Rock Health 2018 H1 Digital Health Investment Report: Five Key Highlights on Vertical Integration and IPO Challenges

ABILITY Network

Medical Insurance Service Provider

PillPack

Full-service Pharmacy

For the digital health sector, the first half of 2018 felt familiar, as it set another semi-annual venture capital record. The sustained upward trajectory in total venture capital investment from 2017 through the first half of 2018 was no coincidence.

Rock Health believes that two forces are at play: on the one hand, the sustained growth in investment is a manifestation of the maturation of digital health;On the other hand,In fact, venture capitalists across all industries, including digital health, are deploying capital at the fastest pace since 2006.

Digital health is increasingly defined by steady, repeat investors and emerging unicorns backed by large corporations in late-stage financing rounds.

Recently, the healthcare industry has seen a significant number of major restructuring announcements, such as Optum’s acquisition of DaVita Medical Group and Fresenius Medical Care, as well as Humana’s acquisition of Kindred Healthcare, indicating a growing trend toward vertical integration.At Rock Health’s recent Corporate Insights Forum, Vinod Khosla of Khosla Ventures pointed out that he has never seen disruptive innovation come from industry giants.

Typically, such innovations are driven by startups dissatisfied with the status quo of the industry, while industry giants acquire these innovative outcomes through capital restructuring.PossessionIndustry ChainWith a larger market share, large healthcare enterprises can expect to achieve higher efficiency and better outcomes. Previously, U.S. courts hadThe affirmative ruling in the AT&T and Time Warner vertical merger case has undoubtedly removed legal obstacles for large-scale healthcare mergers.

“Over the past 30 years, I cannot think of a single field where innovation was driven by a large institution. The retail industry was thrown into disarray by Amazon, not Walmart; the media industry was transformed by YouTube and Twitter, not CBS or NBC; the automotive industry was not reshaped by Volkswagen or General Motors. People used to say you couldn’t build cars in a startup, but then Tesla came along,” said Vinod Khosla.

This pattern also applies to the digital health industry.Apple AcquisitionGliimpse and Beddit,Advancing its healthcare strategy to promote interactive, API-driven access to health records; Google invests $3 trillion in partnerships with digital health startups to advance artificial intelligence.Making Headlines; Salesforce AcquisitionMuleSoft,New software launched for payers; Microsoft deepens its healthcare investments by adding additional leadership to Peter Lee’s Microsoft Healthcare team; Amazon has just announced the acquisition of PillPack, marking its highly anticipated official entry into the prescription drug market.

Whether as customers, partners, investors, or potential acquirers, the future of healthcare startups is inextricably linked to the strategies of large-scale enterprise healthcare companies—perhaps even more so than in other industries. Todd Pierce, a board member at both Dignity Health and Rock Health, recently pointed out that “acquisitions and M&A activity by buyers may be stifling innovation.” His greatest concern is that incumbent healthcare players are adopting new solutions too slowly to sustain startup growth.

Rock Health examined this topic and potential paths forward, summarizing the top five venture capital highlights from the story-rich first half of 2018.

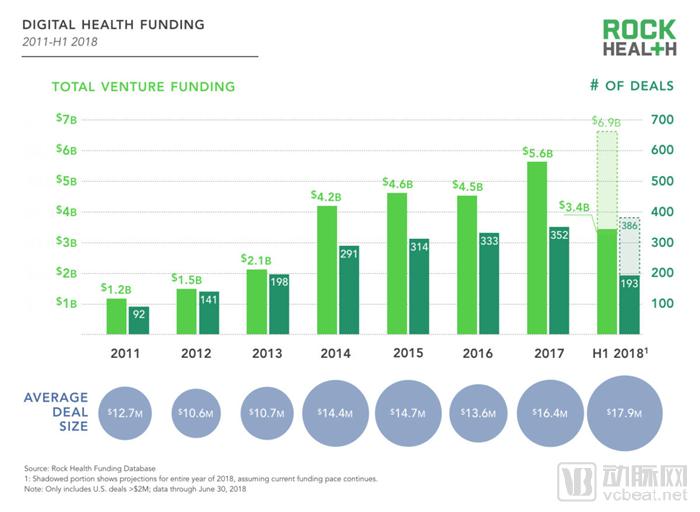

Highlight 1: $3.4 billion invested in digital health, setting a new record

From January 1 to June 30, 2018, the digital health sector completed a total of 193 capital transactions, with total investment reaching $3.4 billion. If capital inflows continue at the high pace seen in the first half (H1) of the year, both the total investment amount and the number of projects in 2018 will surpass those of 2017. Investors have shifted away from their previous strategy of concentrating capital in a small number of startups, opting instead to place larger bets on a broader pool of companies. As a result, the average deal size increased significantly to $17.9 million, setting a new record.

