2018 Tumor Genomic Testing Market Research Report

Source: Jingzhun Research Institute

Author: Liu Jiaying

With the rapid advancement of gene sequencing technology, China’s genetic testing industry peaked in 2015, leading to intensified market competition and a gradual expansion in the scope of genetic testing applications. Currently, BGI Genomics and Berry Genomics have relied on reproductive health genetic testing services, such as non-invasive prenatal screening (NIPS), to go public in 2017 and become leading companies in this niche sector. However, the market landscape in the field of oncology genetic testing remains unstable.

With approximately 4 million new cancer cases annually in China, the market prospects and potential market size for tumor genetic testing are larger than those of the non-invasive prenatal testing (hereinafter referred to as NIPT) market, considering comprehensive factors such as disease complexity and patient needs. It is foreseeable that more leading companies will emerge in this field, where market competition is also intense.

Drawing on the trajectory of the NIPT market as it evolved from disorder to standardization, the oncology genetic testing market is poised for consolidation over the next one to two years. This shift will be driven by the launch of innovative oncology drugs such as PD-1 inhibitors and the regulatory approval of NGS-based high-throughput kits for tumor diagnosis, which will also raise market entry barriers. In light of this, we intend to address the following issues in this report:

(1) Who are the main competitors in the current tumor genetic testing market, and what are their respective market positions?

(2) In the field of oncology genetic testing, what constitutes a company’s core competitiveness? Which companies are able to secure leading market positions by leveraging their core competencies?

(3) What are the current business models of tumor genetic testing companies? Amidst the ongoing market consolidation, which business models are poised to achieve profitability?

(4) What are the future development trends in the oncology genetic testing industry? Beyond the continued expansion of the companion diagnostics market, when will opportunities in cancer early screening emerge?

Similar to the overall technological foundation of the genetic testing industry, the development of tumor genetic testing relies on the widespread adoption of detection technologies such as next-generation sequencing (NGS). Meanwhile, advancements in tumor liquid biopsy technologies, represented by circulating tumor DNA (ctDNA) testing, have further laid the groundwork for the application of genetic testing in the clinical diagnosis of cancer.

1.1 Genetic Testing Technology

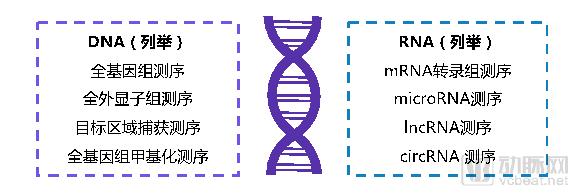

Basic Technology Classification:Genetic testing broadly refers to a suite of technologies that detect chromosomes, DNA, or RNA molecules in body fluids, tissues, cells, or cellular secretions. PCR technology based on nucleic acid amplification, FISH technology based on fluorescent hybridization detection, gene chip technology, and gene sequencing technology collectively form the foundation of genetic testing techniques. The Human Genome Project, launched in 1990, drove the popularization and advancement of sequencing technologies. By around 2014–2015, next-generation high-throughput sequencing (NGS) rapidly reduced the cost of gene sequencing, bringing the cost of individual whole-genome sequencing down to approximately $1,000. Consequently, the clinical application prospects of genetic testing in oncology have become increasingly clear.

Classification by Test Subject:Currently, when classified by specific detection targets and objectives, the genetic testing services offered by most companies can be divided into DNA sequencing and RNA sequencing. DNA serves as the carrier of genetic information, while RNA facilitates the expression of genetic information in proteins. Relatively mature genetic testing methods related to tumor diseases include the detection of DNA molecular gene mutations, insertions, deletions, fusions, and copy number variations. In addition, DNA methylation is also one of the technological research and development directions for many companies. DNA methylation can lead to the silencing and inactivation of gene expression. Methylation changes at specific genes and loci have been proven to be associated with the occurrence of certain tumors. Theoretically, this method can be used for early screening and diagnosis of tumors; however, such detection methods are still in the development stage and require further research and validation.

1.2 Liquid Biopsy Technology

Classification by Detection Target:Tumor liquid biopsy broadly refers to the detection of DNA or RNA in body fluids such as blood, urine, and cerebrospinal fluid to provide information for clinical disease diagnosis. Based on the analytes detected, tumor liquid biopsy can be categorized into circulating tumor cell (CTC) detection, circulating tumor DNA (ctDNA) detection, and exosome detection.

ctDNA refers to DNA fragments derived from tumor cells circulating in peripheral blood. By detecting and analyzing these fragments, tumors can be identified at an earlier stage, before they grow large enough to be visually detected. This technology is currently highly mature and widely applied, primarily for monitoring the progression and evolution of tumorous diseases within the human body.

