Chinese Innovative Biopharma Firms Including MicuRx, Innovent, and Gensci Rush to IPO as Sector Attracts $4.7 Billion in Investment Since 2014

Recently, innovative pharmaceutical companies such as MicuRx Pharmaceuticals, Innovent Biologics, and Ascletis Pharma have successively filed IPO applications with the Hong Kong Stock Exchange. WuXi AppTec, which recently listed on the A-share market, plans to issue H-shares, signaling a wave of capitalization among domestic innovative drug developers. If the listing processes proceed smoothly, the investors behind these innovative pharmaceutical companies will soon enter a period of returns.

A Wave of IPOs by Innovative Drug Companies May Signal the Dawn of a “Golden Age” for Domestic Drug Innovation. Driven by favorable policies, capital infusion, and the opening of channels for value realization, the number of startups and the volume of investment and financing in China’s new drug sector have risen year after year, making innovative drugs one of the most prominent segments in the Chinese pharmaceutical industry.

VCBeat (WeChat ID: vcbeat) has compiled information on policy changes, financing and investment events, and new drug applications in China’s innovative drug sector since 2014. It provides an in-depth analysis of the policy environment under regulatory frameworks such as the priority review and approval reform, the Marketing Authorization Holder (MAH) system, and policies encouraging innovation in drugs and medical devices. The report also examines key product pipelines and therapeutic area distributions of innovative pharmaceutical companies, as well as capital market focus areas and investment rationales, offering a preliminary overview of the development of innovative drugs in China.

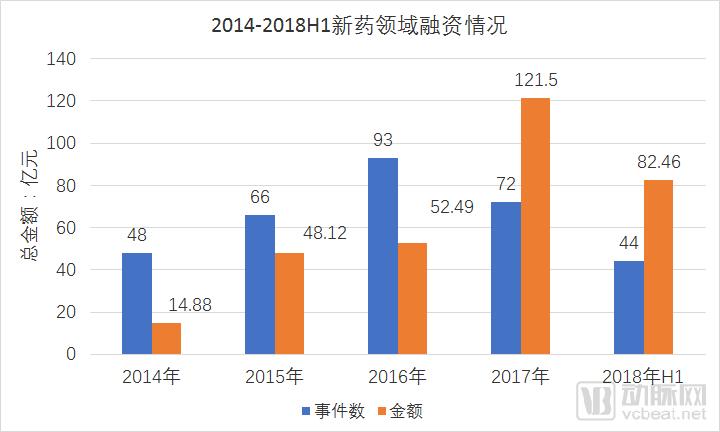

According to data compiled from the VCBeat database and public sources, there have been 323 financing deals in China’s new drug sector since 2014, involving a total amount of approximately RMB 32 billion, with an average single deal size nearing RMB 100 million.

Data sources: VCBeat database, public information; companies in the new drug sector include those involved in innovative chemical drugs, biologics, CROs, CMOs, and CDMOs.

