Localization of PBM for Chronic Disease Management in China: Identifying the Optimal Player Among Five Categories

//Authors: Liu Zeyuan, Zhou Di, Gai Ruijie, Sun Qisong from the Healthcare Team of China Renaissance Capital

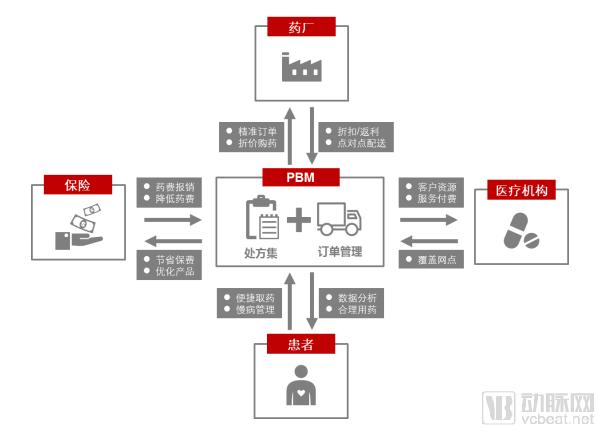

PBM(Pharmacy Benefit Management)Pharmacy Benefit Management (PBM) is a specialized third-party healthcare management service. Its essence lies in redistributing interests among the three major stakeholders in the healthcare system—pharmaceutical manufacturers, healthcare providers (hospitals, clinics, and pharmacies), and payers (social insurance and commercial insurance). Its core value is to reduce waste and abuse of medical resources and lower artificially inflated drug prices.

The Focus of Pharmaceutical Benefit Management Lies in“Benefit”, in layman's terms, it means "storing benefits for the people." "Benefiting the people" is first reflected inPBMEmphasizing a patient-centric approach, particularly in the management of long-term prescription medications for patients with chronic diseases.。PBMthe essence isRefined Management of Pharmaceutical Supply, by analyzing the accumulated long-term medication data of patients with chronic diseases, the drug supply model has transformed from the original "supply-driven" to "demand/order-driven."

By analyzing long-term continuous medication usage, the company proactively reminds physicians to prescribe long-term continuous prescriptions for patients and provides convenient medication access services through offline pickup or mail delivery. Meanwhile,PBMThe company negotiates with upstream pharmaceutical manufacturers to procure drugs at lower costs, while streamlining intermediate distribution channels to improve drug inventory turnover rates. It serves downstream retail pharmacy chains and healthcare institutions through its drug catalogs and formularies.(Formulary)the use of, to reduce waste of medical resources and address the issue of artificially inflated drug prices, without compromising the quality of medical services.

China Renaissance’s Healthcare Team Conducts Research on the Localized Implementation of PBMs,VCBeat (WeChat ID: vcbeat)Reprinted with permission.

PBMs are a product of the U.S. managed care system.

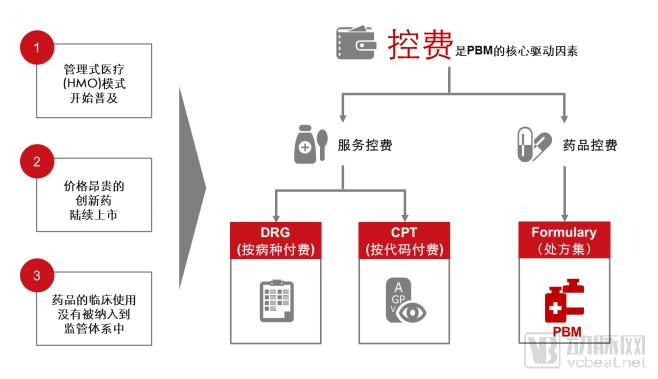

The Historical Background of the Emergence of PBMs

PBMOriginated in the United States during the last century70In the era, the background for its emergence stemmed from three factors: on one hand, innovative managed care(HMO)As this model gained widespread adoption, cost containment became a common imperative for healthcare service providers. Meanwhile, a large number of high-priced innovative drugs have been successively launched onto the market, yet public demand has risen for lower-priced generic drugs with equivalent efficacy. Furthermore, the clinical use of pharmaceuticals has not yet been incorporated into an appropriate regulatory and oversight framework. Consequently, ensuring that medications achieve their maximal clinical benefit while avoiding unreasonable pharmaceutical expenditures has become an urgent priority in healthcare management. Against this backdrop,PBMServices are increasingly differentiating into an emerging industry, with their primary function being to control pharmaceutical expenditures for insurance companies while ensuring the clinical efficacy of patients' medication.