Digital Health Investment, 2011–H1 2018. Image source: Rock Health H1 2018 Investment Report

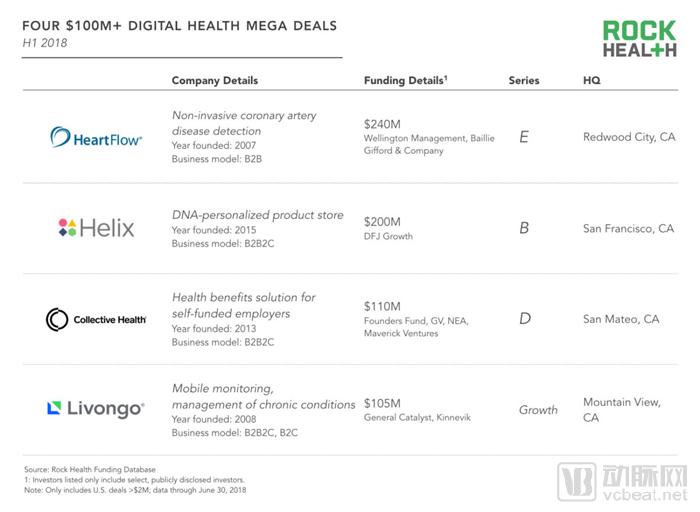

As digital health investments mature, capital is increasingly focused on companies in later financing rounds. In the first half of 2018, four companies completed individual funding rounds exceeding $100 million, qualifying as mega-deals. These transactions collectively accounted for one-fifth of the total investment amount in the first half of 2018 and were all completed by companies located in the Greater Bay Area.

Four Digital Health Companies with Financing Exceeding $100 Million. Image source: Rock Health H1 2018 Investment Report

Four Digital Health Companies with Financing Exceeding $100 Million

1、HeartFlow

Financing Amount: $240 million

Funding Round: B

Investors: Wellington Management, Baillie Gifford & Company

Product Area: Non-invasive Coronary Artery Disease Detection

Established in: 2007

Business Model: B2B

2、Helix

Financing Amount: $200 million

Funding Round: E

Investor: DFJ Growth

Product Area: Personalized DNA Product Storage

Established in: 2015

Business Model: B2B2C

3、Collective Health

Funding Amount: $110 million

Funding Round: D

Investors: Founders Fund, GV, NEA, Maverick Ventures

Product Area: Self-Funded Employer Health Benefit Solutions

Year Established: 2013

Business Model: B2B2C

4、Livongo

Financing Amount: $105 million

Funding Round: E

Investors: General Catalyst, Kinnevik

Product Areas: Mobile Monitoring, Chronic Disease Management

Established: 2008

Business Model: B2B2C, B2C

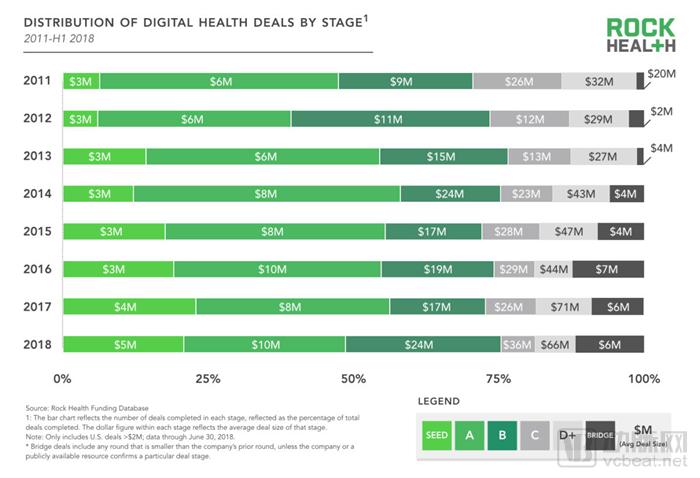

Moreover, the average deal size has increased since last year across nearly every financing round. Meanwhile, the proportion of seed-stage deals decreased from 23% in 2017 to 21% in the first half of 2018, while the number of Series B deals increased.

