Fosun's $106M Investment in Butterfly Network: Exploring the Investment Logic Behind AI-Powered Handheld Ultrasound

Text and Photos: Chen Chuan, Huayi Capital

On July 13, Fosun Pharma (Group) announced its plan to invest US$106 million (approximately RMB 700 million) in the U.S.-based Butterfly Network. The post-investment valuation is approximately US$1.25 billion (approximately RMB 8.3 billion).

Butterfly is a Delaware-based U.S. company specializing in handheld ultrasound and artificial intelligence, founded in 2011. Its first ultrasound imaging product, Butterfly iQ, received FDA clearance for market launch in September 2017. By integrating smartphone applications with cloud technology, artificial intelligence, and deep learning, the device enables a single handheld ultrasound probe to perform examinations across multiple body regions and address diverse clinical application needs through various scanning modes.

Ultrasound Products

The announcement shows that as of December 31, 2017, Butterfly achieved zero dollars in main business income and a net profit of approximately -29.07 million USD (about 194 million yuan).

On this occasion, we will also discuss the investment logic behind AI-powered handheld ultrasound devices.

What is handheld ultrasound, how large is the market, and is it a blue ocean or red ocean in China?

Handheld ultrasound devices are compact, smartphone-sized units capable of performing examinations traditionally requiring large hospital-based B-mode ultrasound systems. Since the 1980s, the United States has pioneered the development of handheld ultrasound devices for battlefield medical care. These rechargeable diagnostic instruments, equipped with satellite-enabled remote image transmission, played a significant role during the U.S. military’s Operation Desert Storm. Subsequently, this technology transitioned from military to civilian applications. General Electric (GE) in the United States developed the first commercial handheld ultrasound device for medical use, which was initially employed for rapid emergency cardiac screening. Currently, handheld ultrasound is widely adopted among family physicians in the United States.

From Battlefield Care to Clinical Use

Handheld ultrasound is no longer the exclusive domain of radiology departments. A large number of clinicians can now easily operate these devices, allowing them to perform preliminary screenings for certain conditions (such as thyroid screening) without requiring patients to wait in line at the radiology department. Furthermore, primary care physicians can carry handheld ultrasound units during home visits, enabling residents in rural and underserved areas to access ultrasound services without leaving their villages.

Use of handheld ultrasound for primary care screening

During field medical operations or disaster relief efforts, injured individuals often cannot receive accurate medical diagnoses immediately, leading to delays in treatment. Handheld ultrasound devices, being portable and less dependent on power sources, can effectively address the challenges in disaster rescue caused by a lack of medical diagnostic equipment.

GE’s first-generation handheld ultrasound system, the VSCAN 1.0, was launched in the United States in 2008, creating a sensation. It was named one of “The 50 Best Inventions of 2009” by TIME magazine and one of “The 100 Best Technological Achievements of 2010” by the renowned popular science magazine Popular Science.

Unfortunately, GE’s handheld ultrasound device has not sold well. The most obvious reason is likely that, for a manufacturer specializing in comprehensive, large-scale medical imaging equipment, selling a low-priced compact device offers significantly lower profit margins for its internal sales team compared to big-ticket items. As a result, GE’s handheld ultrasound has merely become a supplementary product line within this multinational corporation, never rising to the status of a flagship product. Regardless of the high acclaim it has received from the industry or the substantial real market demand, this situation is difficult to reverse.

GE's VSCAN

So, how large is the handheld ultrasound market, and has market education been completed?

First, in China, handheld ultrasound represents an emerging blue-ocean market that requires physician education. Although GE’s VScan was launched as early as ten years ago, GE did not devote significant efforts to market education. Therefore, this is not a market for import substitution, but rather a blue-ocean market awaiting development.

However, the good news is that this market is not as barren as we had assumed. Earlier, the Ministry of Science and Technology of China listed portable handheld ultrasound as a key national R&D project under the 13th Five-Year Plan.

In August 2016, China’s first handheld ultrasound device (manufactured by Langsheng Technology) was officially put into clinical use.

Since 2017, products from two additional companies have successively received certification and entered the market promotion phase, with handheld ultrasound devices beginning to gain prominence at major professional forums and exhibitions.

In November 2017, the “Symposium on the Promotion and Application of Domestically Produced Portable Handheld Ultrasound Devices,” guided by the China Association of Medical Equipment (CAME) and hosted by its Ultrasound Equipment Technology Branch, fully affirmed the importance and necessity of promoting domestically produced portable handheld ultrasound devices in specialized clinical departments and primary healthcare settings.

