Four Key Players Enter the DTP Pharmacy Market, Targeting the Trillion-Yuan Prescription Diversion Opportunity Amid Challenges in Supply Chain, Prescriptions, Professional Services, and Payment

VCBeat (WeChat ID: vcbeat) has previously published a series of articles on the outflow of prescription drugs, exploring the policy background, primary channels for handling such outflows, future market scale, and shifts in pharmaceutical sales structures.

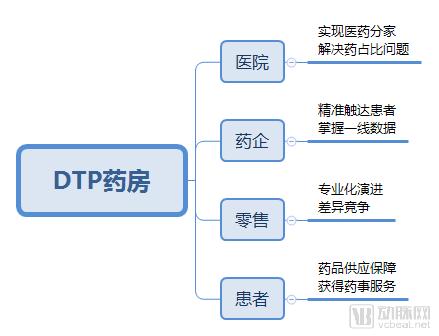

Hospital-adjacent pharmacies, entrusted pharmacy models, Direct-to-Patient (DTP) pharmacies, prescription-sharing platforms, and “Internet + Healthcare” models are the primary channels for accommodating the outflow of prescriptions from hospitals. Among these, DTP pharmacies are particularly noteworthy due to their professional services and capacity to ensure the supply of new and specialty drugs. This paper systematically reviews the DTP pharmacy model and aims to explore:

What Are the Characteristics of DTP Pharmacies, and What Problems Can This Business Model Solve?

How Should the DTP Pharmacy Model Evolve? A Benchmark Against the U.S. Pharmaceutical Retail Market

Which players in China are strategically positioning themselves in the DTP pharmacy sector, and what is the current state of its development?

What Role Do DTP Pharmacies Play Against the Backdrop of Separating Prescribing from Dispensing?

Can DTP Pharmacies Gain a Competitive Edge in the Separation of Prescribing and Dispensing Compared to Other Models?

DTP/DTC are abbreviations for Direct-to-Patient/Direct-to-Customer, referring to a pharmaceutical marketing model that delivers medications directly to patients. Its purpose is to streamline the pharmaceutical distribution channel, enabling patients to conveniently obtain their prescribed medications at specialized out-of-hospital pharmacies. These services typically include professional pharmaceutical care and patient management. In terms of business format, it closely aligns with retail pharmacies, representing an integrated dual aspect of the pharmaceutical retail sector.

The DTP pharmacy model originated in the United States in the 1990s, driven primarily by two factors: first, the differentiation of pharmaceutical distribution and retail sectors, evolving toward greater specialization; and second, pharmaceutical companies’ desire to reach patients more directly and enhance their control over the market.

Key Characteristics of DTP Pharmacies

In the 1990s, after decades of rapid growth, the U.S. pharmaceutical retail market saw a swift increase in industry concentration. By the late 1990s, the chain pharmacy rate had exceeded 50%, making differentiated competition particularly crucial. It was against this backdrop that specialty pharmacies emerged.

Specialty pharmacies provide pharmaceutical care services, chronic disease management, and pharmacy benefit management (PBM) beyond mere medication supply, thereby enhancing patient stickiness and loyalty and standing out in a homogenized competitive landscape. Direct-to-Patient (DTP) pharmacies are a type of specialty pharmacy; together with specialized pharmacies and PBM pharmacy models, they constitute the specialty pharmacy ecosystem.

Furthermore, since the 1970s, the United States has undertaken a series of “healthcare reforms,” with cost containment becoming the central theme for both government health insurance programs and commercial insurers. Under the pressure of cost containment, drug prices have been compressed, placing significant strain on pharmaceutical companies. In this context, pharmaceutical companies have sought to streamline drug distribution channels and reduce process-related costs, enabling drugs to reach patients through more economical means.

The alignment between the specialized pharmacy model and pharmaceutical companies’ needs has spurred the rise of the DTP (Direct-to-Patient) model. Through their ongoing integration, a “win-win-win” outcome has gradually been achieved: pharmaceutical companies have opened up new distribution channels, DTP pharmacies have secured stable revenue streams and established a firm market presence, and they have progressively developed high-value-added services such as pharmaceutical care, patient management, and chronic disease rehabilitation.

