Top 10 Digital Business Models Set to Transform the Health Insurance Industry File for IPO

According to Alipay’s official Weibo account, as the box office success of the film *Dying to Survive* sparked a wave of public interest, search volumes for insurance-related mini-programs on Alipay surged by 400% over the past two days. Meanwhile, following the boat capsizing incident in Phuket, Thailand, travel insurance has also become a focal point of attention.

Amidst irreversible natural disasters and human-made calamities, insurance provides an additional layer of security for daily life. However, even within this industry known for its stability, the waters are far from calm. A report released by the market research firm Research2guidance indicates that digital technologies are reshaping insurance operations. The report also highlights ten disruptive digital business models in the health insurance sector. VCBeat (WeChat ID: vcbeat) has compiled and reported on these findings.

A report by EY on the transformation of the insurance industry points out: In an era focused on differentiated value, insurance products offered in the past had little differentiation and were largely interchangeable. Insurance companies have lagged behind other healthcare institutions in terms of process complexity and price transparency. Furthermore, although insurers regard data and analytics as key drivers of value and sources of growth, they make relatively limited use of the data they have already generated.

Traditional insurance giants are undergoing transformation; their vast data reserves may become either an advantage or a burden. In the past, health insurers’ pricing and risk assessments treated risk as static. In the future, insurers will need not only to perform quantitative analysis on large volumes of data but also to understand why customers make certain choices.

Due to data fragmentation, no single entity in the healthcare sector possesses a comprehensive view of the patient. Different stakeholders—payers, providers, pharmacies, device manufacturers, and others—hold disparate fragments of information. Although companies have begun merging to address many of these challenges (e.g., Symphony Health Solutions and GNS Healthcare), no one is yet capturing and integrating data from the growing pool of mobile health technologies, which are generating real-time insights into patient behavior.

For insurance companies, this exacerbates the problem of information asymmetry. Although health insurers have extensive experience in underwriting and pricing health-related risks, these functions are unfortunately based on limited patient information.

Insurance companies have limited understanding of their customers (whose information typically includes demographic characteristics, the insured’s health status, and family medical history), and regulatory frameworks further restrict the use of certain customer data in pricing.

To make matters worse, emerging technologies such as personal genome sequencing may exacerbate information asymmetry, as insurers may be prohibited from using genomic data in underwriting decisions. As in many other industries, the first to respond to these challenges are likely not the established giants in the insurance sector, but rather innovative new entrants.

Digital Technology Will Transform the Health Insurance Business.The advancement of digital technologies—particularly apps, sensors, and artificial intelligence (AI)—along with the widespread adoption of these technologies, has driven the emergence of new business models in the health insurance sector.Early adopters have begun implementing new digital business models and achieved initial success.

released by research2guidanceThe report, “10 Disruptive Digital Business Models for Health Insurers,” describes how startups, health insurance companies, and payers in general have begun leveraging these technologies to pilot new forms of health insurance products and gradually assume the role of healthcare providers.

research2guidance Report Summarizes 10 Disruptive Digital Business Models for Health Insurers

New digital models are reshaping the relationship between insurers and patients. For instance, digital insurers have rebuilt trust with patients by outsourcing much of their value chain to their members, thereby gaining deeper insights into their needs. Digital business models also tend to blur the lines between payers and care providers. Some pioneers have crossed these boundaries, beginning to offer services that were previously provided exclusively by doctors and nurses.