PBM is a mature business model in the United States.

After nearly half a century of exploration, PBMs have evolved into a mature business model in the United States,Representing the company with ESI (Express Scripts Inc),UNH (Optum Rx),Caremark (CVS Under)。Taking Express Scripts, Inc. (ESI), the largest pharmacy benefit manager (PBM) in the United States, as an example, the company has a total market capitalization exceeding $44 billion, annual revenues surpassing $100 billion for five consecutive years, processes 1.4 billion prescription claims annually, saves more than $1.3 billion in insurance premiums each year, and is ranked among the Fortune 100 companies in the United States.

PBMs Help Effectively Control Drug Costs and Reduce Waste of Medical Resources in the United States

PBMThe core objective is to control pharmaceutical costs. Taking the United States as an example, the current average annual pharmaceutical expenditure per patient is1,184U.S. dollars (including the patient's out-of-pocket portion and various insurance payments), whereas in the absence ofPBMIn the case of business, the cost is as high as2,125USD per person per year, average annual savings per patient941USD costs (including355($ paid by the patient, with the remainder reimbursed by the insurance company). According to the U.S. Food and Drug Administration (ANAHA)prediction,From2012Age2021year,PBMThe company will save costs for insurance companies and patients.35%pharmaceutical consumption, reaching2trillion U.S. dollars.

Typical Service Process of U.S. PBMs

U.S. PBM companies primarily serve patients requiring long-term medication for chronic diseases.In the United States, due to the "separation of prescribing and dispensing," patients with chronic diseases regularly visit offline pharmacies to "purchase medications" based on prescriptions (however, U.S. retail pharmacies are not direct service providers for chronic disease medication purchases; pharmacies merelyPBM(A venue that helps patients make regular payments and collect medications, a point often misunderstood and overlooked by various parties in China). Retail pharmacies will submit pre-filled electronic prescriptionsPBMCompany Review,PBMThe company will, based onFormulary(Formulary) to evaluate whether the drug offers the optimal balance of price and efficacy; if a lower-priced alternative with equivalent efficacy exists,PBMIt is recommended to adopt lower-priced medications.

PBMUpon approval, the medication will be prepared in advance for patient pickup at the designated pharmacy, based on the patient’s medication history and insurance coverage; the patient shall pay the out-of-pocket portion directly to the pharmacy.(Co-pay), with the remaining portion covered by commercial insurance or social security (U.S. social security refers toMedicareandMedicaid) reimbursement. For patients with chronic conditions requiring long-term prescriptions, mailing is available in accordance with reimbursement policies.(Mail-order)Deliver medications directly to your home.

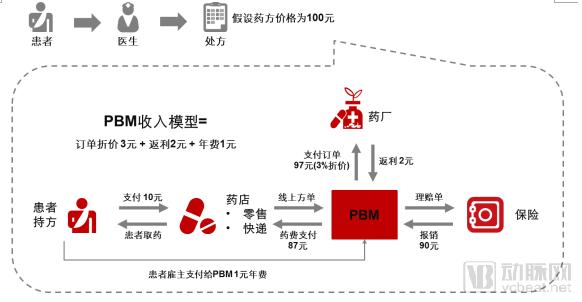

PBM Revenue Model

It is commonly believed that the leading U.S. Pharmacy Benefit Management (PBM) companies derive their revenue primarily from IT-enabled services. However, our research reveals that their core business revenue stems mainly from pharmaceutical distribution and sales, all operating under a central pharmacy supply model.

