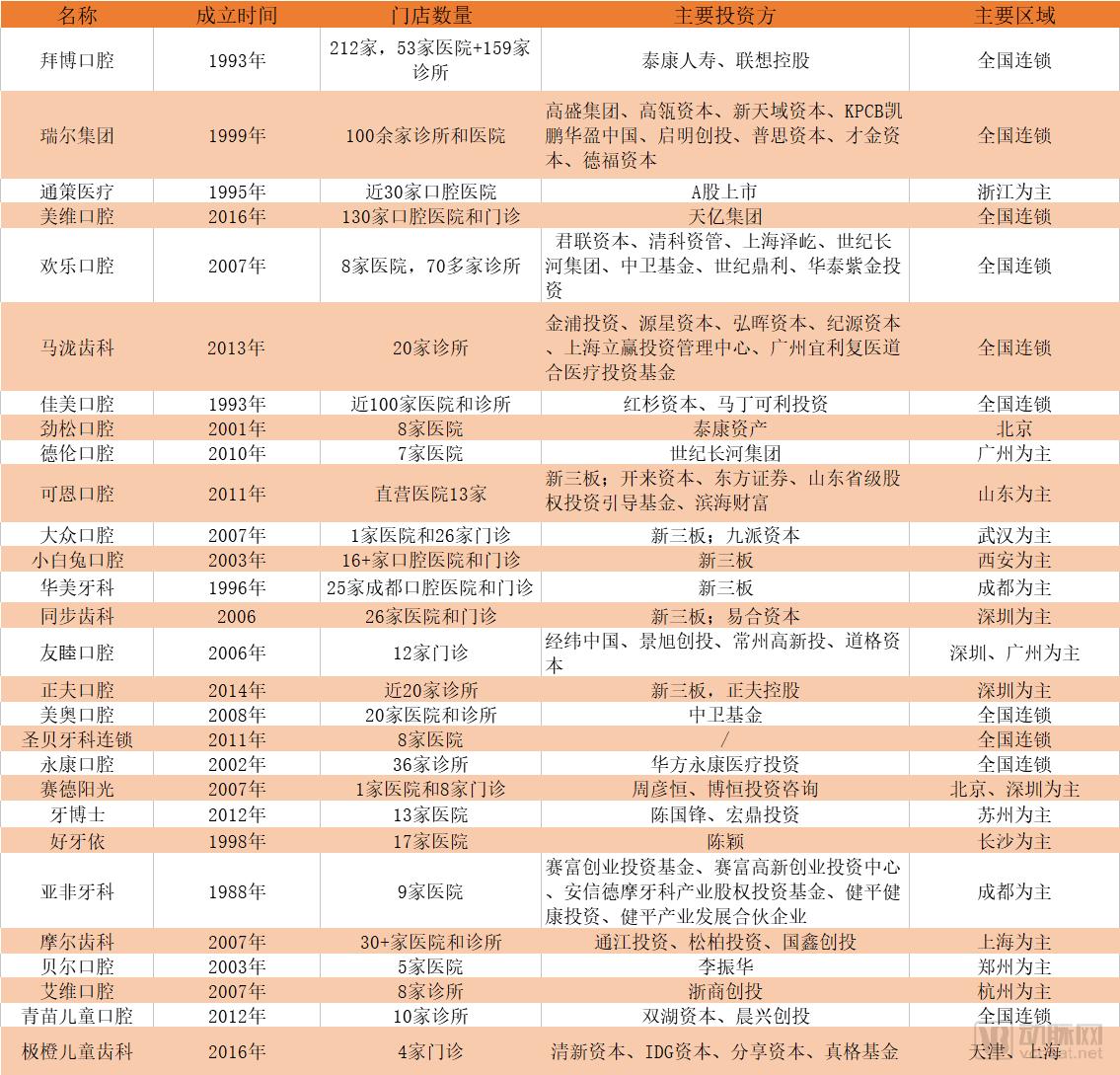

Some Typical Dental Chain Brands in China: Data compiled from publicly available sources, with every effort made to ensure completeness and accuracy.

Bybo Dental: Taikang Holdings Explores the Integration of Dental Healthcare Services and Payment

On May 18, 2018, with the approval of the China Banking and Insurance Regulatory Commission (CBIRC), Taikang Insurance Group officially announced its strategic investment in Bybo Dental Medical Group. Taikang Life Insurance invested RMB 2.06236 billion to acquire a 51.56% equity stake in Bybo Medical. On June 15, the press conference for Taikang’s strategic investment in Bybo Dental was held at Taikang Business School, formally announcing the successful completion of this strategic investment.

As of the end of 2017, Bybo Dental had 212 outlets, including 53 hospitals and 159 clinics, representing a 6% increase from the 200 outlets recorded at the end of 2016, with coverage across 25 provinces and municipalities directly under the central government.

Following Taikang’s equity investment, the next core theme of development will be how to further enhance endogenous growth capabilities. A return to the essence of healthcare—prioritizing dental prevention over treatment—represents a potential shift under Taikang’s holding structure. Taikang will provide Bybo Dental with multifaceted support in capital, customer access, branding, and products, while integrating resources such as IT systems, supply chains, and property assets. The aim is to align service providers with payers, thereby achieving integration between medical services and insurance payment mechanisms.

Arrail Group: Positioning in the Mid-to-High-End Dental Care Market, Strategizing the Thousand-Clinic Plan

In August 2017, Arrail Group announced the completion of a $90 million Series D financing round, jointly invested by Goldman Sachs Group and Hillhouse Capital. Arrail Group currently operates more than 100 clinics and hospitals across 16 major cities in China. Its two dental chain brands are Arrail Dental and Ruitai Dental Hospital; the former targets high-end clientele, while the latter primarily serves the middle class and a broad base of white-collar professionals.