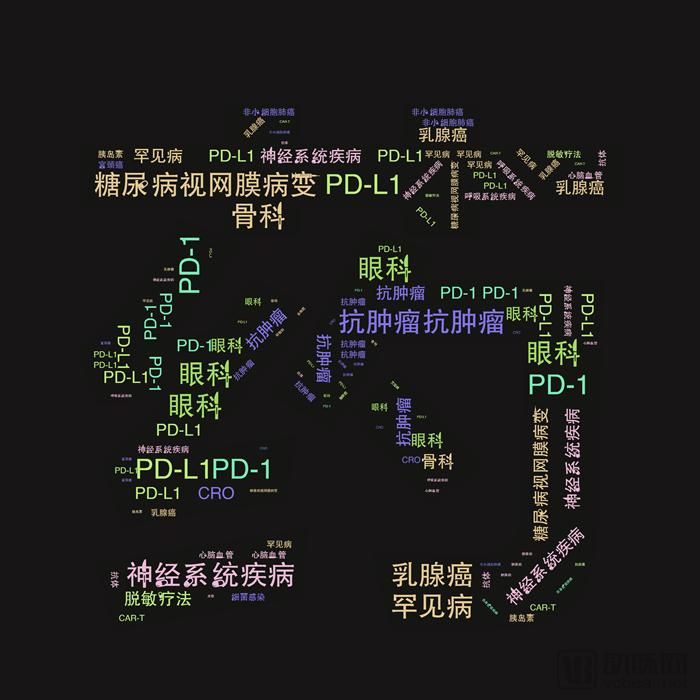

From the perspective of the therapeutic areas primarily covered by the R&D pipelines and product filings of financed companies, oncology, respiratory diseases, diabetes, and cardiovascular and cerebrovascular disorders represent the main therapeutic domains. This is driven by unmet clinical needs, broad patient populations or indications, and prolonged treatment durations in these areas, which have the potential to yield “blockbuster” drugs. Additionally, some companies are also active in ophthalmology, orthopedics, and certain rare disease fields. Overall, innovative pharmaceutical companies have a relatively comprehensive and evenly distributed presence across therapeutic areas.

