11 Core Insights: How Enterprise Chain Models Achieve Maturity – A Case Study of Aier Eye Hospital Group

Content Summary

This article primarily compiles publicly available information, the prospectus, annual reports from 2009 to 2017, and selected industry research reports related to Aier Eye Hospital. We have collected and organized extensive relevant materials for analysis and research, covering more than ten aspects, including the number of hospitals, hospital distribution, the tiered diagnosis and treatment system, data on the top ten core hospitals, in-hospital floor area, personnel structure, incubation period, basic financial metrics, chain management efficiency, and incentive mechanisms.

Analytical Methods:

The full text will conduct an analysis across three dimensions, encompassing more than ten secondary indicators and multiple tertiary indicators. The three primary dimensions are: the self-portrait of chain layout, internal strategies under the chain layout, and standardization models. Within the dimension of chain layout analysis, we divide the development of Aier Eye Hospital into three stages. Through the lens of these three developmental stages, we interpret Aier Eye Hospital’s strategic planning for its chain model, which includes secondary indicators such as the tiered system, the number of hospitals, and hospital distribution. The internal strategies under the chain layout will be analyzed by examining the group’s management structure, personnel structure, and incentive policies to assess their impact on the overall strategic layout. The standardization model extends from the data involved in the chain model analysis to explore the standards for single-store replication at Aier Eye Hospital.

Research Objective:

1. An Analysis of How Aier Eye Hospital’s Chain Model Has Reached Maturity.

2. Analyze the changes in layout strategy, revenue structure, operational strategy, and management strategy across the three stages of Aier Eye Hospital's development.

3. Explore how Aier Eye Hospital standardizes and replicates its successful hospital model.

4. The ultimate objective of this paper is to provide a reference for the chain layout strategy of all chain enterprises through the analysis of Aier Eye Hospital.

1.1 Introduction to Aier Eye Hospital

Aier Eye Hospital Group is a globally leading ophthalmic medical chain institution and a healthcare provider listed on the ChiNext board of the Shenzhen Stock Exchange, with stock code 300015. It was included in the CSI 300 Index in 2015. Aier Eye Hospital Group primarily provides patients with ophthalmic medical services, including diagnosis and treatment of various eye diseases, as well as medical optometry and glasses prescription.

Aier Eye Hospital is the largest ophthalmic medical institution in China and one of the fastest-growing ophthalmic medical institutions in the country.

In the 2008 and 2009 selections of China’s Most Investment-Worthy Enterprises, Aier Eye Hospital Group stood out from nearly 1,000 nominated companies nationwide, being named to the “Zero2IPO – Top 50 Most Investment-Worthy Enterprises in China” list for two consecutive years.

1.2 Business Performance

The 2017 annual report of Aier Eye Hospital Group shows that the group’s revenue reached RMB 5.96284 billion in 2017, with a CAGR of 28.9%; operating profit reached RMB 1.1126 billion, with a CAGR of 26%; gross profit margin reached 46.26%; outpatient visits totaled 5.07 million, with a CAGR of 21.9%; and surgical procedures reached 517,613 cases, with a CAGR of 19.9%.

1.3 Chain Scale

As of 2018, Aier Eye Hospital Group had established more than 200 specialized ophthalmic hospitals across 30 provinces, municipalities, and autonomous regions in mainland China, with an annual outpatient volume exceeding 6.5 million visits. Furthermore, the group has expanded its presence to the United States, Europe, and Hong Kong. Aier Eye Hospital Group has become the largest ophthalmic hospital chain globally.

1.4 Technical Strength

In 2013, Aier Eye Hospital Group jointly established a specialized ophthalmic medical school with Central South University—the Aier School of Ophthalmology at Central South University—primarily dedicated to training advanced master’s and doctoral-level professionals in ophthalmology. In 2014, it further collaborated with Hubei University of Science and Technology to establish the Aier School of Optometry and Ophthalmology. In 2011 and 2015, Aier Eye Hospital successively founded the “Aier Institute of Optometry and Ophthalmology” and the “Aier Institute of Ophthalmology.” With these initiatives, Aier Eye Hospital has integrated the three core domains of ophthalmology: clinical practice, education, and research. The establishment of these academic institutions and research institutes will significantly enhance Aier Eye Hospital’s scientific research capabilities and clinical standards, thereby driving the development and advancement of ophthalmic healthcare in China.

As of 2016, Aier Eye Hospital’s team of specialized ophthalmologists and physicians numbered nearly 3,000, including a large cohort of master’s and doctoral supervisors, holders of Ph.D. and postdoctoral degrees, scholars who have studied in Europe and the United States, and core experts with extensive clinical experience, making it a highly regarded and dynamic force in China’s ophthalmology sector.

1.5 Market Capitalization

As of July 2, 2018, the share price of Aier Eye Hospital Group was RMB 32.30 per share; its total market capitalization reached RMB 77 billion; its price-to-book ratio was 14.09; and its dynamic price-to-earnings ratio was 88.89x.

2.1 Outstanding Financial Performance: Revenue and Outpatient Volume Show Geometric Growth

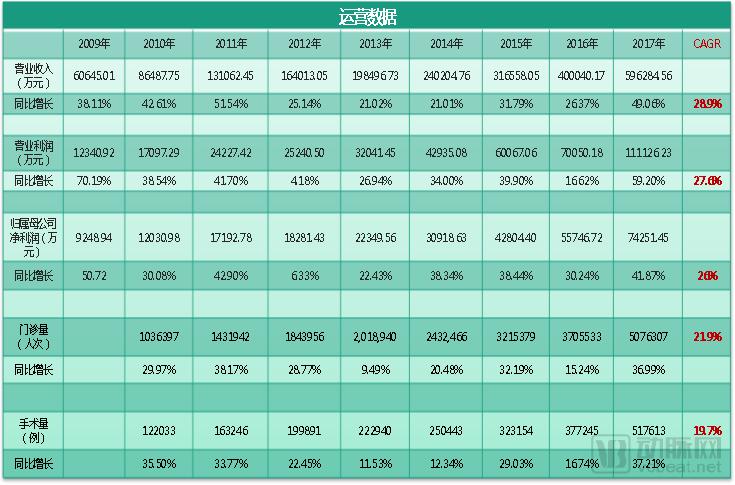

Figure 2.1 Aier Eye Hospital's Historical Operational Data

Data Source: Aier Eye Hospital Annual Reports (2009–2017)

Chart by VCBeat · VBInsight

We have visualized the above data in charts:

Figure 2.2 Aier Eye Hospital's Historical Financial Data

Data source: Aier Eye Hospital Annual Reports from 2009 to 2017

Chart by VCBeat · VBInsight

1. Operating Revenue: Increased from RMB 606.54 million in 2009 to RMB 5.96284 billion in 2017, representing a nearly tenfold growth. The company has maintained robust long-term growth, with a CAGR of 28.9%.

2. Net Profit: From 2009 to 2017, net profit grew from RMB 123.4 million to RMB 1.11126 billion, an increase of nearly eightfold, maintaining high-speed growth over the long term with a CAGR of 26%.

