H1 2018 China Healthcare Investment & Financing Report: Surge in Mega-Deals, Pharma Sector Dominance, and Decline in Early-Stage Projects

According to VCBeat’s database, there were 513 financing deals in the global healthcare sector in the first half of 2018 (1H 2018), with total funding exceeding $14 billion. In China, the healthcare industry recorded 295 financing deals, a slight year-on-year increase of 7%, while the total funding amount reached $5.5 billion, representing a 1.35-fold year-on-year growth. The pharmaceuticals, primary care, and biotechnology sectors attracted the most capital, with their combined funding accounting for more than 60% of the total across all sectors.

Key Findings of the Report

Investment grew steadily, with mega-round financings contributing 81% of the year-on-year growth rate;

The pharmaceutical, primary healthcare, and biotechnology sectors attracted the most investment, while financing remained lukewarm in the distribution channels and medical support fields;

The proportion of early-stage financing projects continues to decline, while the share of mature projects hits a record high;

The healthcare sector saw the highest number of large-scale financing rounds, which occurred in primary care, consumer healthcare, biotechnology, pharmaceuticals, and health tech.

Beijing saw the most active financing, with over 80% of funding events occurring in Beijing, Shanghai, Guangdong, Zhejiang, and Jiangsu;

Sequoia, Matrix Partners China, and Qiming Venture Partners were the most active investors; biotechnology, consumer healthcare, and digital health were the most sought-after sectors.

Financing in the biotechnology, pharmaceutical, and medical device sectors tends to occur at later stages, with larger funding amounts.

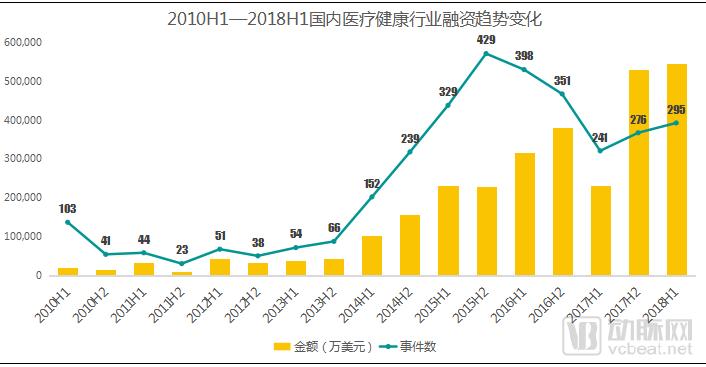

In H1 2018, a total of 295 financing deals occurred in China’s healthcare and medical industry, representing a year-on-year increase of only 7%, which failed to reach the peak levels seen in 2015 and 2016.

In H1 2018, financing in China’s healthcare and medical industry reached $5.46 billion, a significant year-on-year increase of 135%, setting a new record for the highest first-half fundraising amount in the sector. This growth was driven by seven mega-financing rounds exceeding RMB 1 billion each from the fields of primary care, consumer healthcare, biotechnology, pharmaceuticals, and health tech. These seven mega-deals totaled over $1.8 billion, contributing 81% of the growth rate.

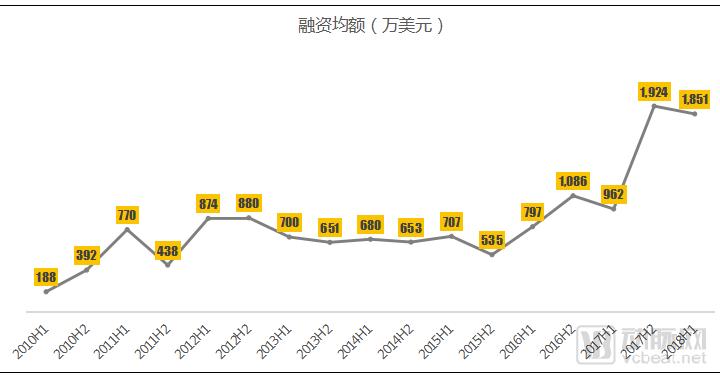

In H1 2018, the average financing amount in China’s healthcare industry experienced a slight decline to USD 18.51 million. Nevertheless, compared with the average financing amounts in recent years, the figure for H1 2018 still demonstrated substantial growth.