Keywords for Innovative Drug Product Lines

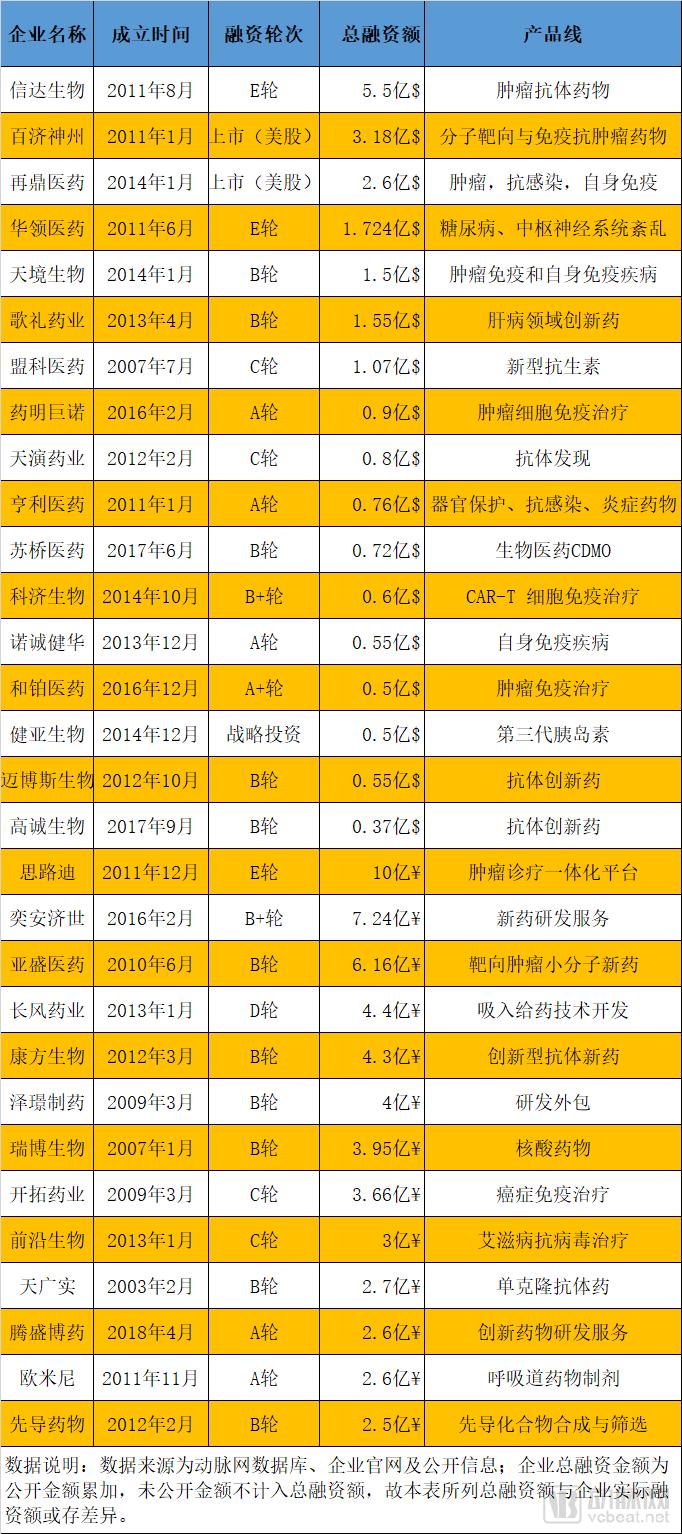

By reviewing financing events from 2014 to the first half of 2018, we identified the 30 innovative drug companies with the strongest fundraising capabilities since 2014, including Innovent Biologics, BeiGene, Zai Lab, Hua Medicine, 3D Medicines, E-Healthcare, and Ascentage Pharma.

Top 30 Innovative Pharmaceutical Companies by Fundraising Capacity

The top 30 companies raised a total of approximately RMB 21 billion, accounting for about 65% of the total financing. This indicates that leading enterprises in the innovative drug sector have secured the majority of funding, indirectly confirming the core logic of new drug investment: backing top-tier teams with large-scale, long-term, and sustained capital commitment.

From the perspective of financing rounds, the vast majority of the top 30 companies have entered Series B and later stages. BeiGene and Zai Lab are already listed, while MicuRx Pharmaceuticals, Innovent Biologics, and Ascletis Pharma have successively announced plans to list in Hong Kong. Given the favorable reception of pre-profit biopharmaceutical companies by the capital markets in the United States and Hong Kong, more biopharmaceutical companies may choose to list in these two locations in the future.