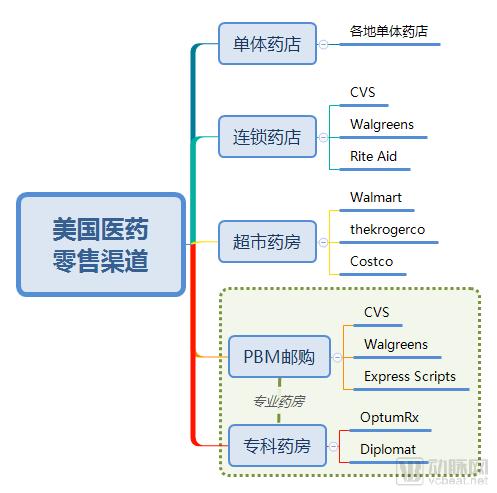

The United States has implemented the separation of prescribing and dispensing effectively, with approximately 70% of prescriptions filled outside hospitals. In contrast, China’s pharmaceutical retail structure roughly follows a 7:2:1 ratio. Major pharmaceutical retail entities in the U.S. include independent and chain pharmacies, specialty pharmacies, Pharmacy Benefit Managers (PBMs), and supermarket pharmacies.

Major Pharmaceutical Retail Channels in the United States

A well-developed network of retail and specialty pharmacies forms the foundation for the separation of prescribing and dispensing. The high concentration and robust management systems within the U.S. retail pharmacy industry provide the infrastructure necessary to support outpatient medication purchases. Furthermore, some insurance companies collaborate with Pharmacy Benefit Managers (PBMs) to deliver medications through their pharmacy networks or mail-order services.

From the perspective of chain pharmacies, Walgreens, CVS, and Rite Aid rank as the top three, with store-count market shares of approximately 34.20%, 30.90%, and 12.30%, respectively; collectively, these three account for 77.4% of the market.

Walgreens and CVS are both major PBM service providers. CVS holds approximately 30% of the PBM market, while Express Scripts and Walgreens account for around 20% and 10%, respectively.

From the perspective of market structure, retail pharmacies and specialty pharmacies roughly split the market. Taking 2016 data as an example, the annual prescription drug market size for the top 15 pharmaceutical retail entities was approximately $300 billion; chain pharmacies such as CVS, Walgreens, and Rite Aid generated around $160 billion in prescription drug revenue. PBMs and specialty pharmacies, including CVS, ESI, OptumRx, Prime Therapeutics, and Diplomat Pharmacy, accounted for the remainder of the market.

Under similar policy and industrial backgrounds, China’s pharmaceutical retail sector is gradually moving toward the U.S. model, with the concept of DTP (Direct-to-Patient) pharmacies gaining widespread popularity in the country.

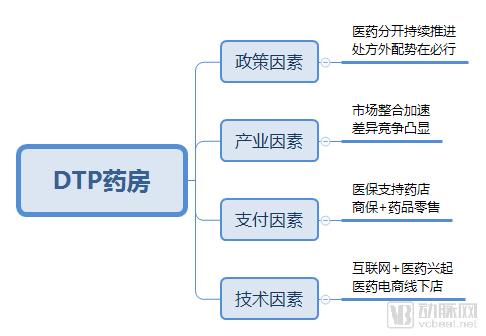

There are roughly four factors influencing the development of the pharmaceutical retail sector: policy factors; the continued implementation of the separation of prescribing and dispensing, along with measures such as zero markups on drugs and controls on the proportion of drug costs, which incentivize hospitals to extend prescriptions to community pharmacies; and the promotion of tiered diagnosis and treatment, which has shifted healthcare access and patient flow toward primary care levels, thereby driving medication demand downward and prompting pharmaceutical companies to focus more on the grassroots market.

