McKinsey Report: Deconstructing Healthcare Consumerism – Affordability Remains a Top Public Concern

McKinsey’s Consumer Health Insights Report indicates that consumers expect to understand the processes and costs of healthcare services through digital tools to inform their decision-making. VCBeat (WeChat ID: vcbeat) has compiled this information.

The respondents in this Consumer Health Insights Report were adults aged 18 and older, including consumers without health insurance. However, due to the small sample size, consumers with niche insurance plans, such as TriCare or Indian Health Services, were excluded. The report has had a broad impact on health insurers, healthcare providers, and other stakeholders within the industry, covering four key themes:

Affordability: The affordability of healthcare remains one of the topics consumers are most concerned about.

Continuity: Many consumers experience a lack of continuity in the healthcare ecosystem (e.g., in the provision of medical services or health insurance).

Digitalization: A growing number of consumers are using digital health tools and expecting greater engagement in the digital space.

Engagement: Consumers are willing to engage in solutions aimed at reducing healthcare costs, but the majority believe they are currently unable to do so.

These findings indicate that consumers desire more from the healthcare industry. When asked, “What would make a healthcare company the best?” respondents identified health insurance as the most important factor (23%), followed by customer service (11%), medical costs (7%), and accessibility (6%). Such fundamental issues may have been overlooked by most industries.

In fact, when respondents were asked what kind of enterprise healthcare organizations should aspire to be, they selected technology-driven innovators such as Amazon, Google, and Apple, as well as exemplary retailers like Chick-fil-A and Walmart. The connections consumers have forged with these companies illustrate what they expect from healthcare institutions. Given the personal stakes involved in health outcomes, healthcare organizations must be particularly consumer-centric. However, based on the current landscape, these institutions still have considerable work to do.

Healthcare affordability holds significant meaning for consumers, a importance manifested in multiple aspects. For instance, when respondents were asked about the barriers they encountered in healthcare, the top three answers were all related to affordability—difficulty in understanding basic medical costs (29%), challenges in deciding whether to insure for treatment (28%), and lack of clarity regarding their medical bills.

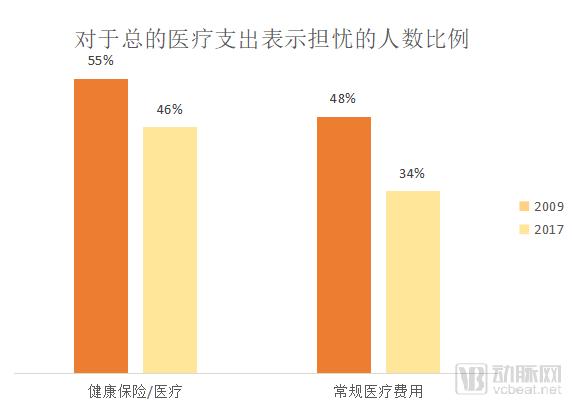

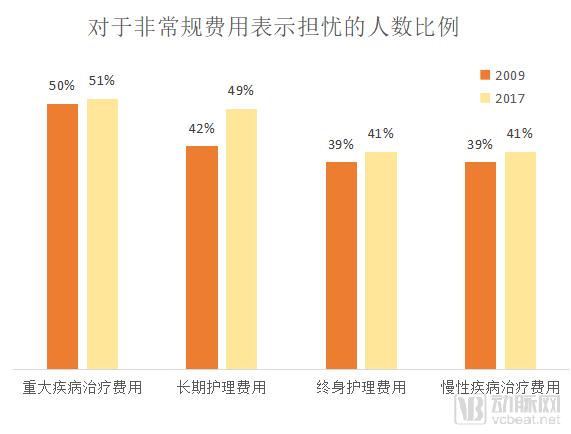

In summary, 72% of respondents expressed concern about at least one type of medical expense (Table 1). We found that consumer concern about overall medical spending has been declining since this question was first included in the survey in 2009. However, concern about non-routine expenses—such as costs associated with end-of-life and long-term care—is on the rise.

