Where Did the Time and Money Go? Decoding the '10-Year, $1 Billion' Reality of New Drug Development

The debate and reflection on the healthcare system sparked by the film “Dying to Survive” continue, particularly with regard to innovative drugs, where the focus centers on why new medications are so expensive and how to improve their accessibility.

VCBeat (WeChat ID: vcbeat) has outlined the general process of new drug development and aims to reconstruct the cost structure of new drug development through a combination of data and case studies. The main argument of this article is:

1. New drug development is generally divided into four stages, taking an average of more than 10 years, with a success rate of less than 1 in 10;

2. Innovative drug R&D is a key strategy for pharmaceutical companies to enhance their competitiveness, with leading multinational pharmaceutical firms averaging an R&D-to-sales revenue ratio of over 20%;

3. Domestic cases reveal that Chinese pharmaceutical companies have already developed a certain level of innovative capacity, and innovative drugs enjoy a broad market;

4. In the cost structure of innovative drug R&D, clinical trials are the most capital-intensive, followed by personnel compensation and equipment costs; Phase IV study costs are also substantial.

5. From policy to market, China is accelerating efforts to “catch up,” with significantly enhanced innovative drug R&D capabilities whose outcomes will gradually materialize in the coming years.

New drug development is generally divided into four phases: early-stage drug discovery, preclinical research, clinical trials, and regulatory approval and market launch.

The primary tasks in the early stage of drug discovery include target disease selection, identification of therapeutic targets, selection of lead compounds, and optimization of lead compounds. The duration of this phase is variable; generally, R&D institutions conduct research based on prior work to ensure feasibility.

The main tasks in the preclinical research phase include identifying candidate drugs, conducting animal experiments, and performing pharmaceutical and pharmacological studies; this process typically takes 3–6 years.

The primary activities during the clinical trial phase include Phase I–III clinical trials, medical statistics, and data analysis. This process typically takes 6–7 years to ensure data integrity and accuracy.

Following positive clinical trial results, submit an application for approval to the drug regulatory authorities, register for production, and launch the product on the market. Post-marketing Phase IV trials are also required to further verify the drug’s safety, efficacy, and adverse reactions.

New Drug Development Process

Typically, it takes more than ten years for a drug to go from research and development to market launch; any significant error at any of the four phases will necessitate starting over.

Generally, among the four stages of new drug development, the clinical trial phase has the highest attrition rate. The success rates are approximately 65% for Phase I, 35% for Phase II, and 20% for Phase III clinical trials. Cumulatively, the overall success rate for the clinical trial phase is less than 10%. In specific therapeutic areas such as oncology, the success rate of new drug development is even lower.

Global data indicate that multinational pharmaceutical companies with high competitiveness also maintain relatively high R&D investment. Data show that in 2017, the ratio of R&D expenditure to sales revenue for the top ten global pharmaceutical companies by R&D spending was generally above 20%, reaching as high as 45%.

Top 10 Pharmaceutical Companies by Global R&D Investment in 2017

Data source: Company announcements, Menet, compiled by VCBeat

Data from China shows that pharmaceutical companies’ R&D investment remains relatively low, with most spending below 7% and the highest at only 12.71%.

Top 10 Pharmaceutical Companies in China by R&D Investment in 2017

Data source: Company announcements, Menet, compiled by VCBeat.

The global competitiveness of multinational pharmaceutical companies is closely tied to their substantial R&D investments. Sustained investment in research and development has driven the creation of high-quality drugs, giving rise to “blockbuster” therapies. For some pharmaceutical companies, a single drug can generate over $10 billion in global sales revenue, maintain market leadership for several years, and deliver substantial profits to the enterprise.

By implementing industrialized and standardized R&D processes, multinational pharmaceutical companies have effectively transformed new drug development from a high-risk endeavor into a matter of probability. Given a consistent 10% success rate, sustained investment ensures a continuous pipeline of high-quality innovative drugs.

However, natural risk aversion has also led to changes in the structure and approach of R&D investment by pharmaceutical companies. First, they tend to favor therapeutic areas with large patient populations, long treatment durations, or high costs, such as oncology, cardiovascular and cerebrovascular diseases, and anti-infectives, while overlooking the needs associated with rare and orphan diseases. Additionally, it is very common to develop similar new drugs targeting the same mechanism or to modify the crystal form of drug molecules to circumvent patents.