Distribution of Financing Rounds for Digital Health Companies from 2011 to H1 2018. Image source: Rock Health H1 2018 Investment Report

Highlight 2: Product efficacy validation based on clinical evidence has beenHigh Capital Attention

Currently, an increasing number of digital health companies have entered a critical phase of product efficacy validation, and they are attracting capital interest due to the clinical validation of their products. For example:

- Virta releases results from its one-year clinical trial and raises $45 million in Series B funding;

- Propeller Health raised $20 million in the second quarter to expand its long-term clinical studies;

- Omada Health has 10 peer-reviewed studies demonstrating the effectiveness of its digital health programs, received full recognition from the CDC in June, and has raised over $127 million;

-Pear Therapeutics completed a $50 million Series B financing round several months after the FDA approved its application for treating substance use disorder;

- Akili Interactive Labs plans to submit its video game-based digital therapeutic candidate for ADHD to the FDA, thereby completing a $55 million Series C financing round;

......

The focus on clinical trials reflectsDigital health companies and investors are adopting a “back-to-basics” mindset. Previously, healthcare companies claiming to possess revolutionary blood-testing technologiesTheranos became embroiled in bankruptcy turmoil due to questions about the validity of its technology. In June 2018, Theranos founderTheranos founder Elizabeth Holmes was charged by U.S. federal prosecutors in California with wire fraud and conspiracy. This case has sounded an alarm for the burgeoning digital health investment sector, making investors wary of repeating past mistakes and thus prompting them to require target companiesCarefully review data and evidence, and seek appropriate validation.

Currently, more companies are opting for clinical validation at the early stages of product development, while investors have raised their expectations. A competitive landscape based on robust results rather than hype is taking shape. On the policy front,The FDA is working to streamline its review process for digital health companies through a pre-certification program, but the plan has not been fulfilled.New rules are being established to meet the specific needs of AI and machine learning algorithms. This is crucial for the continuously expanding“Clinical validation requirements” are undoubtedly a boon.

Highlight 3: Investors Continue to Invest in Digital Health, No Longer Just Tourists

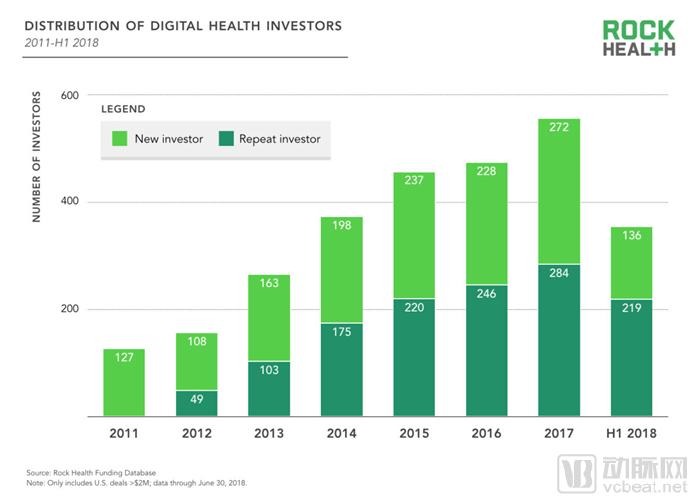

From 2011 to 2015, the number of first-time investors in digital health exceeded that of repeat investors. In recent years, we have been contemplating whether “tourist” investors, drawn by the novelty and associated hype of digital health, would cultivate the conviction, patience, and expertise required for successful healthcare investment. Currently, the answer appears to be yes. Since 2016, the number of repeat investors has begun to surpass that of new entrants into digital health, and the gap between the two continues to widen.

In H1 2018, 62% of investors had already participated in at least one digital health investment by 2011. In 2017, repeat investors accounted for 51% of the total investor base. The participation of these early-stage investors may help drive more digital health companies into later financing rounds.

Distribution of Digital Health Investors, 2011–H1 2018. Image source: Rock Health H1 2018 Investment Report

Data shows that in the first half of 2018 (H1), total investment in digital health by healthcare companies and repeat digital health investors doubled. Founders Fund was the most active digital health investor in H1 2018, having made eight investments. Additionally, Optum Ventures has launched a $250 million fund, which included co-leading the $13.8 million Series B financing round for Rubicon MD, a specialized eConsult platform, to support improvements in healthcare delivery, payment reform, and the provision of consumer-centric medical services.

Bessemer Venture Partners, a prolific digital health investor, has just launched a new $10 million seed fund to invest in AI-driven healthcare technologies.Bessemer launched thisPart of the rationale for this investment stems from the substantial returns generated by its prior participation in Qventus’ $30 million Series B financing round.

