Oscar Health's Strategic Pivot: Halving Annual Losses Amid $3.2B Valuation

Oscar Health

Online Medical Insurance Service Company

As a unicorn in the health insurance sector, Oscar has achieved a valuation exceeding $3.2 billion this year. It is favored by multiple investment institutions, including Verily Life Sciences and Capital G, both under Alphabet, Google’s parent company. Other funds that have repeatedly participated in follow-on investments include Fosun Capital, Founders Fund, and Khosla Ventures.

Data source: Crunchbase (2018 user figures are estimates)

Oscar Health’s development trajectory reveals that 2017 marked a turning point for the company. Although 2017 was not the only year since its inception without any financing or investment activities, Oscar Health managed to halt its continuous substantial losses during this period.

Oscar Health, founded under the Affordable Care Act (Obamacare), initially pursued a development strategy aimed at leveraging technology to achieve low-cost, rapid response and user intervention, thereby reducing costs and risks while expanding insurance coverage.

However, with Trump’s ascent to power and the subsequent shockwaves hitting the Affordable Care Act, Oscar began to pivot by charging higher premiums and implementing a “narrow” provider network.

In March 2018, Oscar secured financing at a valuation of $3.2 billion, indicating that its strategic pivot toward tighter user engagement has proceeded relatively smoothly. As a novel type of insurer, Oscar rewards customers for healthy behaviors, simplifies the claims process, and enhances price transparency, thereby disrupting the traditional relationship between insurers and consumers.

Amid various uncertainties in policies, economic development trends, and technological advancements, specific models remain to be explored. However, across all reform directions, insurance companies should transition from short-term relationships with customers to a long-term service-oriented model.

Even as the most highly valued unicorn in the health insurance sector, Oscar Health faces considerable skepticism from external observers due to its high costs and a long-term loss ratio exceeding 100%. This article aims to dissect Oscar Health’s transformation and development trajectory, examine the ongoing changes within the health insurance industry, identify the challenges underpinning Oscar’s strategic pivot, and explore how Oscar Health is redefining the future of insurance.

The U.S. healthcare system faces two major challenges, the first of which is rising medical costs. Although the United States leads the world in medical technology, treatment protocols, and healthcare talent, its total healthcare expenditure has reached approximately 15% of GDP.

According to current projections, U.S. healthcare spending will exceed 20% of its GDP by 2030. Without reform, it is estimated that by 2050, federal tax revenues will be entirely consumed by Medicare, Medicaid, Social Security, and interest on the national debt.

Second, the population coverage of medical security in the United States lags behind countries such as the United Kingdom, Japan, and Canada, which have achieved universal social security. In the U.S., 15% of the population still lacks any form of health insurance. Despite this, its average life expectancy ranks second to last among OECD countries. Ironically, government spending accounts for 46% of total healthcare expenditure in the United States—similar to the level in China—but falls far short of the 72% average seen in other developed nations. The United States is the country with the highest healthcare spending in the world and the only developed nation with a health insurance coverage rate below 95%. (Source: “In Search of the Perfect Healthcare System”)

One perspective attributes this situation to market-based pricing, which grants pharmaceutical companies and medical equipment providers full autonomy in setting prices, thereby leading to high costs for drugs and medical services. However, data show that in the breakdown of healthcare expenditures in the U.S. healthcare system, the top five categories are hospital expenses (32%), physician fees (26%), prescription drug costs (13%), personal home care (8%), and private insurance administration costs (7%). This indicates that pharmaceutical spending is not the largest component of U.S. healthcare expenditures; rather, the primary cost drivers are the market value of hospital operations and healthcare human resources.

In the history of U.S. healthcare payment, the primary reimbursement models have been fee-for-service and capitation. Under fee-for-service, hospitals and physicians receive higher payments for providing more services. This inevitably leads to overutilization; a study by Dartmouth University indicates that up to half of all medical services in the United States are medically unnecessary.

Moreover, with the intensification of population aging, the number of elderly individuals receiving services continues to rise, driving sustained increases in medical costs and rendering fee-for-service payment models financially unsustainable.

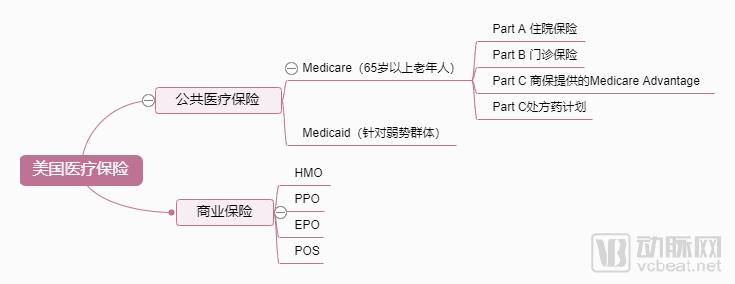

HMO (Health Maintenance Organization): This type of insurance emphasizes prevention, offers limited choice in healthcare providers, and requires enrollees to seek care at designated healthcare facilities. The insurer assigns a primary care physician to each enrollee to address basic medical needs and manage referrals, thereby helping the insurer control healthcare costs.

