Can AI and Big Data Solutions End Health Insurance Fraud?

Where there is insurance, there is insurance fraud.

Insurance fraud can be described as a global phenomenon. In countries such as China, the United States, and the United Kingdom, insurance fraud causes substantial losses to insurers every year, particularly in the two common lines of coverage: health insurance and auto insurance.

To curb such practices, insurance companies have spared no effort. In Germany, approximately €2.2 billion in claims are illegitimate each year, while a report from the U.S. Department of Justice asserts that fraud causes annual losses exceeding $100 billion for the health insurance industry.

While the authenticity of such staggering figures remains debatable (with some statistical estimates ranging from $3 million to $4 million), in today’s landscape where profitability is sought through cost optimization, the insurance industry indeed harbors a vast hidden goldmine awaiting exploitation.

Long ago, insurance companies began using computers to assess the validity of claims, but these assessments were superficial, requiring staff to review claims flagged as “anomalous.” A McKinsey report indicates that only 10% of cases flagged as “anomalous” are truly anomalous.

"Can we replace human labor with artificial intelligence and use deep learning to assess the reasonableness of claims?"

Claims adjusters follow specific rules when determining the validity of a claim, such as assessing whether the reported event could have plausibly occurred and whether the expenses fall within the covered limits. These rules are easily learnable by AI, which can even outperform humans in this task.

After all, humans often feel drowsy when handling repetitive tasks such as these, and the connections between events are likely to be overlooked. For instance, if a patient is prescribed multiple different types of medications with equivalent efficacy for a single disease, staff members may overlook the irrationality of this practice when analyzing whether the unit drug price is reasonable—a nuance that artificial intelligence would not miss.

"If the negative social effects of unemployment among insurance company employees are not taken into account, artificial intelligence outperforms human employees in every aspect."

First, in terms of efficiency, claims that previously required dozens of employees several weeks to review can now be processed in just a few hours with artificial intelligence.

Next is accuracy. According to data from a McKinsey report, artificial intelligence could theoretically reduce current insurance fraud losses by approximately 3%, with every 1% reduction generating tens of billions of euros in gains for the insurance industry.

This approach can, to some extent, reduce the likelihood of conflicts between insurance company employees and policyholders, as the determiner of the outcome is merely an algorithm.

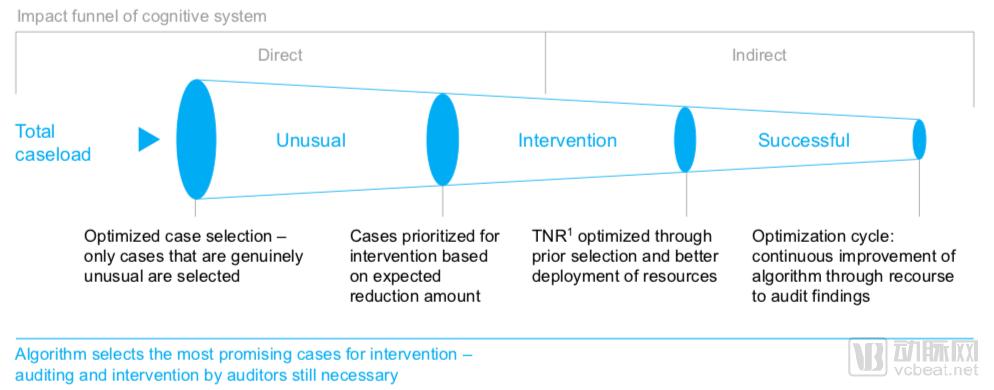

Image source: McKinsey report

The diagram above illustrates the working principle of artificial intelligence. In the first step, all claims are imported into the system, where AI performs initial screening to filter out all normal cases. During this process, the AI identifies correlations among unusual claims, which helps enhance its ability to detect anomalous cases. In the second step, the AI assigns priority levels based on the specific circumstances of each case and forwards them to reviewers, providing reasons for claim denial.

Although AI can address several key pain points in routine insurance operations, the most critical data challenges in the healthcare sector still need to be resolved (with a focus on commercial insurance).

Inputting patient data into insurance companies’ databases is inherently a cumbersome task, but the rapid advancement of computer vision can accelerate this process. For instance, the medical document recognition and analysis cloud platform developed by Yipai Intelligence can identify invoices and laboratory test reports via scanning and automatically enter the data into the database.

