Asthma Industry Research Report (Part I): Market Size to Reach USD 27.4 Billion in 2018, Traditional Anti-Asthma Drugs Heavily Import-Dependent with Domestic Share Only at 10%

According to the World Health Organization (WHO), an estimated 235 million people worldwide currently suffer from asthma, with the incidence rate among children and adolescents showing a year-on-year increasing trend.

An epidemiological survey conducted by the Chinese Asthma Alliance in 2013, covering seven major regions and eight provinces and municipalities across China with a sample size of over 160,000 individuals, revealed that the overall prevalence of asthma in China was 1.24%. The prevalence rates in Beijing and Shanghai increased by 147.9% and 190.2%, respectively, compared to the survey results from ten years earlier. The number of asthma patients in China reached nearly 25 million in 2016 and is projected to reach 45 million by 2025, including 12 million urban pediatric patients.

According to the latest estimates released by the WHO in December 2016, 383,000 people worldwide died from asthma in 2015, with more than 80% of these deaths occurring in low-income and lower-middle-income countries.

Figure 3 Growth Rate of Asthma Patients in Beijing and Shanghai

Source: White Paper on the Current Status of Asthma Management in China

In light of the current state of asthma management and the related market landscape, Probe Capital has authored this report by examining the pharmaceutical market for asthma treatments and digital innovative management approaches.VCBeat (WeChat: vcbeat)Organized and edited.

Key Insights:

1. The large base of asthma patients continues to grow year by year.

2. Medication adherence is poorer in children with asthma, warranting focused attention.

3. The market for traditional anti-asthma drugs remains stable, with a size reaching RMB 27.4 billion.

4. China's asthma medications are predominantly reliant on imported drugs, dominated by foreign pharmaceutical companies GlaxoSmithKline, AstraZeneca, and Merck & Co.

5. Biopharmaceutical R&D is garnering increasing attention, with promising future market growth expected.

Asthma is a chronic inflammatory disease of the airways, characterized by recurrent episodes of dyspnea and wheezing. Clinically, asthma manifests as symptoms such as wheezing, shortness of breath, chest tightness, and coughing. The occurrence, frequency, and intensity of these symptoms vary over time and often worsen at night and/or in the early morning.

This chronic inflammation is associated with the onset and progression of airway hyperresponsiveness. During an asthma attack, the lining of the bronchial tubes becomes inflamed and swollen, and mucus production increases, leading to airway narrowing, reduced pulmonary ventilation, and obstruction of expiratory airflow. While some alterations in respiratory airflow can also occur in individuals without asthma, these changes are more severe in patients with asthma.

Even patients undergoing asthma treatment may experience sudden acute asthma attacks. Most patients can achieve control through pharmacological therapy. However, if asthma remains uncontrolled or if patients are continuously exposed to high-risk environments, these acute exacerbations will occur more frequently and severely, potentially even proving fatal.

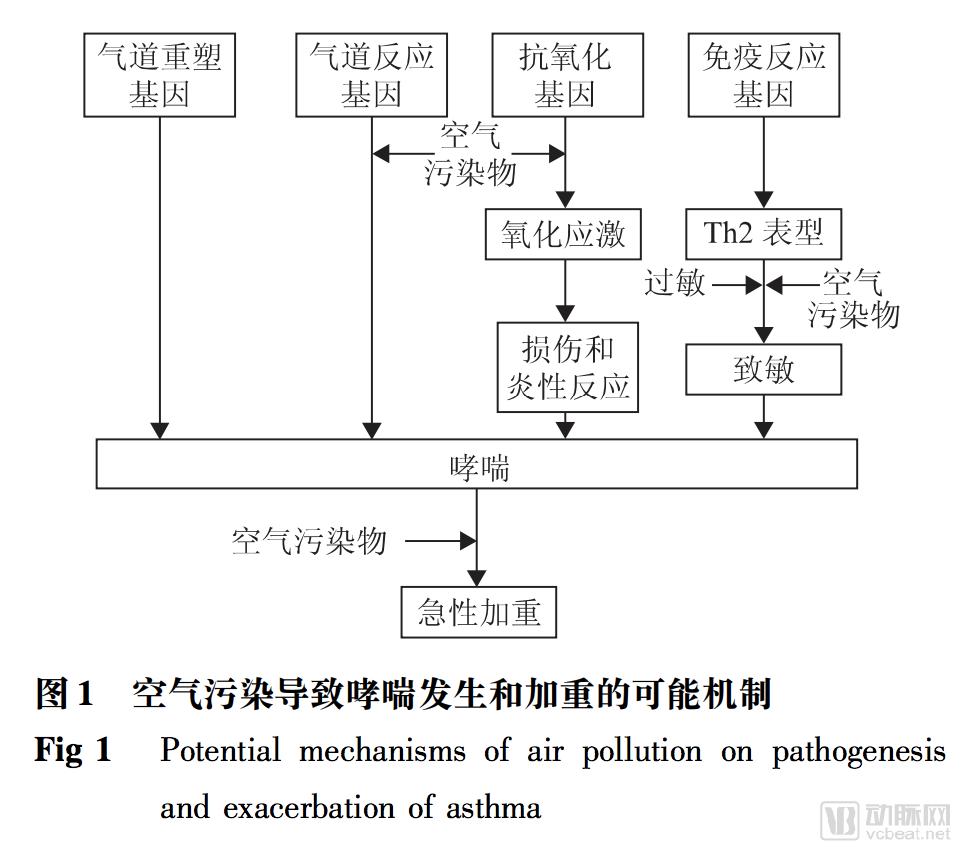

2. Genetic Susceptibility and Environmental Exposure Are the Greatest Risk Factors

The onset of asthma results from the combined effects of genetic and environmental factors. An epidemiological study indicated that 45.2% of children diagnosed with asthma have a family history of allergies. Environmental exposures involve the inhalation of substances and particles that trigger asthma, including:

· Indoor allergens, such as house dust mites in bedding, plush furniture, and pet dander, as well as home renovation materials

· Outdoor allergens, such as pollen and mold

· Tobacco Smoke

· Chemical Irritants in the Workplace

· Air Pollution

· Other triggers, such as cold air, extreme emotions like anger or fear, and physical exercise

· Certain medications, such as aspirin, other nonsteroidal anti-inflammatory drugs (NSAIDs), and blockers

Currently, smog has become a major contributor to the high incidence of asthma. The abundant PM2.5 particles in smog carry sulfates, sulfur dioxide, heavy metals, and various bacteria and viruses into the human respiratory tract. These particles cause obstruction in local lung tissues, leading to reduced ventilation in local bronchi and impaired gas exchange function in bronchioles and alveoli. Furthermore, particles adsorbed with harmful gases can irritate or even corrode the alveolar walls, or enter the systemic circulation via capillaries.