CTCs are viable cells released from tumor tissues into the bloodstream, capable of providing more comprehensive genomic information on tumor cells; however, the sensitivity and specificity of detection technologies

Breakthrough progress is still pending. Exosomes, which can provide more information on RNA and proteins, also await further research.

Advantages and Limitations:Classical tumor diagnostic techniques include tissue biopsy, imaging tests, and others. These detection methods lack the ability to identify early-stage, non-visible tumors. Meanwhile, tissue biopsy methods such as surgical biopsy and needle biopsy are invasive procedures that place high demands on patients' physical condition; some patients are even unable to undergo surgical biopsy. Studies have shown that CTCs and ctDNA may already appear in the blood of early-stage patients before imaging tests reveal obvious signs of tumor development.

Therefore, compared with classical tumor diagnostic techniques, liquid biopsy for tumors can, on the one hand, detect the presence of tumors at an earlier stage. On the other hand, it requires only a small amount of blood or the extraction of body fluids and secretions from patients, thereby reducing sampling discomfort, enabling repeated sampling, and facilitating dynamic monitoring of disease progression. However, this technology also has limitations; its detection accuracy is constrained by tumor type and anatomical location. In other words, not all types of tumors can be accurately detected via liquid biopsy, and the methodology still requires further refinement.

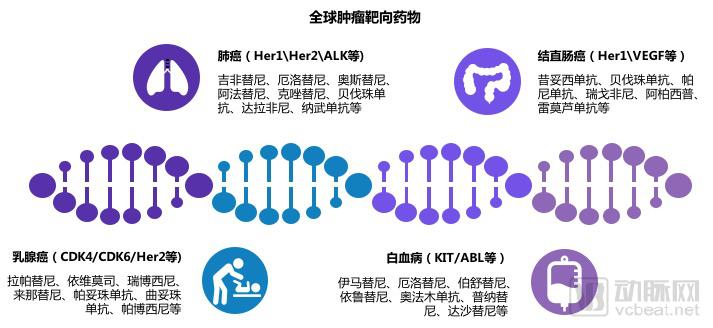

The application of genetic testing in oncology can, in theory, span the entire cancer care continuum, including risk prediction, early screening, molecular subtyping, treatment guidance, and prognosis monitoring. Currently, the most rapidly implemented applications are primarily in tumor molecular subtyping, treatment guidance, and prognosis monitoring. Genetic testing plays a particularly important role in guiding targeted therapy.

Currently, there are over a hundred oncology targeted therapies approved for marketing worldwide, while only more than 20 have been launched in China, primarily focusing on lung cancer, colorectal cancer, and breast cancer. Blockbuster targeted drugs for ovarian cancer and prostate cancer have been approved within the past year. In addition, many other oncology targeted therapies are under development or pending regulatory approval. In the future, genetic testing may become a routine component of treatment protocols for certain cancer patients.

3.1 Market Size

Approximately 4 million new cancer cases are reported annually in China. When accounting for potential recurrences among existing patients, the absolute number is likely even larger, highlighting the promising market prospects for tumor genetic testing. However, the limited number of targeted cancer therapies currently available in the Chinese market, coupled with the fact that the genetic testing industry is still in its early stages, means that the market potential for tumor genetic testing remains largely untapped. According to Burner Rock Medicine’s self-reported data on hospital-end tumor genetic testing services in 2017, the company generated approximately RMB 200 million in revenue that year, capturing a market share of around 20%–25%. Based on this, the market size for NGS-based tumor genetic testing in China last year can be conservatively estimated at less than RMB 1 billion.

This is far from reaching the market capacity “ceiling” for genetic testing in guiding oncology medication.

In the United States, targeted therapies account for over 50% of medication usage among oncology patients, whereas in China, the current figure is approximately 10%–20%. Given the exponential growth of the oncology genetic testing market in recent years and positive factors such as reforms to the drug approval system by the China Food and Drug Administration (CFDA), it is estimated that around 30% of oncology patients will benefit from genetic testing-guided medication in the future, translating to more than one million tests annually. Considering the common occurrence of drug resistance and recurrence in oncology patients, and assuming each patient undergoes genetic testing twice a year, with product prices ranging from RMB 7,000 to RMB 20,000 (averaging RMB 10,000), the potential market size for oncology genetic testing in medication guidance could reach RMB 10 billion.

As for when market potential will be fully unleashed, it is difficult to achieve in the short term. According to BBC Research statistics, the global gene sequencing market size was $7.9 billion in 2017 and is expected to reach $11.7 billion in 2018, with a compound annual growth rate of approximately 30%. Although zero tariffs on all imported anti-cancer drugs in China took effect on May 1, 2018, which may drive sales growth of anti-cancer medications including targeted tumor therapies, the tumor genetic testing market based on NGS technology may still require more than five years to reach a scale of tens of billions of yuan.