Table 1

Note: Percentages cannot be summed directly because many respondents expressed concerns across multiple areas.

Source: McKinsey’s 2017 Consumer Health Insights Report, compiled by VCBeat

These concerns may influence consumers’ perceptions of accessing healthcare services. In the survey, 20% of consumers reported that they did not receive all the medical care they needed. Among them, 60% cited medical costs as one of the reasons. Vision care and dental care were also services that consumers failed to receive, at rates far exceeding those for routine medical care.

Similarly, in another study released in 2017 focusing on consumers with individual insurance coverage, respondents were asked to identify the three most important factors when selecting a health plan. The majority prioritized affordability-related factors. The lowest monthly premium was cited most frequently (56%), followed by the plan’s maximum value (51%) and the lowest out-of-pocket expenses (43%).

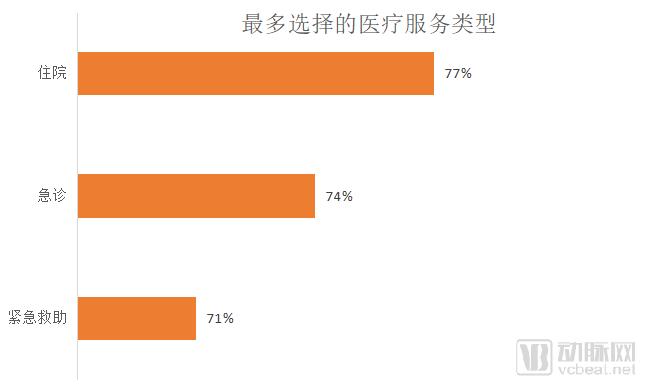

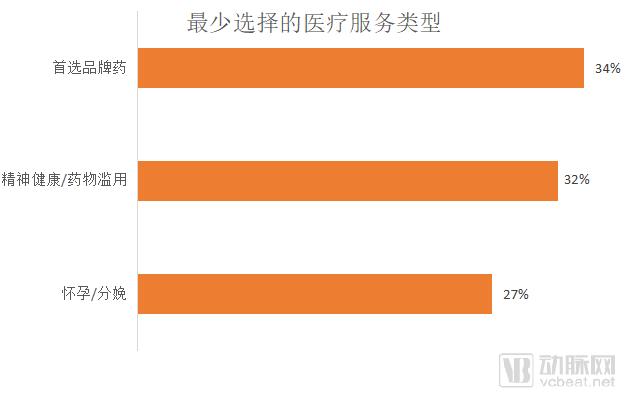

However, consumers are willing to weigh the trade-offs in health insurance plans to obtain the coverage they value most. The CHI report indicates that many consumers are reluctant to lose core medical services in their insurance plans, with hospitalization and emergency care being their primary concerns. In contrast, coverage for pregnancy and childbirth is generally of least concern (Table 2). Views on eliminating pregnancy and childbirth coverage vary significantly across age groups but show little difference between genders. Dental care is the benefit consumers are most eager to add to their health plans.

Table 2: Healthcare Services Chosen by Consumers with Private Insurance or No Insurance

Source: McKinsey’s 2017 Consumer Health Insights Report, compiled by VCBeat

Many consumers lack continuity within the healthcare ecosystem, whether it is defined as an insurance system or a provider of healthcare services. For example, in a survey, only 43% of new enrollees in medical insurance had previously held commercial group insurance. Twenty-five percent participated in Medicaid, and 24% had individual insurance. The remaining 8% had never been insured before. Among the surveyed new enrollees, two-thirds had prior experience with group insurance.

