Where Are the Venture Funds of the World's Top 20 Pharma Companies Investing? Digital Health, AI, Big Data, and Patient Services Emerge as Key Focus Areas

Technology has brought boundless wealth to the pharmaceutical industry, fostering its unprecedented prosperity.

A close observation reveals that many of the world’s leading pharmaceutical companies are century-old enterprises. Their acute sensitivity to innovation enables them to strategically expand into new business areas around their core operations—through internal incubation, investment, partnerships, and acquisitions—thereby achieving sustained growth. Among these strategies, investment poses the greatest test of insight and trend-judgment capabilities, particularly in the realm of venture capital for start-ups.

VCBeat (WeChat ID: vcbeat) has compiled an overview of venture capital investments established by the world’s top 20 pharmaceutical companies, aiming to analyze the investment trends of these industry leaders.

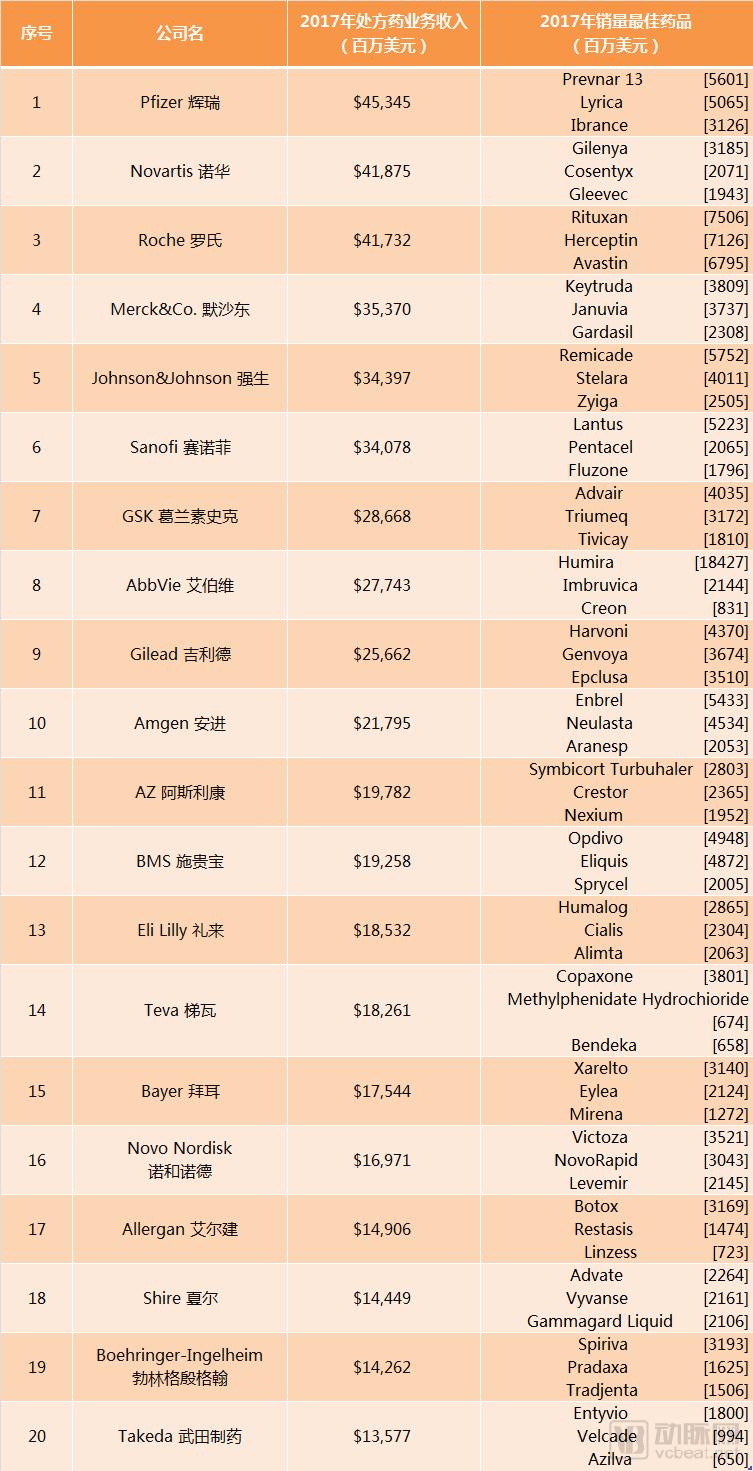

In terms of pharmaceutical revenue, Pfizer topped the global pharmaceutical companies, with prescription drug revenue reaching $45.345 billion in 2017. Novartis and Roche followed closely behind, with pharmaceutical revenues of $41.875 billion and $41.732 billion, respectively. Merck & Co., Johnson & Johnson, and Sanofi came next, with pharmaceutical revenues reaching the $30 billion range.

All of the top 20 global pharmaceutical companies have their “blockbuster” drugs, such as Pfizer’s Prevnar, Novartis’ Gilenya, and Roche’s Rituxan. Of course, the most outstanding single product remains AbbVie’s Humira (adalimumab), which generated $18.427 billion in revenue in 2017, propelling AbbVie into the top ten in pharmaceutical sales rankings.

Below are the 2017 pharmaceutical revenue figures for the top 20 global pharmaceutical companies, along with their blockbuster drugs:

Data Source: PharmExec, VCBeat

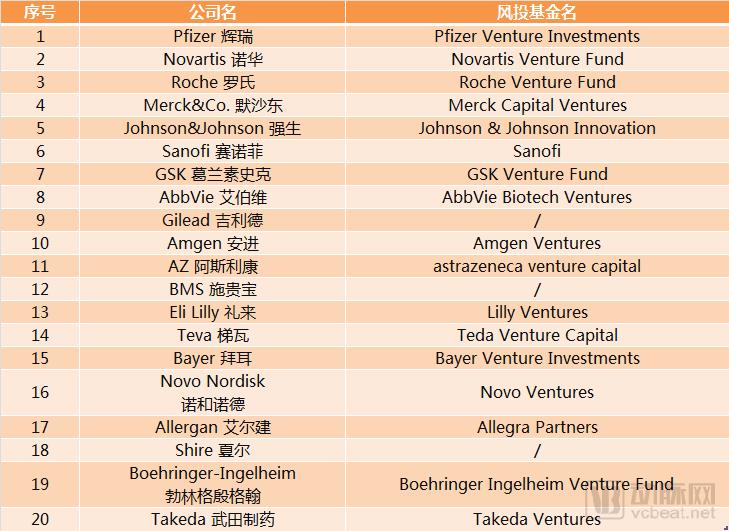