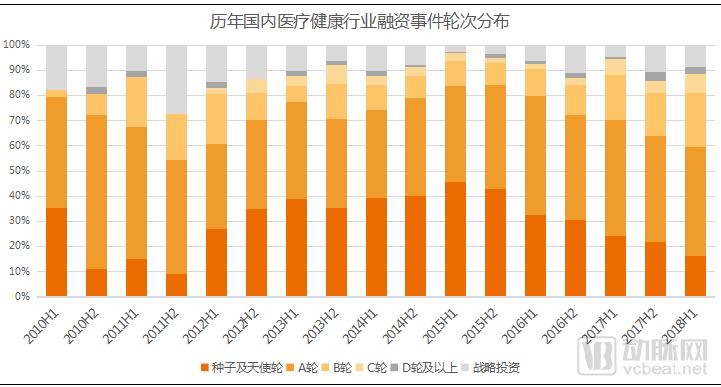

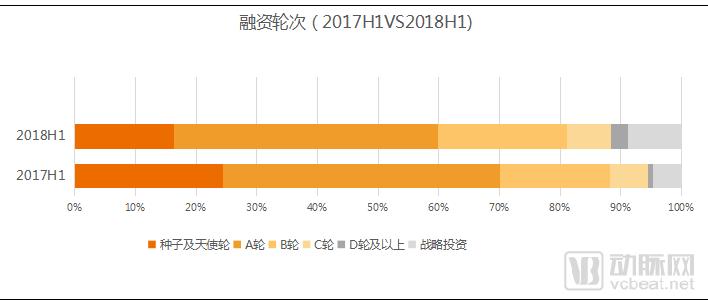

In H1 2018, the proportion of early-stage financing projects in China’s healthcare sector continued to decline, with seed and angel-round deals accounting for 58%, the lowest level in nearly five years.

In H1 2018, financing activity for mature projects in China’s healthcare sector increased, with the number and proportion of Series C, Series D, and later-stage financing deals reaching historical highs of 29 transactions and 9.8%, respectively.

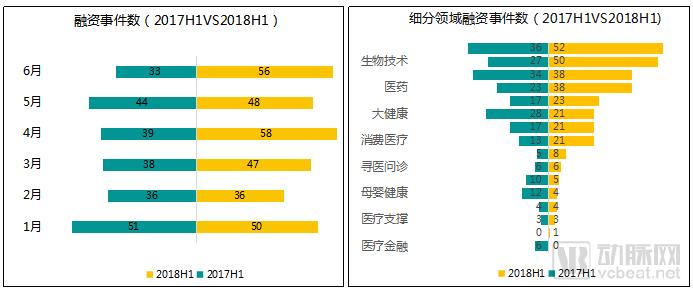

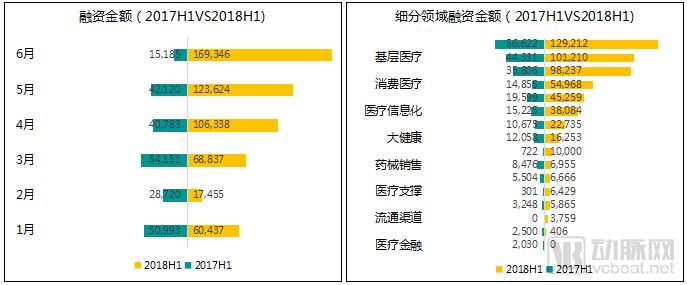

Compared with the first half of 2017 (2017H1), the number of financing events in the first two months of the first half of 2018 (2018H1) was basically on par with that of 2017, while all other months exceeded the 2017 levels, indicating a significant overall increase in financing activity.

In both H1 2017 and H1 2018, the number of financing events in the fields of medical devices, biotechnology, healthcare informatics, and pharmaceuticals ranked among the highest, reflecting capital’s strong preference for these sectors. Compared with H1 2017, H1 2018 saw a substantial increase in financing events in medical devices, biotechnology, pharmaceuticals, and consumer healthcare, while the number of financing events in healthcare finance, maternal and child health, pharmaceutical and medical device sales, and general wellness declined significantly.