Epidemiological studies have confirmed a direct association between air pollution and acute exacerbation of symptoms, decline in lung function, and hospitalization among asthma patients. The European Study on Childhood Asthma indicated that 14% of asthma incidence and 15% of asthma exacerbations were attributable to air pollution.

Source: Chinese Journal of Clinical Immunology and Allergy

"The Negative Impact of Air Pollution on the Health of Asthma Patients"

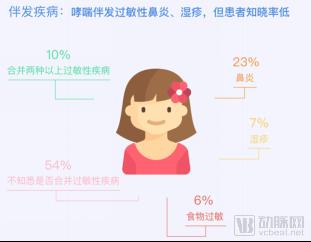

3. Complications: COPD, allergic rhinitis, eczema, etc.

Asthma and chronic obstructive pulmonary disease (COPD) are difficult to distinguish strictly, particularly among smokers and the elderly. Some patients may present with concurrent clinical features of both asthma and COPD, a condition referred to as asthma-COPD overlap (ACO). Compared with pure asthma or pure COPD, ACO is associated with more frequent exacerbations, more rapid decline in lung function, higher mortality, greater consumption of healthcare resources, and poorer prognosis. Epidemiological studies indicate that the prevalence of ACO ranges from 15% to 55%, varying by sex and age.

Asthma is often accompanied by comorbidities such as rhinitis, eczema, and food allergies; however, patient awareness of these conditions remains low.

Allergic rhinitis is closely related to asthma. Epidemiological studies have found that 60%-78% of asthma patients also suffer from allergic rhinitis, and the percentage of children with allergic rhinitis who develop bronchial asthma is approximately seven times higher than that of the general pediatric population. Typically, allergic rhinitis manifests earlier than bronchial asthma in the same individual. As both conditions are chronic inflammatory diseases of the airways, allergic rhinitis is also a risk factor for asthma. Therefore, early treatment of allergic rhinitis can reduce the incidence of asthma in later stages.

Figure 2. Complications of Asthma

Source: "White Paper on the Current Status of Asthma Management in China"

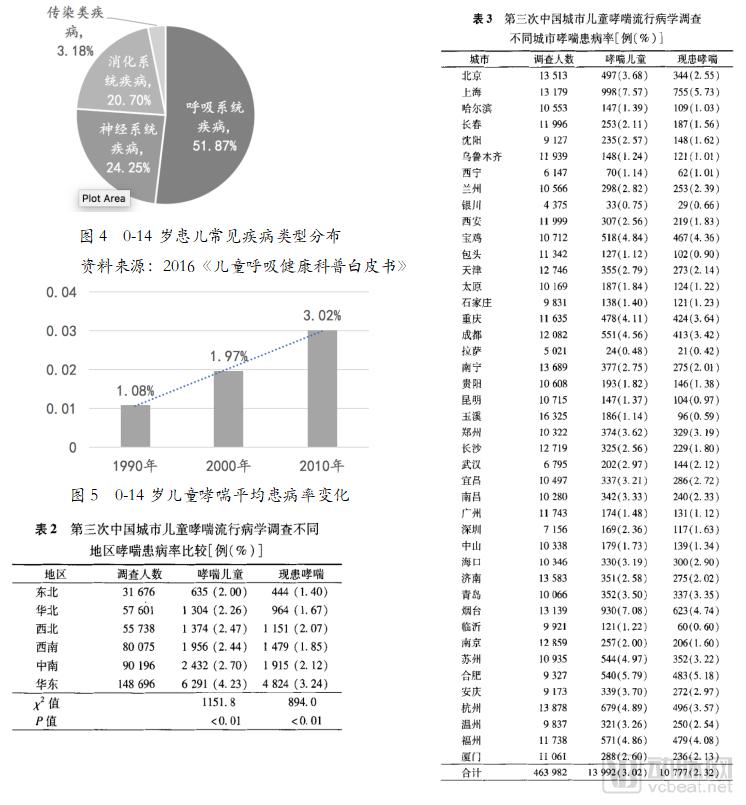

According to the 2016 White Paper on Popular Science of Children's Respiratory Health, respiratory diseases are the most prevalent condition among patients aged 0–14 years, accounting for 51.87% of cases. Among these, upper respiratory tract infections rank first at 39.27%, followed by acute bronchitis at 30.49%, pneumonia in third place at 22.20%, and bronchial asthma at 6.83%.