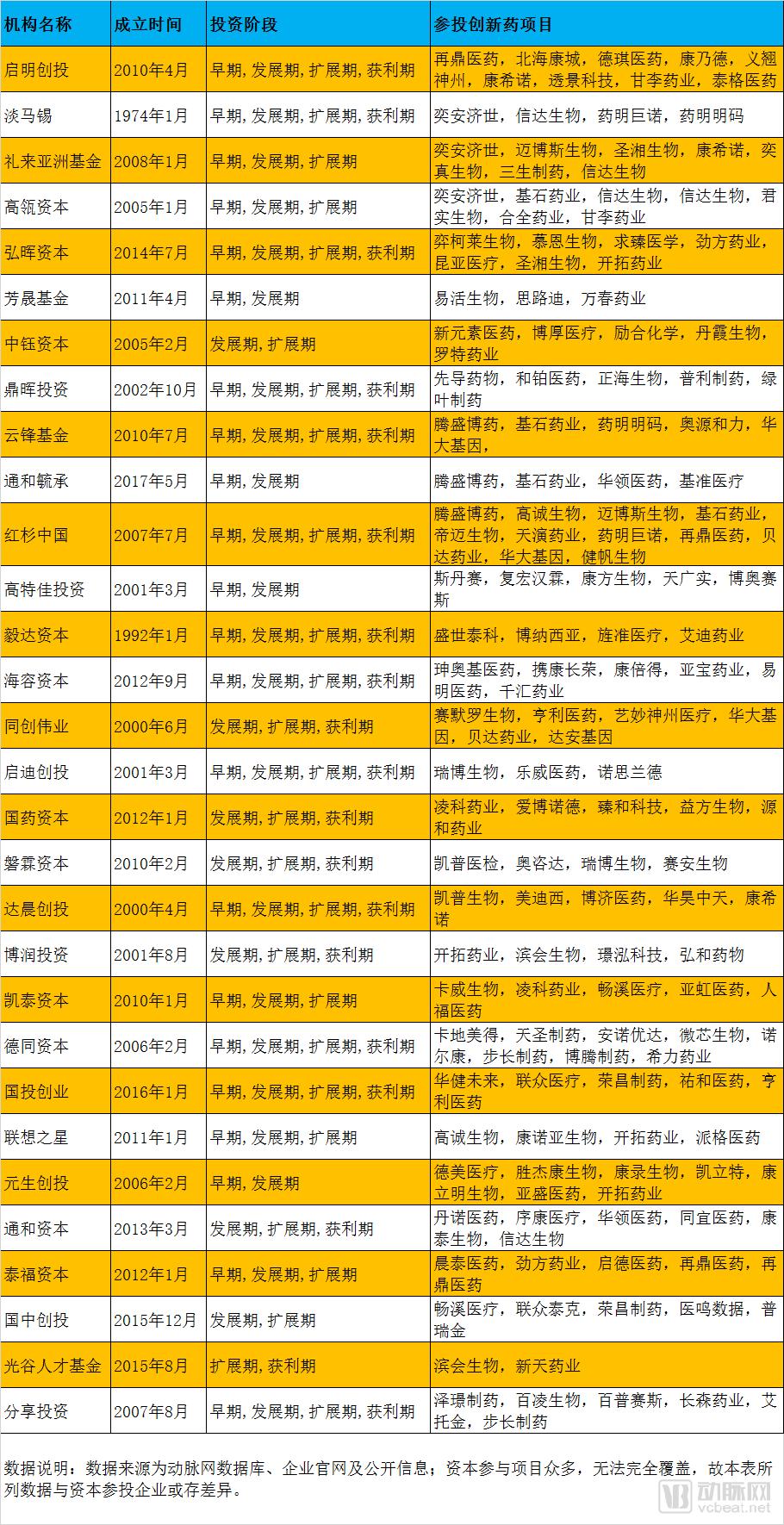

Behind the relatively concentrated financing, major investment institutions in the innovative drug sector also exhibit a trend toward consolidation. Capital firms such as Lilly Asia Ventures, Sequoia China, Hillhouse Capital, Qiming Venture Partners, Temasek, and GTJA have invested in multiple innovative pharmaceutical companies, with significant overlap in their selected targets and evident synergies.

Top 30 Innovative Drug Investment Institutions

An analysis of the establishment dates reveals a strong correlation between the founding of star venture capital firms in the new drug sector and the emergence of innovative pharmaceutical companies, with 2013–2014 serving as a critical timeframe. Based on their backgrounds, these investors can be broadly categorized into two groups: established institutional investors, represented by Sequoia Capital and Temasek, and industrial capital with pharmaceutical expertise, exemplified by Tonghe Capital and GTJA Capital.

Investing in new drugs demands a high level of professionalism, requiring investors to possess deep industry insights and specialized expertise. Established investment firms benefit from accumulated experience, robust management structures, and advice from external consulting experts, enabling them to quickly capitalize on emerging trends in novel therapeutics. In contrast, corporate venture capital invests based on confidence in the target company’s team and product pipeline, bringing not only capital but also additional resources that support the growth of innovative pharmaceutical enterprises.

Furthermore, it is crucial to note that new drug investment involves a time horizon and capital requirement often summarized as “10 years and $1 billion.” This implies that institutional investors in the new drug sector possess substantial financial strength and maintain sustained confidence in their portfolio companies. Consequently, whether established investment firms or industrial capital, once they anchor a project, they will continue to follow up, practicing “value investing.”

China is a major pharmaceutical country, but not a strong one. This is manifested in the weak innovation capabilities of domestic pharmaceutical companies, insufficient R&D investment, and low levels of internationalization; there are still unreasonable aspects in the drug review and approval system, with new drugs lagging behind Europe and the United States in market launch; medical insurance payment provides insufficient support for innovative drugs, and individual payment capacity is relatively weak.

To facilitate the transition from a major pharmaceutical country to a leading pharmaceutical power, a series of policies have been introduced in recent years to encourage pharmaceutical innovation. Key measures include deepening the reform of the drug review and approval system, implementing consistency evaluations for generic drugs, establishing the Marketing Authorization Holder (MAH) system, reforming the medical insurance payment system, and encouraging the development of Contract Research Organizations (CROs).