Industrial environment factors: The retail pharmacy format is relatively mature, and the market is evolving toward vertical and horizontal integration models, where specialty pharmacies can drive differentiated competition;

From the payer perspective, increased health insurance coverage at pharmacies enables patients to receive equivalent reimbursement benefits both inside and outside hospitals. From the commercial insurance standpoint, some insurers have partnered with pharmacies to develop “pharmaceuticals + insurance” models, such as efficacy-based insurance and chronic disease management programs. At the individual patient level, there is a growing willingness to pay for superior treatment outcomes and enhanced pharmaceutical care services.

Technical factors, primarily the “Internet + Healthcare” model, leverage the internet to aggregate patient demand and amplify channel influence. The main models include Internet hospitals combined with pharmaceutical services, online pharmaceutical retail with offline stores, online ordering with in-store pickup or store delivery, and smart pharmacies.

Reasons for the Rise of DTP Pharmacies

Currently, there are roughly four types of players primarily promoting DTP pharmacies, including pharmaceutical manufacturers, distributors, retailers, and internet-plus-pharma companies.

Overview of Major DTP Pharmacy Institutions in China

Data source: VCBeat database, corporate annual reports

Pharmaceutical distribution and retail enterprises are the primary operators of DTP (Direct-to-Patient) pharmacies. This is because DTP pharmacies require robust connections with pharmaceutical manufacturers, making supply chain resources critical. Securing agency rights for new and specialized drugs from manufacturers enables DTP pharmacies to attract a larger patient base and ensure sustainable resource acquisition. Furthermore, DTP pharmacies demand professional medical guidance and pharmacist services; strong ties with hospitals facilitate prescription acquisition and enable the delivery of in-depth patient care.

Pharmaceutical distribution and retail enterprises have cultivated the market for many years, generally possessing abundant industrial and hospital resources. Against the backdrop of the separation of prescribing from dispensing and channel penetration into lower-tier markets, DTP (Direct-to-Patient) pharmacies operated by these enterprises can help hospitals meet the demand for out-of-hospital supply of new and specialty drugs, while simultaneously opening up new sales channels for pharmaceutical manufacturers. Essentially, DTP pharmacies represent a natural transformation of the resources held by pharmaceutical distribution and retail enterprises in response to changes in pharmaceutical sales channels and models.

Nevertheless, the emerging “Internet + Healthcare” model should not be overlooked. In the DTP (Direct-to-Patient) sector, Internet + Healthcare companies leverage their platforms’ aggregation capabilities to rapidly consolidate patient demand across China, offering greater scalability than the “three-kilometer coverage” typical of brick-and-mortar pharmacies. Meanwhile, they can also conduct remote patient management via mobile apps and websites, providing patients with integrated diagnostic, therapeutic, and pharmaceutical services.

It should be noted that internet tools and platforms are, in essence, a form of technology. Traditional pharmaceutical distribution and retail enterprises are also actively adopting this technology. Companies such as Sinopharm, Shanghai Pharmaceuticals, and China Resources Pharmaceutical are all strategically developing “Internet + Healthcare” platforms, with empowering the Direct-to-Patient (DTP) pharmacy model being a key direction.

The outflow of prescriptions is not actually complex; it simply means that hospitals and pharmacies each perform their respective duties. Hospitals return to their core medical function by divesting non-essential drug supply responsibilities, which are instead assumed by pharmacies and other entities. With this clear division of labor, hospitals alleviate the operational burden of pharmacy management, and the previously ambiguous issue of “funding healthcare through drug sales” can be addressed. Meanwhile, pharmacies, through systematic operations, provide patients with enhanced pharmaceutical care services.

Certainly, the separation of pharmaceuticals from medical services is a systemic issue involving the transformation of hospital revenue structures, the reflection of doctors' labor value, unified planning and settlement of medical insurance, and patients' habits in seeking medical treatment and purchasing medications. It cannot be achieved overnight. Hospitals also cannot completely divest their pharmacies, as this would leave inpatients and emergency patients without necessary safeguards.