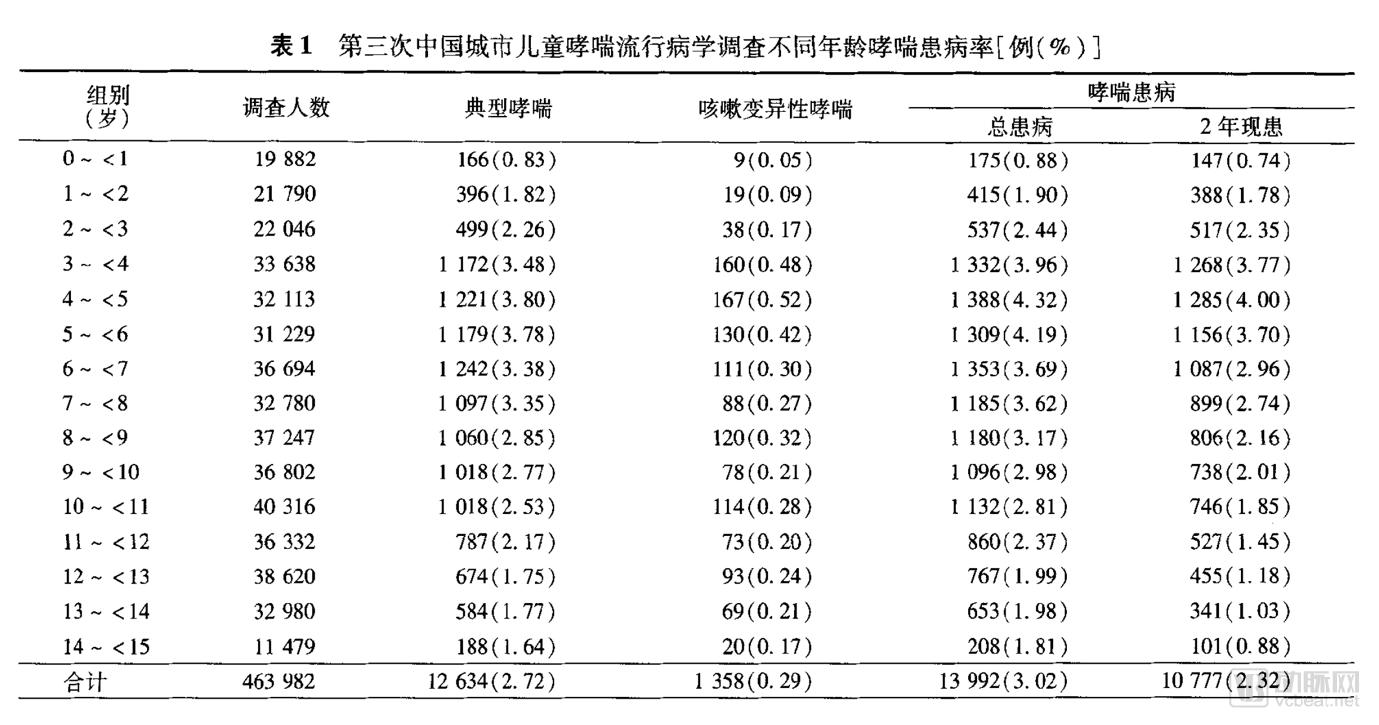

Children are a susceptible population for asthma. Among children, whose bodies are still in the developmental stage, the prevalence of asthma has shown a significant upward trend. According to the results of three national epidemiological surveys on childhood asthma in China, the average prevalence rate among children aged 0–14 years was 1.08% in 1990; this figure rose to 1.97% in 2000; and data from the third epidemiological survey of childhood asthma in Chinese cities in 2010 indicated that the prevalence rate reached 3.02%, representing an increase of approximately 50% compared with the 2000 level. In addition, the prevalence of allergic rhinitis among children has exceeded 7.5%. The prevalence of childhood asthma in China continues to rise at a rate of doubling every decade.

According to the estimates from the "Third National Epidemiological Survey of Childhood Asthma in Urban Areas of China," released in 2010, the overall prevalence of asthma among urban children aged 0–14 years in China was 3.02%, with a prevalence of 2.72% for typical asthma and 0.29% for cough-variant asthma. The primary symptom of cough-variant asthma is isolated coughing, typically manifesting as paroxysmal, non-productive, irritant dry coughs that occur predominantly at night. Patients generally do not exhibit obvious signs of upper respiratory tract infection or fever prior to the onset of coughing, making the condition prone to misdiagnosis as bronchitis.

Meanwhile, the survey revealed that asthma prevalence was higher among children aged 3–9 years, with the highest rate observed in preschoolers (aged 3–5 years) at 4.15%. Furthermore, the likelihood of asthma was significantly higher in boys than in girls, with prevalence rates of 3.51% and 2.29%, respectively.

Source: "The Third National Epidemiological Survey of Childhood Asthma in Urban China"

In terms of regional trends, East China had the highest rate (4.23%), while Northeast China had the lowest (2.00%). Among cities, Shanghai recorded the highest rate (7.57%), and Lhasa the lowest (0.48%). Chongqing (4.11%), Chengdu (4.56%), Yantai (7.08%), Suzhou (4.97%), Hangzhou (4.89%), and Hefei (5.79%) also exhibited relatively high asthma incidence rates.

Source: "The Third National Epidemiological Survey of Childhood Asthma in Urban China"

1. Diagnosis of Asthma

Diagnosis requires a combined assessment of symptoms and test results. Generally, there are two key criteria for diagnosing asthma: a history of variable respiratory symptoms and confirmation of variable expiratory airflow limitation.

"The Guidelines for the Prevention and Treatment of Bronchial Asthma in China" stipulate the diagnostic criteria as follows:

a. Recurrent episodes of wheezing, shortness of breath, chest tightness, and coughing, often associated with exposure to allergens, cold air, physical or chemical irritants, upper respiratory tract infections, and exercise.

b. Scattered or diffuse wheezes, predominantly during the expiratory phase, can be heard in both lungs.

c. The aforementioned symptoms and signs may be alleviated through treatment or resolve spontaneously.

d. Exclude wheezing, shortness of breath, chest tightness, and cough caused by other diseases.

e. For patients with atypical clinical manifestations (e.g., no obvious wheezing or physical signs), the following tests may be performed as appropriate; if any result is positive, it can support a diagnosis of bronchial asthma: (1) Measurement of peak expiratory flow (PEF) using a simple peak flow meter (diurnal variability ≥20%). (2) Positive bronchodilator response [forced expiratory volume in one second (FEV1) increase ≥12%, and absolute increase in FEV1 ≥200 mL].

A diagnosis of bronchial asthma can be made in patients who meet criteria 1–4 or criteria 4 and 5.

To assist in the diagnosis of asthma, pulmonary function testing and allergen skin testing can be performed.

(1) Pulmonary Function Testing:

· Pulmonary ventilation function test: It is one of the important bases for diagnosing asthma and assessing the degree of asthma control. Units with appropriate conditions may conduct ventilation function tests;

· PEF and its variability: Measuring the diurnal variability of peak expiratory flow (PEF) using a simple peak flow meter aids in the diagnosis and disease assessment of patients with atypical asthma;

· Bronchial provocation test: This test can determine the presence of airway hyperresponsiveness. For patients with atypical asthma, referral to a qualified facility for bronchial provocation testing is recommended to aid in the diagnosis of asthma.

· Bronchodilator Reversibility Test: Assesses the reversibility of airflow limitation and aids in the diagnosis of asthma.

(2) Allergen skin test:

· The atopic status of asthma patients can be confirmed through allergen skin testing, which helps identify risk factors contributing to the onset and exacerbation of individual asthma cases, and also aids in selecting patients suitable for specific immunotherapy.

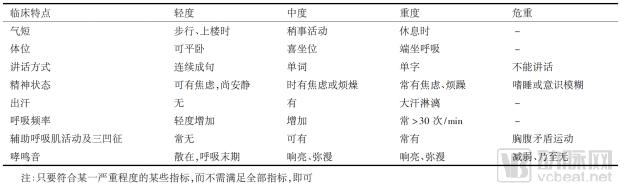

2. Severity Classification of Asthma

Table 4. Classification of Severity in Acute Asthma Exacerbations |

|

Source: Guidelines for the Prevention and Treatment of Bronchial Asthma in China |

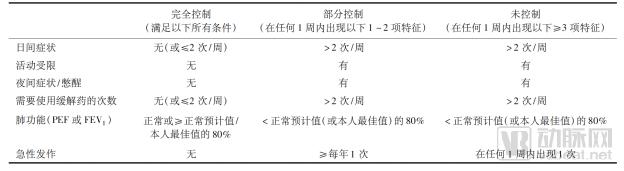

3. Classification of Asthma Control Levels

Table 5 Levels of Asthma Control

Source: "Guidelines for the Prevention and Treatment of Bronchial Asthma in China"

4. Current Status and Pain Points in Asthma Control

Currently, the management of asthma in China exhibits three major characteristics: a rapid increase in the number of patients, a high rate of acute exacerbations, and a low level of disease control.