Compared with the first half of 2017 (2017H1), financing amounts in all months of the first half of 2018 (2018H1) exceeded those of 2017, except for February, which saw a decline.

In both H1 2017 and H1 2018, financing amounts in the pharmaceuticals, primary healthcare, and biotechnology sectors stood out. Compared with H1 2017, financing amounts in H1 2018 declined only in the general healthcare and maternal-and-child health segments, while all other sectors surpassed their 2017 levels. Notably, the pharmaceuticals, primary healthcare, biotechnology, and consumer healthcare sectors saw substantial increases in financing.

Compared with the first half of 2017, the proportion of early-stage projects in China’s healthcare industry decreased in the first half of 2018. The combined share of seed, angel, and Series A rounds dropped from 69% to 58%, while the proportion of mature-stage projects rose from 7% to 9.8%.

In the first half of 2018, among the various sub-sectors of China’s healthcare industry, financing activity was robust in medical devices, biotechnology, healthcare IT, and pharmaceuticals, with these four sectors collectively accounting for over 60% of all financing deals. In contrast, financing cooled in distribution channels, healthcare support services, medical tools, and maternal and child health, which together represented only 4% of total financing events.

Pharmaceuticals, primary healthcare, and biotechnology ranked as the top three sectors in financing amount, with their combined total accounting for over 60% of the overall financing.

Primary healthcare, distribution channels, and the pharmaceutical sector each recorded the highest average transaction value, all exceeding USD 30 million. Notably, the primary healthcare sector witnessed the largest pre-IPO financing round in China’s health tech industry: WeDoctor raised USD 500 million in its Pre-IPO round.

In the first half of 2018, financing in China's healthcare sector remained dominated by early-stage projects, with Seed, Angel, and Series A rounds accounting for 58% of the total.

Medical devices, healthcare informatization, biotechnology, and pharmaceuticals had the highest number of early-stage projects, with each sector recording more than 20 early-stage financing deals, whileThe pharmaceutical, biotechnology, general health, and healthcare informatization sectors have the highest number of new projects.

Early-stage projects account for the highest proportions—each exceeding 75%—in the fields of online medical consultation, general health, rehabilitation and nursing care, and maternal and child health, whereas mature projects predominate in the areas of medical support services and healthcare professional tools.

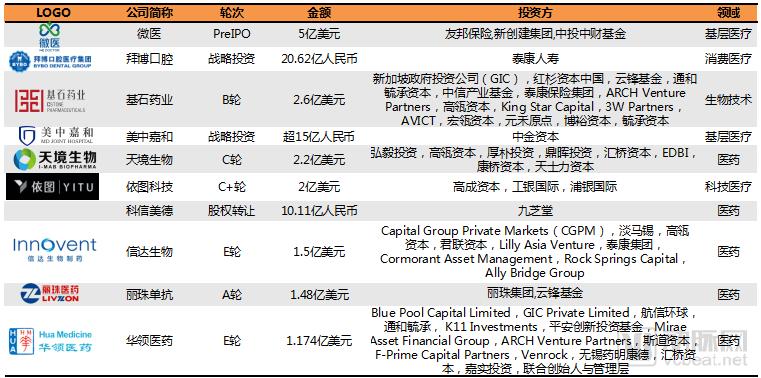

In the first half of 2018, the top 10 funded projects in China’s healthcare and medical industry each raised over USD 100 million, with financing rounds occurring at later stages. These top 10 projects were distributed across primary care, consumer healthcare, biotechnology, pharmaceuticals, and health technology sectors. Among them, the pharmaceutical sector had the highest number of large-scale financing deals, accounting for five of the top 10 spots.

Top 10 Financing Deals in China’s Healthcare Sector, H1 2018

WeDoctor

WeDoctor is China’s leading mobile internet healthcare service platform, founded in 2010 by Liao Jieyuan and his team. Leveraging internet technology, WeDoctor provides trustworthy services—including appointment registration, online consultations, remote consultations, electronic prescriptions, and medication delivery—to hundreds of millions of users in China. On May 9, 2018, WeDoctor announced the completion of a $500 million Pre-IPO financing round, valuing the company at $5.5 billion. This round set a record for the largest pre-listing financing in China’s healthcare technology sector.