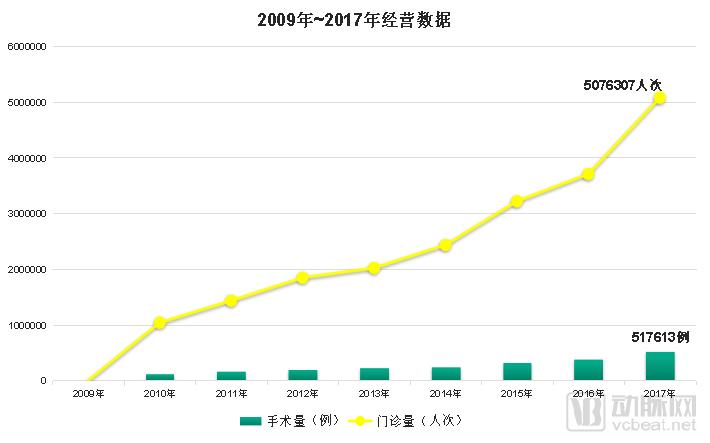

Figure 2.3 Aier Eye Hospital's Historical Financial Data

Data Source: Aier Eye Hospital Annual Reports (2009–2017)

Chart by VCBeat · VBInsight

1. Outpatient Volume: From 2010 to 2017, the number of outpatient visits increased from 1,036,397 to 5,076,307, representing a nearly fivefold increase. The volume maintained rapid long-term growth, with a CAGR of 21.9%.

2. Surgical Volume: From 2010 to 2017, the number of surgical procedures increased from 122,033 to 517,613, representing a 4.2-fold increase. The sector maintained robust long-term growth, with a CAGR of 19.9%.

2.2 Strong Momentum in Three Core Businesses, Favorable Market Prospects

Aier Eye Hospital’s core businesses include excimer laser surgery, cataract surgery, and optometry services. This report collects relevant data on each business segment and other industry information to forecast the revenues of these three core businesses in 2020.

2.2.1 Excimer Laser Surgery-Related Revenue to Reach RMB 5.23 Billion in the Future

Figure 2.4 Forecast of Excimer Laser Surgery Projects

Data source: Aier Eye Hospital 2017 Annual Report, public information

VCBeat · VCBeat Chart

1. Currently, the average unit price for Aier Eye Hospital’s excimer laser procedures is RMB 15,000 per pair of eyes. Based on revenue data from excimer laser surgery alone, Aier Eye Hospital performed approximately 128,700 excimer laser surgeries in 2017;

2. In 2016, the number of myopia cases in China was 400 million; based on a 9% growth rate, the projected number of myopia cases in 2020 is 564 million;

3. Based on the estimated market share of Aier Eye Hospital in 2020, the volume of excimer laser surgeries performed by Aier Eye Hospital Group in 2020 was approximately 292,800 cases. It is projected that in 2020, Aier Eye Hospital’s revenue related to excimer laser surgeries will reach RMB 5.23 billion;

2.2.2 Cataract Surgery-Related Revenue May Reach RMB 4.049 Billion in the Future

Figure 2.5 Forecast of Cataract Surgery Projects

Data source: Aier Eye Hospital 2017 Annual Report, public information

Chart by VCBeat · VBInsight

1. Currently, the unit price for cataract surgery at Aier Eye Hospital is approximately RMB 5,400, which is lower than that of public hospitals (RMB 8,200). Based on the revenue data from cataract surgeries alone, we estimate that Aier Eye Hospital performed approximately 262,420 cataract surgeries in 2017.

2. Based on the 2015 Cataract Surgical Rate (CSR), defined as the number of cataract surgeries performed per million population annually, and its growth rate, the CSR in 2020 is projected to reach 5,305 cases;

3. Based on Aier Eye Hospital’s current market share, it is projected that approximately 594,000 patients will undergo cataract surgery at Aier Eye Hospital in 2020;

4. Coupled with the increase in cataract surgery prices, Aier Eye Hospital’s revenue from cataract surgery procedures is projected to reach RMB 4.049 billion in 2020.

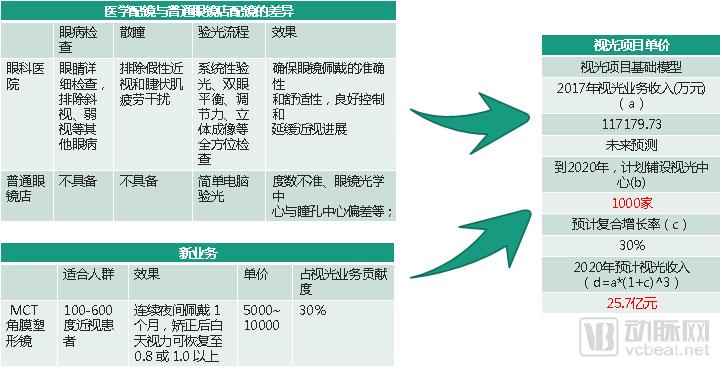

2.2.3 Optometry Services: Related Revenue Expected to Reach RMB 2.57 Billion

Figure 2.6 Optometry Project Forecast

Data source: Aier Eye Hospital 2017 Annual Report, public information

Chart by VCBeat · VBInsight

1. The shift from optometry at optical stores to optometry at hospitals is essentially a demand for consumption upgrading.

2. To penetrate this market segment, Aier Eye Hospital has established numerous optometry clinics within communities, thereby competing directly with eyewear retailers. According to Aier Eye Hospital’s standards for medical optometry, medical optometry is highly likely to rapidly distinguish itself from conventional eyewear dispensing models.

3. According to Aier Eye Hospital’s optometry center expansion plan, the company intended to establish over 1,000 optometry centers nationwide by 2020. With future channel penetration into lower-tier markets and broader access to primary care segments, optometry services are highly likely to become the largest business segment of the Aier Eye Hospital Group.

4. More notably, in the optometry segment, new businesses such as MCT orthokeratology lenses are expected to contribute approximately 30% to the overall optometry business.

5. In 2020, the optometry business is expected to generate RMB 2.57 billion in revenue for Aier Eye Hospital

2.3 Overwhelming Scale: Chain Store Count Far Ahead

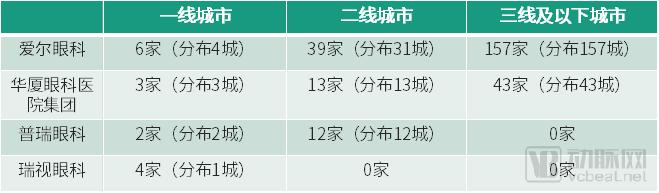

Figure 2.7 Number of Major National Ophthalmic Chain Institutions in China

Source: Public information

Chart by VCBeat · Eggshell Institute

Based on publicly available data, we have compiled the latest statistics on the number of chain branches for major ophthalmic healthcare groups in China. Classified by the number of chain institutions, these groups fall into three tiers. Aier Eye Hospital occupies the first tier, with a combined total of over 200 affiliated hospitals (including both those within and outside its listed entity), far surpassing other ophthalmic chains. The second tier includes ophthalmic chains such as Huaxia Eye Hospital, Purui Eye Hospital, and Airui Sunshine Eye Hospital, each operating more than 10 branches. Among them, Huaxia Eye Hospital ranks at the top of the second tier, second only to Aier Eye Hospital in terms of the number of chain institutions. The third tier comprises numerous ophthalmic medical institutions with fewer than 10 branches, such as Ruishi Eye Hospital.

2.4 Pioneer of the Chain Strategy

Meanwhile, based on the collection of publicly available data, we have compiled the urban outlet distribution of four representative chain ophthalmic institutions at different development stages. In the table, Tier-1 cities refer to Beijing, Shanghai, Guangzhou, and Shenzhen; Tier-2 cities refer to central cities such as municipalities directly under the Central Government and provincial capitals.