A survey by the China Asthma Alliance reported that approximately 66% of patients in China experienced asthma exacerbations in the past year, with 26.8% requiring acute treatment and 16.2% needing hospitalization due to these exacerbations. According to the Global Initiative for Asthma (GINA) guidelines, only 2% of patients achieved complete control, while 51% had partial control, meaning that more than half of the patients did not have their asthma under control. However, GINA states that asthma can actually be controlled in 85% of patients.

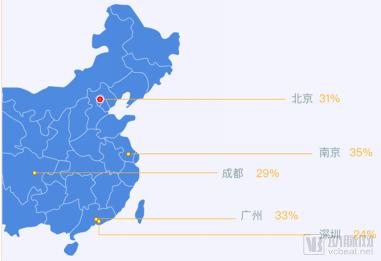

In terms of regional analysis, Nanjing, Guangzhou, and Beijing ranked as the top three cities in asthma control rates, with rates of only 35%, 33%, and 31%, respectively; nearly 70% of asthma patients remained uncontrolled.

Figure 6. City Rankings for Asthma Control Rates

Source: White Paper on the Current Status of Asthma Management in China

The overall control rate of childhood asthma in China is also unsatisfactory. On May 12, 2018, VCBeat reported that 53% of childhood asthma cases were uncontrolled, 44% were partially controlled, and only 2.5% of pediatric asthma patients achieved well-controlled status. Furthermore, nearly one-third of affected children did not receive timely and accurate diagnoses.

Currently, China’s asthma mortality rate stands at 36.7 per 100,000 population, ranking first globally.

The primary reason is poor treatment adherence among patients. It has been reported that the adherence rate to inhaled corticosteroid therapy in asthma patients is less than 50%. In one survey, 83 out of 160 children exhibited resistance to traditional nebulizers.

Second, the excessive economic burden caused by recurrent disease conditions. According to a study published by the General Hospital of Shenyang Military Region in 2015, among asthma patients hospitalized for 5–15 days, the average hospitalization cost per patient with asthma alone was RMB 6,459; however, the vast majority of patients had comorbidities, and the average cost per patient with more than eight comorbidities reached as high as RMB 37,394.

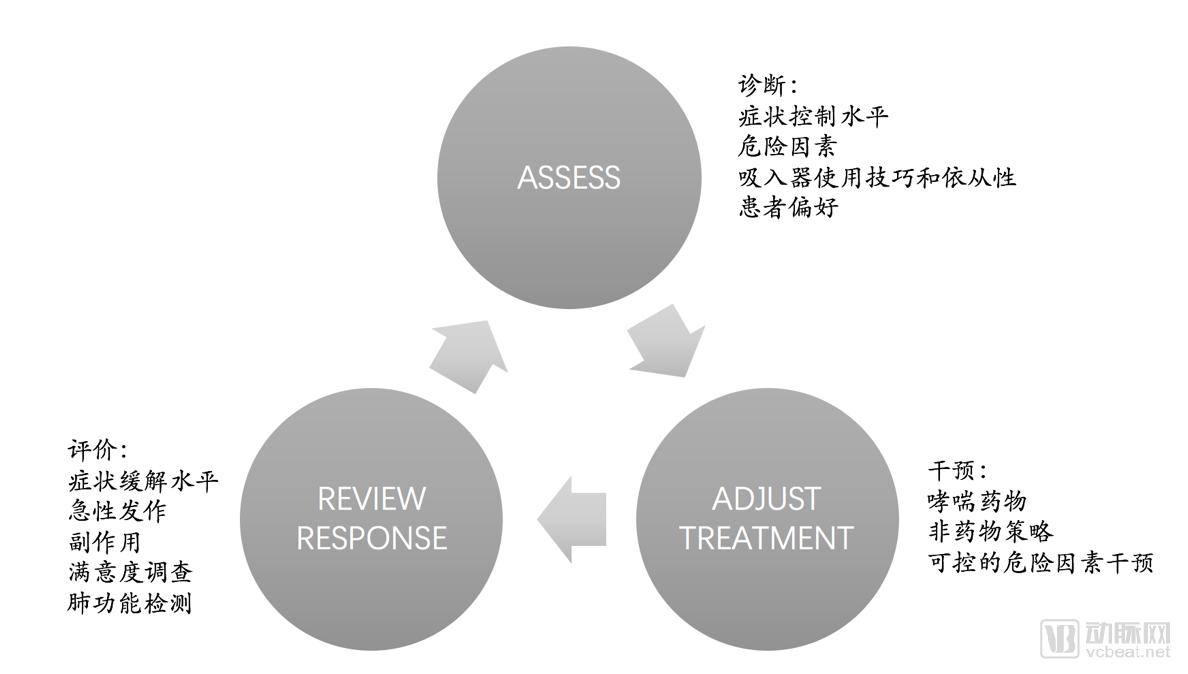

5. Consumption Characteristics: Treatment and Control

The goal of asthma treatment is to achieve long-term symptom control and prevent future risks. This involves managing the patient’s internal disease status (addressing intrinsic factors) and controlling environmental conditions by avoiding asthma triggers (addressing extrinsic factors).

Specific measures include: 1. Avoidance of allergens; 2. Symptomatic treatment; 3. Desensitization therapy; 4. Patient education.

Figure 7. Symptomatic Treatment Cycle for Asthma Management

Source: Global Initiative for Asthma (GINA)