Bybo Dental

Bybo Dental Medical Group is a leading non-public dental healthcare group in China in terms of scale. Founded by Mr. Li Changren in Shenzhen in 1993, it currently operates more than 200 dental medical institutions in over 50 cities, including Beijing, Shanghai, Guangzhou, and Shenzhen. On June 15, 2018, Taikang Life Insurance announced an investment of RMB 2.06236 billion to acquire a 51.56% equity stake in Bybo Medical. Following the investment, Taikang will provide Bybo Dental with multifaceted support in capital, customer resources, branding, and products. It will continuously leverage its own advantages to support Bybo Dental in marketing and promotion, talent development, discipline construction, and product development, while integrating resources such as IT, supply chain, and property management to provide comprehensive empowerment.

CStone Pharmaceuticals

CStone Pharmaceuticals (Suzhou) Co., Ltd. is a biopharmaceutical company dedicated to the development of next-generation innovative drugs, with a primary focus on tumor immunotherapy and combination therapies. The company currently has more than 10 products in its pipeline, four of which have sequentially initiated clinical trials both domestically and internationally. On May 9, 2018, CStone Pharmaceuticals announced the completion of a $260 million (approximately RMB 1.65 billion) Series B financing round, led by Singapore’s sovereign wealth fund, GIC, and participated by Sequoia Capital China, Yunfeng Capital, Tonghe Yucheng Capital, and other investors. This transaction set a record for the largest single Series B financing in China’s biopharmaceutical sector.

Meijiahe

Beijing Meizhong Jiahe Hospital Management Co., Ltd. is a network of oncology diagnosis and treatment centers under CCRC Healthcare Group, as well as an operator of chain independent medical institutions with a focus on radiotherapy. The company specializes in oncology imaging diagnostics and radiation therapy. On April 3, 2018, Meizhong Jiahe announced that it had secured RMB 1.5–1.8 billion in strategic investment from multiple institutional investors, led by CICC Capital.

I-Mab

Tianjing Biotech (Shanghai) Co., Ltd. is an innovative drug R&D enterprise focused on the therapeutic areas of tumor immunology and autoimmune diseases. To date, Tianjing Biotech has more than 10 biological drugs under development. On June 29, 2018, Tianjing Biotech announced the completion of a $220 million Series C financing round, led by Hony Capital and participated by Hillhouse Capital, Hopu Investment Management, CDH Investments, and others. This represents one of the largest Series C financing rounds in China’s innovative drug sector to date.

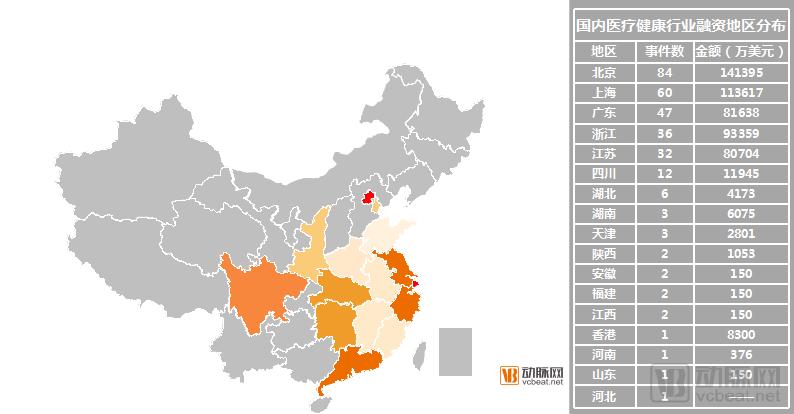

In H1 2018, healthcare financing events in China were distributed across 17 provinces, including Beijing, Shanghai, and Guangdong. Beijing was the most active region, ranking first in both the number of financing deals and the total amount raised. The number of deals in Beijing accounted for 28% of the national total in H1 2018, while the financing amount represented 26% of the national total.