Highlight 4: The IPO Market Is Generally Pessimistic, but Listed Digital Health Companies Show Solid Performance

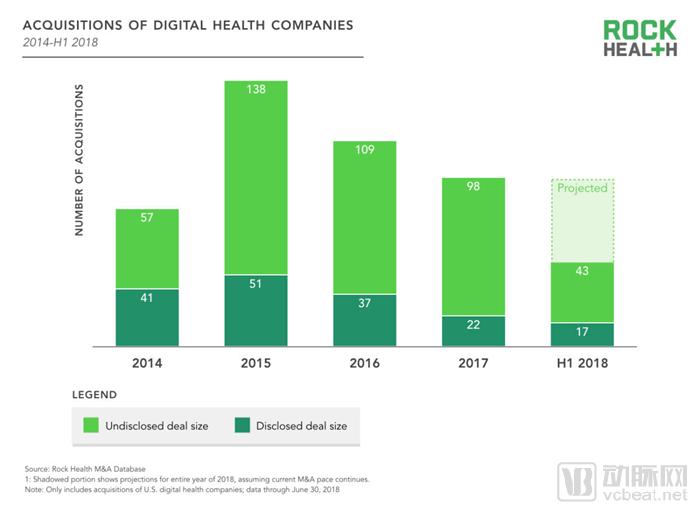

Overall, M&A activity in H1 2018 ran parallel to that of 2017, with a total ofDisclosed60 Digital Health Acquisitions. IPOs have continued their decline from the 2015 peak, but this trend is not unique to digital health. According to PitchBook and NVCA, Q1 exit values and rankings across the entire startup ecosystem have been the lowest since 2013.

Number of Digital Health Acquisitions, 2014–H1 2018 Image source: Rock Health H1 2018 Investment Report

In April 2018, Venrock released its second annual healthcare forecast, identifying Health Catalyst and Grand Rounds as the digital health companies most likely to go public. However, an IPO drought has persisted since iRhythm Technologies went public on October 20, 2016.

Drought is not due toDeficiencyCapital. Historically, digital health companies have raised an average of $136 million from venture capitalists prior to their initial public offerings (IPOs).Since 2011,Thirteen private digital health companies have each raised over $200 million in funding and remain active. However, as financing volumes increase, startups are staying private for longer periods, with the median number of years spent in private ownership across all industries reaching 8.2 years.

On the surface, digital health appears to be reversing the sluggish IPO trend. Recode noted that this spring was a “boon for tech company IPOs,” with biotechnology firms set to go public at an accelerated pace in 2018.

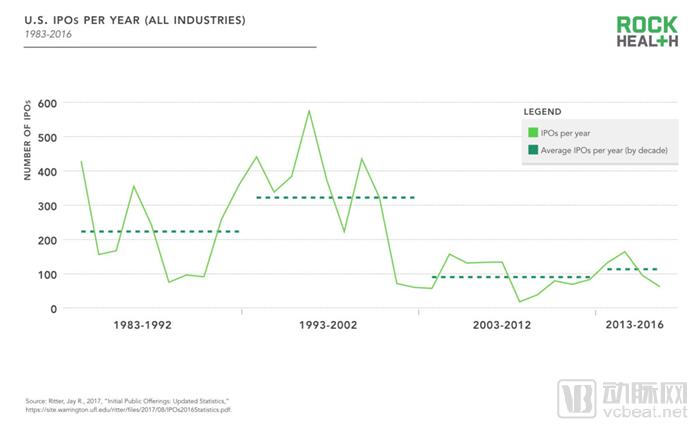

However, in the long run, the IPO boom in H1 2018 was not the same as that in the 1990s; today, companies’ propensity to go public is only half of what it was 20 years ago. The number of listed companies is now lower than it was 40 years ago, and the annual number of IPOs has declined each year since the dot-com bubble burst in 2002.