PBMObtained by the company through negotiations with pharmaceutical manufacturers3%Drug Discounts(Discount); pharmaceutical manufacturers regardingPBMCompany's Direct Rebate2%(Rebates are legal in the United States, Drug rebates are passed on to patients through PBMs, with a portion also allocated to insurance companies, thereby enhancing overall patient benefits.; and those paid by employers or patient members1%Membership Fee(Premium). Therefore, most U.S. PBM companies generate substantial revenue, typically exceeding $100 billion, while their profit margins generally remain at6%approximately.

PBM achieves core drug cost control through drug price negotiation and prescription review to support rational drug use.

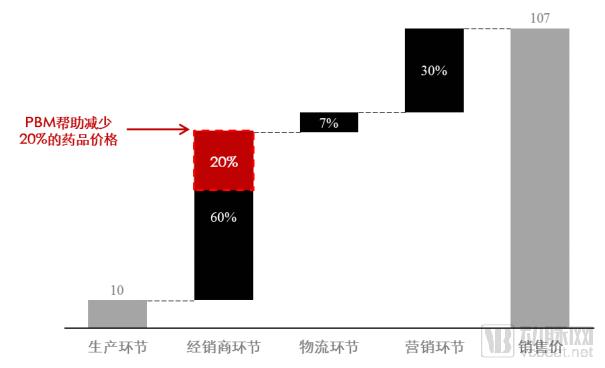

PBMOn one hand, negotiate with upstream pharmaceutical manufacturers to lower drug procurement prices through bulk purchasing. An analysis of the pharmaceutical distribution value chain reveals that the highest profit margins are found in upstream production and downstream sales. In China, the markup at the pharmaceutical distributor level is generally60%, the gross profit margin in the logistics segment is generally7%, the gross profit margin in the downstream terminal marketing segment is at30%approximately. In ChinaPBMIf the company achieves growth and successfully negotiates prices with pharmaceutical manufacturers, it is expected to gain advantages through volume-based procurement.20%gross margin of approximately.

Meanwhile,PBMThe company will formulate dynamically adjusted [policies/protocols] based on a large volume of historical prescription cases and clinical practice guidelines issued by regulatory authorities.Formulary(Formulary) Based on the formulary and big data analytics, reasonable clinical pathways for physicians and rational drug use guidelines are established. The database of these guidelines is integrated into the information systems of physicians and hospitals, enabling software-based monitoring of clinical treatment and prescription practices to eliminate the overprescription of high-cost and unnecessary medications, thereby achieving the goal of controlling pharmaceutical expenditures.

China's pharmaceutical supply system is currently chaotic, with serious waste of medical resources.

Currently, 95% of pharmaceutical sales in China are distributed nationwide through distributors. However, among the more than 13,000 existing pharmaceutical distributors, most can only cover one to two hospitals. The combined revenue share of the top 15 regional distributors is merely 18%. Furthermore, the sales of the top 100 pharmaceutical retail enterprises account for only 29% of the total pharmaceutical retail market. Market concentration is significantly lower than that in mature markets such as the United States, Japan, and the European Union, resulting in an extremely fragmented and disordered pharmaceutical supply system.

Meanwhile, China faces a serious problem of pharmaceutical waste. The primary contributing factors include patients’ irrational purchasing behaviors, physicians issuing “excessive prescriptions” to generate revenue, and the production and sale of drugs in oversized packaging. Statistics show that the average household in major Chinese cities holds 215 expired pills, with 30%–40% of these medications having been expired for more than three years. Nationwide, approximately 15,000 metric tons of drugs are wasted annually due to expiration, with the average financial loss accounting for over 30% of total healthcare expenditures; in severely affected regions, this figure can reach 40%–50%.

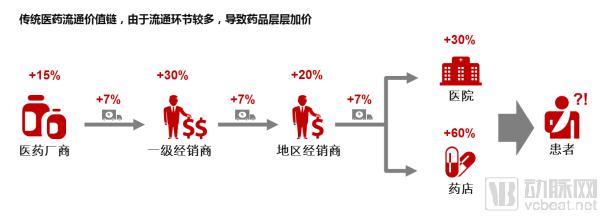

From factory gate to end-user sales, the distribution chain is fraught with complex and chaotic profit structures, leading to artificially inflated drug prices.