The five provinces with the most active financing activities were Beijing, Shanghai, Guangdong, Zhejiang, and Jiangsu. Each of these five provinces recorded more than 30 financing deals and raised over USD 800 million, with both the number of deals and total funding amounts significantly exceeding those of other provinces. Moreover, the total number of financing deals in these five provinces accounted for 88% of all deals nationwide in the first half of 2018 (1H 2018), while their total funding amount represented as high as 94% of the national total for the same period.

In H1 2018, a total of 410 investment institutions entered the Chinese healthcare and medical industry. Among them, Sequoia Capital, Matrix Partners China, Qiming Venture Partners, SoftBank, CDH Investments, Honghui Capital, Legend Capital, and Shenzhen Capital Group were the most active. These eight active investment firms invested in fields such as biotechnology, pharmaceuticals, consumer healthcare, and digital health. They made the highest number of investments in biotechnology (8 deals), consumer healthcare (7 deals), and digital health (6 deals).

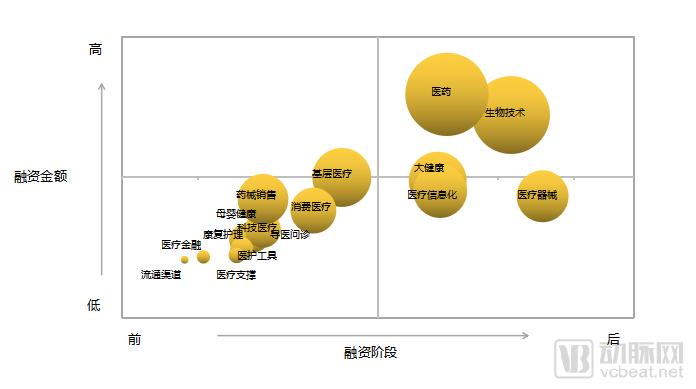

From H1 2010 to H1 2018, in China’s healthcare industry, sectors such as distribution channels, healthcare finance, and healthcare support services ranked higher in terms of overall financing activity but involved smaller financing amounts, whereas fields like biotechnology, pharmaceuticals, and medical devices ranked relatively lower in overall financing activity but attracted larger financing amounts.

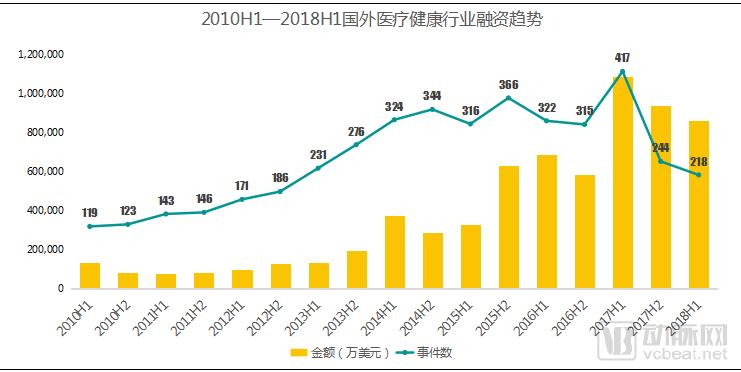

In the first half of 2018 (H1 2018), a total of 218 financing deals occurred in the overseas healthcare and medical industry, representing a year-on-year decrease of 48%. The total financing amount exceeded USD 8.6 billion, a year-on-year decline of 14%, primarily due to a significant reduction in financing projects in the fields of biotechnology, health informatics, medical devices, and digital health.

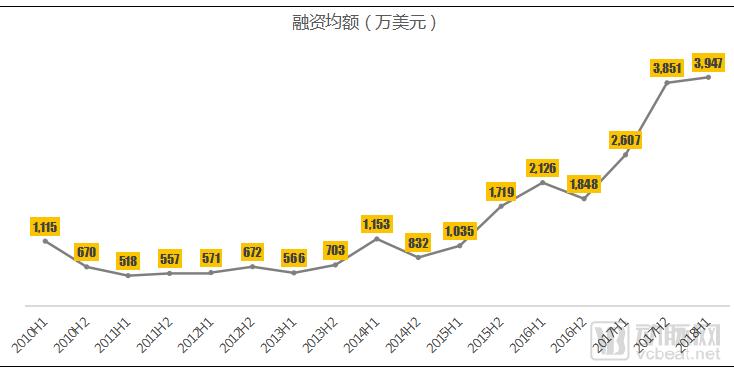

In H1 2018, the average financing amount in the overseas healthcare and medical industry saw a steady, slight increase, reaching $39.47 million.