Annual Number of IPOs in the United States (1983–2016) Image source: Rock Health H1 2018 Investment Report

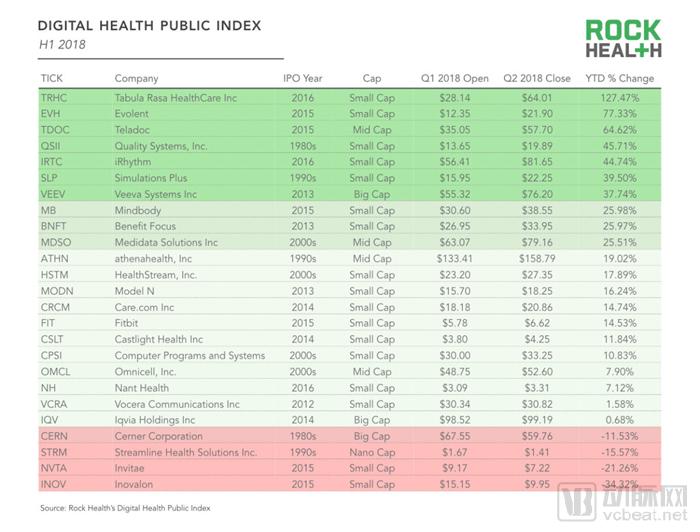

Despite the Bleak Outlook for Digital Health IPOs, the performance of the listed digital health companies index was outstanding. In the first half of 2018, stock prices in the digital health sector rose by a cumulative 22.2%, forming a sharp contrast with the S&P 500 Index, which had risen by only 1.7% year-to-date.

The companies with the largest stock price gains include Tabula Rasa Health Care, up 127.5%; Evolent Health, up 77.3%; and Teladoc, up 64.6%. Only four of the 25 companies in this sector saw their stock indices decline.

Digital Health Sector Stock Index in H1 2018. Image source: Rock Health 2018 H1 Investment Report

“With IPOs already in dire straits,” digital health investors appear to rely more on mergers and acquisitions for liquidity in the long term. Therefore, including healthcareThe Entire IndustryThe market appears increasingly concentrated among large, established companies. As numerous acquirers—including substantial private capital firms—enter the space, digital health startups may be acquired at more attractive valuations before they can achieve the predictable revenue, scale, and growth trajectories required for an independent initial public offering.

Mergers and acquisitions make significant sense for this emerging industry, as digital health startups create novel, complementary innovations that incumbent companies cannot easily replicate. For example, Amazon recently acquired the online pharmacy startup PillPack for nearly $1 billion. PillPack’s digital pharmacy solutions, nationwide contracts, and licenses—covering supply chain, home delivery, and medication adherence elements—enabled Amazon to rapidly enter the prescription drug market. Furthermore, in 2018February,Roche’s acquisition of Flatiron and the signing of a definitive merger agreement with Foundation Medicine in June further reinforced this significance.

Many startups may find that their assets hold greater value to established players in the healthcare industry than going public. As other larger digital health companies, or non-traditional players, enter the healthcare sector, we can expect more M&A rumors, such as those involvingPeople providing prescription drug discount cardsGoodRx-Related Rumors.

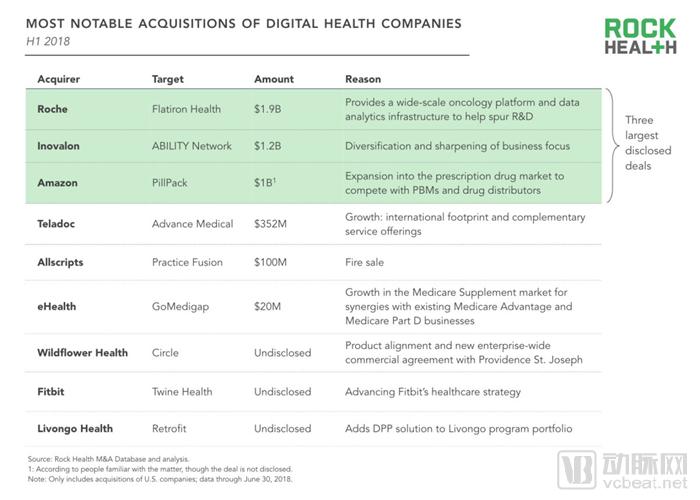

Most Notable Digital Health M&A Deals in H1 2018. Image source: Rock Health’s H1 2018 Investment Report

Most Notable Digital Health M&A Deals in H1 2018

1. Roche Acquires Flatiron Health

Transaction Amount: $1.9 billion

Driver: Provide a broad oncology platform and data analytics infrastructure to drive R&D

2. Inovalon Acquires ABILITY Network

Transaction Amount: $1.2 billion

Driver: Diversification and Sharpening of Business Focus

3. Amazon Acquires PillPack

Transaction Amount: $1 Billion

Drivers: Entering the prescription drug market to compete with PBMs and pharmaceutical distributors

4. Teladoc Acquires Advance Medical

Transaction Amount: $352 Million

Drivers:Expand global markets into Latin America and the Asia-Pacific region, and provide care in 20 languages through the platform.