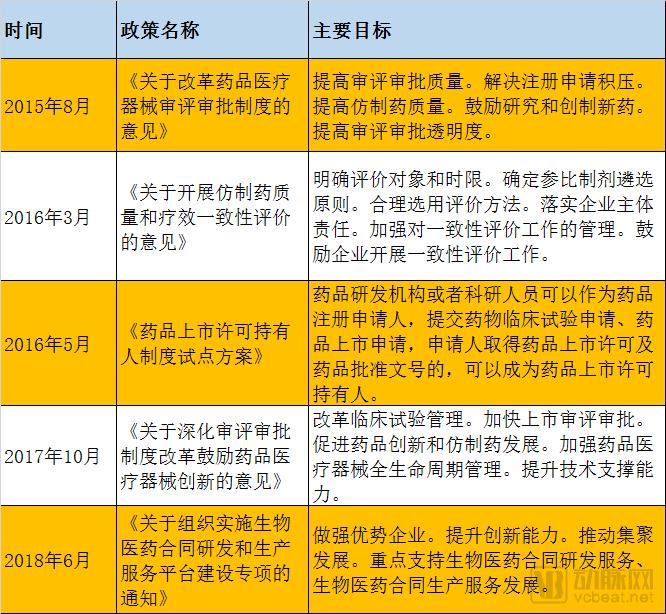

Major Pharmaceutical Innovation Policies in Recent Years

Since the General Office of the State Council issued the “Opinions on Reforming the Review and Approval System for Drugs and Medical Devices” in August 2015, pharmaceutical innovation has received unprecedented attention.The primary objective of new drug approval has also shifted from “addressing the backlog” to “encouraging innovation.”

From a specific pathway perspective, this round of new drug policies has roughly five directions that directly benefit the development of innovative drugs.Priority Review and Approval, the priority review and approval system has been in place for over two years. As of the end of May 2018, there had been 28 batches of public notices on drug registration applications proposed for inclusion in the priority review program, covering a total of 480 acceptance numbers and 300 generic names (counted by different companies).

On June 15, the first PD-1 inhibitor approved for marketing in China entered the market. Benefiting from the green channel for priority review, the approval process for this urgently needed PD-1 drug proceeded smoothly, taking less than nine months from submission to approval. Although this product was not developed by a domestic company, it nonetheless demonstrated the time-window effect of the reforms in the new drug review and approval system.

Benefiting from drug review reforms, innovative drugs from multiple domestic pharmaceutical companies—including Hengrui Medicine, Chia Tai Tianqing, Qilu Pharmaceutical, CSPC Pharmaceutical, Huahai Pharmaceutical, and Tasly—have been included in the priority review program. Overall, these reforms have shortened the time to market for new drugs, which is largely favorable for biopharmaceutical companies involved in innovative drugs, generic drug manufacturers, and foreign pharmaceutical enterprises.

The second is the MAH system.The MAH system decouples drug marketing authorization from manufacturing licensing, stimulating enthusiasm for R&D among universities, research institutions, and small enterprises, thereby strengthening China’s capacity for innovative drug development.

Third, the accreditation of clinical trial institutions is subject to a filing system.Institutions meeting the requirements for conducting clinical trials may, upon registration and filing on the website designated by the drug and food regulatory authorities, accept commissions from drug and medical device registration applicants to conduct clinical trials. Investment by non-governmental entities in establishing clinical trial institutions is encouraged. This undoubtedly addresses the shortage of clinical trial institutions and alleviates the pressure stemming from the scarcity of resources at existing clinical trial institutions.

Other policies and measures, such as the acceptance of international multi-center clinical trial data, the drug patent linkage system, and incentives for the development of CROs and CMOs, have provided supportive infrastructure for innovative drug development. These initiatives have strengthened the regulatory and market systems for innovative drugs, fostering a comprehensive ecosystem for innovation in pharmaceuticals.

Reforms to the medical insurance payment system have also significantly impacted the development of innovative drugs. The core of this round of reforms is “cost containment,” requiring that “expenditures be determined by revenues, achieving a balance between income and outgo with a modest surplus.” Under pressure on the medical insurance fund, reform pathways include restrictions on antibiotic and adjuvant drug use, price negotiations, and other measures.Medical insurance reimbursement should prioritize drugs with proven clinical value, with innovative medicines being a key focus.