PPO (Preferred Provider Organization) No need for a primary care physician; direct access to specialists is available. Users can enjoy discounted rates when seeking medical care at facilities within the preferred provider network.

EPO(Exclusive Provider Organization) Members must seek medical care within the designated network of healthcare providers, without a general practitioner

POS ((point-of-service) Positioned between low-premium HMOs and PPOs with greater flexibility, featuring primary care physicians.

In the United States, the negotiation methods between insurance companies and healthcare providers are determined by the American Medical Association.

In the United States, public health insurance is divided into two categories. The government-led social health insurance programs primarily cover the elderly (Medicare) and vulnerable populations (Medicaid), while health insurance for the working population is provided by commercial insurers. Additionally, some individuals purchase private insurance independently.

Insurance reimbursement constitutes the primary source of income for physicians and healthcare institutions, with payment standards and methods subject to periodic negotiation between both parties. Notably, the government-administered Medicare program employs administrative pricing; physicians and healthcare institutions must either accept or reject these rates. If they choose not to accept them, they are prohibited from treating patients enrolled in Medicare.

Under the fee-for-service model, the American Medical Association (AMA) has established a five-digit coding system for all possible medical treatments, diagnostic procedures, and surgical processes, known as Current Procedural Terminology (CPT) codes. While a drug or device may have disruptive potential to solve a problem in a unique and cost-effective manner, the cost of obtaining a unique CPT code for a new product is prohibitively high. Furthermore, the likelihood of the AMA—an organization representing those susceptible to disruption—approving a product positioned as disruptive is extremely low. Under fee-for-service payment models, where healthcare providers can pass on costs, decision-makers lack the incentive to adopt disruptive technologies.

Commercial insurance institutions negotiate prices with physicians and medical facilities, using the aforementioned Medicare payment standards as a benchmark.

Within the public health insurance system, traditional Medicare is also attempting to transition from the conventional fee-for-service model to alternative payment methods such as bundled payments. The advantage of bundled payments lies in incentivizing providers to control costs while ensuring quality under the dual pressures of competition and insurance performance evaluations. However, a significant issue arises when dominant public insurers adopt bundled payments: it encourages providers to consolidate or merge to gain negotiating leverage and achieve economies of scale, which may ultimately drive up healthcare costs.

The traditional fee-for-service model fails to incentivize healthcare providers to control costs; instead, it hinders the adoption of innovative initiatives that could reduce hospital billable items.

Reforming payment methods to incentivize high-quality, appropriate medical services and control costs is an inevitable path for healthcare reform in the United States. Among the health insurance reform solutions proposed by Clayton Christensen, the father of disruptive innovation in healthcare, different business models delivering healthcare services should be paired with distinct health insurance systems. The predominant model should involve Health Savings Accounts (HSAs) combined with high-deductible insurance plans, replacing traditional private health insurance.

To achieve the goal of reducing healthcare costs, the entire medical system needs to shift its focus toward prevention, as indicated above. The predicament faced by health insurance payers—characterized by a lack of bargaining power and initiative—must also be addressed. Health insurance companies should go beyond merely paying hospital bills; they should begin providing the same health maintenance services that hospitals offer to patients.

No insurance company, no matter how strong, can remain immune to the digital wave. Be it demographic shifts, transformations in the healthcare industry, or sudden changes in regulatory policies, a multitude of uncertainties are compelling health insurers to implement immediate changes.

The impact of chronic diseases driven by population aging is substantial, with the growing burden of these conditions leading to a continuous rise in healthcare expenditures. Both the public sector and taxpayers are seeking more cost-effective incentives to alleviate healthcare spending.

In EY’s report on participatory healthcare, while average life expectancy has increased, healthspan—the period of life spent in good health—has not kept pace. The age at which individuals are expected to cease creating value is 75; however, in reality, by their fifties, many people’s physical conditions can no longer sustain the anticipated level of functioning. In terms of actual medical expenditures, chronic diseases such as heart disease, type 2 diabetes, and hypertension account for 75% of healthcare spending.

These diseases share two characteristics. First, they are largely associated with lifestyle habits and are significantly influenced by behavioral patterns. For these currently incurable chronic conditions, patients must live with their symptoms for the rest of their lives.