Among the top 20 pharmaceutical companies, the vast majority have established dedicated venture capital funds to invest in start-ups. Examples include Pfizer Venture Investments, Novartis Venture Fund, and Roche Venture Fund.

Other companies that have not established dedicated venture capital funds also maintain internal investment departments to invest in innovative projects. It is also worth noting that the top 20 pharmaceutical companies extensively participate in the investment and establishment of industry funds, including subscribing to such funds and co-establishing venture funds with other companies. This trend has been corroborated in China, where pharmaceutical companies establish or collaborate on hundreds of industry funds annually.

Venture Capital Funds of the Top 20 Pharmaceutical Companies

Data Source: Crunchbase, VCBeat

By tracking the top 20 pharmaceutical companies and their established venture capital funds, we have compiled the following table, which illustrates the level of involvement of these pharmaceutical companies in investing in startups.

Data Source: Crunchbase, VCBeat

In terms of the number of investment deals and portfolio companies, Novartis stands far ahead with 172 investment deals involving 44 companies; Pfizer, Roche, Merck & Co., Amgen, and others follow closely, each with approximately 70 investment deals and more than 10 portfolio companies.

From the perspective of involved fields, innovative therapies and drug development that are highly relevant to the core business of pharmaceutical companies account for a significant proportion. Digital tools and platforms that provide support for pharmaceutical operations, such as AI-powered new drug discovery tools and big data collection and application tools, are also favored by pharmaceutical enterprises. With market development of drugs as the core, innovative projects in areas such as online marketing, patient education, and doctor-patient communication are also highly regarded by pharmaceutical companies.