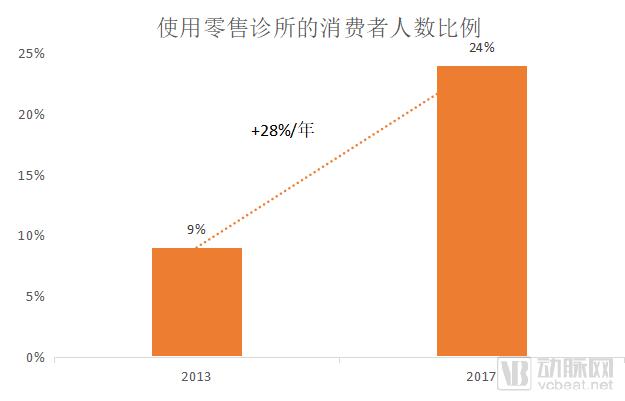

Similarly, the continuity of healthcare service delivery is also declining, with the proportion of respondents having access to basic medical services gradually decreasing from 87% in the initial survey in 2011 to 79% in 2017. Meanwhile, the use of retail clinics has been steadily rising (Table 3). In our survey, more than four out of five respondents indicated their willingness to receive medical care at retail clinics.

Table 3: Steady Rise in Retail Clinic Utilization

Source: McKinsey 2017 Consumer Health Insights Report, compiled by VCBeat

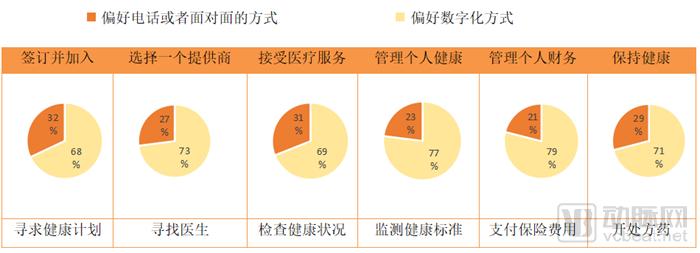

An increasing number of consumers expect digital tools to become a core component of healthcare service delivery. For instance, most respondents prefer digital solutions for communication over telephone or face-to-face interactions (Table 4).

Additionally, 89% of respondents reported awareness of digital appointment scheduling reminders for medical visits, while 55% had used such tools. As awareness of other digital tools grows, their usage is likely to increase correspondingly. Respondents also believed that the healthcare industry should strive to catch up with many digitally advanced enterprises.

Table 4: Approximately 70% of Consumers Prefer Digital Healthcare Solutions

Source: McKinsey’s 2017 Consumer Health Insights Report, compiled by VCBeat

Currently, the adoption of digital tools in the healthcare sector lags behind that of many other industries. For instance, only 49% of respondents reported having used relevant technologies provided by health insurance companies. Usage was highest among individuals aged 18 to 34 (62%) and lowest among those aged 65 to 84 (39%).

The McKinsey 2015 Consumer Insights Report indicates that the relatively low adoption rate of digital tools in the healthcare sector is not driven by concerns over data breaches. Whether the issue of data breaches has been improved will be examined in subsequent research. Consumers primarily use technologies provided by health insurance companies to update personal information (17%), identify benefits covered under their health plans (15%), and locate in-network physicians and hospitals (13%).

Many consumers wish to engage more actively in the healthcare industry, particularly by making better-informed decisions that meet their individual needs, such as affordability. In our survey, respondents emphasized the desire to fully understand medical services before making decisions, thereby enabling greater participation in the healthcare system, even among those with comprehensive insurance coverage. However, the majority of respondents believe they are currently unable to achieve this.

To help consumers achieve this goal, the healthcare industry needs to communicate with them through more effective and diverse channels. Collaboration is of paramount importance. This study offers three viable approaches for health insurers and healthcare providers to engage consumers in solutions aimed at reducing medical expenditures.

Improve Education.Many consumers misunderstand the sources of medical costs, leading to decisions made with insufficient information (Table 5).