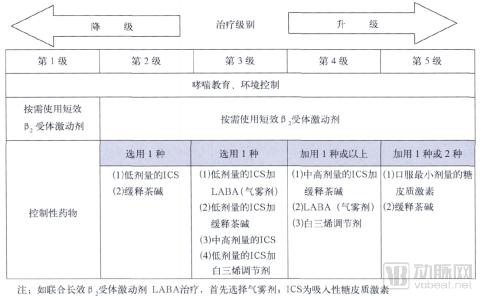

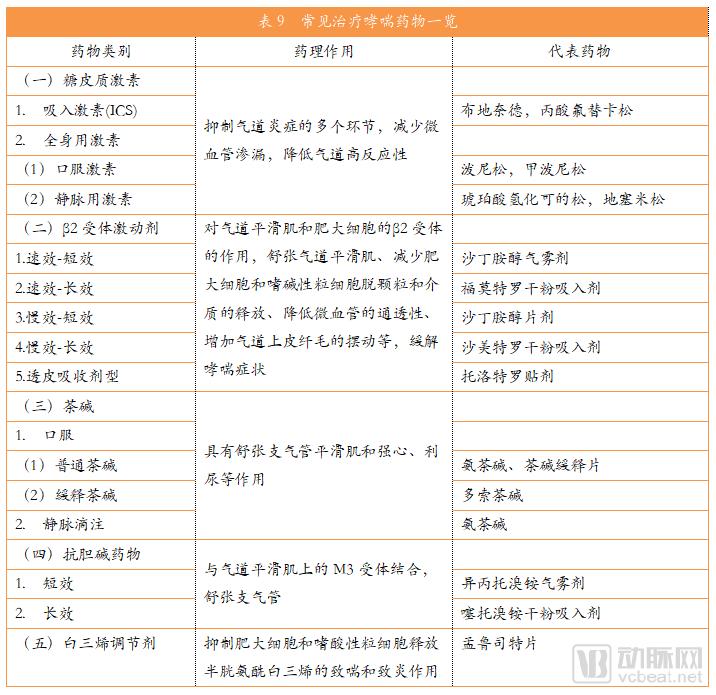

Currently, the main drugs used to treat asthma fall into five major categories: glucocorticoids, β2-adrenergic agonists, leukotriene receptor antagonists, theophyllines, and anticholinergics. Different medications are selected based on the urgency and severity of the patient’s condition; patients with moderate-to-severe or critical asthma require combination therapy.

Table 6 Treatment Plan Based on Asthma Control Levels

Source: Guidelines for the Prevention and Treatment of Bronchial Asthma in China

In recent years, as issues such as poor patient adherence, uncontrollable risk factors, the lack of effective analysis of recurrent episodes, and the difficulty of managing large volumes of data have garnered increasing attention, asthma management products leveraging digital technologies have gradually emerged. These innovations have promoted multidimensional improvements in asthma control, encompassing mobile health, telemedicine and remote monitoring, wearable devices, and artificial intelligence.

Digital management products, such as smart inhalers that monitor asthma medication usage, improve drug adherence; disease and trigger monitoring enable personalized management to reduce the risk of exacerbations; and information systems, data value, and artificial intelligence enhance the efficiency of asthma care management. These represent the future development trends in the asthma industry.

Figure 8. Three Entry Points for Innovative Technologies to Improve Asthma Disease Management

Source: White Paper on the Current Status of Asthma Management in China

In recent years, the incidence of respiratory diseases has increased year by year. The prevention and monitoring of respiratory diseases have received widespread attention from all sectors of society. The government is also improving relevant policies, with the State Council, the National Health and Family Planning Commission, and other authorities issuing multiple documents to deploy measures for the prevention, control, and treatment of respiratory diseases.

1. Analysis of National Macro-Control Policies

2. Analysis of Policies Related to the Anti-Asthma Industry

Furthermore, in recent years, as the outflow of hospital prescriptions has gradually deepened, most anti-asthma medications, which are prescription drugs, have ushered in new opportunities for sales growth at retail terminals. According to data from Menet’s Drug Retail Monitoring and Analysis System, sales of anti-asthma medications in more than 4,500 sample pharmacies across 22 key cities have risen year by year, although the growth rate has slowed slightly; the compound annual growth rate (CAGR) from 2013 to 2015 was 10.5%.

1. Treatment Modalities: Classification of Anti-Asthma Medications

Asthma is difficult to cure completely. Common anti-asthma medications can be divided into two major categories: controller medications and reliever medications:

(1) Controller medications: These prevent asthma attacks by suppressing airway inflammation and require daily long-term use. Including:

· Inhaled corticosteroids (ICS) are the preferred controller medication

· Sustained-release theophylline

· Leukotriene modifiers, with montelukast tablets as the representative drug

· Long-acting β2-agonists/inhaled corticosteroids (LABA/ICS), representative drugs include: GSK’s Advair (salmeterol/fluticasone) and AstraZeneca’s Symbicort Turbuhaler

(2) Relief medications: These can rapidly relieve bronchial smooth muscle spasm and alleviate asthma symptoms, and are typically used on an as-needed basis. Including:

· Short-acting inhaled β2-adrenergic agonists (SABA), with representative products including GSK’s Ventolin and TEVA’s ProAir

· Systemic glucocorticoids

· Inhaled short-acting anticholinergic drugs, etc.

2. Market Size of the Anti-Asthma Drug Industry

With the number of asthma patients increasing year by year, the market size for anti-asthma medications is also expanding annually. According to estimates by the World Health Organization, the global potential market for asthma drugs exceeded $18 billion in 2016 and has been growing at an annual rate of 2.4%, with projections indicating it will reach $18.9 billion this year.

According to a survey by VCBeat’s Eggshell Research Institute, the sales volume of China’s anti-asthma drug market grew from RMB 13.3 billion in 2012 to approximately RMB 18 billion in 2015, representing a compound annual growth rate (CAGR) of around 15%. It is projected to reach RMB 27.4 billion this year.

A simple calculation shows that there are currently nearly 30 million asthma patients in China. If 10% of these patients have good adherence and spend RMB 300 per month on anti-asthma medications, the annual expenditure will amount to RMB 10.8 billion; for the remaining 90% of patients, who spend an average of RMB 300 on anti-asthma medications every six months, the annual expenditure will reach RMB 16.2 billion; the total comes to RMB 27 billion, which supports the data mentioned above.

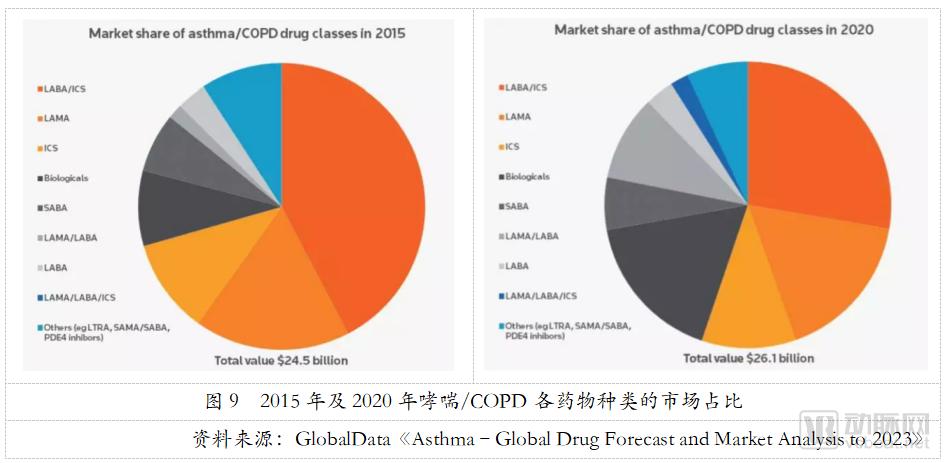

Regarding branded asthma medications, Clarivate Analytics’ Cortellis estimates that the global market for branded asthma/COPD drugs was valued at USD 24.46 billion in 2015 and is projected to remain stable at approximately USD 26.06 billion in 2020, indicating steady market growth. Among these, the share of LABA/ICS combinations is expected to decline slightly but will still hold the leading position. Meanwhile, biologics and long-acting muscarinic antagonist/long-acting beta2-agonist (LAMA/LABA) combinations are poised for rapid development, with their market shares increasing substantially.