Data Source: Crunchbase, VCBeat | Sector classification involves a degree of subjectivity and is for reference only

Although biopharmaceuticals remain the primary focus of venture capital investment by pharmaceutical companies, these firms have also made significant strategic moves under the concept of “digitalization,” including digital therapeutics, digital marketing, and data services. Given the strong correlation between pharmaceutical operations and healthcare services, medical payment systems, and patient preferences, pharmaceutical companies are actively entering these sectors to gain a comprehensive understanding of the market.

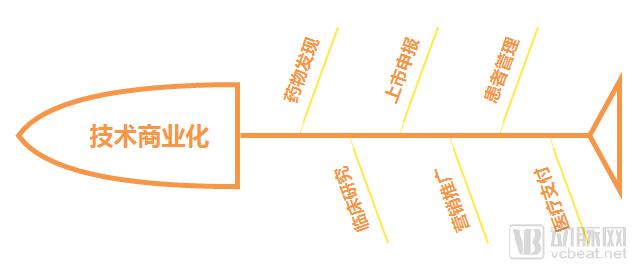

Overall, “technology” remains the core competitiveness of pharmaceutical companies, especially innovative drug enterprises. In addition to their high R&D investment, these companies also acquire new technologies and achieve commercialization through investments, collaborations, and acquisitions. Of course, the term “technology” here refers not only to drug development technologies but also encompasses the entire process from drug development to marketing and patient use.

A Typical Process for the Commercialization of Pharmaceutical Technologies and Key Stages Involved

Pharmaceutical companies invest heavily in every aspect of drug technology commercialization, as well as in any factor that could influence their market trajectory.

Market challenges are also issues that pharmaceutical companies must confront. First, R&D investment costs are rising while returns are diminishing; second, the behaviors of physicians and patients are being influenced by an increasing number of factors, and their choices will directly impact pharmaceutical companies’ revenues.

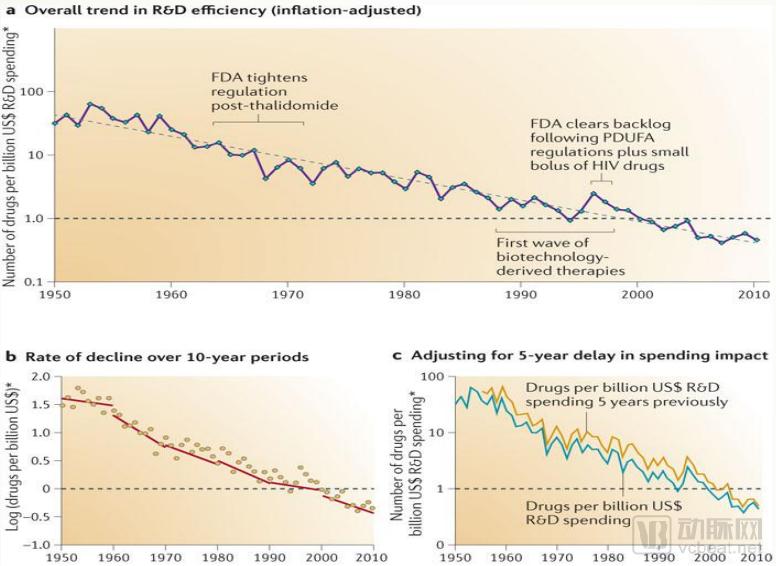

The first point is referred to as the “Reverse Moore’s Law” of the pharmaceutical industry. This term, originating from the IT sector, originally stated that the integration density of integrated circuits doubles every 18–24 months, leading to rapid product iterations; consequently, a product’s price 18 months after launch drops to half its initial offering price. Therefore, if a company continues to sell the same product, it must sell twice the volume today to generate the same revenue it achieved 18 months ago.

The “anti-Moore’s Law” in the pharmaceutical industry refers to the phenomenon where R&D costs continue to rise while the productivity of drug development steadily declines—a trend supported by empirical data. According to a report by Derek Lowe, in the 1950s, U.S. pharmaceutical companies could develop dozens of new drugs for every $1 billion spent; however, since the turn of the millennium, this figure has dropped to less than one.

Even when accounting for factors such as economic growth, inflation, and rising labor costs, the changes in new drug development costs remain striking. This indicates that new drug development has become an activity with extremely high barriers to entry, undoubtedly deterring many ambitious new entrants.

When the success rate of new drug development is taken into account, the outlook becomes even more disheartening. Generally, the clinical trial phase has the highest attrition rate across all stages of new drug development. The success rates are approximately 65% for Phase I, 35% for Phase II, and 20% for Phase III clinical trials. Cumulatively, the overall success rate for the clinical trial phase is less than 10%. In specific therapeutic areas such as oncology, the success rate is even lower. This indicates that new drug development has become a “high-stakes gamble” with bets exceeding one billion U.S. dollars.

The Reverse Moore’s Law in the Pharmaceutical Industry

Amid this trend, the pharmaceutical industry is placing greater emphasis on “technology,” including technologies that enhance drug R&D efficiency or accelerate market revenue generation post-commercialization to recoup costs. In other words, the commercial nature of pharmaceutical companies demands a sharper focus on return on investment than ever before, making it imperative to improve operational efficiency.

“Digital” tools or technologies undoubtedly possess the traits most urgently needed by the pharmaceutical industry. This refers to the application of internet and information technologies across various stages of pharmaceutical operations to transform existing business processes and models, with the primary aim of reducing costs, improving efficiency, or both.

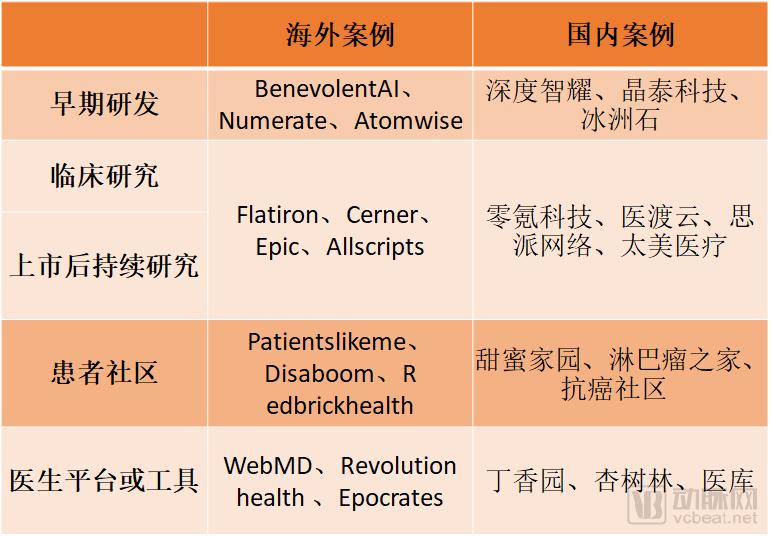

Correspondingly, innovative companies emerging at these different stages have also gained favor among pharmaceutical enterprises. Examples include the application of AI tools in early-stage R&D, the use of big data tools in clinical research phases, digital marketing initiatives via physician-oriented tools/platforms, and the penetration of patient management tools.

From a timeline perspective, collaboration between pharmaceutical companies and technology firms has become increasingly close since 2016:

In October 2016, AbbVie (ObbVie) utilized AIcure’s technology for facial recognition-based medication adherence monitoring in clinical trials;

In December 2016, Pfizer used IBM Watson to test hypotheses for cancer drug discovery;

In February 2017, Bayer employed AI to develop combination therapies tailored to different patient populations;

In May 2017, Sanofi entered into a collaboration with Exscientia, an AI-driven drug discovery company, focusing on diabetes and related conditions;

In November 2017, BMS used PathAI’s platform to analyze pathological samples and assess patient responses to drugs.

A survey by the Pistoia Alliance indicates that 44% of life sciences professionals are currently using artificial intelligence tools, and 94% plan to increase their use of machine learning within the next two years. In clinical development, the application of AI is being integrated with data from sensors and mobile devices to enhance insights into patient behavior and to create more digital products and services.

Application of Digital Tools in the Pharmaceutical Industry

As we can see, many of these “digital” flagship projects have received investment and participation from pharmaceutical companies. For instance, Numerate is backed by Lilly Ventures; Atomwise is supported by Monsanto Growth Ventures (Monsanto was acquired by Bayer); Flatiron Health is backed by Roche; and PatientsLikeMe has established in-depth collaborations with pharmaceutical companies such as AstraZeneca, Takeda Pharmaceutical, and M2GEN. These cases illustrate the pharmaceutical industry’s embrace of digital technologies.

An investor once commented on Roche’s acquisition of Flatiron Health by describing it as “the ferryman” acquiring “the bridge builder.” Traditional pharmaceutical operations are akin to a ferry service, delivering limited outcomes per trip, whereas once a “bridge” is built, it unlocks infinite possibilities on the other side. Specifically, AI tools can enhance the efficiency of compound research and preclinical studies; when combined with precision medicine, they can improve the success rate of clinical trials. Similarly, big data analytics, electronic data capture (EDC) systems, and online marketing tools can yield comparable benefits.

The development of the internet and mobile internet after 2000 ushered in the 1.0 era of digital tool adoption in the pharmaceutical industry. Subsequently, the emergence of technologies such as the Internet of Things (IoT), sensors, big data, artificial intelligence, and blockchain after 2010 propelled the industry’s digitalization into the 2.0 era.

Just as advances in biotechnology have brought targeted therapies for precision medicine to the pharmaceutical industry, this new wave of digitalization—centered on AI, big data, wearable devices, and flexible sensor technologies—will reshape the driving forces and trajectory of the pharmaceutical sector. In the future, only companies that can accurately grasp digital trends will secure a place amidst technological transformation. The top 20 pharmaceutical companies that have taken the lead in investing in digital health firms are undoubtedly ahead of the curve.

Atomwise, founded in June 2012, is a company that leverages computing technologies for drug discovery and development. Its project aims to simulate pharmaceutical processes using supercomputers, artificial intelligence (AI), and complex algorithms to predict the efficacy of new drugs while reducing research and development costs. The company is headquartered in San Francisco, United States.

Atomwise’s core product is the AtomNet system, which employs statistical methods to extract data from millions of experimental affinity measurements and thousands of protein structures, thereby predicting the binding of small molecules to proteins. Typically, during the early stages of drug discovery, researchers must identify candidate drugs that are both effective and safe from among millions of compounds, while also characterizing the features underlying the binding between potential drugs and their target proteins.

This complex multi-task optimization is where computers excel. Atomwise’s AI technology leverages combinations of convolutional neural networks to predict novel bioactive molecules, freeing research and development from the constraints of limited compound libraries and the time required for screening. As a result, the discovery and optimization process, which traditionally takes years, can be compressed into just a few weeks.

Atomwise completed a $45 million Series A financing round in March 2018, with investors including Monsanto Growth Ventures, Tencent, and Baidu, bringing its total fundraising to over $50 million. Atomwise’s business partners include Merck & Co., AbbVie, Monsanto, and Duke University.

Click Therapeutics, founded in April 2012 and headquartered in New York, USA, is dedicated to providing patients with digital prescription therapeutic solutions through the development and commercialization of software.

By leveraging cognitive and neurobehavioral mechanisms, Click’s Digital Therapeutics™ can intervene in individual behavior from within, and may be designed for standalone use or in combination with other biologic therapies. The company’s Clickometrics® adaptive data science platform continuously personalizes the user experience to optimize patient engagement and therapeutic outcomes.

The company’s currently commercialized product is Clickotine, an app designed to help people quit smoking by digitally deploying cessation strategies such as teaching controlled breathing exercises, enabling users to log their smoking habits and emotions, and sending motivational messages, among other features. Following a groundbreaking clinical trial, the Clickotine program has been rolled out nationwide in the United States to serve the public.

In July 2018, Click Therapeutics announced the completion of a $17 million financing round, led by Sanofi Ventures. During its seed funding round, Click had secured investment from Flatiron Health. To date, Click’s total fundraising has exceeded $25 million.