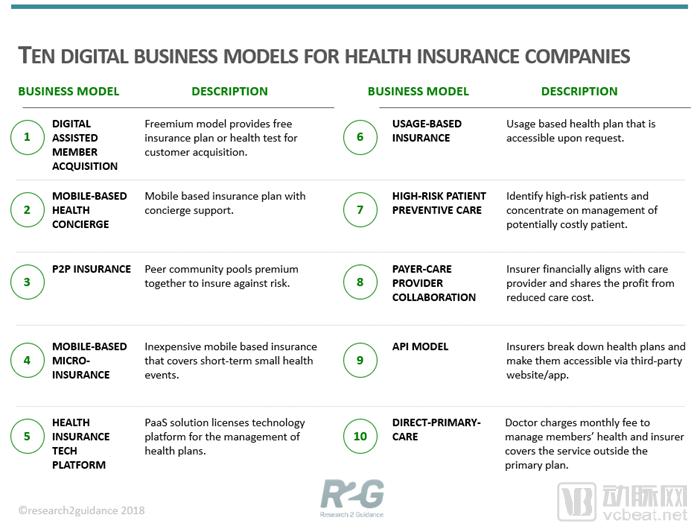

1. Acquiring users through digital assistance is a freemium business model.The freemium model offers customers free insurance plans or health tests with their purchases. Insurers are becoming more involved in users’ health management, rewarding healthy behaviors. The role of insurance companies is evolving—from merely quantifying and pricing risk to actively influencing and mitigating it. In this data-centric, technology-enabled new model, the volume of information available to insurers is growing exponentially, requiring companies to gain a deeper understanding of their customers than they currently possess. In the future, insurers may also serve as users’ health stewards. Beyond collaborating with core suppliers such as technology firms and hospitals, insurers will need to partner with large supermarkets, gyms, and sports facilities.

2. Mobile Health Contracted Medical Care refers to a service where health insurance providers assemble specialized, customized teams for users, enabling them to complete all health insurance claims via their mobile phones.The insurance industry has begun to transform its complex claims processes and lengthy cycles, but these changes fall far short compared to advancements in other sectors. In new health insurance models, users enjoy more convenient operations. The care services provided by Oscar Health may illustrate this model: each member is assigned a care guidance team and a dedicated nurse. This means that every phone call or text message is handled by a dedicated specialist rather than a call center. Users receive personalized care from a team familiar with their health conditions. They refer to this as the “Concierge Team.”

3. P2P Insurance Refers to Risk-Sharing Communities. Members of the Same Community Share Premiums to Mitigate Risk.Peer communities share premium costs to mitigate risk. Members contribute a certain amount of funds to join a mutual aid group and receive medical financial assistance according to the principle of “shared burden in case of illness.” All user contributions are exclusively used for mutual aid, enabling low- and middle-income groups to easily afford coverage and gain risk resilience. The operational model is similar to Shuidi Mutual Aid, a subsidiary of Shuidi Inc., where members can join the mutual aid program for as little as RMB 9 and receive up to RMB 300,000 in medical funding. However, in China, Shuidi Mutual Aid operates as an online mutual aid platform, and the China Insurance Regulatory Commission has explicitly stated that the products offered by “Shuidi Mutual Aid” do not constitute insurance.

4.Mobile micro-insurance covers health insurance plans for short-term minor illnesses or small-scale long-term health insurance.For instance, ZhongAn Insurance has launched a women-exclusive insurance plan with premiums starting at just RMB 20, providing comprehensive coverage for female-specific malignant tumors, specified diseases, specified carcinoma in situ, and specified surgeries.

5.A health insurance technology platform refers to a tech platform that sells its technologies for managing health plans and users to its B-end clients.The insurance industry is not only facing disintermediation but will also be technology-driven in the future. Blockchain, for instance, serves as a significant force propelling transformation within the sector. By establishing an industry-wide synchronized information database, blockchain helps address fraud and mitigate risks, while enabling more efficient claims processing. The market is projected to reach $42 billion by 2023.

In 2016, ZhongAn Insurance established its technology subsidiary, “ZhongAn Technology,” a fintech company dedicated to research in cutting-edge technologies such as blockchain, artificial intelligence, big data, and cloud computing. By bringing together top-tier scientific and technical talent from the industry and leveraging its accumulated sector expertise, ZhongAn Technology delivers technological products and industry-specific solutions to the fields of inclusive finance and healthcare, thereby supporting innovation and startup incubation for both internal teams and external partners. In 2018, ZhongAn further founded “ZhongAn International” to focus on global promotion and international cooperation opportunities within the insurtech sector.