3.2 Market Competition Factors

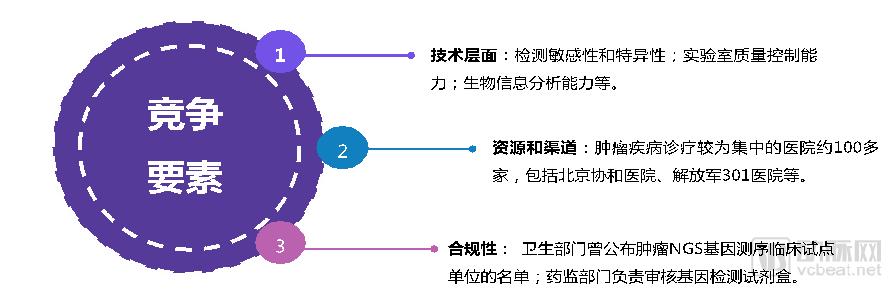

Tumor genetic testing is one of the clinical application areas of genetic testing. Similar to the mature market for non-invasive prenatal screening (NIPS), competition in this sector primarily revolves around technology, resources, distribution channels, and regulatory compliance. However, within the specific field of tumor genetic testing, market entry barriers are higher across these four dimensions due to the complexity and heterogeneity of cancer diseases. As market competition intensifies, companies lacking core competencies will be gradually eliminated.

3.2.1 Technical Level:In the field of oncology genetic testing, the sensitivity and specificity of detection technologies, laboratory quality control capabilities, and bioinformatics analysis capabilities have a decisive impact on the accuracy of test results and their clinical guidance value. This process involves multiple steps, including ctDNA extraction and enrichment, sequencing library construction, and target region capture, each with distinct technical requirements and thresholds. Moreover, oncology genetic testing and liquid biopsy technologies are evolving rapidly; companies that fail to keep pace with the latest trends are easily eliminated from the market. For instance, the currently prominent PD-1/L1 immune checkpoint inhibitors require the assessment of tumor mutational burden (TMB), microsatellite instability-high (MSI-H) status, and other parameters. These requirements impose far greater demands on detection technologies than those for conventional targeted cancer therapies.

3.2.2 Resources and Channels:In addition to robust technical capabilities, the accumulation of scientific research resources and the expansion of clinical channels are also key factors in market competition within the tumor genetic testing sector. As of the end of April 2018, there were a total of 12,596 public hospitals in China, including 2,267 tertiary hospitals. Approximately 100 hospitals, where the diagnosis and treatment of cancer are relatively concentrated—such as Peking Union Medical College Hospital, the PLA General Hospital (301 Hospital), and Peking University Cancer Hospital—absorb the majority of cancer patients in the country. These institutions represent priority targets for scientific research collaboration and clinical promotion channels for companies operating in the tumor genetic testing field.

Therefore, in product design and service workflows, all market competitors must fully understand the research and clinical needs of hospitals and physicians. This includes details such as shortening the turnaround time for test reports, emphasizing the integration of genetic testing data with clinical phenotypes, improving the readability of test reports, and paying attention to communication methods with patients. In the future, as policies promoting tiered diagnosis and treatment and medical consortia advance, some high-volume tertiary hospitals in local regions will have the willingness to offer tumor genetic testing services but lack the corresponding service capabilities; these institutions are likely to become another important frontier in the field of tumor genetic testing. Currently, some companies are attempting to co-establish molecular diagnostic centers with local tertiary hospitals, using these centers as platforms to promote tumor genetic testing services and products.

3.2.3 Compliance:Compliance is another core competitive factor in the field of oncology genetic testing. Currently, regulatory oversight in this sector primarily involves the health authorities and the drug administration departments. As early as 2015, the former National Health and Family Planning Commission issued the "Technical Guidelines for Genetic Testing of Drug-Metabolizing Enzymes and Drug Action Targets (Trial)" and subsequently announced the list of clinical pilot units selected for tumor next-generation sequencing (NGS). Meanwhile, oncology genetic testing kits based on NGS technology and bioinformatics analysis software have always been classified as medical devices, requiring approval from the drug administration authorities before they can be marketed. In particular, such approval directly determines whether a company’s products can obtain government endorsement and access the large-scale hospital market; otherwise, if only the Laboratory Developed Tests (LDT) model is adopted, growth potential will be limited.