Including primary healthcare and remote mountainous area assistance programs, handheld ultrasound has successfully been added to the government procurement list due to its portability advantage.

This blue-ocean market encompasses the clinical departments of 20,000 Tier I, II, and III hospitals in China, 70,000 township health centers and community service centers, 640,000 village clinics, as well as a vast overseas market, making it highly attractive.

First, let us provide an overview of the industry development of handheld ultrasound. It is worth noting that progress in China is on par with that overseas.

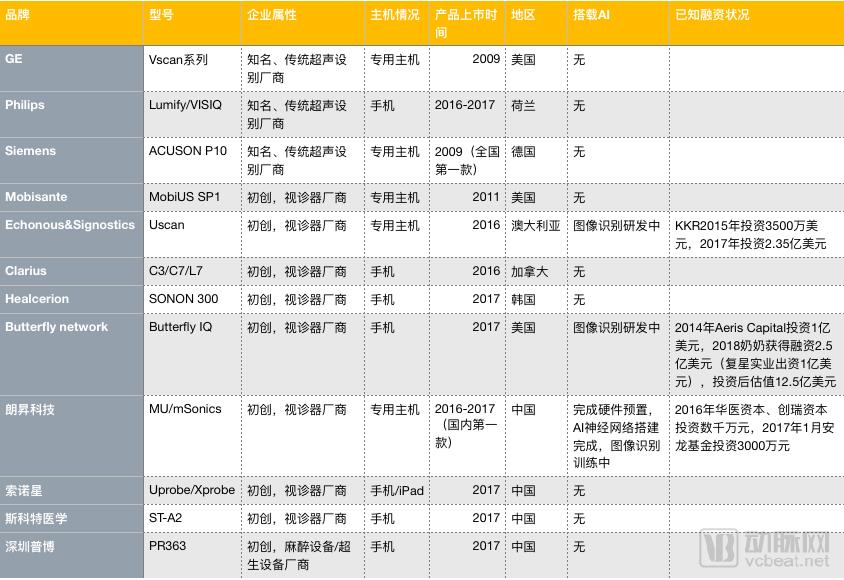

The following table lists the major handheld ultrasound products and companies worldwide.

Globally, handheld ultrasound devices have experienced two waves of product innovation.

First Wave: Giants Led by GPS Took the Lead. From 2009 to 2011, products included GE’s first-generation Vscan, Siemens’ Acuson P10, and Mobisante’s MobiUS. Due to limitations in design philosophy and technological maturity, these devices exhibited significant shortcomings in usability and image quality.

The Second Wave: Startups at Home and Abroad Launch Simultaneously. Between 2016 and 2017, Chinese and foreign companies advanced largely in sync, with the first handheld ultrasound products receiving regulatory approval during this period. In China, Langsheng was the first to achieve this milestone, followed closely by Sonostar and Suzhou Scott. Internationally, key players included Australia’s Signostics, Canada’s Clarius, and Butterfly Network in the United States (backed by Fosun). Compared to the first generation, these next-generation products featured significant improvements in design philosophy and technical approaches, delivering markedly enhanced usability and image quality, thereby largely phasing out first-wave products.

It is evident that the majority of handheld ultrasound manufacturers worldwide are startups. In China, several companies have already obtained regulatory approvals, indicating a relatively early start in this sector. Regarding artificial intelligence (AI) development, three companies globally have established dedicated teams for ultrasound AI research: Signostics from Australia, Butterfly from the United States, and Langsheng from China. The demand for such AI assistance tends to focus on delineating organ structures and identifying lesions.

Next, we will provide a brief introduction to these three companies specializing in handheld ultrasound and artificial intelligence.

Signostics was acquired by the ultrasound equipment company Echonous. It raised $35 million in 2015 and $235 million in 2017, with investment from private equity giant KKR. Its Uscan system features AI-powered bladder segmentation based on deep learning algorithms, volume calculation, and peripheral vein guidance.

EchoNous – The R&D team at Signostics comprises innovators from diverse fields, including healthcare, artificial intelligence, industrial design, manufacturing, and software engineering, possessing mature capabilities in ultrasound AI research and development. Signostics boasts a strong founding and technical team. However, there is no publicly available information regarding its hardware technology and platform, and the channels for data acquisition remain unknown. Although the product targets only specific application scenarios—namely, bladder segmentation and volume calculation, as well as vascular guidance—which do not impose stringent requirements on data sources, a lack of sufficient data may lead to bottlenecks in subsequent application development.