A more reasonable projection is that China’s pharmaceutical retail channels will evolve toward a U.S.-style structure, with an approximately 3:7 split between in-hospital and out-of-hospital channels. Although this represents a long-term goal, it still allows for an estimation of the scale of “prescription outflow.”

In 2016, China's pharmaceutical market size was approximately RMB 1.5 trillion, representing a year-on-year growth of 8.3%. Tiered hospitals accounted for 68.4% of the market, pharmacies for 22.2%, and online pharmacies for merely 0.3%. Based on these figures, assuming the pharmaceutical market maintains a growth rate of around 8%, and that approximately 10% of prescriptions are filled outside hospitals by 2020, the scale of prescription outflow in 2020 is projected to reach approximately RMB 140 billion.

The DTP pharmacy business model is not solely designed to accommodate the outflow of prescriptions from hospitals. From a beneficiary perspective, factors such as the accelerated launch of new drugs, expanded coverage by commercial insurance, and increased out-of-pocket spending capacity will all stimulate continuous growth in the market size of DTP pharmacies.

The core product portfolio of DTP (Direct-to-Patient) pharmacies consists of novel and specialty drugs targeting oncology, autoimmune diseases, and other conditions, as well as medications for chronic diseases requiring long-term administration. From the perspective of drug supply, the availability of novel and specialty drugs is set to increase as China implements policies such as zero tariffs on anticancer drugs and priority review and approval for innovative therapies. Furthermore, there is a time lag between market approval and inclusion in the national medical insurance scheme; during this transitional period, DTP pharmacies will serve as a critical distribution channel. Even after these drugs are covered by medical insurance, DTP pharmacies can maintain their channel advantage through insurance reimbursement mechanisms.

From the perspective of commercial health insurance, data from the China Insurance Regulatory Commission (CIRC) shows that the compound annual growth rate (CAGR) of the health insurance market size was 42% between 2011 and 2016. In 2017, as of November, the gross written premiums for health insurance business reached RMB 410.554 billion, a year-on-year increase of 6.87%. The health insurance market size is projected to reach RMB 1 trillion by 2020. The rapid expansion of commercial health insurance coverage helps improve the level of social security, while also increasing coverage for new and specialty drugs, thereby stimulating their sales and benefiting the DTP (Direct-to-Patient) pharmacy model.

Furthermore, as national income levels rise, citizens will invest more in healthcare services. There is a stronger willingness to pay out-of-pocket for medications that demonstrably improve treatment outcomes, which benefits the DTP (Direct-to-Patient) pharmacy model.

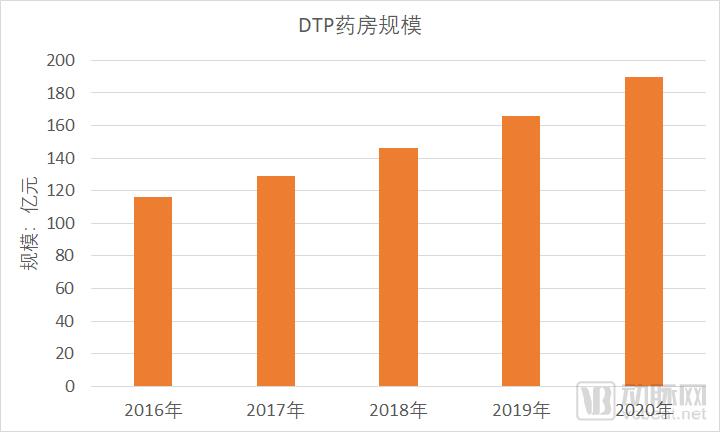

Based on calculations from annual reports of listed companies and publicly available data, the market size of DTP (Direct-to-Patient) pharmacies in China was approximately RMB 13 billion in 2017. The growth rate of the DTP pharmacy sector is expected to outpace that of the overall pharmaceutical retail market, with the market size projected to reach around RMB 19 billion by 2020.