Secondly, the contract research model has emerged and gained prominence in pharmaceutical R&D, typically adopting a results-based payment structure for collaborative development. Large pharmaceutical companies export their R&D standards and processes to Contract Research Organizations (CROs), thereby converting fixed costs into variable costs, and agree to engage in joint development upon achieving tangible results to capture commercial value.

Business models that provide technical or management support for new drug development are also emerging, including patient recruitment, clinical trial data management, and real-world studies. These services help reduce the cost of new drug development and improve its efficiency.

Of course, more importantly, the rise of generic drugs has eliminated the upfront costs and processes associated with drug discovery and clinical trials, thereby increasing the success rate. In terms of pricing, they are also more readily accepted by the market. Taking the United States as an example, generic drugs account for 88% of all prescriptions, meeting the demand of government health insurance programs and commercial insurers for high-quality, affordable medications.

In addition, the research direction of "drug repurposing" is beginning to emerge. Discovering new drugs by identifying new indications for off-patent medications or through combination therapies represents a low-cost, high-efficiency approach to new drug development.

Having discussed the R&D process for innovative drugs and the innovation investments of leading enterprises, we now turn to a domestic case study—Beta Pharma. This pharmaceutical company has a relatively focused portfolio of innovative drug products and business operations. As a publicly listed company with transparent data, it lends itself to in-depth analysis.

Beida Medicine was established in 2003 by a team of overseas-returned PhDs. Its main product is Icotinib (Conmana), which is primarily indicated for the first-line treatment of patients with locally advanced or metastatic non-small cell lung cancer (NSCLC) harboring sensitive mutations in the epidermal growth factor receptor (EGFR) gene. It is also applicable for the treatment of locally advanced or metastatic NSCLC after failure of at least one prior chemotherapy regimen, where previous chemotherapy mainly refers to platinum-based combination chemotherapy.

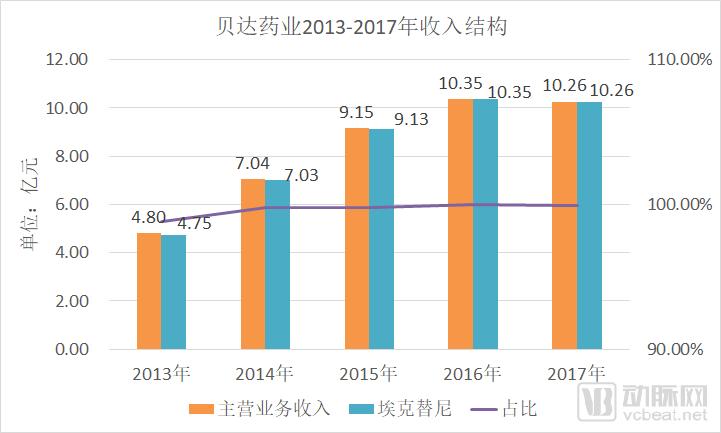

Icotinib was approved for market launch in 2011 and achieved strong market performance. Its sales revenue reached RMB 475 million, RMB 703 million, and RMB 913 million in 2013, 2014, and 2015, respectively. In 2016, its sales surpassed RMB 1 billion, with volume exceeding 550,000 boxes.

Betta Pharmaceuticals' Revenue Structure, 2013–2017

Data source: Company annual reports, compiled by VCBeat

In November 2016, Beta Pharma rang the opening bell on the ChiNext board, with Conmana contributing over 98% of its sales revenue and accounting for more than 99% of its gross profit. It can be said that Conmana, as a single drug, propelled Beta Pharma’s initial public offering.

Betta Pharmaceuticals' Net Profit Data from 2013 to 2017

Source: Company annual reports, compiled by VCBeat

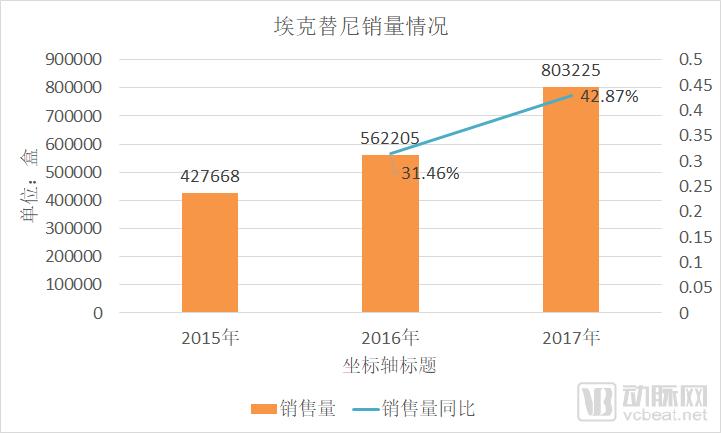

In February 2017, icotinib was included in the National Reimbursement Drug List (NRDL). Following price adjustments, its sales volume increased by 42.87%, largely offsetting the impact of the price reduction and achieving a “price-for-volume” strategy, with annual sales reaching RMB 1.026 billion. In fact, prior to its inclusion in the NRDL, Conmana (icotinib) had already been covered by medical insurance reimbursement in certain local regions, where its price had been adjusted accordingly.