Figure 2.8 Distribution of Major National Ophthalmic Chain Institutions in China

Source: Publicly available information

Chart by VCBeat · VBInsight

Based on simple calculations, we know the number of single stores per city for the four ophthalmology chain institutions.

Figure 2.9 Number of Stores per City for Major National Ophthalmology Chain Institutions

Chart by VCBeat · Eggshell Institute

2.4.1 Aier Eye Hospital Adopts a City-Specific Targeted Layout Strategy

Based on the above two sets of data, we believe that, in light of the layout characteristics of individual cities, we can categorize single-city layouts into three types:

Table 2.10 Distribution of Major Ophthalmology Hospitals by City in China

VCBeat Chart by VCBeat

1. City-Specific Strategic Layout: Aier Eye Hospital implements targeted strategies based on the unique characteristics of each city, such as its economic level and other factors.

2. Single-City, Single-Hospital Layout: Huaxia Eye Hospital ignores city-specific characteristics, with one chain hospital per city

3. Multi-hospital layout in a single city: Ruishi Ophthalmology focuses its expansion within one city, deploying four facilities in Shanghai.

2.4.2 Aier Eye Hospital Is at the Forefront of Its Panoramic Strategic Layout

In addition to the aforementioned classification of layout models for medical chain institutions in individual cities, we have collected, organized, and analyzed the outlet networks of selected chain enterprises. Furthermore, by referencing the maturity level of their chain operation models, we have categorized the overall strategic landscape of the entire chain industry into three types:

Figure 2.11 National Panoramic Strategic Layout of Major Ophthalmology Services

Chart by VCBeat · VBInsight

1. Aier Eye Hospital began its development in 2003. Over the past 15 years, it has adopted a strategic deployment that evolved from a regional to a nationwide layout. Currently, Aier Eye Hospital has moved beyond the exploratory phase into a mature stage, with a well-established business model. The company implements a nationwide layout structured in a pyramid distribution pattern, resulting in a significant national brand effect.

2. Regional layout, primarily focusing on key cities within a specific region (a single province or multiple provinces), aiming to establish regional brand influence through this strategic placement. For example, He Shi Eye Hospital concentrated its efforts by establishing seven hospitals in seven cities across the three northeastern provinces of China, thereby achieving a regional layout through these seven facilities.

3. Single-City Layout: Concentrating the establishment of multiple hospitals in a key city to build high market trust within the target city, thereby creating a single-city brand effect. For example, Ruishi Eye Care has established four ophthalmic medical institutions in Shanghai, gaining a certain degree of market recognition in Shanghai’s ophthalmology market.

Apart from Aier Eye Hospital, other ophthalmic enterprises, whether implementing regional or single-city layouts, are only in the initial to exploratory stages of the chain model. Regardless of their current layout strategies, these ophthalmic chain enterprises have yet to achieve a mature form of strategic chain deployment.