3. Market Landscape of the Anti-Asthma Drug Industry

(1) Imported Drugs and Domestically Produced Drugs

China's asthma medications are primarily dependent on imported drugs.

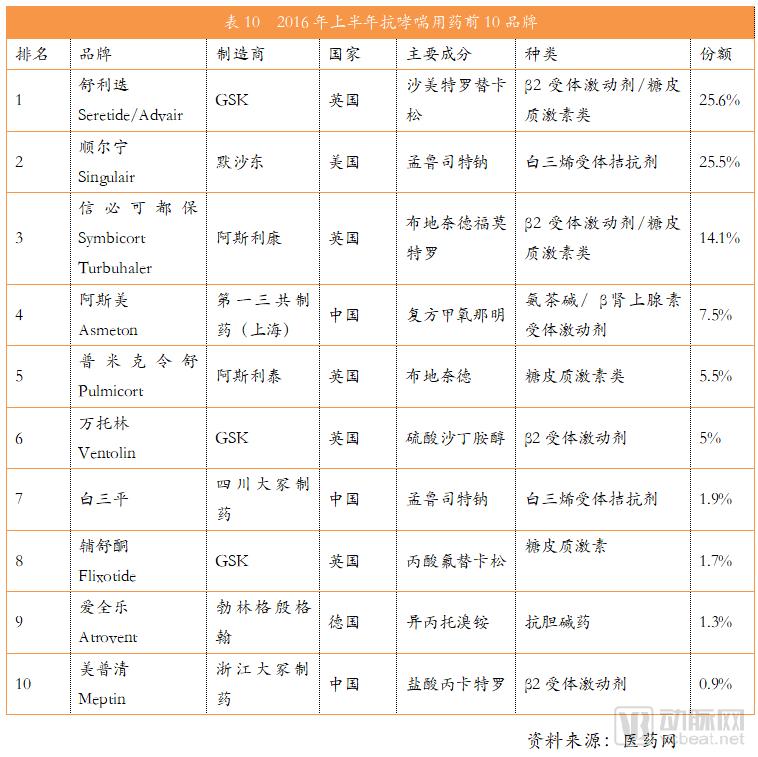

In the first half of 2016, the top ten anti-asthma drugs in the domestic market were Seretide, Singulair, Symbicort Turbuhaler, Asmeton, Pulmicort Respules, Ventolin, Bailiping, Flixotide, Atrovent, and Meptin, accounting for a total of 89% of the market share. However, among these, only three were domestically produced—Asmeton, Bailiping, and Meptin—with their combined market share amounting to just 10.3%.

Domestic substitute drugs frequently contain chlorofluorocarbons (CFCs). However, with the implementation of new policies in 2016, China will no longer approve exemptions for the pharmaceutical use of CFCs and will gradually phase out medicinal inhalers containing CFCs. This development poses further challenges to the research and development of domestically produced drugs.

(2) Chemical Drugs, Traditional Chinese Medicine Patent Drugs, and Biological Drugs

Anti-asthma medications can be broadly categorized into chemical drugs, traditional Chinese medicine (TCM) proprietary medicines, and biologics, with chemical drugs dominating the market.

Chemical drugs encompass a wide variety of products and diverse dosage forms. Classified by physical form, they include aerosols (comprising pressurized metered-dose inhalers, sprays, and dry powder inhalers), tablets, pills, capsules, solutions, injections, patches, powders, and granules. Among these, aerosol formulations hold a dominant market share of approximately 50%. As inhaled medications, they deliver drugs directly to the lungs, ensuring uniform distribution and rapid onset of action, while effectively minimizing gastrointestinal irritation and resulting in relatively fewer adverse reactions. Tablets account for roughly 30% of the market, favored for their stable quality, accurate dosing, and convenience in administration and portability. Capsules and solutions follow as the next most prominent categories.

The market share of proprietary Chinese medicines accounts for less than 10%, with a limited number of brands and low market concentration. In terms of dosage form distribution, tablets hold more than half of the market share, followed by pills and capsules in descending order. Among these, pills are gaining market share year by year and demonstrating strong growth potential, owing to advantages such as slow disintegration and drug release, prolonged therapeutic effect, reduced toxicity and irritation, and fewer adverse reactions.

In recent years, the research and development of biologics has garnered increasing attention, with promising market growth expected in the future. Biologics have demonstrated significant therapeutic efficacy in treating severe persistent asthma. Representative agents include Xolair (omalizumab injection), developed by Novartis and Genentech (a member of the Roche Group), and Nucala (mepolizumab), developed by GSK.

In addition, new biologics such as dupilumab (pre-registration), jointly developed by Sanofi and Regeneron, are currently in the late stages of development. The market launch of these products will provide patients with more treatment options in the biologics market for asthma. According to Cortellis Competitive Intelligence, the global biologics market for asthma and COPD is projected to exceed $4.425 billion in 2020, with a corresponding market share of 17% and a growth rate of 14.87%.

4. Case Study: Analysis of the Enterprise and Its Products

GlaxoSmithKline

GlaxoSmithKline (GSK) is a giant in the anti-asthma drug industry. Its best-selling anti-asthma medications include Seretide/Advair, the leading LABA/ICS combination; Ventolin, a β2-adrenergic agonist; Flixotide, a glucocorticoid; and Nucala (mepolizumab), a biologic agent. Together, these products account for more than 30% of the total market share.

Advair is a salmeterol/fluticasone inhaler that was first launched in 1999, becoming the world’s first long-acting beta2-agonist/inhaled corticosteroid (LABA/ICS) combination therapy. According to Clarivate Analytics data, Advair achieved global sales of $5.661 billion in 2015, making it the best-selling anti-asthma/COPD medication worldwide. However, Advair also faces pressure from generic competitors. It is reported that more than 20 companies, including Mylan UK, Novartis Shanghai, Hengrui Medicine, Chia Tai Tianqing, and Shandong Jingwei, have filed applications for the development of generic versions of Advair. Currently, however, the market penetration rate of generics remains low, posing a limited competitive threat to the originator drug.

In addition, GSK has also launched the new drug Breo Ellipta (vilanterol/fluticasone), the world’s first once-daily LABA/ICS combination therapy for the treatment of asthma in patients aged 18 years and older.