Estimation of DTP Pharmacy Scale

Data Source: IMS, compiled by VCBeat

Guoda Pharmacy

Since 2014, Guoda Drugstore has been strategically developing its Direct-to-Patient (DTP) pharmacy business. As one of the innovative ventures in pharmaceutical retail, and leveraging Sinopharm Group and Sinopharm Accord’s extensive experience in pharmaceutical distribution and retail, as well as their deep connections with upstream manufacturers and downstream hospitals across the industry chain, Guoda Drugstore’s DTP business has achieved rapid growth.

According to the annual report, at the end of 2016, Guoda Drugstore had 16 DTP (Direct-to-Patient) pharmacy stores. In 2017, it added 24 new stores, bringing the total to 40. In 2017, Guoda Drugstore’s DTP sales revenue reached RMB 1.22 billion, a year-on-year increase of 20.33%. Based on the calculation of RMB 1.22 billion divided by 40 stores, the average annual revenue per DTP store of Guoda Drugstore was as high as RMB 30.5 million.

Shanghai Pharmaceuticals

Shanghai Pharmaceuticals is one of the earliest large-scale pharmaceutical distributors in China to strategically deploy Direct-to-Patient (DTP) pharmacies, having entered this sector in 2010. Leveraging its resources in distribution and retail, the company has built a DTP pharmacy network that originated in Shanghai and now covers most of East China. Additionally, it utilizes its cold-chain logistics capabilities to extend the service radius of its pharmacies and enhance their reach.

In November 2017, Shanghai Pharmaceuticals acquired Cardinal Health’s China business for over RMB 3 billion. The integration of Cardinal Health China’s DTP (Direct-to-Patient) pharmacies further solidified Shanghai Pharmaceuticals’ position as the operator of the largest DTP service network for new and specialty drugs in China. Currently, Shanghai Pharmaceuticals’ DTP pharmacy network covers more than 20 provinces and municipalities, with over 70 stores in total. Each pharmacy serves a radius exceeding 150 kilometers and provides free home delivery services to ensure access to self-pay medications for patients.

Yibao Brand New Pharmacy

Beijing Yibao Quanxin Pharmacy was established in February 2001 as a wholly-owned subsidiary of China Resources Pharmaceutical Group. Since 2009, it has expanded into specialty pharmacy services, strengthening its portfolio in novel and specialty medications as well as oncology drugs.

According to China Resources Pharmaceutical’s 2017 annual report, the Group accelerated the integration of retail resources in areas such as operational management, product categories, and information systems, actively established a centralized procurement platform, advanced the deployment of its Direct-to-Patient (DTP) business in western China, and vigorously pursued innovative business models including chronic disease management. By the end of the reporting period, the number of DTP pharmacies had reached 88, covering more than 50 cities across China.

The annual report also disclosed that the gross profit margin of China Resources Pharmaceutical’s retail business was 17.5%, a decrease of 0.8 percentage points compared with 2016. The decline in gross profit margin was primarily attributable to the rapid growth of its direct-to-patient (DTP) high-value drug delivery business, which carries relatively lower profit margins.

LinkCare • Smart Pharmacy

LinkCare Smart Pharmacy is operated by LinkDoc Technology, China’s largest unicorn enterprise in medical big data and artificial intelligence. LinkDoc specializes in medical big data—particularly oncology big data—and AI services, providing comprehensive big data solutions that cover pharmaceutical companies, healthcare institutions, insurers, and patients. It is reported that LinkDoc completed a RMB 1 billion Series D financing round in the first half of the year, laying a solid foundation for its future development.

To further enrich and refine its big data business layout, LinkDoc Technology established a dedicated subsidiary in September 2017 to oversee the nationwide deployment and operation of DTP pharmacy-diagnosis and treatment complexes. This initiative will become LinkDoc’s most critical enabling business for medical big data, creating strategic scenarios for new healthcare models.

LinkCare • Smart Pharmacy leverages deep collaborations between LinkDoc Technology and numerous large pharmaceutical companies and top-tier hospitals both in China and abroad to provide patients with integrated diagnosis, treatment, and medication services. Currently, LinkCare • Smart Pharmacy operates more than 20 stores, covering most provincial capital cities across China, and is projected to expand its store count to 40 by 2018.