In the transformation of health insurance, the focus must shift from the traditional fee-for-service and outcome-based payment models to a greater emphasis on prevention. Both health insurers and governments should consider how to reform existing systems to incentivize healthy behaviors among users. The insurance industry needs to transition away from the fee-for-service model.

This business model also effectively addresses patients’ needs. While patients purchase health insurance to share risk, their primary goal is always to maintain good health. Furthermore, all consumers seek financial returns. However, the Health Savings Account (HSA) model requires consumers to forgo traditional, conservative comprehensive insurance policies and assume a certain level of risk, with the benefits from HSAs accumulating over the long term. In contrast, behavior-based reward models, such as that employed by Oscar Health, are more effective in incentivizing positive changes in consumer behavior.

New business models have emerged in response to these issues. For example, Oscar Health rewards users for healthy behaviors, capitalizes users’ insurance accounts, and sets coverage limits for specific patients and conditions when paying hospitals.

As a tech-driven insurance company, Oscar has innovatively introduced smart devices into users’ health management. Oscar provides wearable devices to help users with assisted exercise and health monitoring; if users meet their targets, they can receive rewards of up to $20 in their Amazon accounts. This is just the first step for Oscar Health in helping its customers become healthier.

To reduce customers' health risks, Oscar has not limited itself to partnerships with hospitals; it has begun offering services previously provided exclusively by hospitals. In November 2016, Oscar partnered with the renowned Mount Sinai medical center in the United States to establish a brick-and-mortar clinic located in Brooklyn Heights, New York. This physical facility is available exclusively to Oscar members. The medical center provides chronic disease management and preventive care (excluding acute conditions), vaccination registration, and physician consultations. It also offers free classes to members, such as yoga sessions tailored for women.

Oscar Health is shifting from its previous model of paying for outcomes to paying for user behavior and value.

Although the health insurance sector is dominated by numerous industry giants, unicorns continue to emerge frequently. In transforming the entire health insurance system, focusing on user behavior is key; however, due to high employee turnover, employers have limited motivation to use behavioral incentives to promote individual healthy behaviors. While chronic diseases impose the greatest pressure on the healthcare system, the government tends to prioritize short-term fiscal concerns. Moreover, all parties are constrained by outdated systems and mechanisms, making it difficult to break down internal barriers and leverage existing data.

Startups in the health insurance industry can reshape the sector with their greater flexibility. First, they are responding to the global trend toward user-centricity. The democratization of technology has empowered ordinary consumers, who now demand greater transparency and protection, as well as more convenient services.

The rise of mHealth is also driving a user-centric trend. The boundary between medical devices and smart devices is becoming increasingly blurred. With advancements in technologies such as sensors, AI, and mobile applications, individuals can easily monitor their health status. The Internet of Things (IoT) has the potential to disrupt chronic disease management systems. Currently, user medical data is fragmented, with no single entity possessing a complete view of a patient’s medical records—not even insurance companies. The winner will be whoever first establishes a closed-loop service ecosystem, masters the data chain, and gains deep insights into users.

Health insurance has already lagged behind many tech companies in medical innovation. In the current wave of technological advancement, failure to adapt means falling behind.

Oscar Health is dedicated to enabling users to complete all operations via its app. At its inception, Oscar aimed to cover a broader population; today, its “narrowed” provider network is designed to deliver higher-quality services. Oscar’s Net Promoter Score (NPS) stands at 37, compared with the industry average of 12.

As can be seen from the official website, Oscar Health provides health insurance solutions for both individuals and employers.

For users who insure their entire family, Oscar Health provides a dedicated team to address their healthcare needs. Customers who purchase health insurance plans receive 24/7 free doctor consultations and access to a network ecosystem comprising high-quality physicians and hospital resources. Unlike complex traditional insurance processes, all services offered by Oscar are managed through its mobile app.

Oscar Health’s competitiveness in its offerings to employers rests on two pillars: first, its strong reputation and exceptionally high user satisfaction; second, its bargaining power. Oscar can save each employee of a company $600–$900, a compelling figure for many large enterprises.

The products offered to corporate employees differ slightly from those available to general consumers. Oscar Health also provides free physician consultation services, although these are not available 24 hours a day, seven days a week. While corporate employees have access to a dedicated professional care team provided by Oscar Health, this team currently offers online services only. However, to streamline the referral process from primary care physicians to specialists, corporate employees can consult directly with designated specialists.

Currently, Oscar has over 2,000 corporate clients, including construction firms, law firms, and restaurants.

In terms of physician resources, Oscar Health boasts a large network of high-quality primary care physicians and frontline clinicians. Oscar partners with top-tier healthcare systems; all of the top 20 ranked healthcare systems in the United States are its partners, although Oscar currently provides services in only six U.S. states. Within Oscar’s healthcare ecosystem, there are over 3,500 physicians spanning more than 140 specialties.