GSK’s other blockbuster drug, Ventolin, a salbutamol sulfate inhaler launched in 1969, is the leading product among short-acting β2-agonists (SABAs). Clarivate Analytics predicted that global sales of Ventolin would reach $928 million in 2015 and $1.043 billion by 2020.

Flixotide is a fluticasone propionate aerosol, a glucocorticoid medication with potent local anti-inflammatory and anti-allergic effects. The patent for Flixotide expired in 2011. Currently, no generic fluticasone propionate aerosols have been approved for marketing in China; however, fluticasone propionate creams manufactured by Zhejiang Xianju Pharmaceutical Co., Ltd. and Hubei Hengan Pharmaceutical Co., Ltd. are already on the market.

In the field of biologics, GSK developed Nucala (mepolizumab), the world’s first anti-IL-5 agent, providing a new therapeutic option for patients with severe asthma. Data indicate that Nucala significantly improves asthma control in patients whose condition remains uncontrolled despite treatment with Xolair (omalizumab), an asthma biologic co-marketed by Novartis and Roche. The drug received FDA approval in December 2015. According to GlaxoSmithKline’s 2016 annual report, global sales of Nucala amounted to $127 million in 2016. Although the product has not yet been approved for import into China, GlaxoSmithKline’s clinical trial application for import has been approved.

Figure 10 Overview of Selected GlaxoSmithKline Anti-Asthma Medications

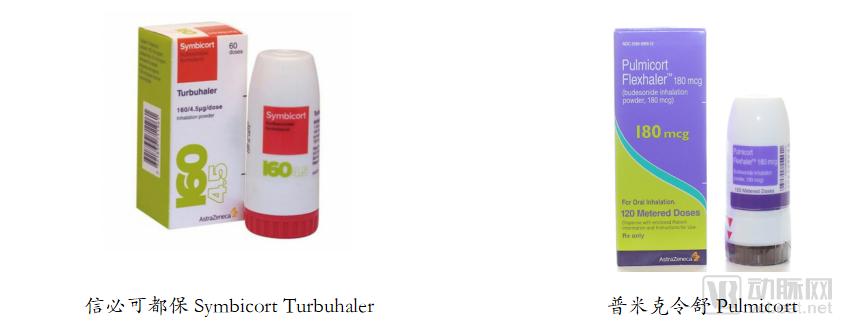

AstraZeneca

AstraZeneca boasts best-selling products including Symbicort Turbuhaler and Pulmicort.

Symbicort is an asthma medication launched by AstraZeneca in 2007. Its active ingredients are formoterol and budesonide, classifying it as a LABA/ICS combination therapy. Symbicort forms fatty acid esters within the airways; its water-soluble components exhibit significant binding to mucosal tissues, resulting in sustained action. Systemic adverse reactions are rare at therapeutic doses. It is primarily indicated for the long-term maintenance treatment of asthma in adults and children aged 12 years and older to control airway inflammation.

Furthermore, patients’ lung function improves within 15 minutes after medication administration. In 2013 and 2014, Symbicort’s global annual sales increased by 12.9% and 15.4% year over year, respectively. According to data from the HDM system, spending on Symbicort in public hospitals in key Chinese cities was projected to reach RMB 286 million in 2017, representing a 15.03% year-over-year increase.

Pulmicort is an inhaled corticosteroid medication whose active ingredient is budesonide. It is currently the first-line drug for the long-term management of asthma. As a maintenance therapy, Pulmicort plays a positive role in the treatment of glucocorticoid-dependent bronchial asthma, non-glucocorticoid-dependent asthma, and chronic obstructive pulmonary disease (COPD). It can be used to control and prevent asthma symptoms in children aged 12 months to 8 years. According to Clarivate Analytics data, global sales of Pulmicort reached USD 1.014 billion in 2015 and were projected to reach USD 1.2 billion by 2020. Data from the HDM system indicate that spending on budesonide in key public hospitals across major Chinese cities was estimated at RMB 639 million in 2017, representing a year-on-year increase of 13.99%.

In the field of biologics, AstraZeneca’s anti-interleukin-13 (IL-13) monoclonal antibody, tralokinumab, has entered Phase III clinical trials. However, late last year, two Phase III trials—STRATOS 2 and TROPOS—evaluating tralokinumab for the treatment of patients with severe uncontrolled asthma both failed to meet their primary endpoints, marking the failure of tralokinumab in this indication. AstraZeneca is currently conducting another Phase II study to investigate tralokinumab for the treatment of mild-to-moderate idiopathic pulmonary fibrosis (IPF).

Figure 11 Overview of Select AstraZeneca Anti-Asthma Medications

Merck & Co.

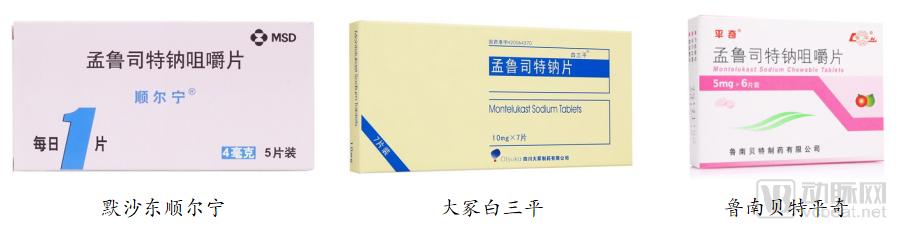

Merck & Co. holds the blockbuster leukotriene receptor antagonist Singulair (montelukast sodium), an oral anti-asthma medication administered once daily.

Montelukast binds with high selectivity to receptors in the human airways, specifically inhibiting cysteinyl leukotriene (CysLT1) receptors, thereby alleviating airway inflammation and effectively controlling asthma symptoms. It can be used as a long-term medication for patients with mild, moderate, and severe asthma. In combination therapy, it can reduce the dosage of inhaled corticosteroids in patients with moderate-to-severe asthma and enhance their clinical efficacy. It is widely used for the prevention and long-term treatment of asthma in adults and children, including the prevention of daytime and nighttime asthma symptoms, and to some extent, can "treat asthma at its root."

Singulair was first launched in 1998 and reached its sales peak in 2011, significantly outperforming other anti-asthma medications with global sales reaching $5.924 billion. However, in recent years, due to patent expiration and the rise of generic drugs, its sales have declined year by year. According to data from Clarivate Analytics, Singulair’s global market sales were only $1.297 billion in 2015 and dropped to $732 million in 2017, with projections indicating a further decline to $538 million by 2020.

Currently, the U.S. FDA has approved abbreviated new drug applications (ANDAs) for generic montelukast from more than ten pharmaceutical manufacturers. In China, montelukast sodium tablets (10 mg) and montelukast sodium chewable tablets (5 mg) have been approved for marketing, while 43 additional products (measured by acceptance numbers) have received clinical trial approval, indicating intense market competition.