Founded in May 2007 and headquartered in San Bruno, California, Numerate combines advanced developments in computer science and statistics with traditional medicinal chemistry approaches, dedicated to providing a drug design platform for companies developing small-molecule therapeutics. The platform primarily focuses on the research and development of drug candidates for cardiovascular diseases, metabolic disorders, neurodegenerative diseases, Alzheimer’s disease, and Huntington’s disease.

With 11 years of establishment, the company has accumulated profound technical expertise. Based on 3D ligand modeling, it enables the use of machine learning to address phenotype-driven drug discovery challenges without requiring structural data of compounds. Such R&D efforts often involve low-throughput, high-content biological problems.

In April 2018, Numerate joined ATOM (Accelerating Therapeutics for Opportunities in Medicine), whose founding members include GSK, two U.S. national laboratories, and several prestigious universities.

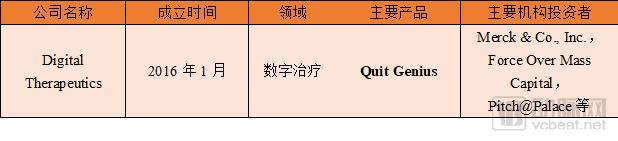

Digital Therapeutics was founded in January 2016 by a team of clinicians who believed that behavioral interventions could have a profound impact on health outcomes. However, for the vast majority of people, sustaining behavior change is difficult, and accessing high-quality, evidence-based behavioral therapy remains challenging.

Digital Therapeutics’ first product was the smoking cessation therapy Quit Genius. The product underwent two years of preparation prior to its launch, with a development team comprising scientists, behavioral specialists, physicians, and smokers. The therapy incorporates a series of cognitive behavioral interventions, including audio-visual content, animations, and interactive exercises. According to data published on its official website, the product achieved a smoking cessation success rate of 36%, reduced cigarette consumption by 60%, and saved employers more than $155 million.

In fact, the pharmaceutical industry has long been focused on digital prescription therapies, a concept championed by Sean Duffy, CEO of Omada Health. Currently, about a dozen companies are developing digital therapeutics, including Welldoc, Virta Health, Propeller Health, and Big Health.

GNS Healthcare was founded in 2000, stemming from a series of ideas by its founder, Colin Hill: Can genetic and genomic data be translated into computational models of disease progression and drug response? Can these models reveal new drug targets, novel therapeutics, and predictive biomarkers to enable personalized medicine? Can breakthroughs in machine learning, modeling, and simulation be combined with ever-increasing supercomputing power? And can this vision be realized to transform the treatment of diseases such as cancer, diabetes, Alzheimer’s disease, heart disease, and multiple sclerosis?

These challenges led Colin Hill and Dr. Iya Khalil to found GNS Healthcare at Cornell University in 2000. The technology is built upon the foundational work of Dr. Stuart Kauffman (a five-time MacArthur “Genius” Grant recipient), Dr. Judea Pearl (a Turing Award laureate), as well as advances in systems biology, chaos theory, statistical physics, and artificial intelligence.

GNS Healthcare’s flagship product is the REFS platform (Reverse Engineering & Forward Simulation). True to its name, the platform operates by first ingesting large volumes of data on disease mechanisms derived from extensive patient health records, clustering similar mechanistic patterns, and inferring causal factors from observed outcomes. Subsequently, REFS simulates treatment processes to determine which therapeutic interventions and medications yield optimal results. By identifying causal relationships among variables, REFS can rapidly pinpoint factors relevant to specific individuals, thereby enabling precise personalized medicine.

REFS serves commercial health plans, healthcare delivery systems, the pharmaceutical industry, and research institutions. Its partners include Novartis, BMS, Celgene, Horizon Blue, and others. GNS Healthcare has raised over $50 million to date.

At this year’s ASCO Annual Meeting, GNS and ACTO (Alliance for Clinical Trials in Oncology) presented study results demonstrating that GNS effectively helps identify responses to different medications or medication combinations in patients with metastatic colorectal cancer (mCRC) in Phase III trials, thereby facilitating stratified treatment for these patients. This research was initiated in 2015, and the initial findings were announced at the 2017 ASCO Annual Meeting.