3.3 Market Competition Landscape

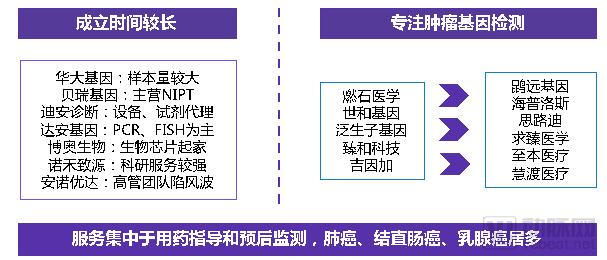

In the current landscape of tumor genetic testing, the main market competitors can be broadly categorized into two groups. The first group consists of relatively “established” genetic testing companies founded earlier, including BGI Genomics, Berry Genomics, Dian Diagnostics, and Daan Gene. Among these, BGI Genomics and Berry Genomics went public in 2017 leveraging their non-invasive prenatal testing (NIPT) businesses. BGI Genomics processes a larger volume of genetic testing samples, while Berry Genomics, in collaboration with the National Liver Cancer Center, launched an early liver cancer screening project, aiming to strengthen its position in early tumor screening. The second group includes companies such as CapitalBio Corporation, Daan Gene, and Novogene, which were generally established around 2000 or 2010. These companies primarily focused on biochips, PCR technology, or scientific research services, and thus do not hold significant competitive advantages in the clinical application of tumor genetic testing.

The second category of market competitors, most of which were established around 2015—the peak period for the development of genetic testing—focused on tumor genetic testing from their inception. A small number of companies were founded before 2010 but also specialized in tumor genetic testing as their core business. Due to their relatively focused business directions, these companies possess technological and professional advantages. Particularly fueled by the venture capital boom, many startups initially invested substantial funds in the research and development of tumor genetic testing technologies and in accumulating sample databases. However, after nearly three years of market competition, a large number of companies have been eliminated, while only a few remain competitive.

Among them, Burning Rock Biotech, established in 2014, and Geneseeq, founded as early as 2008 in Toronto, Canada, currently hold leading market positions. In terms of revenue and market share, the hospital terminal service revenues of Burning Rock Biotech and Geneseeq rank among the top in the tumor genetic testing market dominated by next-generation sequencing (NGS). Furthermore, their NGS-based tumor genetic testing kits have entered the “Special Approval Channel for Innovative Medical Devices,” with expectations to receive regulatory approval and launch in the second half of this year or next year.

Among other companies focused on oncology genetic testing, startups such as Geneseeq, GenePlus, and Fudan-Zhangjiang Biotechnology have grown rapidly. By leveraging scientific research collaborations or sales and marketing efforts, they have quickly accumulated large volumes of sample data, with distribution channels extending to top-tier (Grade A tertiary) hospitals in major cities. Meanwhile, companies like Kunyuan Biotechnology, 3D Medicines, ZhiBen Medical, and HelioGene have also attracted attention from the capital markets due to their unique business models, strong technical capabilities, or the involvement of renowned scientists.

However, the overall landscape of the tumor gene testing market remains unstable. The core business of the vast majority of tumor gene testing companies is concentrated on medication guidance, and product differentiation in this market is not yet significant. It is expected that as high-throughput NGS tumor gene testing kits continue to gain regulatory approval, and more targeted therapies—including PD-1 immune checkpoint inhibitors—are launched, the competitive landscape in this field will become clearer, and corporate competition will shift toward differentiation.

3.4 Characteristics of the Business Model

LDT Model:Currently, in the field of tumor genetic testing, testing institutions only need to obtain appropriate laboratory accreditation to issue test reports using techniques such as PCR and FISH, or to promote approved PCR kits to hospitals. However, the application of NGS in tumor diagnosis and treatment is still in the pilot stage; only pilot units are authorized to issue clinical test reports, and the CFDA has not yet approved any high-throughput NGS kits for tumor diagnosis for market release.

Therefore, in the field of tumor genetic testing, companies primarily based on NGS technology platforms mainly adopt the third-party external testing (LDT) model. They assist physicians in assessing patient conditions and participating in the diagnosis and treatment of cancer patients through scientific research collaborations with clinicians, issuing advisory reports, or establishing joint laboratories with pilot hospitals. This model requires companies to maintain close ties with clinicians, employs promotional strategies similar to those of pharmaceutical sales representatives, and places high demands on the company’s channel control capabilities.

IVD Product Model:Starting in the second half of this year, the China Food and Drug Administration (CFDA) is expected to sequentially approve next-generation sequencing (NGS) kits for tumor diagnosis for market launch. At that time, the in vitro diagnostic (IVD) product model may become the preferred choice for more oncology genetic testing companies. Currently, most of these kit products target a few specific genes, falling within the scope of small-panel genetic testing. This makes them suitable for promotion in hospital pathology departments, facilitating their adoption as routine in-house tests. The advantage of this model lies in the significant boost to corporate revenue once the products are included in hospital procurement lists, provided that the hospitals possess the corresponding testing equipment.