Butterfly is a U.S.-based handheld ultrasound company. Its primary ultrasound product is the Butterfly IQ, which consists of an ultrasound probe connected to a chip that transmits data to iPhones. The company raised $100 million in 2014 from investors including Aeris Capital, and secured $250 million in July 2018, with Fosun Industrial investing $100 million.

The Butterfly IQ device under its portfolio adopts the company’s proprietary ultrasound chip technology, integrating the performance of three typical ultrasound probes into a 2D matrix array composed of thousands of MEMS elements. It is currently applied in imaging for musculoskeletal, cardiac, and peripheral vascular applications, with future efforts focused on advanced areas such as AI-based recognition and tumor screening. At present, AI computing power relies on cloud computing, and there is no clear indication of plans to improve hardware platforms and transmission speeds in the future. The source of AI data has not been disclosed. The price of a single accompanying product is $2,000 (excluding tariffs).

Langsheng Technology is a high-tech company engaged in the research, development, and production of miniature ultrasound imaging equipment and high-end intelligent hardware. Its current primary focus is on handheld and portable ultrasound devices, as well as advancing the intelligence of medical ultrasound applications through AI-based recognition of ultrasound images.

The founding team is highly capable, comprising imaging experts and AI technology specialists.

In the field of artificial intelligence, Langsheng focuses on the development of specialized intelligent ultrasound products for real-world clinical applications, including: AI voice recognition-based command interaction and control applications, carotid plaque detection for carotid artery screening, brachial plexus nerve identification for pain management and anesthesia applications, and AI-based ultrasound image enhancement technologies.

Unlike traditional large-scale ultrasound systems, handheld ultrasound devices are not primarily used by sonographers but are mainly targeted at clinicians.

Handheld ultrasound opens up three incremental markets that are difficult for large-scale ultrasound systems to reach: 1. Hospital clinical departments, particularly the emergency and critical care market; 2. The primary healthcare institutions market; 3. The out-of-hospital disaster emergency response market.

Anesthesiologists Use Handheld Ultrasound

It is worth noting the significant assistance provided by handheld ultrasound in primary healthcare and medical aid in remote areas.

In remote mountainous areas with complex terrain and muddy conditions due to rain, when vehicles cannot reach the destination, doctors have to carry equipment and hike on foot. In such scenarios, portable handheld ultrasound devices prove particularly useful; especially during power outages in these regions, only handheld ultrasound devices that do not require an external power source can continue to operate.

A Brief Story of Medical Aid to Tibet: In 2017, the National Community Medical Service Volunteer Group traveled to Nyingchi, Tibet, to conduct a one-week medical assistance campaign. The journey was arduous, with the highest altitude along the route exceeding 4,700 meters, while the work environment was situated at an elevation of nearly 3,000 meters. The ultrasound diagnosis team of the volunteer group went to rural areas in Bomi County to perform health check-ups and echinococcosis screening for villagers, using handheld ultrasound devices.

Let’s shed some light on hepatic echinococcosis, a formidable parasitic disease also known as hepatic hydatidosis. In China, it is predominantly endemic in provinces and autonomous regions with developed livestock industries, including Xinjiang, Qinghai, Ningxia, Gansu, Inner Mongolia, and Tibet. In layman’s terms, these parasites “consume” the human liver. Early detection of this condition generally relies on ultrasonography.

During this medical aid mission to Tibet, the volunteer team conducted comprehensive abdominal screenings beyond the standard physical examination scope for 2,246 Tibetan residents. The screenings identified four confirmed cases and seven suspected cases of hepatic echinococcosis; one case each of renal cell carcinoma, bladder cancer, diffuse liver injury, renal angiomyolipoma, horseshoe kidney, renal agenesis, and nephrolithiasis; 50 cases of cholelithiasis; and three cases of hydronephrosis. Patients with hepatic hemangioma, acute cholecystitis, and other conditions were also detected. These findings provided a solid basis for controlling disease progression and implementing further preventive and therapeutic measures.

With the story concluded, it is clear that handheld ultrasound devices have extensive applications in primary healthcare. To facilitate their widespread adoption among primary care physicians, the role of artificial intelligence must be highlighted.