Icotinib Sales Performance Over the Past Three Years

Data source: Company annual reports, compiled by VCBeat

The 2017 annual report also revealed that cumulative sales revenue of icotinib since its market launch had reached RMB 4.518 billion, with a total of 155,000 patients having taken the drug. In the first quarter of 2018, icotinib’s sales increased by more than 20% year-on-year. As provincial medical insurance reimbursement schemes continue to be implemented, icotinib is expected to see further growth in sales volume.

As the first listed company on China’s A-share market with innovative drugs as its core business, Betta Pharmaceuticals serves as a high-quality case study for analyzing domestic innovative pharmaceutical enterprises. As a publicly traded company, it provides relatively detailed and accurate financial disclosures, enabling us to dissect the cost structure of new drug development by examining materials such as Betta Pharmaceuticals’ prospectus, annual reports, and regulatory submission documents.

Data from the Center for Drug Evaluation (CDE) shows that Icotinib Hydrochloride Tablets (Conmana) were submitted for clinical trial approval in December 2005 and approved in June 2006.

According to data from the Clinical Trial Data Center, the Phase I and Phase IIa clinical studies of icotinib hydrochloride tablets in patients with various types of tumors, particularly non-small cell lung cancer (NSCLC), were approved by the Ethics Committee of the First Affiliated Hospital, Zhejiang University School of Medicine, in November 2007. The study was designed as a non-randomized controlled trial. A total of 71 participants across multiple cohorts were enrolled in the study, which concluded in December 2009.

During the same period, a Phase I study of icotinib hydrochloride tablets was also conducted at Peking Union Medical College Hospital from August 2007 to July 2008, with a total of 16 participants enrolled in two cohorts.

Icotinib was submitted for production approval in August 2010 and approved in June 2011. This indicates that the first two clinical trials demonstrated favorable results, meeting the requirements for production approval.