Due to the earlier adoption of PCR technology and its relatively lower cost compared to NGS, PCR-based diagnostic kits currently dominate the IVD market for genetic testing. However, as NGS sequencing costs continue to decline and given its ability to analyze a broader range of genes, NGS-based diagnostic kits for tumor diagnosis are expected to capture a significant share of the in-hospital market. Meanwhile, the LDT model will continue to play a crucial role in large-panel genetic testing services covering hundreds of loci.

4.1 Burning Rock Biotech: Leveraging the Characteristics of the Healthcare Industry to Early Deploy IVD Reagent Products

Establishment Date:March 2014.

Financing Status:In the second half of 2016, it secured RMB 300 million in Series B financing from Sequoia Capital, Lifeline Ventures, CMB International, and Legend Star; in 2015, it raised RMB 150 million in Series A+ financing from Lifeline Ventures, Sequoia Capital, and Legend Star; in 2014, it obtained RMB 40 million in Series A financing from Northern Light Venture Capital and Legend Star.

Team Composition:CEO Han Yusheng, former General Manager of BioTek Instruments in China and Investment Manager at Northern Light Venture Capital; COO Chuai Shaokun, with 13 years of experience in bioinformatics and translational medicine; CMO Liu Hao, who previously led new drug R&D at Novartis and Pfizer. The team consists of approximately 450 members, with significant proportions in the R&D, Medical Affairs, Bioinformatics Analysis, and Marketing departments.

Main Products or Services:

1. Provides over 30 types of genetic testing services based on cancer type, genotype, and other factors, such as the 520-gene large panel test, hereditary tumor susceptibility gene testing, 168-gene testing for lung cancer, and specialized genetic testing for colorectal cancer and lymphoma.

2. The subsidiary’s IVD product, the EGFR/ALK/BRAF/KRAS Gene Mutation Combined Detection Kit (Hybrid Capture Sequencing Method), was granted entry into the CFDA’s Special Approval Channel for Innovative Medical Devices in 2016 and is expected to receive approval in August or September of this year.

Development Model:

1. Strengthen efforts across academic, brand, and marketing dimensions to gain recognition from the academic community and clinicians for product and service quality, while adjusting product and service design strategies based on clinical needs;

2. Prioritize regulatory compliance by being the first to apply for the innovative pathway for IVD products, with a focus on automating bioinformatics analysis to capture the domestic market and demonstrate product quality.

Strategic Direction:

1. Based on the judgment that genetic testing will inevitably shift toward an in-hospital model and greater regulatory compliance, we plan to build a corporate moat through IVD kit products and by enhancing product quality.

2. Participate in drug R&D by domestic enterprises, while maintaining the clinical market as the core business; strategically focus on hospitals with concentrated oncology diagnosis and treatment services to enhance the market penetration of medication guidance services among patients with intermediate- to advanced-stage cancer; meanwhile, prioritize early cancer screening as a key area for technological R&D.

Market Promotion:

1. The service network covers nearly 400 hospitals, with market promotion priorities determined based on hospital size and the volume of oncology diagnosis and treatment;

2. While promoting oncology medication guidance services, provide complimentary patient prognosis monitoring services to obtain continuous sample tracking data for technological R&D;

3. Collaborate with manufacturers of oncology targeted therapies, such as AstraZeneca, to promote companion diagnostic services for their drugs.

Key Data:To date, we have served over 70,000 patients and collected 1,000 samples for early screening R&D. In collaboration with partner hospitals and physicians, we have published nearly 30 SCI-indexed articles in academic journals such as Annals of Oncology, with an average impact factor of approximately 6.4; nearly half of these articles have an impact factor greater than 10. Furthermore, we have undertaken 180 joint research projects with hospitals and physicians.

Advantages and Highlights:

1. First-mover advantage. The company determined early on that genetic testing would shift toward in-house hospital testing, thereby making test kits a strategic focus. In China, medical device approval typically takes more than three years; however, entering the innovative approval pathway can shorten this period to 1.5–2 years. This means that companies securing approval first gain a first-mover advantage, enabling bulk sales of test kits and reducing operational costs.

2. Strategic Advantages. By building on technological stability and product quality, while prioritizing the development of academic influence and brand reputation, the company can solidify the foundation for product promotion and sales—namely, recognition by clinicians and healthcare institutions—thereby ensuring a highly sustainable development model. Furthermore, given the government’s currently ambiguous regulatory stance on large-panel genetic testing services, the approval of small-panel kits helps mitigate risks associated with policy uncertainty.