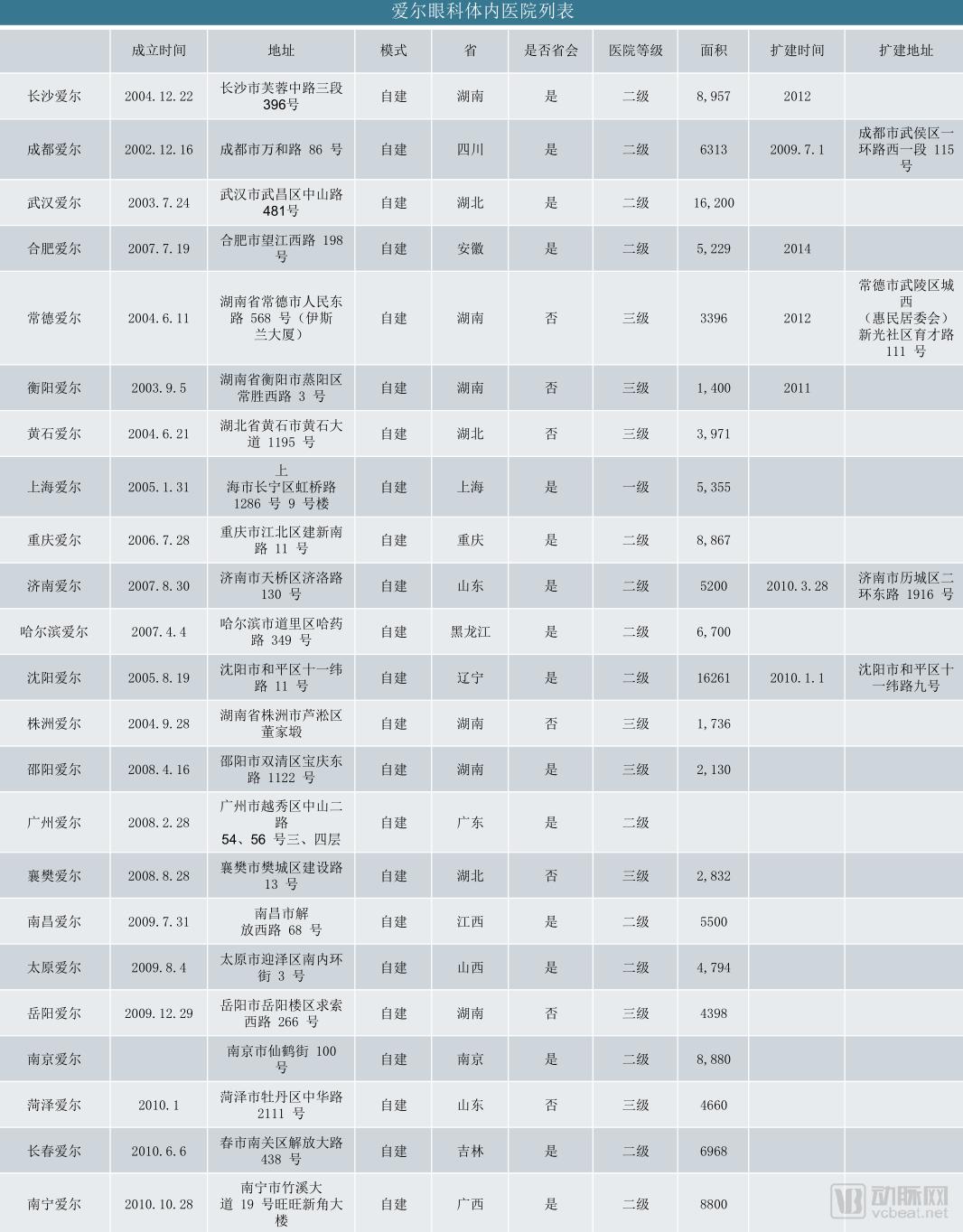

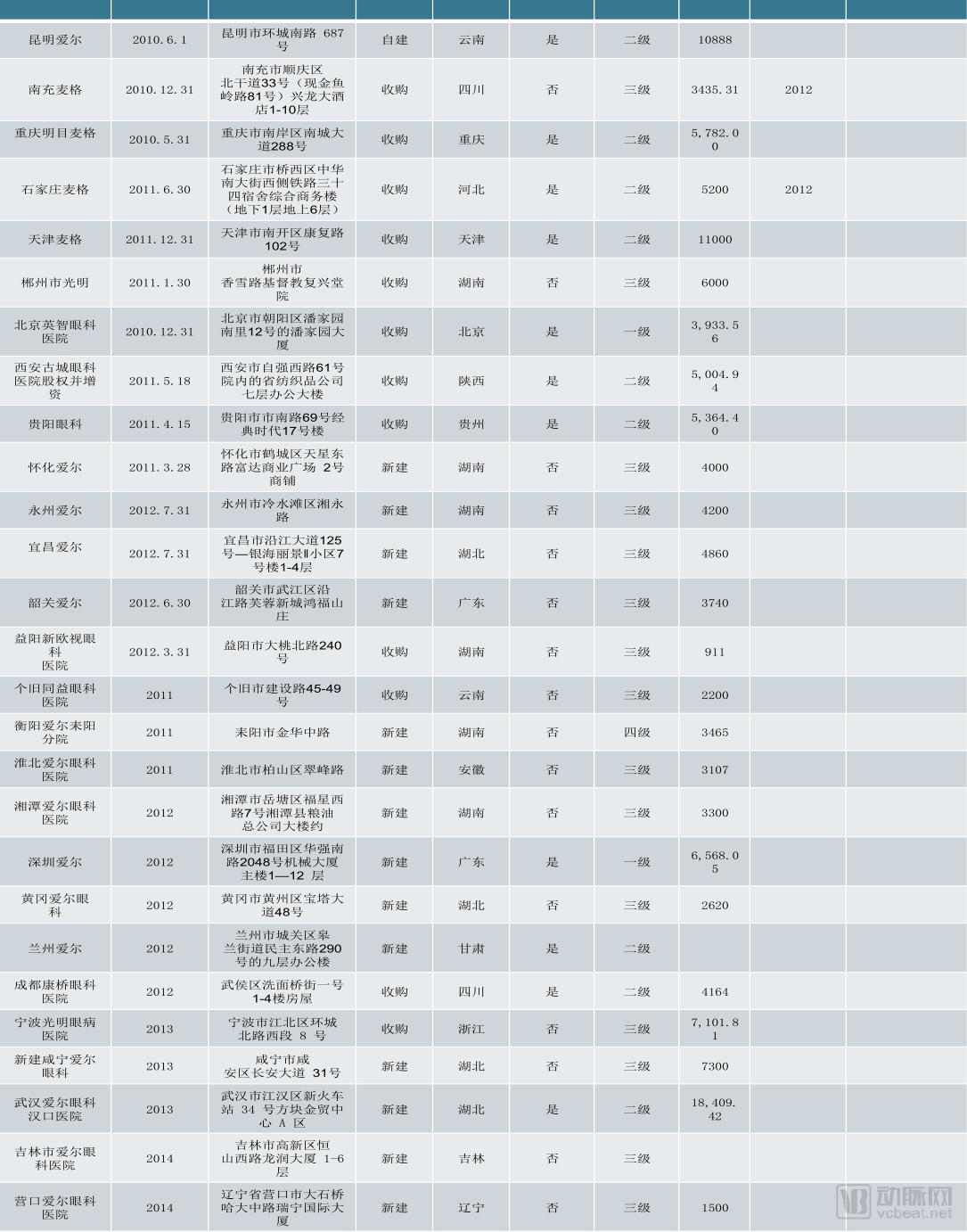

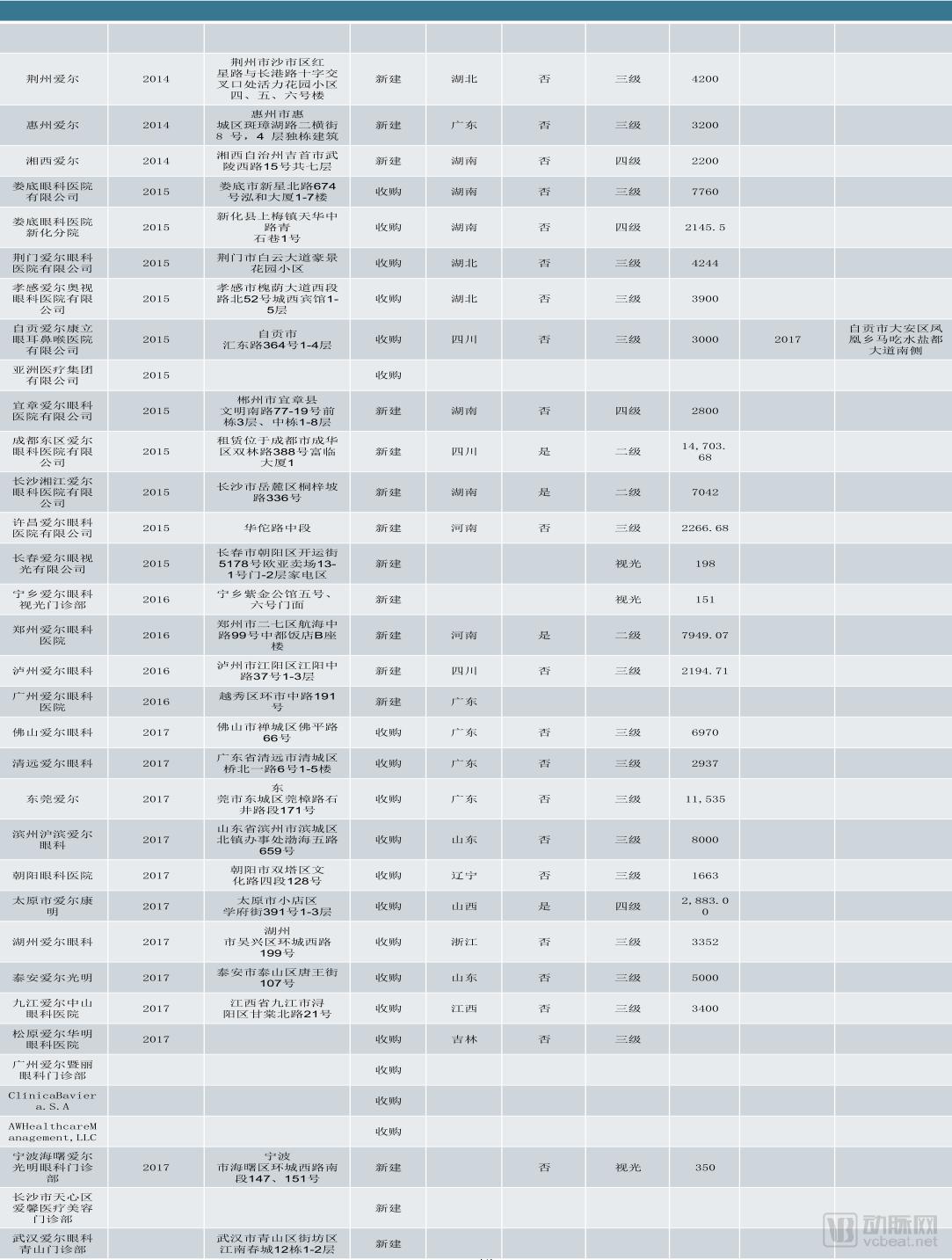

2.5 List of Aier Eye Hospital’s In-House Hospitals

This article specifically compiles information on in-house hospitals from Aier Eye Hospital Group’s prospectus and annual reports from 2009 to 2017. Data are organized across multiple dimensions, including establishment date, location, establishment model, province, hospital classification, floor area, and expansion status, resulting in the following list of hospitals (subsequent analyses and data references are based on this list):

Figure 2.12 List of Hospitals in Aier Eye Hospital's Financial Statements

Source: Prospectus and Annual Reports from 2009 to 2017

VCBeat · VCBeat Chart

Overall, Aier Eye Hospital Group leads the industry in terms of financial performance, number of chain outlets, and strategic layout, making it highly valuable for research on the development of the chain business model.