IMS data show that in the montelukast market at public hospitals in key Chinese cities during the first three quarters of 2017, Merck & Co.’s oral tablets, granules, and chewable tablets under the brand name “Singulair” accounted for 75.31%, Otsuka’s chewable tablets “Baisanping” accounted for 13.29%, and Lunan Better’s chewable tablets “Pingqi” accounted for 11.4%.

Figure 12 Singulair and Its Generic Drugs

Teva Pharmaceuticals

Israel’s pharmaceutical giant Teva owns anti-asthma drugs, including the biologic reslizumab (Cinqair) and ProAir RespiClick, an inhaled powder formulation of albuterol sulfate.

ProAir RespiClick is the first FDA-approved, breath-actuated dry powder inhaler for the treatment of acute asthma symptoms, demonstrating excellent efficacy in managing acute asthma exacerbations. ProAir contains albuterol sulfate, a short-acting beta-agonist (SABA), in powdered form. It is indicated for patients aged 12 years and older with asthma to treat and prevent bronchospasm associated with reversible obstructive airway disease, as well as to prevent exercise-induced bronchospasm. According to Clarivate Analytics data, the market size for ProAir was $549 million in 2015; however, due to competition from generic drugs, it is projected to decline to $350 million by 2020.

Figure 13 Overview of Selected Teva Pharmaceuticals’ Anti-Asthma Medications

Cinqair, a biologic agent targeting the same mechanism as Nucala, is a fully human monoclonal antibody against IL-5. Approved by the FDA in March 2016, it reduces exacerbations in patients with severe eosinophilic asthma, while improving lung function and alleviating asthma severity, making it suitable for the treatment of eosinophilic asthma. Common adverse reactions include elevated blood creatine phosphokinase levels, myalgia, and allergic reactions. This product has not yet been approved for import into China, and there are currently no domestic or import application records.

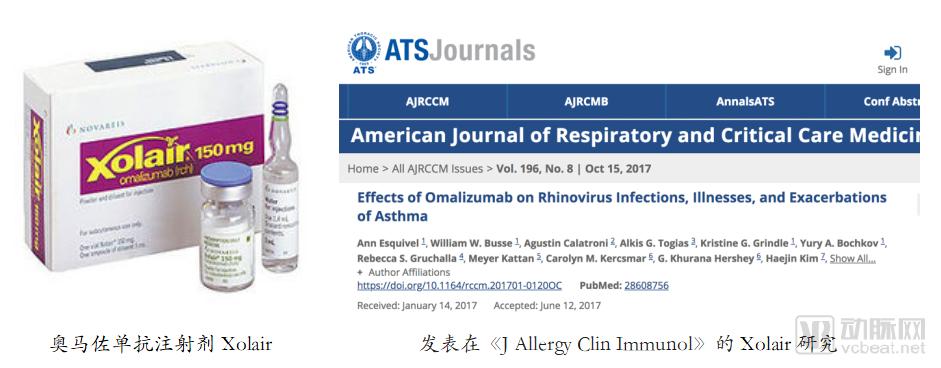

Novartis and Roche

Xolair (omalizumab), a biologic injection developed by Novartis and Genentech (a member of the Roche Group), was launched in 2003 as the first and currently only anti-IgE therapy approved by the U.S. Food and Drug Administration (FDA) for persistent allergic asthma. Omalizumab is a humanized anti-IgE antibody that reduces levels of free IgE in plasma and blocks the binding of IgE to its receptors on mast cells and basophils, thereby achieving therapeutic effects. It is indicated for the treatment of allergic conditions such as asthma, chronic idiopathic urticaria, and eczema, and demonstrates a favorable safety and tolerability profile.

According to Clarivate Analytics data and Novartis’ 2016 annual report, global sales of Xolair reached $2.082 billion in 2015 and $2.378 billion in 2016, and are projected to exceed $2.797 billion by 2020.

On August 24, 2017, China’s CFDA approved Novartis’ omalizumab injection, marketed as Xolair, for the treatment of adults and adolescents aged 12 years and older with moderate-to-severe persistent allergic asthma whose symptoms remain inadequately controlled despite therapy with inhaled corticosteroids (ICS) and long-acting beta₂-agonists (LABA), thereby providing a cutting-edge therapeutic option in the field of targeted anti-allergic and asthma treatments.

Figure 14. Omalizumab Injection Xolair and Related Literature

The large base of asthma patients is increasing year by year.

Currently, there are nearly 30 million asthma patients in China, and this figure is projected to reach 45 million by 2025. However, as a chronic disease, asthma can only be controlled, not cured; furthermore, the number of patients continues to rise year by year due to worsening air pollution.

Poorer Medication Adherence in Pediatric Asthma Warrants Focused Attention

Children are a susceptible population for asthma. The overall prevalence of asthma among urban children aged 0–14 years in China is 3.02%; it is projected that by 2015, there will be 12 million urban pediatric asthma patients in China. Children with asthma have more sensitive airways and poorer medication adherence, necessitating personalized guided treatment.

The Traditional Anti-Asthma Drug Market Remains Stable, with a Scale Reaching RMB 27.4 Billion

Currently, there are nearly 30 million asthma patients in China. If 10% of these patients have good adherence and spend 300 yuan per month on anti-asthma medications, the annual expenditure will amount to 10.8 billion yuan; the remaining 90% of patients spend an average of 300 yuan every six months on anti-asthma medications, resulting in an annual expenditure of 16.2 billion yuan; the total comes to 27 billion yuan. This figure supports the 27.4 billion yuan reported by VCBeat’s VBInsight. Meanwhile, the compound annual growth rate is approximately 15%.

China's asthma medications rely heavily on imports, dominated by foreign pharmaceutical companies GlaxoSmithKline, AstraZeneca, and Merck & Co.

Currently, the domestic anti-asthma drug market relies heavily on imports. Among the top ten drugs, only three are domestically produced—Asmeton, Baiping, and Meipulinqing—accounting for just 10% of the total market share. GlaxoSmithKline, AstraZeneca, and Merck & Co. each hold approximately 25% of the market share.

Biopharmaceutical R&D is gaining increasing attention, with promising future market growth.

Biologics have demonstrated favorable therapeutic efficacy in the treatment of severe persistent asthma. Currently, major multinational pharmaceutical companies, including GlaxoSmithKline, Roche, and Sanofi, are actively exploring biologic therapies for asthma. The global biologics market for asthma and chronic obstructive pulmonary disease (COPD) is projected to exceed USD 4.425 billion in 2020, corresponding to a market share of 17%. On August 24, 2017, China’s Food and Drug Administration (CFDA) approved Novartis’s omalizumab injection, marketed under the brand name Xolair.