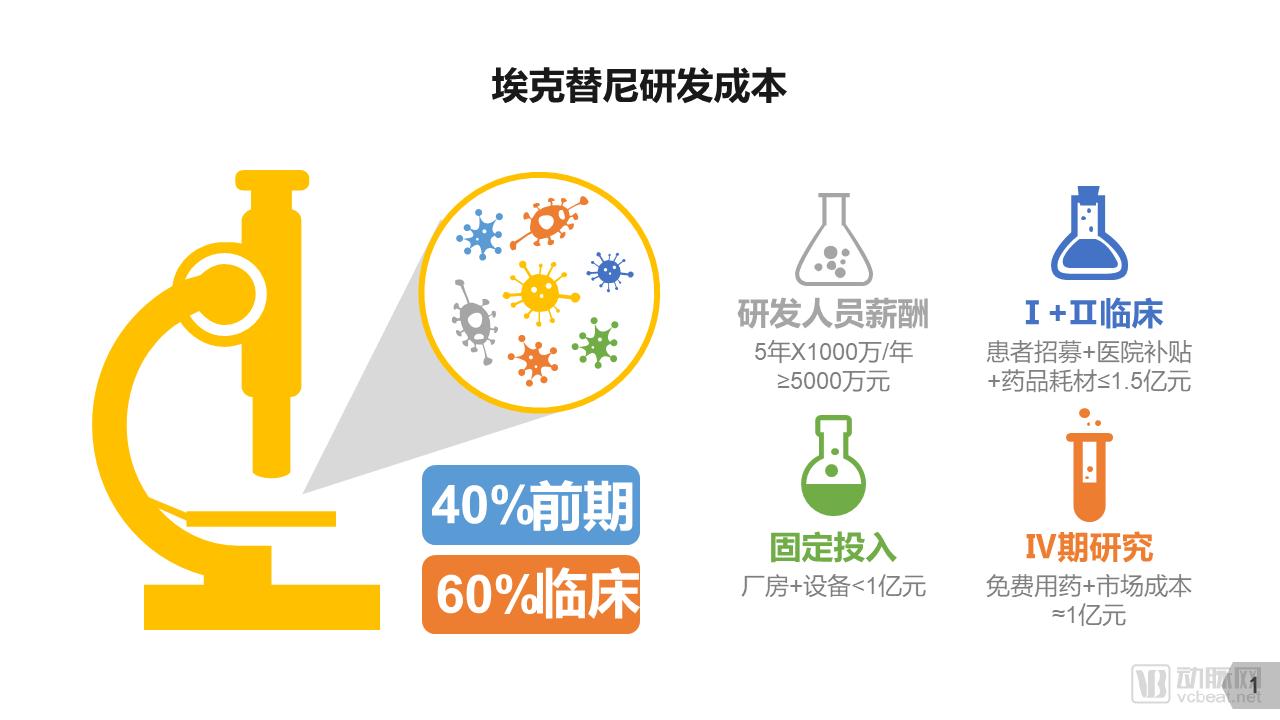

Industry insiders estimate that, based on standard industry costs for clinical patient recruitment, hospital subsidies, and pharmaceuticals and consumables, the pre-market clinical trial costs for icotinib amounted to approximately RMB 150 million.

In addition to clinical trial costs, drug development expenses also include R&D personnel compensation, preclinical research, equipment procurement, and facility construction, details of which can be found in the prospectus.

According to the prospectus, Beta Pharma’s fixed assets amounted to RMB 87.79 million at the end of 2013 and RMB 86.27 million at the end of 2014. Given that fixed assets represent one-time capital expenditures on equipment, facilities, and the like, the company’s spending in this category during the R&D phase would not exceed RMB 100 million.

Beida Pharmaceutical’s personnel compensation amounted to RMB 11.3 million and RMB 13.88 million in 2013 and 2014, respectively; based on a five-year R&D cycle, the cumulative R&D labor expenditure is estimated at approximately RMB 50 million.

Therefore, it can be estimated that the total R&D expenditure for icotinib was approximately RMB 250–300 million. Among these costs, clinical trials were the most capital-intensive.

Following the market launch of icotinib, a free medication program was implemented as part of the Phase IV study. In conjunction with this Phase IV clinical trial, Beta Pharma jointly conducted a subsequent free medication program for icotinib with the China Pharmaceutical Industry Research and Development Promotion Association.

After patients had continuously self-paid for icotinib for six months, those whose treatment response was assessed as effective by registered physicians at designated medical centers of the study, according to RECIST criteria, and who passed the review conducted by the Icotinib Subsequent Free Medication Program Office, became eligible to receive icotinib free of charge. Data show that a cumulative total of 50,440 patients enrolled in the free medication program, with 2,744,281 boxes dispensed in total. This volume exceeded the sales of icotinib during the same period and can also be regarded as a significant cost.

As disclosed in the prospectus, the costs of free medication for Icotinib’s Phase IV clinical trials from 2013 to the first half of 2016 were RMB 8.7314 million, RMB 16.8822 million, RMB 25.8165 million, and RMB 16.2464 million, respectively, all of which were expensed in the period in which they were incurred.

Based on this calculation, the total cost of Icotinib’s free medication program since its market launch is approximately RMB 100 million. However, this figure should not be viewed solely as a Phase IV clinical trial expense, as market promotion is also a significant objective; the difference lies primarily in the accounting treatment.

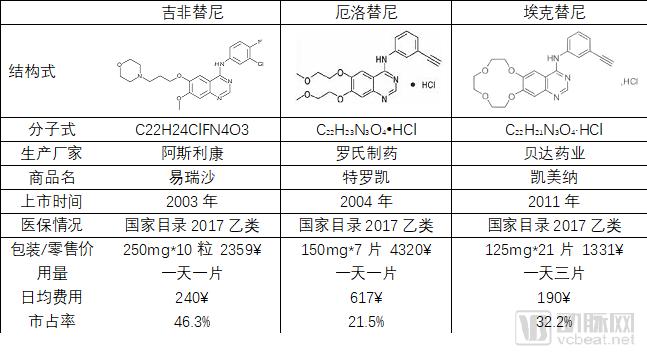

It is worth noting that Icotinib’s competitors, Gefitinib (Iressa) and Erlotinib (Tarceva), have implemented similar promotional initiatives. AstraZeneca partnered with the China Charity Federation to launch the Iressa Patient Assistance Program, which was officially initiated in 2007; Roche collaborated with the China Charity Federation to establish the Tarceva Patient Assistance Program, launched in 2008.