6.# On-Demand InsuranceOn-demand insurance is a usage-based model that allows members to customize health plans according to their needs with the help of mobile applications.Amid the sweeping tide of big data and user-centricity, the insurance industry is compelled to confront new challenges, moving away from the outdated “one-size-fits-all” approach. Instead, it is leveraging big data to launch personalized and customized insurance products. SURE, an overseas insurance sales platform, offers customized insurance solutions to its customers. By employing artificial intelligence to predict the areas in which users are most interested in obtaining coverage, SURE recommends the most cost-effective insurance options once users make their selections.

7. High-risk patient preventive care models focus on insuring and managing patients who may incur substantial healthcare costs.Leveraging big data and wearable devices to identify potential major health threats, enabling insurance coverage for critical illnesses and reducing medical costs. An Ernst & Young report on the insurance industry highlights that chronic diseases account for an increasing share of healthcare expenditures, prompting both public sectors and taxpayers to seek ways to curb these costs. For long-term conditions such as diabetes and hypertension, some insurers are focusing on these high-risk areas by leveraging the Internet of Things (IoT) ecosystem and collaborating with public sector entities to help users manage their health risks associated with high-risk diseases.

8. The payer-provider collaboration model represents a closer and more digital partnership between payers and providers, particularly for hospitals. Insurers align financially with healthcare providers and share in the profits generated from reducing medical costs. Collaboration between insurers and hospitals yields greater competitive advantages. First, it helps build stronger trust. Second, through joint efforts in preventive care, timely intervention, and compliance monitoring, it reduces patients’ out-of-pocket medical expenses. Meanwhile, designated hospitals streamline the claims process, delivering a superior healthcare experience for customers.

9. API health insurance model insurers, and enable access through third-party websites/applications.Health insurance users generate millions of critical data metrics every day. If health insurance companies can penetrate this dynamic market, leveraging their financial strength and substantial value, they will not only become leading data providers but also ensure the security of their own critical data.

10. Direct Primary Care Model。In this model, general practitioners charge a fixed monthly fee, rather than billing separately for routine consultations and prescriptions as in traditional practice. This one-time fee is lower than the combined cost of previous individual consultations and prescribed medications. This model streamlines the clinical workflow, allowing physicians to focus more on patient care. The involvement of insurance companies helps alleviate the financial burden on both physicians and patients by covering costs that exceed the fixed fee.

Early adopters of these models have seen favorable outcomes, with positive impacts primarily evident in company valuations, the ability to attract new members, cost structures, and revenue streams. Currently, the primary impact of digital business models is on company valuations, as directly reflected by the hype surrounding certain companies in the investment community. Companies such as Oscar, Clover Health, and Bright Health achieved valuations exceeding $1 billion after only a few years of operation.

Health insurers and startups in the United States and China are the most proactive in adopting new digital business models. Companies in other regions tend to adopt a follower strategy or engage in imitation.

The report also lists several companies that are disrupting the health insurance model; VCBeat has compiled an overview of the current status of nine of these companies.

1. Oscar health

Oscar Health was founded in 2013 against the backdrop of the Affordable Care Act’s individual mandate, initially focusing on leveraging internet and big data technologies to provide health insurance services to low-income populations. The company began its transformation following President Trump’s election and subsequent efforts to repeal the Affordable Care Act.

The transformation has already been achieved. Oscar has begun charging higher premiums and now offers a so-called “narrower network,” which uses technology to connect members with physicians, encouraging them to access a curated panel of high-quality healthcare providers.

Within the care services provided by Oscar Health, each member is assigned a care guidance team and a dedicated nurse. This means that every phone call or text message is handled by a designated individual rather than a call center. Members receive personalized care from a team well-versed in their health conditions, which Oscar refers to as the “Concierge team.”

Oscar Health has raised a total of $890 million in funding. Investors include Ping An Insurance, Goldman Sachs, and two subsidiaries of Alphabet (Google’s parent company): Capital G and Verily.