Following the completion of the financing, Arrail Group will further establish and refine its development strategy, and announce the launch of the “Thousand-Clinic Initiative.” The company aims to open more than 1,000 dental clinics and hospitals across China within five to eight years, committed to promoting the widespread availability of professional, high-quality mid-to-high-end oral healthcare services.

Tongce Group: Regional General Hospital + Branch Model, Launching the Dandelion Plan

Topchoice Medical has pioneered the “Regional General Hospital + Branch Hospitals” development model, an upgrade to its previous “Central Flagship Hospital + Branch Hospitals” operational framework. Under this model, the Regional General Hospital platform supports physicians’ clinical skills and academic standing while building brand influence within the region. Meanwhile, the branch hospitals optimize healthcare resource allocation and enhance patient access, thereby accumulating a robust customer base and capturing market share.

Currently, the Hangzhou Stomatologist Group has been established, with three central hospitals located at Pinghai Road, Chengxi, and Ningbo. In 2017, the newly operational hospitals under the company included: Hangzhou Stomatological Hospital Chengbei Branch, Hangzhou Stomatological Hospital Xiaoshan Branch, and Yiyang Stomatological Hospital; the hospitals under new construction were: Wenzhou Cunji Stomatological Hospital, Suzhou Cunji Chengxi Stomatological Hospital, and Hangzhou Chendong Stomatological Outpatient Department.

Currently, Topchoice Medical has established a comprehensive layout in adult dentistry, pediatric dentistry, digital orthodontics, and hospital information-based internet platforms. In terms of medical services, the company actively implements the CM (Case Manager) team management model, which consists of attending physicians, resident physicians, medical assistants, nurses, and customer service personnel, to provide classified management and precise services for patients.

Over the past decade, Topchoice Medical has primarily focused its operations within Zhejiang Province, adopting a cautious and small-scale approach to expansion outside the province. This year, it launched the “Dandelion Plan,” aiming to establish 100 branch clinics across Zhejiang Province within three years.

Meiwei Dental Care: Business Partner Model, Empowering Regional Leading Brands

Meiwei Dental Healthcare, a subsidiary of Tianyi Group, leverages its “Business Partner” model to collaborate with leading regional dental brands. By focusing on three key dimensions—strategic investment, standardization, and brand management—Meiwei empowers outstanding Chinese dental healthcare brands to achieve personalized growth. Currently, Meiwei operates 12 branded chains with 130 clinics nationwide, and three of its regional markets have achieved annual revenues exceeding RMB 100 million.

Meiwei is a company driven by the synergistic forces of industry, capital, and management, with dental healthcare at its core. By introducing a “business partner” mechanism, it builds a stable, win-win community of shared destiny, providing comprehensive empowerment across multiple dimensions, including capital, talent, technology, market, and management.

By implementing rigorous management certification, we transform our affiliated dental brands into leading dental healthcare institutions that integrate academic excellence, precision care, digitalization, patient comfort, and informatization. This approach enhances their comprehensive operational management and profitability, empowers them to scale up and strengthen their market position, supports the development of outstanding Chinese dental chain brands, and facilitates personalized growth. The core strategy is to enable partner dental institutions to become the top-tier brands in their respective regions.

Since its inception in 2016, Meiwu has integrated and established new brands, including Jiangxi Zhongshan Dental, Tianjin Aichi Dental, Kunming Hanmei Dental, and Wuhan Tsinghua Sunshine Dental, all of which have achieved year-on-year revenue growth of nearly 1–2 times.

Happy Dentistry: Legend Capital Leads Series B Funding, Focusing on Five Strategic Areas

In June 2018, Happy Oral Care secured RMB 450 million in Series B financing, led by Legend Capital. Over the past 11 years, leveraging the technical expertise of its founding team of dentists from Peking University School of Stomatology, Happy Oral Care has adhered to a prevention-first philosophy and developed the “Three Diseases, Two Technologies” framework, establishing a comprehensive system for preventive and therapeutic dental care characterized by rapid diagnosis, minimal discomfort, and superior clinical outcomes. The company currently operates 8 hospitals and more than 70 clinics.

Additionally, Guri Orthodontics, the premium brand under Happy Dentistry, has fully rolled out digital diagnostic technology. Over the past 18 years, Guri Dental has established multiple dental clinics in Beijing’s core business districts.

In the future, Happy Dentistry will focus its efforts on the following five areas: first, comprehensively promoting digital diagnostic technologies; second, striving to deliver patient-centered medical services that inspire trust and satisfaction; third, placing high priority on the research and development of standardized models; fourth, establishing specialized dental departments with distinctive competitive advantages; and fifth, gradually building a strong positive reputation online.

Ma Long Dental: Empowered by Key Opinion Leader (KOL) Dentists, Strategizing Across the Entire Industry Chain

In 2012, Malo Clinic officially entered China, initiating its layout across the entire industry chain. In March 2017, Malo Clinic completed a Series C financing round of RMB 110 million, led by Jinpu Fund, with co-investment from Source Code Capital and Honghui Capital.

Currently, 20 dental clinics have been established across multiple cities in China, with preparations underway in Nanjing and Xi’an. The company also operates a denture processing center, an education and training center, a procurement center, and a clinical teaching base for aesthetic dentistry. Leveraging physician IP branding, Malo Clinic is backed by prominent figures such as Dr. Malo and Dr. Cui Yutao. It has made significant inroads into adult dental implantology, aesthetic restoration, and pediatric dentistry, while simultaneously establishing two core systems: “productization of medical services” and “financial operations management.”

Related Reading: