Why WeDoctor, LinkDoc, and Medlinker Are Rushing to Embrace State Capital: The Real Reasons Behind the Trend

2018 was destined to be an extraordinary year for domestic companies involved in medical big data. It all seemed to begin after Haihong Holdings changed its name to Guoxin Health.

Prior to the capital injection by China Venture Capital Fund, Haihong Holdings reported operating revenue of RMB 184 million in 2017, a year-on-year decrease of 15.15%; net profit attributable to shareholders of the listed company stood at RMB 17 million, down 40.49% year on year. By April, following its corporate name change, Haihong Holdings’ market capitalization had exceeded RMB 40 billion, doubling from its pre-adjustment level before the introduction of state-backed investors and business restructuring.

Following Haihong, several other Chinese companies involved in medical big data—WeDoctor, LinkDoc Technology, Quanyu Medical, and Medlinker—have also successively attracted the favor of state-owned capital, with each securing financing exceeding RMB 500 million.

VCBeat has previously published analyses noting that state-owned capital’s investments in the healthcare sector are predominantly concentrated at Series A and later stages, favoring companies whose business models have already been validated by the market and investors. Most of these companies are unicorns within China’s healthcare industry.

VCBeat’s analysis suggests that the alliance between medical big data companies and state-owned capital is no accident, but an inevitable move as the industry reaches a certain stage of development. In this regard, it is necessary to clarify three points:

1. What is the background behind medical big data-related companies successively introducing state-owned capital this year?

2. Why was 2018 a turning point for the state ownership of companies in the healthcare big data sector?

3、What new industry opportunities can state-owned capital bring to unicorn companies that were previously unavailable?

With these questions in mind, VCBeat consulted the heads of several medical big data companies in China.

Question 1: What is the background behind the successive introduction of state-owned capital into medical big data-related enterprises this year?

Why Is State-Owned Capital Actively Participating in Investments in Private Enterprises?

On December 12, 2017, Peng Huagang, Deputy Secretary-General of the State-owned Assets Supervision and Administration Commission (SASAC), stated at the China Listed Companies Summit that SASAC would intensify its efforts to develop a mixed-ownership economy, promoting complementary advantages, mutual reinforcement, and common development among capital of various ownership types.

According to VCBeat, there are currently three main models of mixed-ownership reform for enterprises in China: first, introducing non-state capital to participate in the reform of state-owned enterprises;Second, state-owned capital is encouraged to acquire equity stakes in non-state-owned enterprises through various means, with state-owned capital investment and operating companies making equity investments in non-state-owned enterprises that demonstrate significant development potential and strong growth prospects.; third, to explore the implementation of employee stock ownership in mixed-ownership enterprises. Employee stock ownership is primarily achieved through methods such as capital increase and share expansion, or by contributing capital to establish new entities; additionally, indirect stock ownership methods such as debt-to-equity swaps are also utilized.

The second factor is the primary driver for state-owned capital investing in private enterprises. These three mixed-ownership reform approaches correspond to the three major types of mixed ownership:

(I) Mixed-ownership enterprises jointly composed of public and private ownership

It can be further subdivided into two forms: one is enterprises formed by the joint venture of state-owned or collective economies with foreign capital, such as Chinese-foreign cooperative operations and joint ventures; the other is enterprises formed by the union of state-owned or collective economies with domestic private economies.

(2) Mixed-ownership enterprises formed by the combination of public ownership and individual ownership

This includes enterprises that have absorbed partial equity holdings by their own employees during the shareholding system reform of state-owned enterprises, as well as mixed-ownership enterprises in collective economies implementing the joint-stock cooperative system, where collective ownership is combined with individual ownership.

(3) Mixed-ownership enterprises jointly formed by state-owned enterprises and collective enterprises within the public ownership sector

such as a consortium composed of urban state-owned enterprises and rural township enterprises or urban collective enterprises.

Furthermore, Peng Huagang noted that, under the premise of effectively fulfilling responsibilities for the operation of state-owned assets, state capital should grant enterprises more comprehensive operational autonomy. It is essential to ensure that regulatory oversight extends wherever state capital is invested, thereby substantially enhancing the effectiveness of state-owned asset supervision. This statement also indicates that the role of state capital extends beyond merely providing funding; it also serves as an industry regulator. For the relatively sensitive sector of medical big data, the entry of state capital is therefore inevitable.

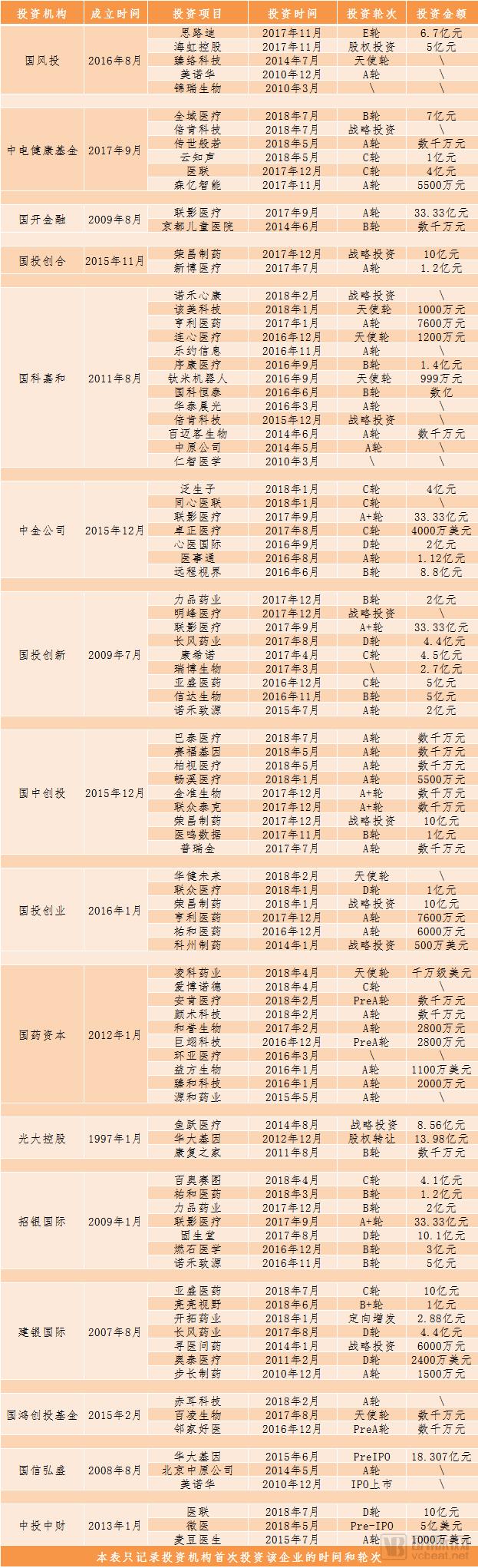

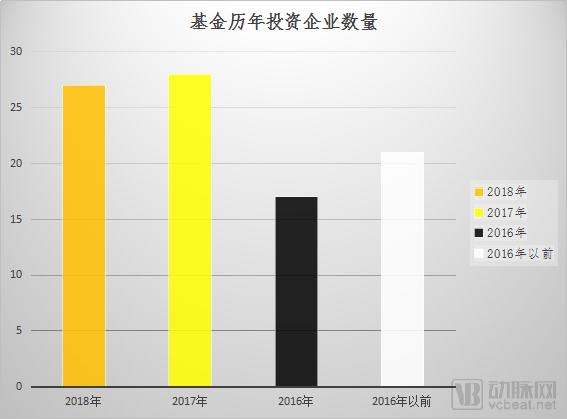

To clarify the development trends of mixed-ownership economies in the healthcare sector, VCBeat has compiled data on investment and financing activities in the healthcare industry by major state-owned funds (see table below). As shown in the table, the vast majority of these funds were established before 2016. Since 2016, these state-owned capital entities have not only seen a substantial increase in the number of investments but also demonstrated a year-on-year growth trend. Notably, in 2018, despite only half of the year having passed, the number of investments had already nearly reached the total for 2017, underscoring the significant impact of macroeconomic policies.

Data sources: VCBeat Knowledge Base, Tianyancha

Data Sources: VCBeat Knowledge Base, Tianyancha

Nowadays, promoting the development of big data has become a national imperative. Starting with the issuance of Document No. 47 by the General Office of the State Council, which aims to promote and standardize the application of health and medical big data, health and medical big data has been designated as a critical foundational strategic resource for the nation. Similar to state-controlled resources such as oil and electricity, the positional attributes and strategic significance of big data are self-evident.

Whether in terms of overall strategy or the healthcare sector, national plans cover everything from top-level design to data privacy, security mechanisms, standardization, data sharing, and business models. Regarding data openness, government-level planning, regulation, and safeguards are required for post-sharing data oversight, as well as for data privacy and security protection.