Even after the implementation of the “Two-Invoice System,” from the perspective of distribution channels, pharmaceuticals still flow from manufacturers to large distributors with nationwide networks, then to multiple distributors across provinces, cities, and towns, before finally reaching hospital pharmacies or retail drugstores. At each stage, upstream manufacturers often sell drugs at marked-up prices, and distributors at various levels in the distribution chain add further markups.60%approximately, with final sales terminals—hospitals and retail pharmacies—applying further markups15%-30%, the cumulative markups at each stage have collectively led to artificially inflated drug prices.

China’s National Medical Insurance Accounts Are in Deficit, Making Drug Cost Containment Urgent

2017China's Urban Employee Basic Medical Insurance in225of the pooled regions where medical insurance funds faced deficits, accounting for of China's urban employee pooled regions32%, among which22All pooling regions have accumulated deficits from previous years; the national urban resident basic medical insurance has108In some pooling regions, expenditures have exceeded revenues, placing an unsustainable burden on medical insurance funds. Furthermore, as the growth rates of expenditures for various medical insurance funds now surpass their revenue growth rates, it is imperative to urgently control medical insurance costs, particularly pharmaceutical expenses.

PBMIt has been validated in the United States to hold significant value in reducing waste and abuse of medical resources, as well as helping to address the issue of artificially inflated drug prices. Therefore,PBMHow Should Models Be Effectively Localized and Implemented in China? SuccessfulPBMWhat key success factors should the model possess?

After comparing different players in the industry, we have found that successful localization in ChinaPBMThe model must possess the following six key success factors:

i. Strong drug price negotiation power: Ensures PBMs procure drugs from upstream pharmaceutical manufacturers at lower prices

ii. Prescription Issuance and Review Capability: Ensuring that PBMs assist patients in the rational use of medications based on drug prescriptions

iii. Sufficient patient volume: Ensuring that the PBM has an adequate patient base and pharmaceutical sales volume

iv. Mature supply chain system: Ensuring efficient pharmaceutical distribution

v. Comprehensive payment-side safeguards: ensuring final payment for pharmaceuticals

vi. Continuous medication data for chronic diseases: Ensuring PBMs understand the medication patterns of patients with chronic conditions

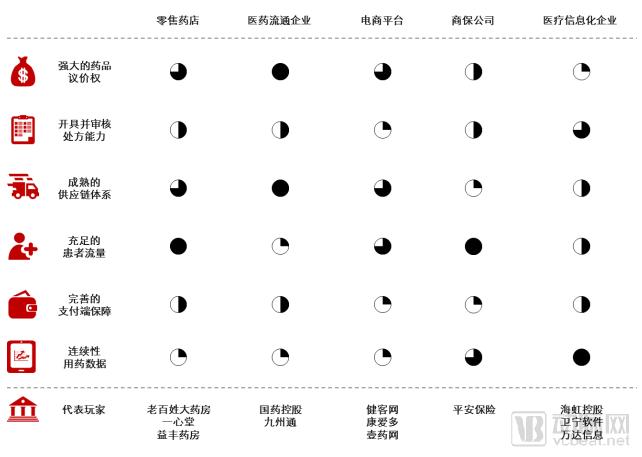

Due toPBMGiven its immense inherent value and the successful precedent set in the United States, there is a growing desire within China to emulate this model.PBMThe model has been implemented in China. Currently, the major active players in the domestic market fall into five categories: retail pharmacy chains, medical distribution companies, e-commerce platforms, commercial insurance companies, and healthcare IT enterprises. By comparing these five types of players across six dimensions, we have scored their capabilities and provided individual analyses:

Retail Pharmacy

United StatesCVS(The largest retail pharmacy chain in the United States) Its subsidiary, Caremark, is the second-largest PBM company in the United States, so many people believe that retail pharmacy chains are the best recipients for the localized implementation of PBMs. However, after research, we found that although Chinese retail pharmacies have strong capabilities in terms of patient traffic and drug bargaining power, their disadvantages are also obvious.

a) Retail pharmacies generally face high fixed costs (such as rent and labor), making it difficult to sell low-margin medications for chronic diseases.Currently, retail chain pharmacies across China are predominantly located in urban centers with high density. Their fixed costs are generally substantial, with some pharmacies’ fixed costs accounting for nearly 50% of their revenue. Consequently, to achieve profitability, most pharmacies prioritize promoting high-margin drugs with profit margins exceeding 60%. In contrast, everyday medications for chronic diseases—those truly needed by the general public—typically have gross margins below 30%, leaving pharmacies with neither the incentive nor the capacity to promote them. However, these high-volume, long-term chronic disease medications represent the core focus of Pharmacy Benefit Managers (PBMs).

b) Retail pharmacies generally lack licensed pharmacists and, consequently, suffer from relatively low public credibility.After a prescription is transferred to a pharmacy, medications can only be dispensed based on the patient’s actual condition following review by a licensed pharmacist. However, there are currently 300,000 licensed pharmacists registered in social pharmacies and medical institutions across China. Based on the total of 440,000 pharmacies nationwide, this averages out to only 0.6 licensed pharmacists per pharmacy, meaning that at least nearly one-third of pharmacies are unable to review prescriptions and dispense medications to patients.

c) Retail pharmacies find it difficult to resolve issues related to the pooling of medical insurance funds.Health insurance accounts are divided into individual accounts and pooled accounts. Currently, pooled accounts are not accessible to retail pharmacies; therefore, purchases at pharmacies are primarily made by patients paying out-of-pocket or using their health insurance individual accounts. A significant reform trend worth noting is that if future reforms integrate individual accounts into the pooled system, retail pharmacies will face considerable challenges in selling medications covered by health insurance.

Pharmaceutical Distribution Enterprises

The advantage of pharmaceutical distribution companies lies in their well-established supply chain systems, which allow for effective control over the costs of drug logistics and distribution. However, they face disadvantages in prescription issuance and acquiring consumer-end (C-end) patient traffic.

a) Pharmaceutical distribution companies cannot accept prescriptions.Prescriptions remain within the hospital system (even though prescriptions that are dispensed outside hospitals are generally filled by pharmacies and primary healthcare institutions).

b) Pharmaceutical distribution companies are distant from patients.Pharmaceutical companies rely more heavily on pharmacies for sales, which prevents them from truly reaching patients and effectively owning customer traffic.

E-commerce Platform

E-commerce platforms only address the issue of information flow.; missingBargaining Power; Inability to Fulfill Prescriptions。

a) E-commerce platforms are unable to achieve the unification of information and data.E-commerce platforms require integration with hospital HIS systems to obtain prescription orders. However, given the vast number of hospitals across China and the hundreds of HIS vendors, information silos have emerged, making unified integration highly challenging in the medium to long term.

b) Fragmented user demand has weakened the platform's bargaining power with pharmaceutical manufacturers in order negotiations.E-commerce platforms connect directly with individual patients, whose fragmented demand prevents the formation of standardized, large-volume orders. This, in turn, weakens the platforms’ bargaining power with pharmaceutical manufacturers.

c) E-commerce platforms are not yet qualified to handle prescription drugs.Relatively few platforms are qualified to issue electronic prescriptions. The electronic prescription market has not yet achieved scale, and most e-commerce platforms are limited to selling over-the-counter (OTC) medications.