Table 5: Sources of Health Insurance Costs

Source: McKinsey’s 2017 Consumer Health Insights Report (left) | Interviews with actuarial experts (right), compiled by VCBeat

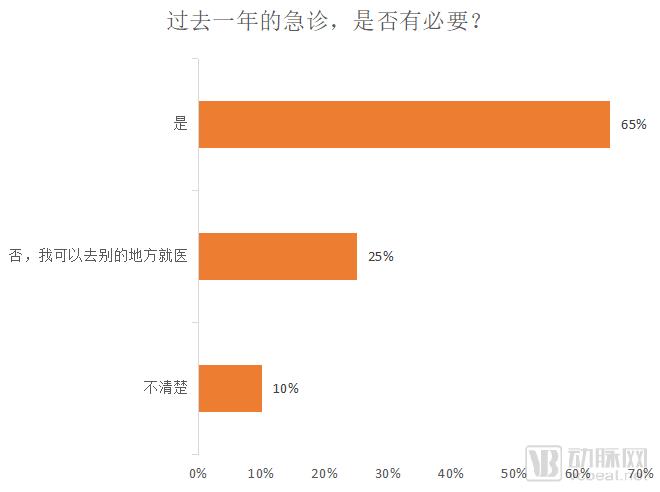

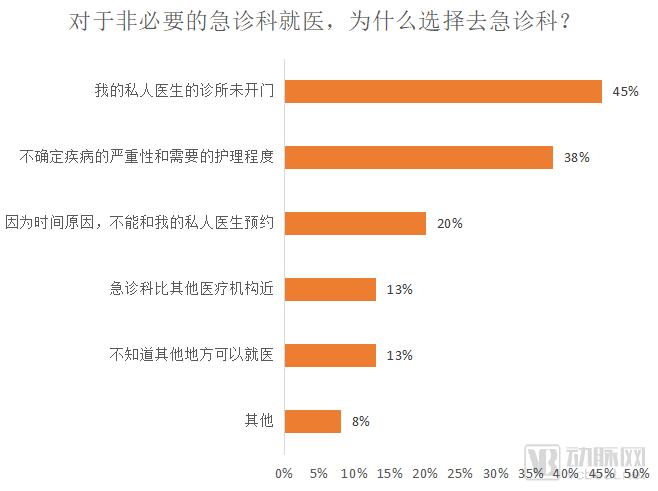

Improvement Guidelines.Consumers often fail to utilize healthcare services effectively, leading to increased costs. For instance, among respondents who visited the emergency department (ED) within the past year, one-quarter indicated that they could have sought care elsewhere but often chose the hospital ED due to practical considerations (Table 6).

Table 6

Source: McKinsey’s 2017 Consumer Health Insights Report, compiled by VCBeat

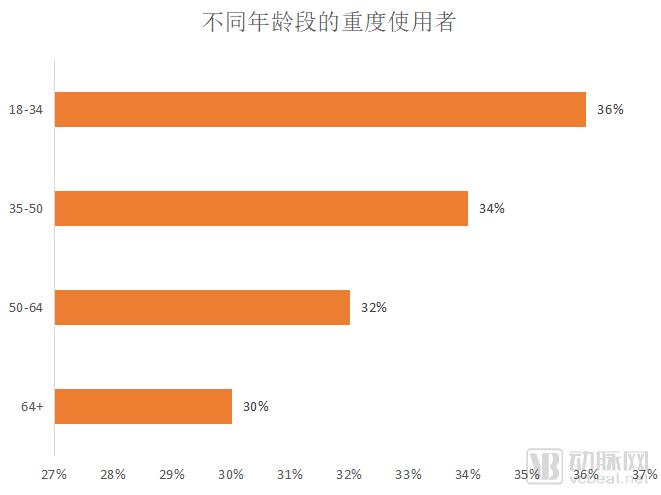

Frequent emergency department visits are particularly prevalent among young adults (aged 18 to 34). They are the only group more likely than older respondents to be high utilizers of healthcare services (Table 7). High utilizers are defined as those in the top 10% of healthcare spenders within each age group.

However, among these young people, 67% had visited the emergency department more than once in the past year (compared with 59% of all heavy users). Young heavy users can be further divided into two groups: those who use the emergency department for non-urgent conditions and those who do not frequently use the emergency department. The latter are three times as likely as the former to have a designated primary care physician.