Of course, the case of icotinib does not fully represent the R&D costs and structure of innovative drugs. First, its drug development concept was benchmarked against gefitinib and erlotinib, making it a “me-too” innovative drug. It did not require independently identifying new targets or conducting compound screening from scratch, resulting in relatively lower costs. Additionally, considering the lower labor and resource costs in China, the total cost of developing icotinib was also comparatively lower.

Nevertheless, the case of Beta Pharma offers a broad overview of the primary and secondary costs, as well as the cost structure, associated with innovative drug R&D, thereby providing a valuable benchmark for new drug investment.

Comparison of the Three Major Drugs: Gefitinib, Erlotinib, and Icotinib

Data sources: Medication Reference, Yaozhi.com, 111.com.cn, compiled by VCBeat

“Dying to Survive” Exposes the Imbalance Between Supply and Demand for Innovative Drugs in China. Most innovative drugs are developed by multinational pharmaceutical companies, which hold significant pricing power. Even with uniform global pricing, these drugs impose a considerable financial burden on Chinese patients, whose incomes are lower than those in developed countries. Consequently, patients turn to low-cost generic drugs from India.

Why India Can Produce Low-Cost Generic Drugs Is Closely Related to Its Pharmaceutical Policy Environment. The Most Significant Factor Is Compulsory Licensing of Patents, Which Allows Indian Companies to Manufacture Generic Versions Before the Original Drug Patents Expire. This Measure Aims to Ensure Access to Medications for Its Citizens, Making India a “No-Go Zone” for Patented Drugs. However, Due to Factors Such as Patent Protection Systems and Trade Rules, Although China Has Similar Legal Provisions, They Have Never Been Implemented.

There are three approaches to addressing the “Dying to Survive” dilemma: first, strengthening our domestic capacity for innovative drug R&D, leveraging the cost and competitive advantages of local enterprises to deliver superior innovative pharmaceutical products; second, reducing the prices of innovative drugs from multinational pharmaceutical companies through measures such as tariff reductions, value-added tax adjustments, and price negotiations; and third, improving the social security system, including critical illness assistance under basic medical insurance, commercial health insurance, and charitable patient assistance programs.

In fact, these three aspects are precisely what we are currently implementing. For instance, the reform of drug review and approval has shifted from “addressing backlogs” to “encouraging innovation,” allowing innovative drugs to access a green channel for priority review and approval. Furthermore, policies and measures aimed at fostering innovation in pharmaceuticals and medical devices—such as the implementation of the Marketing Authorization Holder (MAH) system, the transition to a filing-based system for clinical trial institutions, the acceptance of international multi-center clinical trial data, the establishment of a drug patent linkage system, and incentives for the development of Contract Research Organizations (CROs) and Contract Manufacturing Organizations (CMOs)—have provided comprehensive support for the advancement of innovative drugs.

In terms of reducing the prices of innovative drugs, measures include health insurance negotiations that trade price for volume. Meanwhile, China implemented a zero-tariff policy on anticancer drugs starting May 1. On June 20, the State Council’s executive meeting further adopted measures to accelerate the approval of new drugs already marketed overseas, implement price reductions for anticancer drugs, and strengthen the supply guarantee for scarce medicines.

With improved policies and industry follow-through, leading pharmaceutical companies such as Hengrui Medicine, Fosun Pharma, CSPC Pharmaceutical Group, Kelun Pharmaceutical, Tasly, and BeiGene are actively positioning themselves in the field of innovative drugs. Data from the Center for Drug Evaluation (CDE) shows that nearly 80 innovative drugs have entered Phase III clinical trials or production application stages, covering areas such as oncology, respiratory diseases, and diabetes, including cutting-edge PD-1/PD-L1 therapies.

From a capital perspective, since 2013/2014, VC/PE investment in the innovative drug sector has entered a period of sustained growth. Data from VCBeat shows that since 2014, there have been 323 financing rounds in China’s new drug sector, involving a total amount of approximately RMB 32 billion, with an average single financing amount close to RMB 100 million. This trend has also fostered the emergence of leading enterprises such as Innovent Biologics, MicuRx Pharmaceuticals, Ascletis Pharma, Zai Lab, and BeiGene.

With improved policies, industrial follow-through, and capital support, China’s innovative drug sector is on a path of sustained growth. In the future, unconventional heroes like the “Drug God” will become increasingly rare.