Currently, the greatest obstacles and pain points in promoting ultrasound screening at the primary care level are the inability to interpret ultrasound images and the lack of proficiency in operating ultrasound equipment. AI-assisted rapid identification and delineation technology for dynamic ultrasound regions will become the most effective and convenient solution to address these pain points.

We categorize current artificial intelligence applications in the field of ultrasound into diagnostic AI and segmentation AI.

1. AI with annotation capabilities (CFDA Class II).

2. Provide AI for auxiliary diagnosis, including functions for distinguishing between benign and malignant conditions (CFDA Class III; current approval policies are unclear, and the state is actively establishing databases).

The first type of AI is already sufficient to help handheld ultrasound rapidly expand its application in clinical departments of secondary and tertiary hospitals, particularly in promoting ultrasound screening in primary healthcare settings. Currently, the greatest barriers and pain points in promoting ultrasound screening at the primary care level are the inability to interpret and operate ultrasound equipment. Undoubtedly, AI-assisted technologies for rapid identification and delineation of dynamic anatomical structures in ultrasound will become the most effective and convenient solution to address these challenges. Moreover, with smooth and unobstructed regulatory approval pathways, this application is highly practical and well-suited to real-world clinical needs. Of course, this also requires a large volume of clinically positive cases to train machine learning algorithms and optimize neural networks.

The second type of AI is currently very popular and represents a future trend; however, significant obstacles remain in terms of both technology and regulatory approval. This application has the potential to truly ignite the grassroots market for handheld ultrasound devices in the future, making it highly promising, though patience will be required.

According to industry insiders, clinicians have warmly welcomed this type of AI-powered handheld ultrasound for contouring. When used as a digital stethoscope, it makes the diagnostic and treatment process more intuitive and eliminates the hassle of referring patients to the ultrasound department specifically for sonographic examinations. Moreover, different forms of ultrasound devices can play unique roles in various application scenarios.

When applied in clinical departments, the portability requirements for ultrasound devices are significantly higher. Consequently, handheld ultrasound systems are increasingly in demand among clinicians due to their ease of use, lower cost, and ability to meet requirements for image clarity and functionality. These devices also have broad applications in other scenarios. For instance, in emergency centers, AI-enabled portable ultrasound with outlining capabilities can substantially improve work efficiency and facilitate house calls. Furthermore, they are highly popular in the education of novice physicians, helping them identify organs, tissues, and lesions. This enables faster proficiency and progress while reducing the burden on experienced physicians for hands-on instruction.

Meanwhile, with the aid of AI-assisted contouring, primary care providers—mainly township and village doctors, nurses, and other healthcare personnel who have not received training in ultrasonic diagnosis or even lack a comprehensive understanding of anatomy—can also quickly become proficient in its use.

Overall, a higher number of physical channels is not always better, as it leads to increased power consumption and larger device size. The algorithm chip is the core component and the key to device miniaturization; it can overcome hardware limitations to achieve superior image quality. Post-processing capabilities and screen quality serve as supplementary enhancements. For long-term use, system stability is critical, as poor stability can lead to medical incidents.

The imaging quality of ultrasound equipment is closely related to two aspects: the number of physical channels in the hardware, and the implementation capability of algorithmic chips.

For ultrasound equipment, the number of physical channels can be likened to engine displacement in automobiles. A higher channel count enables the simultaneous transmission of more electrical signals, activates more transducer elements at once, and generates richer acoustic waves. This results in more diverse echo returns and subsequent electrical signal conversions, yielding richer and more detailed imaging. Manufacturers have continuously experimented with the number of physical channels in medical ultrasound devices. Currently, high-end large-scale color Doppler ultrasound systems commonly feature 128 channels or even more, while mid-range large-scale systems have reached 64 channels. Low-end large-scale systems with 32 channels still exist in the market but are gradually being phased out. While increasing the number of physical channels undoubtedly enhances image quality, it inevitably introduces certain changes: larger equipment size, thicker data transmission cables, and increased power consumption. These factors pose little issue for large ultrasound systems but represent a critical drawback for miniaturized devices. Consequently, prior to the launch of China’s first domestically produced handheld ultrasound device, the Chinese ultrasound industry remained skeptical about the feasibility of handheld ultrasound equipment with clinical value.

In the market for large-scale ultrasound systems, the wave of domestic substitution is unfolding vigorously in the mid- and low-end segments. This trend is closely tied to the continuous development and maturation of China’s ultrasound industry ecosystem, with Chinese manufacturers rapidly narrowing the hardware gap with their international counterparts. However, a significant disparity remains between Chinese and international brands in the high-end equipment market, a gap largely reflected in the level of algorithmic chip implementation.

If the number of physical channels is likened to the body of ultrasound performance, then algorithm and chip implementation can be understood as its soul. Hardware provides the foundational resources for ultrasound imaging, but the effective allocation and utilization of these resources to achieve maximum efficiency fall within the domain of algorithm and chip technology. Superior core ultrasound algorithms and chip implementations can enable ultrasound devices to deliver performance levels far exceeding what their existing hardware specifications would suggest. For instance, achieving imaging quality equivalent to 32 channels using only 8 physical channels requires precise and ingenious design concepts in signal transmission and resource allocation, underpinned by systematic and long-term technological accumulation. Currently, many well-known domestic ultrasound brands have fully matched imported brands in terms of hardware capabilities; however, there remains a significant gap between them and imported brands in the research, development, and accumulation of algorithm and chip technologies. There are no unified industry standards for the algorithmic implementation of ultrasound equipment, and its high degree of uniqueness often serves as a key differentiator in performance among products.

In addition to the aforementioned two factors, post-processing capabilities and screen quality can also significantly impact image quality. The first two factors are akin to hard metrics, forming the foundation of imaging, whereas the latter two serve as soft enhancements. Advanced post-processing techniques can deliver exceptional “aesthetic” improvements, transforming originally low-quality images into clear and detailed visuals while ensuring high fidelity. This highly skilled craft places substantial demands on the technical team’s expertise.

Next is screen quality. A high-end screen and a standard screen can produce markedly different visual outputs even when receiving the same signal. As portability is a key feature of handheld ultrasound devices, their usage environments differ significantly from those of large-scale ultrasound systems. Variable lighting conditions and non-fixed light sources are common; therefore, a screen capable of delivering clear images under diverse lighting conditions undoubtedly enhances the product’s imaging performance. For instance, Langsheng Technology has equipped its device with an all-weather AMOLED display. This type of screen offers high contrast and extremely fast response times, features currently adopted primarily by major smartphone manufacturers such as Samsung for its high-end models and Apple for the iPhone X. Most importantly, AMOLED screens maintain clear visibility regardless of ambient light, making them particularly valuable in outdoor and emergency rescue scenarios.

Beyond imaging quality, the system stability of medical ultrasound devices is also critically important. For instance, if screen lag or system failure occurs during an ultrasound-guided puncture procedure, it could directly lead to a medical incident. Even in non-intraoperative scenarios, due to the specific real-time requirements of medical ultrasound examinations, screen delay and freezing result in a poor operational experience and significantly impair physicians’ work efficiency. Achieving robust system stability in ultrasound equipment relies on mature system implementation technologies. Unlike the high degree of uniqueness associated with algorithm-specific chips, system implementation follows certain established industry standards. Ordinary companies can achieve basic system operation by adhering to these standard protocols, but they often encounter significant bottlenecks. Conversely, attaining power consumption levels and system stability that surpass industry norms imposes exceptionally high demands on a company’s expertise in system implementation.

In terms of computing power, although the AI used for delineation requires only a neural network with hundreds of parameters, it is typically hosted on large-scale devices. Deploying this neural network on handheld devices presents challenges such as insufficient GPU computational power, low power consumption constraints, and hardware costs.

To achieve real-time ultrasound imaging diagnosis and treatment, having a robust mobile hardware platform and a skilled software-hardware development team is crucial.

For example, Langsheng Technology’s products reserve GPU/DSP resources for AI within the device. Leveraging the low-power Qualcomm Snapdragon 820 hardware platform, and through extensive neural network optimization and system adaptation, they enable AI computation on mobile terminals. This allows up to thousands of optimized neural networks to be deployed on mobile terminal hardware systems, essentially realizing the application of contouring AI on handheld devices.

In contrast, the AI chips currently common among other manufacturers, such as Nvidia chips, are prohibitively expensive and consume excessive power, making it impractical to perform AI computations on mobile devices.

In other words, users obtain results in real time as they operate the device. If we were to follow conventional approaches by offloading AI computations to the cloud—relying on an upload-compute-download workflow—it would severely compromise the real-time dynamic performance of ultrasound imaging, delivering a fatal blow to user experience.

This necessitates shifting AI computation from the cloud to local devices, which places significant demands on hardware performance. Therefore, whether driven by the need for improved future imaging quality or AI operational requirements, dedicated handheld consoles represent a major trend.