For details, see the VCBeat report:

2. Water Drop

Shuidi Inc., founded just over two years ago, has rapidly joined the ranks of internet companies with hundreds of millions of users, boasting more than 100 million independent paying users and over 400 million registered users. Currently, the company operates four core businesses: “Shuidi Mutual Aid,” “Shuidi Crowdfunding,” “Shuidi Insurance,” and “Shuidi Charity,” making it the fastest-growing internet-based protection platform in China.

Shuidi Inc. also secured RMB 210 million in investment from Tencent, BlueRun Ventures, Gaorong Capital, Sinovation Ventures, IDG Capital, ZhenFund, Meituan Dianping, and the Tongcheng Public Welfare Foundation, achieving a valuation of nearly RMB 3 billion.

Shen Peng, the founder of Shuidi, is a former executive at Meituan. A graduate of the Central University of Finance and Economics, he co-founded Meituan Waimai in 2013 and served as the head of its national operations, leading the platform to capture the largest market share in China. In April 2016, Shen left Meituan Dianping to establish Shuidi Company.

Shuidi Insurance has been able to capture a significant market share in a short period, becoming the leading distribution platform for numerous insurance products. For each product category, Shuidi selects only the one or two options with the highest cost-performance ratio. Its platforms, Shuidi Chou (Shuidi Crowdfunding) and Shuidi Huzhu (Shuidi Mutual Aid), not only command a user base of over 400 million but also serve as the most effective channels for consumer education.

3. ZhongAn Insurance

ZhongAn Insurance is China’s first internet-based insurance company, driven by the philosophy of leveraging technology to upgrade the insurance industry. Established in October 2013, ZhongAn Insurance was jointly invested in by Alibaba Group, Ping An Insurance, and Tencent. The company went public in 2017.

ZhongAn’s strategy for designing insurance products has always been characterized by “small premiums, high frequency, large volume, and fragmentation.” Leveraging scenarios in e-commerce (Taobao), online travel agencies (Ctrip), and consumer electronics (Xiaomi), return shipping insurance, flight delay insurance, and screen breakage insurance have long contributed the majority of ZhongAn’s premium income. By entering numerous consumption scenarios through small-ticket insurance products, ZhongAn has accumulated vast amounts of data; the more scenarios it covers, the more comprehensive its data becomes, resulting in more precise user profiling.

Although ZhongAn Insurance has consistently enjoyed strong investor confidence and capital support, it has also faced persistent criticism for its inflated valuation, weak profitability, and excessive reliance on distribution channels.

In November 2016, ZhongAn incubated a technology company—ZhongAn Technology—dedicated to providing technical solutions to small and medium-sized insurance companies and other clients.

For details, see the VCBeat report:

The First Internet Insurance Stock Is Born: ZhongAn Insurance’s Valuation May Reach $10 Billion

4.BIMA

BIMA is dedicated to providing insurance services for low-income consumers. It has raised a total of $170 million in funding and is valued at approximately $300 million. Founded in 2010, BIMA is an insurance platform specializing in “microinsurance” services for emerging markets, with headquarters in Stockholm, Sweden, and London, UK. By partnering with local mobile operators and insurance companies, BIMA offers affordable insurance and medical consultation services.

Although BIMA originated in Europe, its business operations began in Ghana, a less developed country. Currently, BIMA’s largest markets include Ghana, Sri Lanka, Bangladesh, and Pakistan. The company serves 26 million customers across 15 countries worldwide, with 75% of them accessing insurance for the first time. Notably, 93% of its customers live on less than $10 per day.

All BIMA products are registered, purchased, claimed, and paid for via mobile phones. Wherever there are mobile devices, BIMA can sell its products. For people in remote areas, smartphones are not required; insurance products can be purchased via SMS. There are no strict restrictions on issues such as whether policyholders have bank accounts. Therefore, BIMA is very easy to promote, both in terms of hardware requirements and ease of operation.