5. Allscripts Acquires Practice Fusion

Transaction Amount: $100 Million

Driver: Targeted price reduction sale

6. eHealth Acquires GoMedigap

Transaction Amount: $20 million

Rationale: Strengthen partnerships with telecom operators and strategic allies to expand the population covered by health insurance services.

7. Wildflower Health Acquires Circle Women's Health Platform

Transaction Amount: Undisclosed

Drivers:Product Consistency and New Enterprise-Wide Commercial Agreement with Providence St. Joseph

8. Fitbit Acquires Twine Health

Transaction Amount: Undisclosed

Driver: Accelerating Fitbit’s Healthcare Strategy

9. Livongo Health Acquires Retrofit

Transaction Amount: Undisclosed

Rationale: Adding a DPP solution to the Livongo portfolio

In fact, existing digital health companies are the biggest acquirers of digital health startups, completing half of the M&A transactions in the first half of 2018. With ample capital, digital health companies seek rapid growth by expanding their product lines and hiring new employees, making mergers and acquisitions an ideal strategy.

A Wave of Telemedicine Acquisitions Emerged in H1 2018. To date, telemedicine companies TruClinic, Reach Health, Avizia, and Advance Medical have all been acquired by large digital health firms. As Medicare expands reimbursement rates and more states enact new telemedicine regulations, these companies may seek to expand the geographic reach of their customer base.

Highlight 5: Technology-Driven Behavioral Health Solutions Gain Investor Favor

Currently, mental illness is receiving heightened attention in the United States. The suicides of fashion designer Kate Spade and celebrity chef Anthony Bourdain have sparked public discourse, exposing the lack of behavioral health solutions across the nation. In fact, searches for “mental health services near me” on Google have reached an all-time high, indicating a societal need for more accessible, on-demand services.

Number of “Mental Health” Searches in the U.S., 2011–H1 2018. Image source: Rock Health H1 2018 Investment Report

Fortunately, emerging digital health companies are seeking more cost-effective and scalable ways to reach affected populations. In the first half of 2018 (H1 2018), behavioral health startups raised more funding than in any previous six-month period, with 15 such companies securing a cumulative total of $273 million—nearly double the $177 million raised in H1 2016. Among these 15 companies, more than half featured virtual or on-demand components.

Behavioral Health Companies That Secured Funding in H1 2018. Image source: Rock Health’s H1 2018 Investment Report

Through mental health apps, patients can receive immediate responses. In the United States,Psychiatric appointments may need to be scheduled nearly 25 days in advance, making immediate response appearparticularly important. Furthermore, the application provides more accessible and cost-effective services for individuals seeking face-to-face treatment, reaching those who are uninsured and cannot afford traditional mental healthcare costs, as well as patients who may be unable to access conventional treatment settings. For example, Ginger.io, a behavioral health app developer, reported that “user traffic is substantial outside the traditional 9 a.m. to 5 p.m. hours,” and its machine learning algorithms can monitor when patients should receive clinical or psychiatric care.

The aforementioned approach is not only convenient and reproducible but also effective. Multiple studies have demonstrated the efficacy of online programs utilizing cognitive-behavioral methods, and companies have leveraged these findings in developing their solutions. For example, after completing an initial assessment, Lantern users are assigned to specific protocol-based intervention plans, with their daily exercises supported by professional coaches.

H1 2018, WoebotLeveraging machine learning chatbots to improve access to mental health services,Secured $8 million in financing. Additionally, in May, Lyra Health completed a $45 million Series B financing round, and Regroup Therapy secured $5.5 million in funding. These companies have strengthened interpersonal connections by helping users match with providers either in person or remotely.

Actually,Investors paid attention toA Range of Mental Health Solutions from Prevention to Treatment. For instance, Calm.com and 10% Happier, which focus on using meditation to improve routine mental health, have raised $27 million and $5 million, respectively. Meanwhile, Pear Therapeutics, a company specializing in FDA-approved digital therapeutics for substance use disorders, completed a $46 million Series B financing round.

Summary

Rock Health predicts that the momentum seen in the first half of 2018 will continue through the end of the year. Venture capital investment is set to reach new highs in terms of total funding amount, number of deals, and average deal size. With the entry of well-capitalized startups boasting robust pipelines and ambitious goals to enhance healthcare capabilities, a surge in mergers and acquisitions is expected in the near future.