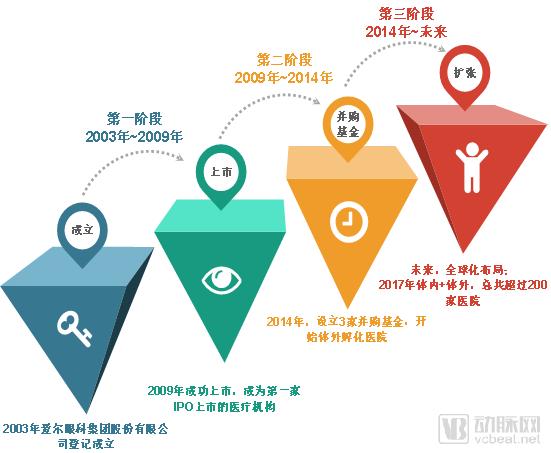

3.1 Three Key Development Stages of Aier Eye Hospital

Based on the maturity of Aier Eye Hospital Group’s chain operation model, we divide the group into three key stages. This paper comprehensively collects data changes across these three stages. Relying on this data, we analyze the variations in key metrics for each stage and provide a multi-faceted interpretation of Aier Eye Hospital’s chain layout model.

Phase I: 2003–2009, Exploration of the Chain Store Model

Phase II: 2009–2013, Chain Model Replication

Phase III: 2014–Present, Maturation of the Chain Model and Rapid Expansion

Figure 3.1 Three-Stage Development Chart of Aier Eye Hospital

VCBeat · VBInsight Chart

This section constitutes the core of this article. We will focus on interpreting the three stages in the development history of Aier Eye Hospital, analyzing changes across these stages in terms of the tiered diagnosis and treatment system, hospital distribution, expansion trajectory, hospital listings, expansion models, hospital characteristics, and revenue structure.

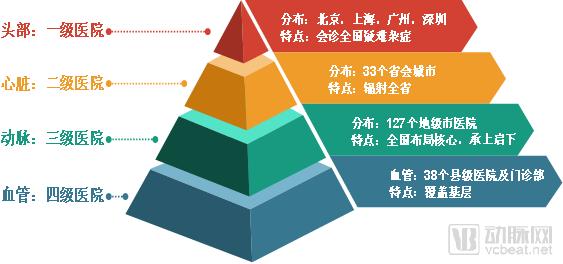

3.2 The Core of Chain Expansion: The Tiered Diagnosis and Treatment System

Since its inception in 2003, Aier Eye Hospital Group has established a tiered diagnosis and treatment system, continuously implementing it in alignment with the Group’s internal development trajectory. The core of this tiered diagnosis and treatment system comprises two key aspects:

1. Comprehensive support from higher-level hospitals to lower-level hospitals: technical support, management support, operational support, etc.;

2. Tiered Referrals from Lower-Level to Higher-Level Hospitals: Critical Care Transfers, Information Feedback, etc.

From 2003 to 2014, Aier Eye Hospital Group underwent a process of exploring and replicating its chain model, primarily implementing a three-tier hospital network layout. Starting in 2014, with its chain model matured, Aier Eye Hospital Group entered a phase of rapid replication and expansion to further increase market share, initiating the deployment of a fourth-tier hospital network on top of the existing three-tier structure.

Figure 3.2 Schematic Diagram of Aier Eye Hospital’s Tiered Diagnosis and Treatment System

VCBeat · VBInsight Chart

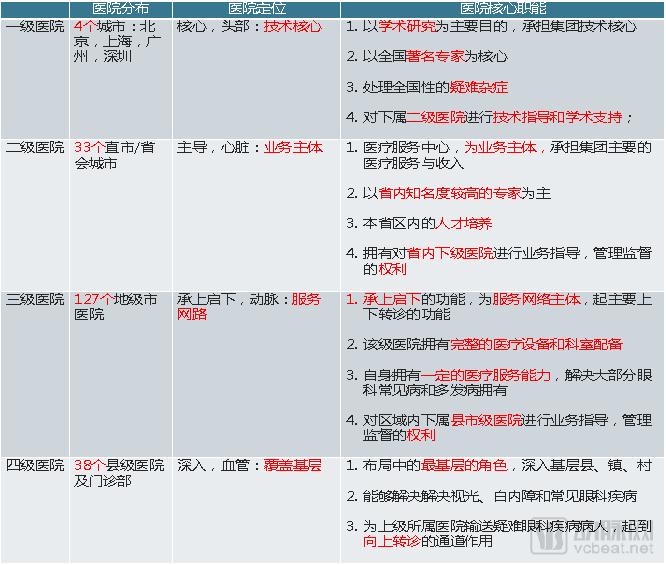

Based on Aier Eye Hospital's tiered diagnosis and treatment system, we have outlined the roles played by hospitals at each level within this framework:

Figure 3.3 Interpretation of Aier Eye Hospital's Tiered Diagnosis and Treatment System

Chart by VCBeat · Eggshell Institute

3.3 Hospital Distribution: Centered on the Two Lakes Region, Radiating Across China

3.3.1 National Distribution: Most Prevalent in Third-Tier Cities; Highest Concentration in Central and East China

Figure 3.4 National Distribution of Aier Eye Hospital

Data source: Haitong Securities

Chart by VCBeat · Eggshell Research Institute

Data shows that Aier Eye Hospital currently has more than 200 chain locations.

Categorized by city tier: Hospitals in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen focus primarily on scientific research, with the smallest number totaling only six; hospitals in second-tier cities serve as the core of each province, municipality, and autonomous region, undertaking the main business operations, with a total of 39; hospitals in third-tier cities constitute the main body of the group’s chain network layout, having the largest number, with a combined total of 157 in-house and outsourced facilities.

By region: Nearly half of the chain outlets are located in Central and East China, with those in Central China primarily concentrated in the Hunan-Hubei region.