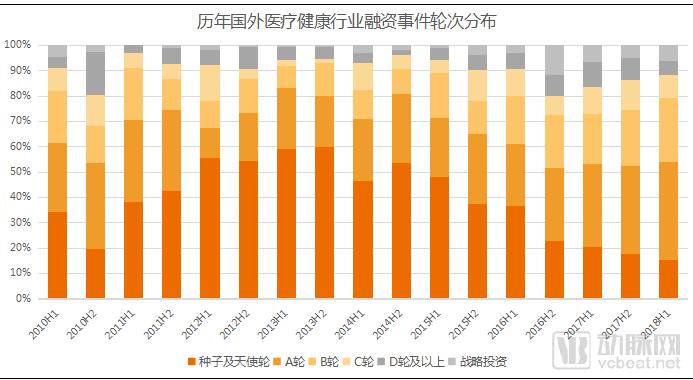

A comparison of the distribution of financing rounds in the overseas healthcare industry over the years reveals that the proportion of seed and angel rounds as well as Series A projects continued to decline in the first half of 2018, reaching a three-year low of 45%.

In H1 2018, the proportion of mature projects in the overseas healthcare and medical industry declined, with Series C, Series D, and later-stage projects accounting for 12%, the lowest level in the past three years.

In H1 2018, the overseas healthcare and medical industry saw active financing in biotechnology, healthcare informatics, and medical devices, with these three sectors accounting for 59% of all financing deals. In contrast, financing cooled in medical finance, maternal and child health, and rehabilitation and nursing care, which together represented only 3% of total financing events in H1 2018.

Biotechnology, pharmaceuticals, and medical devices attracted the most investment, with their combined funding accounting for 72% of the total in H1 2018, while fundraising in the fields of nursing tools, consumer rehabilitation and care, and consumer healthcare fell short of expectations.

In H1 2018, seed and angel rounds as well as Series A financing accounted for 45% of healthcare projects abroad, a lower proportion compared to China (58%).

Biotechnology, healthcare informatization, and tech-enabled healthcare accounted for the highest number of early-stage projects, with each sector recording more than 15 deals. Among these, healthcare informatization and biotechnology saw the largest number of new projects.

Early-stage projects dominate in maternal and child health, medical consultation, and tech-driven healthcare, each accounting for over 60% of the total. In contrast, mature projects are more prevalent in healthcare finance, medical devices, and general wellness, with each sector comprising over 15%.

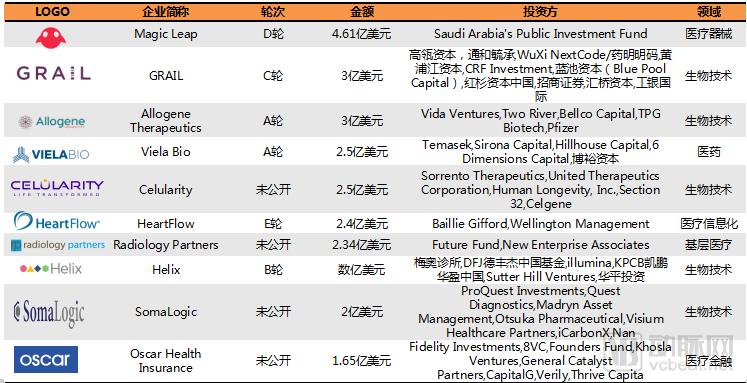

In the first half of 2018, the top 10 funded projects in the overseas healthcare and medical industry each raised more than $150 million. These top 10 projects were distributed across primary care, biotechnology, healthcare finance, medical devices, healthcare informatics, and pharmaceuticals. Among these, the biotechnology sector had the highest number of large-scale funding rounds, accounting for five of the top 10 spots.

Top 10 Financing Deals in China's Healthcare Industry in H1 2018