In terms of partnerships, BIMA collaborates with Allianz, a global insurance giant. Since 2004, Allianz has been offering microinsurance products and has currently launched nearly 25 such products across 11 developing countries in Asia, Africa, and Latin America. In 2016, Allianz’s microinsurance premium income reached €303 million, with cumulative coverage extending to 55 million people. Allianz X, the investment arm of Allianz, has participated in two consecutive follow-on funding rounds for BIMA, making it a major investor in the company.

5.Clover health

Clover Health is a “unicorn” company that provides health insurance for seniors aged 65 and older through insurtech solutions. Headquartered in San Francisco, USA, Clover Health is a health insurance startup founded in 2014. After five rounds of financing, it has raised a total of $425 million, with a valuation of approximately $1.2 billion.

Generally, health insurance companies prefer to underwrite healthy individuals, as patients with chronic conditions incur high medical costs. Consequently, cost containment for the chronically ill has long been a key operational challenge for health insurers. Clover Health aims to manage the health of customers with chronic conditions and control medical expenditures through data analytics. It predicts diseases that may pose health threats and provides insurance coverage accordingly. Although the insurance industry traditionally prefers insuring healthy clients, companies like Clover Health are actively working to improve the health of their customer base.

From 2013 to 2017, Clover Health’s membership grew from a few thousand to 25,550, with projected operating revenue of $275 million in 2017. In 2015, by leveraging medical data from 7,000 members to effectively reduce the incidence of complications and acute symptoms, Clover Health cut its hospital readmission rate in half, from 12% in 2014 to 6% in 2015.

6.Bright health

Founded in 2015, the company is forging exclusive partnerships with health systems and institutions in the market to support the relationship between patients and providers. Headquartered in Minneapolis, the company will also reshape how people and doctors achieve better health through exclusive collaborations with healthcare systems and health insurance plans. It has raised a total of $240 million across two rounds of financing.

Bright Health is committed to transforming the traditional healthcare system through a collaborative care model. BRight Health is a venture-backed health insurance company that primarily offers health plans and integrated technological expertise, providing economic incentives to health systems for the delivery of efficient, high-quality healthcare. The company is working exclusively with leading health systems and health insurance plan providers to foster closer relationships between patients and care providers.

7.Bind

Bind is designed for today’s mobile lifestyle. Unlike traditional health insurance, which may include services you never need or want, Bind allows you to pay only for what you need, not for what you don’t, and adjust your coverage as your needs change, truly delivering on-demand, customized insurance.

Through machine learning, Bind leverages its proprietary algorithms to help users more effectively reduce healthcare benefit costs. Having completed three rounds of financing, Bind has raised a total of $72.5 million. The company is currently backed by multiple institutional investors, including Ascension Ventures, Lemhi Ventures, and UnitedHealthcare.

8.Collective health

Collective Health offers companies a smarter alternative to traditional health insurance. Through its cloud-based, integrated health benefits platform, the company enables insured employers to derive greater value from their healthcare investments while providing better care for their employees. To date, it has raised a total of $259 million in funding, with Google leading its Series C round.

In the $1.2 trillion employer-sponsored health insurance market, Collective Health has experienced exponential growth—its membership increased 500-fold over three sales cycles. Currently, the company covers 70,000 employees across 15 self-insured employers; clients includeThe World's Largest Game Developer and PublisherActivision Blizzard, CrossFit, eBay, Silicon Valley big data company Palantir, and Red Bull.

9.Ottonova

Ottonova Krankenversicherung is a German insurance company aiming to drive genuine innovation within the private, more traditional health insurance sector. Ottonova empowers users to truly understand the insurance services they purchase. In contrast to short-term coverage, Ottonova champions sustainable personal health management insurance. The earlier one joins the Ottonova insurance plan, the lower the premiums incurred.

Ottonova does not pursue a low-price strategy; instead, it emphasizes high-quality service. Ottonova offers human customer support, which reduces time costs and provides users with a smoother service experience.