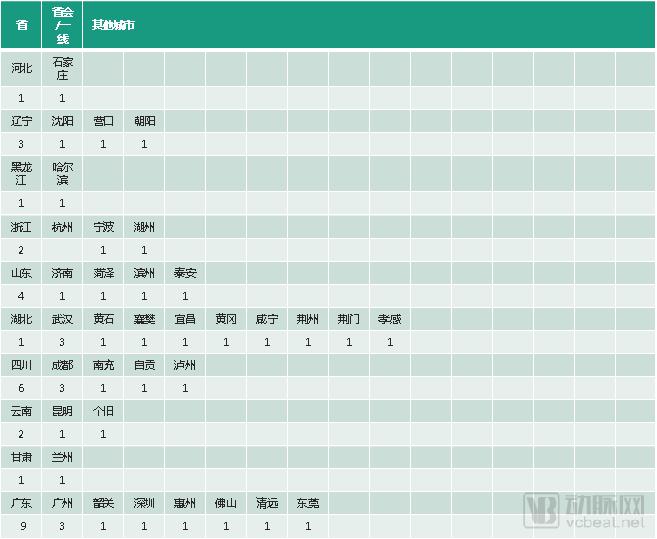

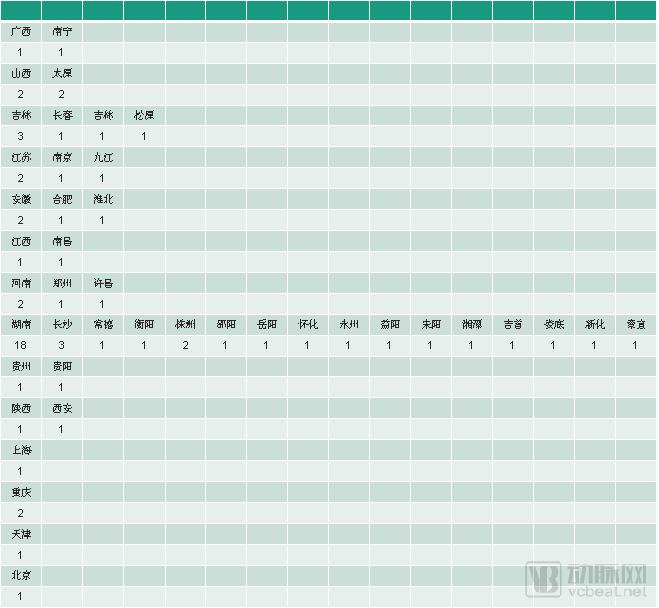

3.3.2 Distribution of In-Hospital Deployments: Multiple Installations per City in Single Urban Areas; Highest Number of Hospitals in the Two Lake Region and Guangdong

We have compiled the current distribution of hospitals within Aier Eye Hospital Group from annual reports and public data:

Figure 3.5 Distribution of Aier Eye Hospital’s In-Country Hospitals by City

Data Source: VCBeat · Eggshell Research Institute

Chart by VCBeat · VBInsight

From the perspective of Aier Eye Hospital’s single-city layout, excluding Zhuzhou, all cities with more than one eye hospital are provincial capitals or central cities, which correspond to Tier-2 hospitals. In these cities, a single hospital per city is no longer sufficient to meet business demands, indirectly demonstrating that Tier-2 hospitals constitute the core revenue driver in Aier Eye Hospital’s four-tier strategic layout. Apart from these provincial capitals and central cities, nearly all other cities have only one hospital.

Figure 3.6 Distribution of Aier Eye Hospital’s Domestic Hospitals by Province

Data source: VCBeat · Eggshell Research Institute

Chart by VCBeat · Eggshell Research Institute

3.4 Expansion Pathway: From “Single-Wheel” to “Dual-Wheel” Drive, with In Vitro Diagnostics as the Future Core

From the perspective of Aier Eye Hospital’s provincial distribution, Hunan, Hubei, and Guangdong have the largest number of hospitals. As the starting point and core demonstration region for Aier Eye Hospital’s strategic layout, the “Two Lakes” region (Hunan and Hubei) has served as a model for expansion into other areas. Based on an analysis of Aier Eye Hospital’s business model (detailed later in this report), this report concludes that the company’s expansion trajectory has followed a spiral pattern, radiating outward from the Two Lakes region to neighboring provinces and eventually across China. Guangdong Province aligns with Aier Eye Hospital’s development trajectory; furthermore, given that Guangdong’s GDP ranks among the highest nationwide, the number of Aier Eye Hospitals there is second only to that in the Two Lakes region.

Figure 3.7 Number of Aier Eye Hospital’s In-House and Outsourced Hospitals

Data Source: Public Information

VCBeat · VCBeat Research Chart

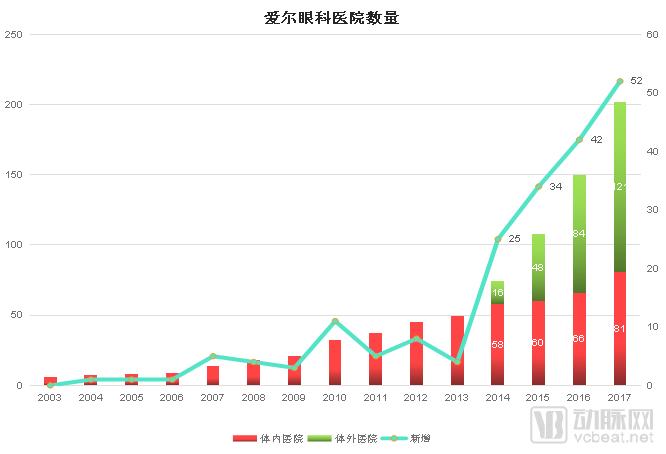

Figure 3.8 Number and Growth of Aier Eye Hospital Branches

Data Source: Public Information

VCBeat · VCBeat Research Institute Chart

Data shows that from 2003 to 2009, as the first phase of Aier Eye Hospital Group’s chain strategy layout, the overall expansion pace was relatively slow. In particular, before 2007, the group was in the initial stage of exploring its chain model, with an expansion rate of one hospital per year. After 2007, the exploration of the chain model entered an advanced stage, and the expansion pace accelerated significantly to align with future IPO plans.

From 2009 to 2014, Aier Eye Hospital Group continuously explored its chain operation model. Following its successful listing on the ChiNext board, the company saw a significant enhancement in both capital and brand effects, marking its entry into the second phase of strategic layout. Since 2010, backed by sufficient funding and leveraging favorable timing, geographic advantages, and human resources, Aier Eye Hospital accelerated its pace into the stage of replicating its chain operation model.

Due to Aier Eye Hospital’s years of operation, the group has maintained rapid revenue growth annually. The existing simple model of greenfield investments and acquisitions can no longer meet Aier Eye Hospital’s expansion needs. Furthermore, in light of the China Securities Regulatory Commission’s requirements for information disclosure by listed companies, Aier Eye Hospital Group adopted an off-balance-sheet M&A fund model for expansion starting in 2014, marking its third phase of development. This off-balance-sheet M&A fund model will become the core of Aier Eye Hospital Group’s strategic expansion in the future.

The expansion model via off-balance-sheet M&A funds not only effectively mitigates adverse financial impacts but also significantly accelerates the company’s growth rate. Currently, Aier Eye Hospital Group participates in seven M&A funds, namely: Shenzhen Qianhai Oriental Aier Medical Industry M&A Partnership Enterprise, Beijing Huatai Ruilian M&A Fund Center, Hunan Aier Zhongyu Ophthalmic Medical Industry M&A Investment Fund, Huatai Ruilian Phase II Industrial M&A Fund, Nanjing Aier Anxing Ophthalmic Medical Industry Investment Center, Hunan Liangshi Bank of Communications Ophthalmic Medical Partnership Enterprise, and Hunan Liangshi Changsha Bank Medical Industry Investment Fund Partnership Enterprise.

Since 2014, Aier Eye Hospital has gradually increased its investment in the M&A fund model, raising the shareholding ratio of a single fund from no more than 10% in the early-stage four-tier funds to nearly 20% in later three-fund structures.