Commercial Insurance Companies

Commercial insurance companies do not cover middle-aged and elderly patients with chronic diseases; their bargaining power for drug pricing and capacity to handle prescriptions are relatively weak, and the cost-containment objectives of commercial insurers conflict with the interests of pharmaceutical manufacturers.

a) PBMs cover a large number of middle-aged and elderly patients with chronic diseases, who are not covered by commercial insurance.PBM companies generally provide long-term medication services for patients with chronic diseases covered by insurance, primarily those with hypertension and diabetes. Since the majority of these patients are middle-aged and elderly, commercial insurers have historically classified them as uninsurable.

b) Commercial insurance holds a low market share and limited influence in the medical insurance sector.As a key payer in healthcare security, commercial insurance accounts for less than 20% of China’s medical expenditure, whereas social insurance covers nearly 80%. Consequently, commercial insurers lack significant bargaining power over pharmaceutical pricing and the capacity to handle prescription volumes.

c) Commercial Insurance Conflicts with the Core Interests of Pharmaceutical Companies.The core objective of commercial insurance is to achieve profit targets through cost containment, which conflicts with the interests of pharmaceutical companies; consequently, discrepancies and conflicts of interest are inevitable in the actual drug procurement process.

Medical Informatics Company

Medical Informatics Companies Have No DrugsBargaining power and prescription review authority, with no direct consumer interaction and no integration with commercial insurance.

a) Prescription drugs are predominantly dispensed within hospitals, and the authority for prescription review does not lie with healthcare IT companies, making it difficult to implement initiatives that modify prescriptions to reduce medication costs.

b) At best, the company only provides price management services for social security departments; it does not directly interface with commercial insurance and is essentially more akin to a third-party administrative tool for basic medical insurance.

c) The company only collects and manages data, does not have direct contact with offline users, and has no fixed customer base.

So, who is the most suitable end-service provider for the localized implementation of PBMs? We believe it is urban primary community health service institutions.

What Are Primary Community Health Service Institutions?

Community health service institutions are healthcare providers with Chinese characteristics, serving as the primary component of urban grassroots medical services. They are categorized into community health service centers and community health service stations. Historically, these institutions were generally government-run, with the main objective of providing basic public health services and essential medical care to community residents. In urban areas, according to30,000–100,000Community residents or planned and set up according to the jurisdiction of the sub-district office1Community health service centers shall establish several community health service stations as needed. Each community health service institution manages the residents within its jurisdiction assigned by the government, with a typical service radius of3-5kilometers.

Why Community Health Service Institutions?

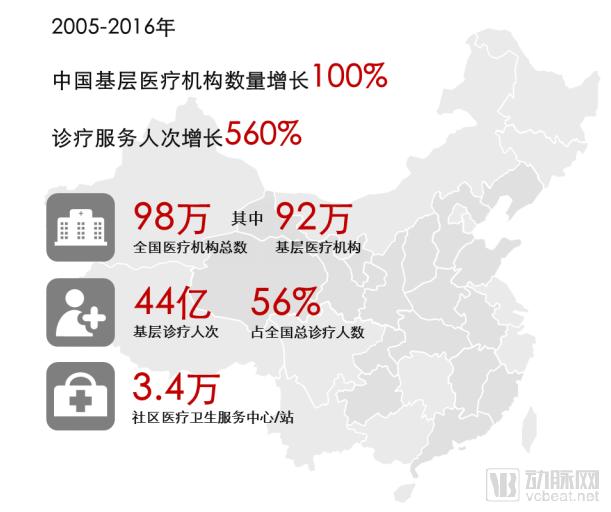

1. Community health service institutions have access to ample patient flow.

Given their government-run nature, community health service institutions enjoy inherent trust from patients. Furthermore, services such as immunization, maternal health management, chronic disease management, and routine health management for the elderly15Basic public health and medical services provided free of charge to residents are all delivered at community health service institutions. As these institutions are generally located near residential communities, offering convenient access, they attract a high volume of patient traffic.2017Annual patient visits at the Community Health Service Center nearly8100 million. With the continuous advancement of healthcare reform policies such as first-contact care at the primary level, tiered diagnosis and treatment, and family doctor contracting, patient volume is increasingly shifting to primary care institutions, driving higher traffic growth for community health service organizations.