The development of the medical big data industry is primarily hindered by two issues: first, the integration challenges associated with data interoperability, and second, deficiencies in data-sharing mechanisms. By leveraging state power in conjunction with industrial capital, it is possible to effectively address interoperability integration challenges, establish a sharing mechanism for the health and medical big data sector, and build an industry-wide sharing platform. This will better facilitate the practical application and implementation of big data and artificial intelligence in the healthcare and pharmaceutical industries.

Question 2: Why was 2018 a turning point for the state-led consolidation of healthcare big data companies?

Chen Daoguang, Vice President of Quanyu Medical, believes that after several years of development, the medical big data industry has entered a new phase, with leading enterprises emerging in various sub-sectors. These companies have established clear business models and identified corresponding monetization strategies, which serve as the prerequisite for the entry of state-owned capital.

Since the pilot phase, enterprises have been continuously updating and iterating their systems, refining their products, including data applications. However, bottlenecks have emerged across the industry, such as issues related to equipment, data security, and the appropriate scope of data utilization. In particular, concerns regarding national security have constrained the development of medical big data.

In the later stages of financing, companies need to build on their early-stage foundations to enter periods of rapid growth and explosive expansion. Therefore, they must aggressively expand their market reach to benefit more patients. At this stage, endorsement from public hospitals and the rational, compliant use of data become critical.

Chen Daoguang believes that the company’s decision to introduce state-owned capital in 2018 was primarily driven by the strong capability of state-owned investors in navigating policy landscapes and guiding strategic direction. Their investment also serves as an endorsement of the company’s innovative explorations across various domains. Furthermore, state-owned capital typically engages in these sectors as part of a strategic layout, enabling it to better mobilize resources to support the company’s long-term development.

Huang Yinze, CEO of Zechuang Tiancheng, highlighted the concept of data property rights confirmation. He believes that medical data and personal health data are both sensitive in nature, and defining their ownership, usage rights, and application scenarios is a prerequisite for data sharing and utilization. If personal data, genetic data, or health data are traded arbitrarily or misused, it could result in severe losses. Therefore, deep involvement by state-owned capital can better regulate the big healthcare data industry.

Taking medical record data under hospital custody as an example, hospitals do not hold ownership of the data, as it inherently belongs to patients. However, due to the trust-based relationship between patients and physicians, doctors have the right to access medical records and utilize the data for diagnosis and treatment. For medical big data companies, which function as information technology service providers offering analytics and application services based on medical data, the primary responsibility—shared with hospitals and physicians—is to safeguard personal privacy and ensure data security. Meanwhile, in the process of accessing, managing, and utilizing such data, various issues concerning data property rights and application scenarios inevitably arise; in this context, state-owned capital plays a significant role.

In addition to hospital data, he also mentioned clinical research data. With the continuous development of real-world studies, the volume of such data has reached a considerable scale. For instance, the respiratory disease-specific cohort data platform built by his company is expected to manage clinical research data for more than 300,000 patients with respiratory diseases by the end of 2020. The ownership and application scenarios of clinical research data are relatively clear. After obtaining informed consent forms signed by patients and performing de-identification, clinical researchers can manage and analyze the collected data based on specific clinical research projects.

Chen Daoguang also offered a similar perspective, arguing that medical big data constitutes a strategic resource in terms of data utilization. As genetic and health data continue to accumulate, such data are becoming increasingly diversified and valuable. However, this trend is accompanied by escalating risks of data leakage and security threats.

However, if these data are subjected to strict control measures or excessive regulation by relevant national authorities, it could lead to industry contraction or stagnation. Therefore, the entry of state-owned capital into private enterprises can be regarded as the most viable approach at present.