Based on the collected and organized information regarding Aier Eye Hospital Group’s expansion model through off-balance-sheet M&A funds, we believe that:

a. Aier Eye Hospital has invested nearly RMB 1.2 billion, leveraging over RMB 16 billion

b. Among all merger and acquisition (M&A) funds, Aier Eye Hospital merely assumes the role of a Limited Partner (LP). This strategic positioning circumvents the deficiencies in Aier Eye Hospital Group’s own capital operations, avoids involvement in the core management of the funds, and delegates all capital operations of the funds to professional investment management firms.

c. In M&A funds, the general partner (GP) leverages its advantages in capital operations to achieve rapid expansion, with a growth rate far exceeding that of the traditional model combining organic growth and mergers and acquisitions.

d. After acquiring or establishing new hospitals, the M&A fund operates them externally through the incubation period, gradually introducing standardized training and processes aligned with those of the Aier Eye Hospital Group into the operations of these off-balance-sheet hospitals.

e. After the off-site hospitals achieve initial profitability, they will be acquired by Aier Eye Hospital Group and gradually injected into the listed company’s system in batches from the M&A fund.

f. This model can meet the China Securities Regulatory Commission’s requirements for information disclosure by listed companies, thereby avoiding the adverse impact on annual report disclosures caused by poor financial performance during the incubation period of newly established or acquired hospitals, while ensuring compliance.

g. During the period of adopting the traditional expansion model, the stock price rose from a high of RMB 3.88 on its listing day in 2009 to around RMB 6.3 in 2014, representing an increase of less than onefold. However, after shifting to the merger and acquisition (M&A) fund model, the stock price climbed from approximately RMB 6.3 per share in 2014 to the current RMB 32.2 per share, a fivefold increase, despite experiencing significant market volatility.

h. At the time of integration into the listed company’s system, the target hospitals were only marginally profitable; post-integration, they are expected to continue achieving rapid growth within the Aier Eye Hospital Group’s operational framework.

Since 2014, external expansion has become the core strategy of the group’s growth. The number of hospitals surged from 49 before 2014 to over 200 in 2017, representing an overall expansion rate increase of more than 500%. The rapid expansion driven by merger and acquisition (M&A) funds is not merely a significant increase in quantity; as more off-balance-sheet hospitals under these funds are integrated into the listed company’s system, the performance growth contributed by these hospitals will become increasingly pronounced. Under this model, the value of Aier Eye Hospital will increase substantially.

3.5 Shift in Expansion Model: Tiered Spiral Expansion, Accelerating from Slow to Fast

This article outlines three distinct expansion models of Aier Eye Hospital at different stages, based on the analysis of data from the hospital list in the previous section and combined with other relevant information mentioned earlier:

Figure 3.8 Interpretation of Aier Eye Hospital's Three-Stage Expansion Model

Data source: VCBeat · Eggshell Research Institute

VCBeat · VCBeat Chart

Based on the above data summary, we have identified changes in expansion models from Phase I to Phase III:

1. Core Strategy Changes:

(1) Starting from the Hunan-Hubei region, continuously refine the business model in this area, replicate its success, and expand steadily into surrounding regions.

(2) Changsha/Wuhan → Two Lakes Region → Central/Provincial Capital Cities (Tier 1 and Tier 2 Hospitals) → Major Prefecture-Level Cities Nationwide (Tier 3 Hospitals) → Grassroots Layout (Tier 4)

(3) The list of in-house hospitals included in the 2017 report sufficiently demonstrates Aier Eye Hospital’s expansion progress.

2. Shift in Expansion Logic:

(1) Early Stage: Expansion primarily relied on self-funded, in-house construction → Initial IPO Stage: Utilization of raised capital alongside internal funds for expansion, with the strategic logic shifting from purely in-house construction to a combination of in-house construction and M&A → Rapid Deployment Stage: Expansion fueled by internal funds and capital raised through follow-on offerings. Driven by the need for accelerated expansion, the strategy evolved into in-house construction complemented by acquisitions via multiple off-balance-sheet industrial funds (with acquisitions through industrial funds becoming the dominant model).

3. Change in dilation rate:

(1) The expansion rate is significantly adjusted according to different periods

(2) Average expansion of 2.5 stores/year → Average expansion of 7 stores/year→Average Expansion of 38 Stores/Year

4. Changes in the Classification of Key Hospital Layouts:

(1) Secondary/Primary Hospitals → Secondary/Tertiary Hospitals → Tertiary/Quaternary Hospitals

5. Changes in the Main Radiation Range:

(1) Major Hunan-Hubei Region → Surrounding Provinces and Cities → China

3.6 Phased Shifts in the Types of Hospitals Undergoing Major Expansion: Maturity Determines Hospital Characteristics

Throughout these three phases, Aier Eye Hospital Group will prioritize either greenfield development or mergers and acquisitions (M&A) of different types of hospitals, depending on the maturity of its chain operation model. In the first phase, expansion is primarily driven by self-built hospitals. In the second phase, newly constructed hospitals remain the main vehicle for expansion, although their characteristics evolve. In the third phase, expansion is predominantly achieved through the acquisition of existing hospitals.

Regarding the different types of hospital expansions across these three phases, this paper categorizes them as follows: hospitals already in operation prior to the initial public offering (IPO) in Phase I, self-built hospitals established after the IPO in Phase II, and hospitals acquired through mergers and acquisitions (M&A) after the IPO in Phase III. We collected data from Aier Eye Hospital’s annual reports between 2009 and 2017, including revenue figures for the top ten hospitals and information on significant contracts during the reporting periods, to summarize the key characteristics of these three types of hospitals across the three phases:

Figure 3.9 Interpretation of Hospital Types Across Aier Eye Hospital’s Three Major Development Stages

Data sources: Public information, VCBeat·VCBeat Research Institute

Chart by VCBeat · Eggshell Research Institute

By analyzing hospital types, we compare the distinct characteristics of these three categories of hospitals:

Figure 3.10 Comparison of Aier Eye Hospital Across Its Three Major Development Stages

Data sources: public information, VCBeat · VBInsight

Chart by VCBeat · VBInsight

Our conclusion is:

1. Number of Hospitals: Post-IPO M&A Hospitals > Post-IPO Self-Built Hospitals > Pre-IPO Existing Hospitals

2. Average Hospital Area: Pre-IPO Existing Hospitals > Post-IPO Self-Built Hospitals > Post-IPO M&A Hospitals

3. Maturity: Hospitals acquired post-IPO = Hospitals existing pre-IPO > Hospitals self-built post-IPO

4. Scale (Area and Revenue): Hospitals existing before the IPO > Self-built hospitals after the IPO > Acquired hospitals after the IPO

5. Profitability: Hospitals existing before the IPO > Hospitals acquired after the IPO > Hospitals built in-house after the IPO

6. Growth Rate: Self-built Hospitals Post-IPO > Acquired Hospitals Post-IPO > Existing Hospitals Pre-IPO

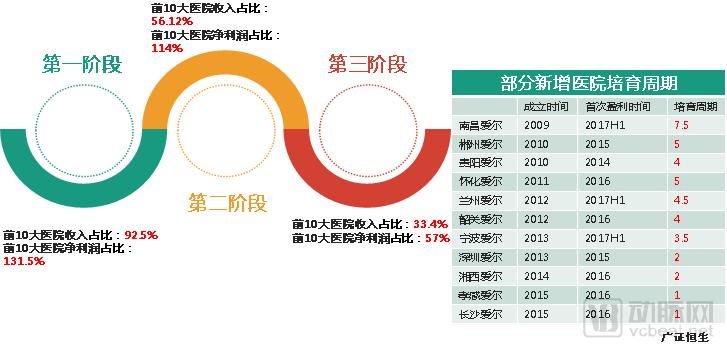

3.7 Revenue Structure Adjustment: Maturity Determines Changes in Revenue Structure

This article compiles data on the revenue and net profit shares of the top ten hospitals across three phases, as well as data on newly built hospitals, and conducts an organized analysis of the data.