Table 7: Younger individuals are more likely to frequently visit the emergency department

Source: McKinsey 2017 Consumer Health Insights Report, compiled by VCBeat

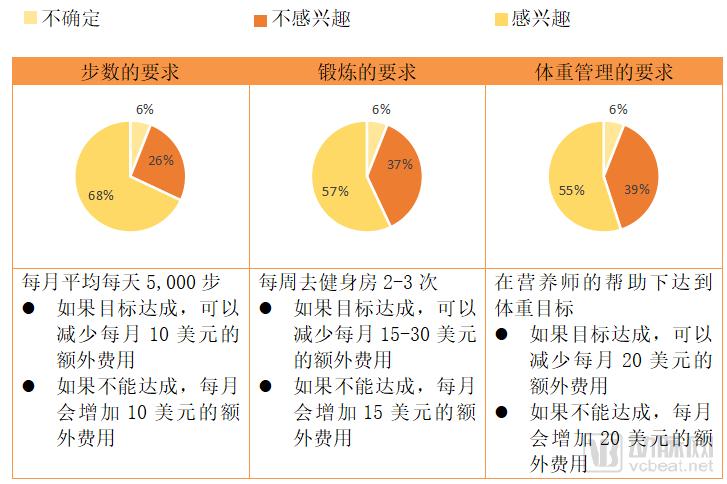

Better incentives.Consumers stated that they would be willing to change their consumption behaviors if their medical expenditures could be reduced (Table 8). More effective incentive mechanisms can help achieve this goal.

Table 8: Consumers' Willingness to Reduce Spending by Changing Behaviors

Source: McKinsey 2017 Consumer Health Insights Report, compiled by VCBeat

The healthcare industry can collaborate with consumers to address these issues, ultimately achieving a win-win outcome. For instance, as noted in surveys, many concerns about affordability stem from a lack of transparency or understanding. Health insurers and healthcare providers can take steps to better inform patients about potential medical costs. When consumers understand their total and out-of-pocket medical expenses, they are better equipped to choose the appropriate types of services and select the optimal health plans that meet their needs.

Consumers are highly concerned about healthcare affordability and pay close attention to insurance coverage and practical issues. They view healthcare as extending beyond the current scope of health insurers and healthcare providers, thereby creating opportunities for insurers to develop value-based, differentiated products that meet individual consumer needs (e.g., narrowing or layering provider networks, and expanding insurance offerings). This new product portfolio should be sufficiently flexible to adapt to evolving consumer needs as their quality of life improves. Consumers often require assistance when transitioning from one type of insurance coverage to another.

Consumers are increasingly seeking to reduce their reliance on traditional medical services, which means that innovators and disruptors have greater opportunities while also posing challenges to the existing healthcare system. For instance, managing overall healthcare expenditures may become more difficult when patients do not establish long-term relationships with primary care providers, even though the cost of visiting retail clinics is generally much lower than that of hospital care. Healthcare professionals today need to consider how to collaborate with consumers to maintain continuity in these therapeutic relationships.

Today’s consumers also expect greater digital engagement. A growing number of consumers believe that healthcare institutions should provide digital tools, just as companies in other industries do. By learning from leading technology firms, healthcare institutions can better design the digital tools consumers need and ensure their proper functionality. Furthermore, healthcare institutions should take steps to inform consumers about available digital tools, since awareness is closely linked to adoption. Health insurers and healthcare providers that neglect to learn from technology companies may face the risk of being displaced by emerging competitors.

Finally, collaborating with consumers is crucial for controlling healthcare expenditures. Health insurers and providers have ample opportunities to engage with consumers, helping them manage their health, medical care, and healthcare costs. For instance, they can help consumers understand how their behaviors impact healthcare spending and assist in correcting misconceptions. By leveraging digital tools to enable timely, on-demand engagement and provide meaningful incentives, insurers and providers can truly partner with consumers to change their behaviors and improve public health.

Healthcare consumption habits are changing in ways beyond imagination, and this transformation will continue. The 2017 Consumer Health Insights Report can help health insurance companies and healthcare providers better communicate with consumers and deliver the services they need.

Reference: https://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/healthcare-consumerism-2018