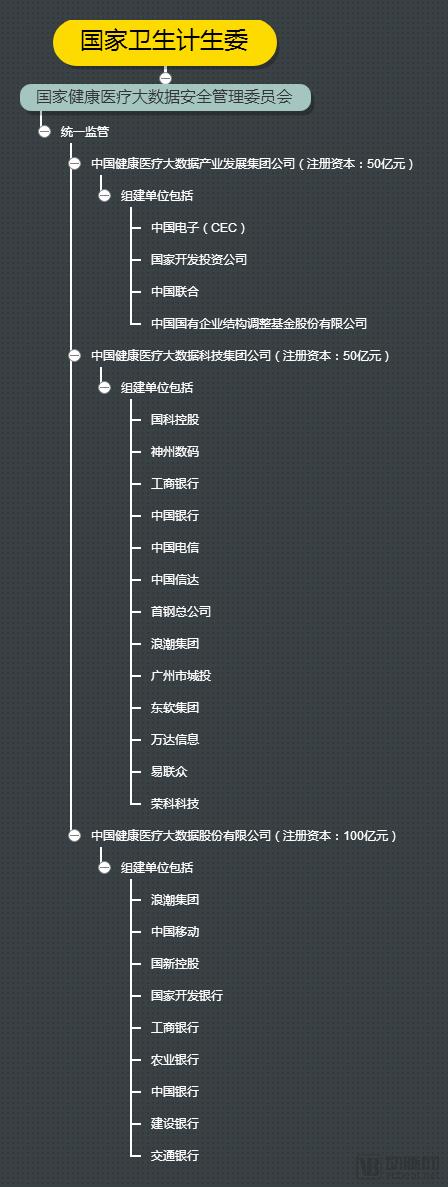

In 2017, the National Health Commission of China established the construction of national pilot centers for health and medical big data. In addition to promotion and guidance by local governments, enterprises are also required to assume responsibility for their construction. To this end, the National Health Commission took the lead in establishing three enterprises referred to within the industry as the “National Team.”

With the announcement in June 2017 by China Health and Medical Big Data Co., Ltd. regarding its preparatory establishment, coupled with the ongoing preparations for China Health and Medical Big Data Industry Development Group Co., Ltd. and China Health and Medical Big Data Technology Development Group Co., Ltd., a preliminary tripartite corporate structure dominated by “national teams” has taken shape in China’s health and medical big data sector.

Compared with private medical big data enterprises, the three major “national teams” possess certain regulatory and data ownership capabilities. This industry landscape can also be glimpsed from the actions of several companies.

In 2018, CE Health Fund successively participated in investments in Medlinker, a verified physician platform; Unisound, an IoT and AI service provider; Senyi Intelligence, a medical natural language processing company; and Chuanshi Technology, a supply chain technology enterprise in the pharmaceutical industry. The total investment amount for these four deals approached RMB 700 million.

In May 2018, Inspur initiated the establishment of China’s first Strategic Alliance for the Health and Medical Big Data Industry Ecosystem. The founding members included more than 30 organizations, such as Xiamen Zhiye, Miaoyijia, Huajian Lanhai, Kangfuzi, Renhe Future, Shandong University, and Jinan Industrial Development Investment Group.

It is evident that, since 2018, a state-owned background has become a prerequisite for entry into the medical big data sector. Driven by the three major national teams, the introduction of state capital into medical big data companies has become an overarching trend.

Question 3:What industry opportunities previously unavailable can state-owned capital bring to unicorn enterprises after its entry?

In the past, private enterprises harbored certain concerns about state-owned capital. This was because many state-owned investors, upon acquiring a significant equity stake, would impose specific financial reporting requirements that constrained corporate development. However, the new mixed-ownership reform measures introduced by state-owned capital are now bringing substantial benefits to private firms. Chen Daoguang believes that with the infusion of state-owned capital, companies can expect upgrades in four key areas: management, market access, brand influence, and funding.

Compared with non-state capital, state-owned capital is more cautious. It selects enterprises with a stronger sense of responsibility for investment, reflecting an assessment of the entire medical big data market and an evaluation of corporate compliance and rationality. Furthermore, state-owned capital assists enterprises in streamlining their financial, management, business development, and scientific research systems, thereby promoting more standardized growth.

Most importantly, the entry of state-owned capital can provide overarching oversight over the use of medical data. With the extensive platform resources offered by state-owned capital, big data enterprises in the healthcare sector can develop in a more orderly manner, avoiding blind industry competition.

For medical big data enterprises, the brand effect of state-owned capital can also enhance their social credibility. In the course of conducting business, if a medical big data enterprise has a state-owned capital background, it will be able to achieve twice the result with half the effort in negotiations and communications with hospitals.

The head of LinkDoc Technology also offered a similar perspective, noting that in the current environment, state-backed enterprises are more likely to receive greater policy support, or even preferential treatment.

State-owned backgrounds facilitate greater opportunities for government-enterprise collaboration (with entities such as the National Health Commission, the China Food and Drug Administration [CFDA], and the National Healthcare Security Administration), and are more conducive to data acquisition at both regional and national levels. The development of the national “1+5+X” data center framework, along with the two major regional models in Guizhou and Fuzhou, exemplifies state-led initiatives to establish and build regional data centers. This background also fosters stronger collaboration with medical institutions, which serve as the primary source of hospital data.

If enterprises participate in initiatives such as big data legislation, data security regulations, industry standards, and government policies guiding the development of big data, a state-owned background can ensure the company’s legality, compliance, and political security at the “source.” Furthermore, to enhance a company’s distinctiveness and brand competitiveness within its industry (among competitors), a state-owned background is an indispensable asset.