In July last year, the Ministry of Human Resources and Social Security included 36 drug varieties in the "National Reimbursement Drug List," among which were multiple innovative drugs. The Ministry stated that high priority was given to innovative drugs and treatments for rare diseases during the negotiations. All drugs listed under the National Major New Drug Creation Special Project since the "12th Five-Year Plan," such as chidamide, conbercept, and apatinib, were successfully included through negotiation. Recombinant human coagulation factor VIIa for treating hemophilia and recombinant human interferon beta-1b for treating multiple sclerosis were also successfully added to the drug list. Innovative pharmaceutical companies that directly benefited include Shenzhen Chipscreen Biosciences, Kanghong Pharmaceutical, and Hengrui Medicine.

From the perspective of market demand, healthcare insurance payment reforms have strengthened support for innovative drugs, directly benefiting the expansion of the innovative drug market. Additionally, although the basic medical insurance fund is under financial pressure, its revenue growth has been accelerating overall, ensuring sustained payment capacity. Furthermore, the development of commercial health insurance and the Direct-to-Patient (DTP) model has further enhanced both the demand for and channel capabilities of innovative drugs, thereby unleashing their market potential.

Domestic innovative drug concept stocks include Hengrui Medicine, Fosun Pharma, CSPC Pharmaceutical Group, Betta Pharmaceuticals, Kelun Pharmaceutical, and Tasly. These companies entered the innovative drug and innovative generic drug sectors early, with some products now reaching the harvest phase. They have received positive feedback in both the pharmaceutical and capital markets, potentially serving as role models for other enterprises venturing into innovative drugs.

CSPC Pharmaceutical Group

CSPC Pharmaceutical Group, formerly known as “China Pharmaceutical,” initially focused on antibiotics and active pharmaceutical ingredients (APIs). Due to intensifying competition in the API market, the company expanded into the finished dosage form market and dedicated years to research, development, and investment in innovative drugs. Three major innovative drug products under CSPC—Oxiracetam (Aolaining), Butylphthalide (NBP), and Levamlodipine (Xuanning)—were successively launched, generating substantial market revenue for the company.

According to the annual report of CSPC Pharmaceutical Group, the sales revenues of its three major innovative drugs—Oxiracetam (Oulaining), Butylphthalide (NBP), and Levamlodipine (Xuanning)—in 2016 were RMB 3.683 billion, RMB 2.926 billion, and RMB 1.122 billion, respectively. Other products, including Doxorubicin (Duomeisu), Pegylated Recombinant Human Granulocyte Colony-Stimulating Factor (Jinyouli), and Elemene (Ailineng), also achieved annual sales exceeding RMB 100 million.

CSPC Pharmaceutical Group’s Q1 2018 financial report showed that its revenue increased by 55.2% year-on-year to HK$5.39 billion, and its net profit rose by 42.6% year-on-year to HK$910 million. One of the main drivers for the growth in revenue and net profit was the continued ramp-up of innovative drug products. In particular, sales of NBP (Butylphthalide) and Jinyouli (Pegfilgrastim) grew rapidly after being included in the National Reimbursement Drug List last year. Furthermore, monthly sales of Paclitaxel Albumin-Bound Nanoparticles, launched in March 2018, exceeded HK$15 million within just one month, demonstrating strong market performance.

Meanwhile, CSPC Pharmaceutical Group has nearly 200 drug candidates in its pipeline, including several Class 1 innovative drugs such as Pinocebrin for Injection for Alzheimer’s disease and SKLB-1028 Capsules for acute myeloid leukemia and non-small cell lung cancer. Some of these candidates have completed clinical trials and are awaiting regulatory approval for market launch. As more innovative drugs gain approval and enter the market, CSPC Pharmaceutical Group is poised to achieve greater returns in both the pharmaceutical and capital markets.

Beta Pharma

Beida Pharmaceutical is a pharmaceutical enterprise founded by a team of overseas-educated PhDs, dedicated to research and development and innovation. Its flagship product, Icotinib Hydrochloride (Conmana), was praised by Chen Zhu, the then Minister of Health, as being comparable to the emergence of the “Two Bombs, One Satellite” in the field of public welfare.