Challenges and Risks:The tumor gene testing market is fiercely competitive. The company currently ranks among the top tier in this market; however, in addition to competitive pressure from Geneseeq, it faces potential external threats from other rapidly growing companies such as Zhenhe Technology and GenePlus.

4.2 Zhenhe Technology: Addressing Clinical Needs and Conducting Comprehensive Assessments of Oncological Diseases

Date of Establishment:November 2014.

Financing Status:In February 2018, it announced the completion of a C-round financing of RMB 210 million, led by Matrix Partners China and Zenovo Innovation Capital; in February 2017, it announced a B-round financing of RMB 128 million, led by Zenovo Innovation Capital, Kaifeng Venture Capital, and Yahui Precision Medicine Fund; around 2016, it secured an A-round financing of RMB 26 million from Yifuze Investment, Kaifeng Venture Capital, and Zehou Capital.

Team Composition:CEO Du Bo, a graduate of the Department of Biology at Peking University; Chief Medical Officer Zhang Henghui, with over 10 years of experience in clinical practice and translational research. The company employs more than 300 staff members, with PhDs accounting for over 21% and Master’s degree holders for over 40% of its R&D team.

Main Products or Services:

1. Testing services include multi-target tumor detection and combination therapy, medication guidance protocols for solid tumors, and protein detection products targeting PD-L1/PD-1 and the four mismatch repair (MMR) proteins in solid tumors, covering multiple cancer types such as colorectal cancer and breast cancer.

2. NGS-based kit products for colorectal cancer and lung cancer are in the pre-submission preparation phase.

Development Model:

1. Based on a comprehensive assessment of oncological diseases, we assist physicians in formulating diagnostic and therapeutic strategies by leveraging multi-dimensional approaches, including genetic testing and protein profiling.

2. Address the needs of clinicians and patients by focusing on shortening report turnaround times and improving report readability, thereby facilitating the use of test results in clinical practice and research.

3. Establish a big data center for precision diagnosis and treatment of tumors, and an oncology outpatient clinic.

Strategic Direction:

1. Always start from clinical needs; the technical platform and testing dimensions are not limited to next-generation sequencing, providing valuable guidance on clinical diagnosis and treatment plans for doctors and patients, such as distinguishing between primary and metastatic tumors, thereby more precisely guiding patient medication.

2. In addition to participating in CRO (Contract Research Organization)-like services such as target screening for pharmaceutical companies, further expand the scope and depth of collaboration with pharmaceutical enterprises.

Market Promotion:The sales network covers most provinces in China, with an initial focus on the urban clusters in East China, North China, and South China.

Key Data:To date, more than 50,000 sample data points have been accumulated, with the vast majority derived from third-party testing services. From 2017 to 2018, 14 research findings were accepted for presentation at the American Society of Clinical Oncology (ASCO) Annual Meeting. A 1,900-square-meter production facility for medical devices and diagnostic reagents has been established in the Taizhou National Medical High-Tech Industrial Development Zone in Jiangsu Province, and an 1,800-square-meter big data center for precision oncology diagnosis and treatment has been built in Wuxi.

Advantages and Highlights:

1. Strategic Advantages. Since its inception, the company has focused on addressing clinical needs by optimizing product design and service workflows, maintaining scientific research collaborations with clinicians, and solving practical clinical problems, thereby facilitating subsequent service delivery and product promotion.

2. Product Advantages. During product development and technical optimization, we closely followed the latest industry and technological trends. For instance, we launched testing services for PD-L1/PD-1 inhibitors as early as 2017, which helped us establish a competitive edge over subsequent rivals.

Challenges and Risks

1. Technological Uncertainty. The tumor gene testing industry is still in its early stages, with many technical challenges remaining, such as the capture of ctDNA and the correlation between methylation and tumor medication.

2. Policy Uncertainty. Currently, there are still many obstacles to establishing for-profit medical institutions either in partnership with hospitals or independently.

4.3 Gene+: Focusing on Precision Prevention and Treatment of Tumors, Adhering to Data-Driven Approaches

Establishment Date: April 2015

Funding Status:In August 2016, it announced that it had secured RMB 200 million in Series A financing from investors including BGI Genomics, Volcanic Stone Investment, and Sinopharm Capital.

Team Composition:Chairman Yi Xin, formerly Chief Operating Officer of BGI Medical and Deputy Director of BGI Research Institute; CEO Yang Ling, formerly Head of the Health Division at BGI Health and Director of the Shenzhen Key Laboratory for Clinical Molecular Diagnostics.

Main Products or Services:

1. Clinical testing services spanning the entire cancer care continuum. We have launched four series of diagnostic products—precision oncology medication guidance, treatment efficacy monitoring, postoperative surveillance, and hereditary risk assessment—along with corresponding baseline plans for whole-disease-course management.