After data extraction, the system can preprocess textual information using NLP technology. Japan’s Fukoku Mutual Life Insurance replaced 34 life insurance claims specialists with IBM Watson starting in January 2017.

Watson can scan medical records and diagnosis and treatment histories provided by hospitals, leveraging NLP technology to extract and process this complex information, thereby freeing up staff to handle other matters related to claims settlement. Meanwhile, AI’s extensive knowledge across various domains also enables insurance companies to reduce their reliance on highly specialized personnel.

Supported by the aforementioned technologies, we can streamline the development process of cognitive systems into four components:

1. Compile and preprocess appropriate data. Given the vast volume of data that health insurance companies must handle, this task is non-trivial; the key lies in ensuring data integrity and consistency. Meanwhile, the test dataset should include historical patient data and claims data;

2. Utilize various statistical models to analyze patient, diagnosis, and claims data. At this stage, correlations between certain diagnoses and claim amounts can already be identified. This analysis lays the foundation for developing effective models to flag anomalous claims. Test data is then used to train the cognitive system. By incorporating additional insurance data and external information through analysis, the AI eventually begins to independently learn new data and case patterns;

3. To facilitate subsequent evaluation and select the system for final deployment, several cognitive systems were programmed and then benchmarked against specific metrics. Based on the test results, we selected the system capable of most reliably predicting claims;

4. Use a validated system to review new claims received under real-world conditions, and further refine the algorithm.

Given the limited depth of commercial health insurance in China and the relatively more developed commercial insurance systems in Europe and the United States, the companies engaged in AI for insurance compiled here are all located abroad.

In 2007, Accolade was founded in Seattle, Washington. Its Maya Intelligence platform helps patients select the health insurance that best meets their needs based on patient information, thereby reducing healthcare costs. Its partners include both insurance companies and clients with mandatory coverage obligations, and it currently provides related services to over 1.1 million customers.

The company stated that the platform leverages natural language processing (NLP) to analyze and synthesize text-based data, constructing user profiles based on factors such as benefit plans, medical history, and claims history to facilitate patient record management. Upon logging in, patients can access their personal profiles, demographic information, and relevant insurance details. If users wish to discuss issues such as medical care or billing with a nurse or medical assistant, the platform features a referral function that matches them with healthcare professionals best suited to their background and needs.

According to statistics, Accolade successfully reduced healthcare costs in the second year of its collaboration with Temple University Health System (TUHS), achieving total savings of $9.8 million.

Collective Health, founded in 2013 and headquartered in San Francisco, California, offers a CareX platform that integrates population health data and medical claims to streamline clients’ healthcare management processes.

In March 2017, Collective Health launched a pilot program to provide enrollment guidance for employers, employees, and their dependents, while using an AI system to track their subsequent behaviors.

As of August 2018, Collective Health had 15 employers and 70,000 employees enrolled in the CareX system.

Kirontech, founded in 2014 and headquartered in Cambridge, UK, leverages its AI-powered software platform, KironMed, to reduce inefficiencies in the claims management process.

KironMed’s algorithm is trained on data from large public databases. The algorithmic platform integrates these data to identify various types of medical claims and establish patterns associated with health insurance fraud (inaccurate billing) or waste (i.e., underutilization of services).

As of March 2017, the company had raised $3.5 million in Series A financing jointly with venture capital technology firm Leap Ventures.

Azati, founded in 2001 and headquartered in Livingston, New Jersey, leverages AI to detect fraud on insurers’ customized self-service websites and mobile insurance platforms.

When policyholders log in to the platform, they can track their claims and file new ones through Azat. If the system detects potential fraud while analyzing a new claim, it forwards the case to the insurance company’s special investigation unit (SIU) experts for further review. The software platform also provides flagged annotations to explain the rationale behind the AI’s decisions.

The use of AI in the insurance industry can hardly be considered a radical innovation; rather, it involves the integration and synthesis of various proven AI technologies. Nevertheless, this combination of diverse applications has the potential to save global insurers substantial amounts in claims payouts.

We need not worry that advanced analytics will deter individuals from purchasing insurance; only those intent on committing insurance fraud would shy away from such systems, while ordinary people will marvel at the unprecedented claims processing speed enabled by AI.

Relevant applications have been gradually developing overseas. When commercial insurance in China flourishes, we may no longer worry about choosing insurance plans.