Conmana was approved for market launch in 2011. In 2016, its sales revenue exceeded RMB 1 billion, with sales volume surpassing 550,000 boxes. In November 2016, Beta Pharma went public on the ChiNext board, with Conmana contributing over 98% of sales revenue and more than 96% of gross profit. It can be said that Conmana, as a single drug, propelled Beta Pharma’s initial public offering.

Annual report data show that in 2015, icotinib participated in the first round of national drug price negotiations. In May 2016, the results of the national drug price negotiations were announced, with icotinib, as the only domestically produced innovative drug shortlisted, experiencing a 54% price reduction (to RMB 1,399 per box after the reduction). In the fourth quarter of 2016, various regions began to sequentially list icotinib for online procurement at the negotiated price. In February 2017, icotinib, as a domestically produced innovative anticancer drug, was included in the new version of the National Reimbursement Drug List published by the Ministry of Human Resources and Social Security.

In 2017, the sales volume of Icotinib increased by 42.87%, basically offsetting the impact of price reductions and achieving a "price-for-volume" strategy, with annual sales reaching RMB 1.026 billion. The annual report also revealed that since its launch, Icotinib has achieved cumulative sales revenue of RMB 4.518 billion, with a total of 155,000 patients having taken Icotinib. In the first quarter of 2018, Icotinib's sales revenue grew by more than 20% year-on-year. As provincial medical insurance coverage expands, Icotinib is expected to continue seeing significant growth in sales volume.

After establishing a solid foothold with a major innovative drug, Beta Pharma has maintained its momentum. Over the past three years, its R&D investment in new drugs reached RMB 120 million, RMB 161 million, and RMB 380 million, accounting for 13.11%, 15.60%, and 37.09% of its annual sales revenue, respectively. Currently, Beta Pharma has more than 30 projects in its pipeline, seven of which have entered clinical trial stages, providing room for sustained future performance growth.

The cases of CSPC Pharmaceutical Group and Betta Pharmaceuticals demonstrate that in China’s vast pharmaceutical market, pharmaceutical companies can seize market opportunities by strategically positioning innovative drugs. Particularly in therapeutic areas addressing major diseases with broad indications, domestically produced innovative drugs can compete head-to-head with products from multinational pharmaceutical companies, thereby meeting clinical needs while realizing their own commercial value.

The research and development of innovative drugs is a capital-intensive, long-cycle endeavor, making financial support particularly crucial. In addition to funding models backed by listed platforms, such as those of CSPC Pharma Group and Betta Pharmaceuticals, venture capital (VC) and private equity (PE) investments constitute a significant force.

Investing in innovative drugs rarely yields short-term returns, making investor patience crucial. Given the profitability requirements for listings on China’s A-share market, innovative pharmaceutical companies cannot achieve securitization until they have established stable profitability—unless through mergers and acquisitions. Consequently, listing in Hong Kong or the United States has become the primary option for these firms.

The listing of innovative pharmaceutical companies in Hong Kong and the United States is not driven by capital speculation, but rather represents a “relay” of capital support. From venture capital (VC) and private equity (PE) to the public capital markets, the financial backing for innovative drugs has become more robust, transforming investment in this sector from a “gamble” into a viable “business.” This development is undoubtedly positive news for the advancement of innovative drugs and therapeutic approaches, as only an institutionalized and industrialized investment model can ensure consistent output.

The recently hit film “Dying to Survive” reflects a harsh reality of innovative drug development: on one side are the exorbitant R&D costs and clinical outcomes fraught with uncertainty, while on the other are ordinary patients unable to afford medication, ultimately leaving generic drug manufacturers that disregard drug patents as the biggest beneficiaries.

The development of innovative drugs in China is essentially about resolving the contradiction between clinical needs and exorbitant drug prices. Only when Chinese innovations gain a foothold in the global market and break the monopoly held by multinational pharmaceutical companies will the era of “excessive profits” for their innovative drugs come to an end. This will enable ordinary patients to access better treatments with dignity.

George Merck, founder of Merck & Co., stated, “Merely inventing a new drug does not mark the completion of our mission. We must also explore effective pathways to ensure that the finest scientific achievements benefit all of humanity.” Advances in therapeutic modalities are not achieved overnight; fortunately, pharmaceutical innovation in China has taken its first step.