2. High-throughput (NGS) IVD products for pan-cancer detection. Establish a clinical application demonstration platform for the NGS-IVD model, providing decentralized, simplified operational models along with training, technical support, and services for joint clinical laboratories. The independently developed OncoBox high-performance computing workstation for oncology integrates high-performance computing hardware, bioinformatics analysis software, gene interpretation databases, and data management platforms into a unified system, enabling fully automated generation of reports from sequencing data.

3. Research services in collaboration with pharmaceutical companies. Through testing and diagnostic services, we assist in patient screening for clinical trials to improve success rates and develop companion diagnostics to support drug market approval; through data services, we help enterprises reduce drug R&D expenditures.

4. Public-Oriented Health Baseline Program. This program monitors cancer risk across three major dimensions—somatic mutations, immunity, and genetics—to comprehensively assess an individual’s susceptibility to nearly ten types of cancer, including gastric cancer.

Development Model:

1. Guided by tumor genomic data, we are committed to acquiring more comprehensive and systematic tumor sample datasets, leveraging data mining to enhance patient therapeutic benefits, thereby expanding the dimensions of our testing services.

2. Guided by the trend toward large-panel NGS testing in tumor genetic analysis, and leveraging technical platforms such as immune repertoire sequencing and tumor molecular clone monitoring, we promote an NGS large-panel testing service covering 1,021 tumor-related genes.

3. Formed a strategic partnership with BGI to develop domestically produced sequencers, sequencing kits, and other products, thereby reducing sequencing costs; entered into a strategic agreement with Rongzhilian to collaborate comprehensively in areas such as bio-cloud platforms and NGS clinical diagnostics, accelerating the clinical translation of high-throughput next-generation sequencing (NGS).

Strategic Direction:

1. Adopting a dual-pronged strategy of clinical testing services and IVD products to meet clinical and research needs, we continue to provide comprehensive and flexible 1,021-gene large-panel testing services. With the market approval of the Gene+Seq sequencer, we are focusing on the R&D and regulatory submission of small-panel assay kits, with targeted promotion in tertiary hospitals and specialized oncology hospitals at all levels.

2. Amid the current surge in new drug development, we will engage more systematically in pharmaceutical R&D processes, such as biomarker research and target screening for pharmaceutical companies, to assist them in identifying patient populations likely to benefit from oncology drugs.

3. Leveraging the NGS-ctDNA detection platform, we provide early cancer screening services for the general population, establish individualized continuous dynamic genetic data baselines for participants, and achieve comprehensive, precise, and personalized health management.

Market Promotion:Through collaborative initiatives such as joint research with physicians and multi-center clinical trials, the company has gained physician recognition for its technologies and products, while enhancing their understanding of the clinical value and patient benefits. This strategy has facilitated the acquisition of more extensive oncology data and simultaneously driven sales growth in clinical testing services. Currently, the company collaborates with nearly 300 hospitals, predominantly Tier-3 Grade-A hospitals in first-tier cities.

Key Data:To date, more than 60,000 tumor NGS testing data samples have been accumulated, with nearly 50,000 of these samples generated through scientific research collaborations, predominantly involving free testing. The data dimensions include genetic testing data, follow-up data, and clinical data. By the end of 2019, the cumulative number of tumor samples is projected to reach 200,000. Based on NGS-ctDNA detection technology, there are over one hundred collaborative research projects with medical institutions.

Advantages and Highlights:

1. Clear market positioning. The services and products are clearly defined, with differentiated service and product models designed according to regional variations and hospital-specific needs, thereby establishing a competitive edge through differentiation.

2. Abundant clinical resources. The rapid accumulation of tumor sample volumes provides a platform for subsequent scientific research analysis and big data mining of tumor genes.

Challenges and Risks:In the initial stage, large volumes of data can be accumulated through scientific research collaborations and free testing; however, this approach requires substantial capital investment and is difficult to sustain in the later stages of development. Policy barriers also hinder the clinical application of ctDNA.

4.4 3DMed: Gene Testing Synergizes with Drug Development

Establishment Date:December 2010

Financing Status:The latest round, namely the Series E financing, took place in the second half of 2017, co-led by China State-owned Capital Venture Investment Fund and China Equity Capital, with the amount reaching RMB 670 million; the company secured RMB 146 million in its Series D financing in 2015.

Team Composition:Xiong Lei, Chairman and Co-CEO, brings 17 years of experience in tumor biology and pharmacology research; Gong Zhaolong, CEO, has 10 years of experience in new drug review at the U.S. FDA and 10 years of experience in drug development.