2. Community Health Service Institutions Bear the Primary Responsibility for Chronic Disease Prevention and Control

Community-based medication primarily consists of traditional Chinese medicine preparations, antihypertensive drugs, antidiabetic agents, and cerebrovascular regulators for chronic disease management. The sales growth rate in this channel is significantly higher than that in hospital channels. Taking cerebrovascular regulatory drugs as an example,2015Annual Sales Growth Rate18%, significantly higher than that of the hospital channel5%. With the continuous advancement of policies promoting the management of chronic diseases at the primary care level, patients with chronic conditions have become a key focus of primary healthcare institutions. Long-term medication regimens for chronic diseases are relatively consistent, resulting in a comparatively lower dependence on physicians for prescription renewals. The State Council stipulates2017Year85% The aforementioned prefecture-level cities shall implement family doctor contract services to achieve the target coverage rate of family doctor services.30%Coverage Rate of Contracted Services for Key Populations60% Above. For contracted patients with chronic diseases, the quantity of medication dispensed per prescription may be extended as appropriate. For commonly used medications in the stable phase of four major chronic conditions—hypertension, diabetes, coronary heart disease, and cerebrovascular disease—the procurement and reimbursement catalogs shall be unified between large hospitals and primary healthcare institutions. Eligible patients can enjoy these benefits at primary healthcare institutions.2The convenience of obtaining a month’s supply of medication will attract more patients with chronic diseases to pick up their prescriptions at community health centers.

3. Community Health Service Institutions Are the Preferred Destination for Prescription Outflow

Unlike non-medical institutions such as pharmacies, community health service centers have the capability to prescribe and review prescriptions. Even for patients with chronic diseases who require regular medication, it is necessary to monitor changes in their condition and adjust medications accordingly. Therefore, comprehensive medical services are an indispensable element in reducing medical risks. Furthermore, community health service centers possess relatively abundant physician resources.2017Community Health Service Center in the Year3.510,000, equipped with licensed physicians190,000name, i.e., the average number of staff per outlet5.7licensed physicians, compared to the average number of licensed pharmacists, approximately0.6For human-operated pharmacies, they offer greater capacity and higher professionalism.

4. Community health service institutions have a comprehensive payment guarantee system.

Community health service institutions are all connected to the medical insurance system, allowing the use of both personal accounts and pooled funds. Against the backdrop of insufficient capacity in the medical insurance fund, it is difficult to open the pooled fund account to social pharmacies, whereas integrating personal accounts into the pooled fund better aligns with the current situation. For patients with chronic diseases, long-term medication needs result in continuous pharmaceutical expenses, making reimbursement eligibility a critical factor in choosing where to obtain prescriptions. A robust payment guarantee system will drive higher patient traffic to community health service institutions.

In summary, the PBM model, which originated in the United States, has disrupted the traditional pharmaceutical supply system. Its core philosophy has shifted from a “supply-driven” model, where physicians prescribe medications, to a “demand-driven” model centered on patient medication adherence. By leveraging lean supply chain management and highly automated warehousing and logistics systems, the model streamlines pharmaceutical distribution channels and enhances drug turnover efficiency. Furthermore, it employs data-driven models to accurately predict patient medication needs, thereby ensuring consistent medication access for patients with chronic conditions while minimizing waste from unused medicines. This approach truly delivers benefits to the public and aligns with the current direction of China’s healthcare reform policies.

Most market participants seeking to enter the space are currently unable to disrupt the entrenched interest chains and lack the capacity to create long-term value. There is a market need for a PBM platform company that understands both healthcare institutions and patients, as well as pharmaceutical manufacturers and medical insurance payers. Only by balancing the interests of all stakeholders can the existing interest chains be transformed. Starting with community-based care may be a viable approach.

About China Renaissance Capital:

Founded in 2000, China Renaissance Capital Limited is a leading new-economy investment bank and investment institution in China. Its core businesses include private equity financing, mergers and acquisitions, and asset management, with comprehensive coverage and outstanding performance in the TMT, consumer, and healthcare sectors. Over the past three years, it has completed nearly 100 financing and M&A deals, with a cumulative transaction value exceeding RMB 80 billion.