Figure 3.11 Revenue Structure of Aier Eye Hospital Across Three Major Phases

Data Source: Guangzheng Hengsheng, VCBeat · Eggshell Research Institute

VCBeat · VCBeat Institute Chart

We believe that the primary revenue drivers of Aier Eye Hospital Group have shifted from its top ten hospitals to a broader base where the majority of hospitals within the group are collectively profitable. Furthermore, the significantly shortened ramp-up period marks the increasing maturity of its chain operation model.

1. Phase I (2003–2009): Insufficient data during the incubation period; the primary profit contributors were the top ten core hospitals. Revenue and net profit were basically derived from these top ten core hospitals, while hospitals outside the top ten consistently reported negative net profits, mainly because most of them were in the early incubation stage.

2. Phase II (2009–2014): With a cultivation period of 3–5 years, the primary profit generators were the ten core hospitals. Revenue and net profit were largely derived from these ten core hospitals, while most of the non-top-ten hospitals reported negative net profits. During this period, the proportion of revenue and net profit contributed by the ten core hospitals continued to decline, as some mature hospitals underwent secondary expansion.

3. Phase III (post-2014): With a cultivation period of 1–2 years, the primary profit generators are the ten core hospitals and non-core hospitals. Both revenue and net profit are derived from these core and non-core hospitals. The proportion of revenue and net profit contributed by the ten core hospitals has been declining at an accelerating rate. Some mature hospitals have undergone secondary expansion, while previously cultivated hospitals have begun to contribute back to the listed company, resulting in a rapid increase in their share of revenue and net profit.

3.8 Chapter Summary: A Mature Model, Paving the Way for the Future

This section integrates all the aforementioned dimensions and summarizes the key core elements involved in each of the three developmental stages of Aier Eye Hospital. We categorize the key core elements of each stage into four aspects, summarizing the distinct changes brought about by the strategic layout at each stage, and interpret the four key core elements for each phase using charts and graphs.

Figure 3.12 Summary of Core Elements in the Three Major Phases of Aier Eye Hospital

Data Source: VCBeat · Eggshell Research Institute

VCBeat · VCBeat Institute Chart

Based on the three-stage changes shown in the table above, we can conclude that the evolution path of core elements across different stages is as follows:

1. Maturity: Model Exploration → Model Replication → Full Model Maturity

2. Hospital Development Model: Primarily organic in-house development → In-house development supplemented by M&A → Primarily M&A driven by industrial funds

3. Revenue Structure: Core Hospitals → Non-Core Hospitals

4. Network: Implement a three-tier network layout → Improve the three-tier network layout → Implement a four-tier network layout

4.1 Management Structure: Efficient Internal Hierarchical Management System

The transition of Aier Eye Hospital Group’s chain model from an exploratory phase to a mature stage is accompanied not only by the expansion of its hospital network but also signifies the maturation of its internal tiered management system. We analyze Aier Eye Hospital Group’s internal tiered management system across three levels.

4.1.1 Group Decision-Making Level (Central):

(1) Based on the Group’s overall strategic planning, appropriately delegate authority for certain non-core investments and management decisions while maintaining macro-level coordination and oversight.

(2) At the group level, establish department-specific academic committees and department-specific marketing departments:

a. Establish academic committees for each department to uniformly manage and supervise the technology, quality, and talent development of all ophthalmology-related departments.

b. Establish market operation departments based on clinical specialties, and manage and integrate the Group’s diverse resources across the national market from the perspective of a nationwide strategic layout.

4.1.2 Intermediate-Level Supervision and Implementation Tier (Provincial Level):

(1) Strictly implement the Group’s delegation of authority and assignment of tasks to each province in accordance with its strategic layout.

(2) Possess the authority to supervise and manage hospitals of all levels within subordinate provinces.

4.1.3 Grassroots Operational Level (Hospitals at All Levels):

(1) Implement a dual-leadership system with separate roles for the CEO and the Hospital Director, ensuring that professionals handle their respective areas of expertise:

a. CEO: Daily operations, marketing, and administrative management

b. Hospital Director: Responsible for overseeing all matters related to medical practices and their implementation.

The remainder of Chapter 4 will focus on analyzing the internal management under Aier Eye Hospital’s tiered management system. We believe that well-aligned internal management is crucial to the strategic layout of chain enterprises, and we hope our analysis can provide references for corporate internal management.

Chapter 5: Based on the preceding analysis, we will summarize a standardized model for the expansion of Aier Eye Hospital’s chain operation and provide reference benchmarks for other chain enterprises through key standardization replication indicators of Aier Eye Hospital.

Chapter 6: A Brief Analysis of Other Ophthalmic Chain Cases, Highlighting Why Aier Eye Hospital Stands as a Benchmark Enterprise in Exploring the Chain Model.

Finally, we will present the 11 core insights that constitute the essence of this article. These insights offer valuable reference points for chain enterprises in formulating their strategic layouts.

Below is the complete table of contents. The full report comprises seven chapters and 58 pages. To read Chapters 4, 5, 6, and 7, please scan the QR code to become a VCBeat member and download the complete report, or purchase the report individually in the VCBeat Reports section.

I. Aier Eye Hospital: The Most Mature Strategic Layout, Leading the Way Among Chain Enterprises

1.1 Introduction to Aier Eye Hospital

1.2 Operational Performance

1.3 Chain Scale

1.4 Technical Strength

1.5 Market Capitalization

II. Operations and Data: Industry Unicorn

2.1 Outstanding Financial Performance: Geometric Growth in Operating Revenue and Outpatient Visits

2.2 Focusing on Three Core Businesses with Promising Market Prospects

2.3 Overwhelming Scale: Chain Store Count Far Ahead

2.4 Pioneer of the Chain Strategy

2.5 List of Hospitals in Aier Eye Hospital’s Financial Statements

III. A Self-Portrait of a Chain Network Spanning Over 200 Hospitals

3.1 Three Key Development Stages of Aier Eye Hospital

3.2 The Core of Chain Expansion: The Tiered Diagnosis and Treatment System

3.3 Hospital Distribution: Centered on the Two Lakes Region, Radiating Across China

3.4 Expansion Pathway: From “Single-Wheel” to “Dual-Wheel” Drive, with Out-of-Hospital M&A as the Future Core

3.5 Change in Expansion Pattern: Tiered Spiral Expansion, Accelerating from Slow to Fast

3.6 Phased Shifts in the Primary Types of Expanding Hospitals: Maturity Determines Hospital Characteristics

3.7 Adjustment of Revenue Structure: Maturity Determines Changes in Revenue Structure

3.8 Chapter Summary: Mature Models, Unlocking Future Paradigms

IV. Internal Management: An Indispensable Component of Strategic Layout

4.1 Management Structure: Efficient Internal Hierarchical Management System

4.2 Personnel Structure Changes Along with the Shift in Expansion Model

4.3 Incentive Policies Yield Significant Results

V. Single-Store Standardization Model: Introducing Standardization Based on the Model

VI. Brief Analysis of Cases Related to Ophthalmology Chains

6.1 Huaxia Eye Hospital Group

6.2 C-MER Eye Care

6.3 Aier Eye Hospital Group

7、11 Core Perspectives on the Chain Store Model