Main Products or Services:A theranostics company integrating diagnostic services and drug development. Its diagnostic offerings include companion diagnostics for oncology medication guidance. It is developing tumor-targeted therapies and PD-L1 immune checkpoint inhibitors, with the latter having entered late-stage clinical trials.

Development Model:

1. Through diagnostic services, we provide a data entry point for drug development and establish capabilities in companion diagnostics during the drug development process. Meanwhile, we have built an academic promotion team integrated with diagnosis and treatment, laying the foundation for drug development and marketing;

2. Leverage the advantages of companion diagnostic biomarker development through new drug development. Enhance the success rate of clinical trials and establish market entry barriers for drugs by selecting targeted patient populations.

Strategic Direction:Continue to leverage precision medicine based on companion diagnostics as a strategic entry point to guide and define drug development directions, promote the integration of diagnostics and therapeutics, establish an ecologically collaborative value chain, and achieve a closed-loop system for integrated diagnosis and treatment of oncology.

Key Data:In the diagnostic services segment, we currently have companion diagnostic business collaborations with physicians from over 200 Grade IIIA hospitals, serving nearly 20,000 patients. In the new drug development segment, three drugs have entered clinical trials, one of which is in the late stage of drug development.

Advantages and Highlights:Pursuing companion diagnostic (genetic testing) services in parallel with drug development facilitates the direct realization of the value of genetic testing data. Furthermore, regulatory approval and market launch of new drugs can raise the competitive barriers for the companion diagnostic business.

Challenges and Risks:Both genetic testing and drug development require substantial investment, with the latter involving longer development cycles and greater capital needs, posing significant challenges to corporate operational capabilities.

5.1 Product Homogenization:Currently, in the field of oncology genetic testing, the products and services offered by market participants are largely focused on medication guidance and prognosis monitoring. In particular, most medication guidance is based on approved drugs or publicly known targets. An overall assessment of the top 10 companies currently leading this market reveals that the differentiation between higher-ranked and lower-ranked competitors is not sufficiently pronounced.

5.2 Technical Uncertainty:Although tumor genetic testing and liquid biopsy technologies are advancing rapidly, the technologies and products remain immature. There is still room for improvement in sensitivity, specificity, and accuracy of test results. For instance, challenges such as minimizing ctDNA loss during detection, and reducing false-positive rates and error rates need to be addressed. Furthermore, discrepancies in test results across different companies may negatively impact the overall public perception of the tumor genetic testing industry among patients.

5.3 Policy Uncertainty:The clinical application of NGS in tumor diagnosis is still in the pilot phase. Although NGS-based tumor gene testing kits are expected to be approved soon, third-party outsourcing services remain unregulated, leaving gray areas in industry oversight. Drawing from the NIPT market’s development, during which testing services were once completely suspended, tumor gene testing still faces significant policy uncertainty.

6.1 Market Landscape to Undergo Reshuffling:Although the tumor genetic testing industry as a whole is still in the data accumulation stage, four or five companies are already leading in terms of sample volume, data completeness, and market share. As more targeted drugs come to market, raising the bar for testing technologies, and as physicians become better at assessing the quality of testing products, a number of companies that fail to keep pace with technological and industry trends will be eliminated. Given that the China Food and Drug Administration (CFDA) is expected to sequentially approve certain next-generation sequencing (NGS) tumor genetic testing kits for market launch in the second half of this year and next year, the overall landscape of the industry is projected to gradually clarify by 2019, undergoing a consolidation process in which only three out of ten major players will remain.

6.2 Companies Move Toward Differentiated Competition:Constrained by the current maturity of technology and products, the vast majority of oncology genetic testing companies currently focus their business on medication guidance and companion diagnostics. However, as technology continues to evolve and the industry landscape becomes increasingly defined, key market players will shift toward differentiated competition. Such differentiation may manifest in technological platforms, choices of business and commercial models (such as IVD product models versus LDT models), or a strategic focus on specific cancer types and the coverage scope of genetic loci. Without such differentiation, companies will be unable to establish core competencies that distinguish them from competitors.

6.3 Early Cancer Screening as the Second Growth Curve:Driven by the rigid demand for precision diagnosis and treatment among patients with intermediate- to advanced-stage tumors, and given that targeted therapies will occupy an increasingly prominent position in the medication regimen for cancer patients, medication guidance and prognosis monitoring remain the primary growth drivers for the tumor genetic testing industry, as well as the main revenue source for the majority of companies in this sector. However, with advancements in early cancer screening technologies and the further accumulation and mining of data from patients with intermediate- to advanced-stage tumors, early cancer screening is poised to become the second growth curve for the tumor genetic testing market. Nevertheless, due to significant technical challenges and the need for further validation of additional information, this niche market is expected to require at least another 2–3 years of development before reaching maturity.