Due to the scarcity of emergency medical resources in the United States, Oscar can arrange for users to be taken to the nearest hospital. When users are far from their familiar areas, the care advisory team provided by Oscar Health can help them identify which hospitals are the optimal choices.

Although the measures adopted by Oscar Health will increase labor costs and appear to require users to make more changes during adoption, compared with clinical consultations in traditional models, mobile healthcare enables real-time health management for users in a more convenient manner. Its adoption rate is expected to be faster, and these services can deliver a better medical experience for users.

Oscar Health’s disruption of the health insurance industry will not happen overnight, but it is inevitable.

Under the Affordable Care Act’s individual mandate, Oscar Health is scaling up its operations, while major insurers such as Aetna, Anthem, Humana, and UnitedHealth Group have either scaled back or completely exited their ACA-compliant individual health insurance businesses. After failing to effectively manage the costs associated with enrolling members in these plans, larger market participants are reducing their footprint or withdrawing from the individual market altogether.

In the face of high administrative and management costs, Oscar CEO Mario Schlosser stated that they are using technology to build a new insurance claims system.

Schlosser stated that this represents a significant improvement over most claims processing systems, which are currently largely cobbled together using programming tools from the 1970s.

Updating the claims system infrastructure will enable it to perform seemingly simple tasks that are often challenging in the current healthcare system, such as providing higher reimbursement to physicians for peak hours like evenings and weekends, or giving members clearer visibility into their out-of-pocket costs for surgeries or tests.

The project has been underway for two years, building upon Oscar’s $165 million fundraising campaign. This year, the company expects significantly improved performance, with Oscar reporting that its premium revenue now exceeds medical claims costs. Oscar plans to work closely with health systems in each state, enabling it to direct members toward a more organized, high-quality, yet affordable healthcare provider network.

Josh Kushner, a co-founder of Oscar Health, is the brother of Jared Kushner, President Trump’s advisor and son-in-law. Today, it has also become evident that, as healthcare legislation proves more resilient than anticipated, Oscar is able to focus on achieving expansion.

According to Forbes magazine, two years ago, Oscar Health still adopted a “narrowing” strategy. This year, Oscar Health has applied to offer insurance services in 14 new markets across nine states. The development of this new business will double its existing operations.

Oscar has ventured into providing healthcare services, rather than merely paying for them, with its first clinic located in Brooklyn. It is also exploring other types of insurance, including throughMedicare Advantage InsuranceSelling insurance to the elderly.

Schlosser stated, “We are currently focused on delivering strong experiences and favorable cost outcomes, but we have mechanisms in place for different markets.”

Although, from a current perspective, startups still face higher loss ratios due to adverse selection among users, the younger demographic that Oscar Health favors may prefer high-coverage plans that provide substantial protection against critical illnesses.

However, in light of the overall direction of healthcare reform, the insurance industry must address its capacity to manage health risks. Leveraging big data, insurers should engage in closer collaboration with public sector entities, healthcare providers, and technology companies, thereby participating comprehensively in users’ health management.

A report by Ernst & Young recommended that health insurance companies need to make changes in four areas: 1. Collaborate with other entities to build a healthcare ecosystem that truly incentivizes and stimulates healthy behaviors. 2. Shift claims processing from a focus on procedures to an emphasis on value and behaviors. 3. Leverage big data insights into customers to reduce medical costs and mitigate risks. 4. Explore new marketing methods and sales channels.

Oscar Health’s transformation exemplifies the aforementioned direction. By delivering more customer-friendly services, ensuring seamless claims processing, and leveraging various methods to anticipate and understand customer needs, Oscar has achieved a truly customer-centric model. The company has shifted from the traditional insurance functions of pricing and underwriting risk to actively engaging in customers’ health behaviors, thereby influencing and mitigating risks.

Given Oscar Health’s current losses and its relatively small policy volume compared to traditional insurance giants, many remain skeptical. Yet why do so many investors still choose to back Oscar? History has shown that if a startup masters a new innovation capable of disrupting the existing economic model, it can defeat nearly any established corporation.

In his book The Innovator’s Dilemma, Professor Clayton Christensen of Harvard Business School stated: “Disruptive innovations are often perceived as trivial and novel. They are seen as having limited revenue potential—particularly when compared to the substantial income that established incumbents generate from their existing products—and as failing to meet the needs of mainstream customers. For example, when the first personal computers emerged in the late 1970s, they were dismissed by incumbent (mainframe) computer manufacturers and their enterprise customers as inconsequential novelties. Yet, as is typical with disruptive innovation, personal computers improved at a pace far exceeding the expectations of existing computer manufacturers. By the time these companies belatedly recognized the growth potential of this new market, they scrambled to enter it. Few survived the transition. Most did not.”