China's Top 100 Pharmaceutical Retailers Report: Capital Frenzy Reshapes Industry Landscape

At the 2018 West China Pharmaceutical Conference, on August 13, the “2017–2018 Annual Comprehensive Competitiveness Ranking of Chinese Pharmaceutical Retail Enterprises” was grandly unveiled. As a deeply partnered media outlet for the conference, VCBeat (WeChat ID: vcbeat) attended the event in its entirety and provided comprehensive coverage.

The top 100 competitive pharmacy chains achieved a total sales volume of RMB 136.4 billion, accounting for 37.2% of China’s pharmaceutical retail market share; with a double-digit growth rate of 10.4%, they outperformed the industry average growth rate of 8.5%. As a deep-cooperation media partner of the 2018 WestPharma Conference, VCBeat (WeChat ID: vcbeat) attended the entire event and provided comprehensive coverage.

Changes in the Top 100 Competitive Chain Enterprises for the 2017–2018 Period

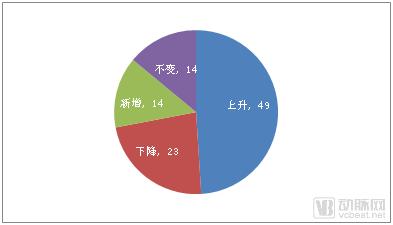

Compared with previous rankings, this year’s list highlights two prominent features: the industry landscape continues to undergo intense volatility, and polarization is becoming increasingly pronounced. Among this year’s Top 100 Most Competitive Companies, 14 new companies have been added, as 13 companies from last year’s list were acquired—including some highly ranked firms among the Top 100.

In terms of rankings, only 14 companies maintained their positions, 49 companies moved up, and 23 companies dropped. The changes in rankings were primarily driven by two factors:

First, the shift in rankings resulting from filling the vacancies left by the 13 companies that were on last year’s list but dropped off this time;

Second, competition today is like sailing against the current; without significant improvement or change, one will be quickly overtaken.

Polarization has become more pronounced than in previous years: the combined sales volume of the top 10 companies on the list reached RMB 53.3 billion, while that of the bottom 10 was RMB 3.4 billion, a 15.7-fold difference between the two.

In terms of output efficiency, a pattern emerges where higher-ranked players exhibit wider performance gaps: across the entire retail pharmacy terminal market, the top 10 chain pharmacies account for 5.5% of stores but generate 14.5% of sales revenue; the top 100 chains account for 15.6% of stores and 37.2% of sales revenue.

It is worth noting that Gaoji Medical and Quanyi Health were ineligible for the ranking, as some of their acquired chain pharmacy subsidiaries are still undergoing changes in business registration with the Administration for Industry and Commerce. Had these two companies been included in the list, the aforementioned two characteristics would have been even more pronounced.

In the pharmaceutical retail sector, major capital players can be broadly categorized into four groups: the first group consists of industry insiders, represented by the five listed companies in the sector; the second group comprises upstream capital, primarily funded by pharmaceutical manufacturers; the third group includes external capital, represented by various investment and financing institutions; and the fourth group involves cross-industry capital, represented by internet companies with operations in healthcare and pharmaceuticals.

The first category of capital consists of indigenous players, which can be described as the backbone of the industry’s development over many years;

The second type of capital is often criticized for “straying from its core business,” which tends to provoke resentment among end users; consequently, few players are willing to take the risk.

The third type of capital is currently the most financially powerful “catfish” stirring up the entire market; the fourth type, having changed its previous modus operandi, can be considered a new entrant.

The most aggressive capital forces in the current battle for market share are those of the first and third categories.

The table below reveals two major characteristics:

First, the expansion of industry and non-industry capital across China has become intertwined and interpenetrating, with many regions witnessing near “close-quarters combat.”

Second, industry insiders’ capital, being grounded in daily operations, still observes a certain degree of mutual avoidance of “spheres of influence.” In contrast, outside capital is not subject to such constraints, resulting in an intertwined investment landscape where each player’s holdings overlap with those of others.

As capital competition intensifies, chain pharmacy enterprises ranked below 50th on the Top 100 Competitiveness List have become the primary targets for acquisition. Of the 13 listed companies acquired or brought under controlling interest last year, 12 were ranked below 50th. Meanwhile, all 14 newly listed companies on this year’s Top 100 Competitiveness List fall within the bottom 50 rankings.

In terms of the forms and objectives of capital participation, the strategies are diverse, ranging from full acquisitions to majority and minority stakes, from valuation adjustment mechanisms (VAMs) tied to IPOs to those linked to performance targets, from “patchwork” listings to long-term strategic layouts, and from pursuing growth to blocking competitors.

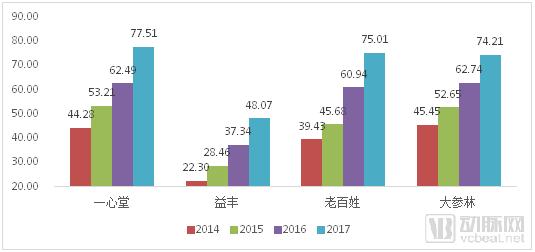

It must be acknowledged that capital has played a significant role in promoting industry growth. The most typical examples are chain enterprises such as Yixintang, Yifeng Pharmacy, Laobaixing Pharmacy, and Dashenlin, which leveraged the capital strength gained from their public listings to achieve large-scale expansion and rapid development. Meanwhile, Guoda Drugstore completed an initial round of expansion with the support of state-owned capital prior to its merger into Sinopharm Accord.

Sales Scale of the Four Major Listed Chain Stores (RMB 100 million) (Source: Annual Reports of Listed Companies)

Moreover, as the “turf war” intensified in 2017, the pace of mergers and acquisitions among the four listed companies continued to accelerate. The only player that appeared relatively “calm” was Sinopharm Holding Guoda Drugstore, a representative of the state-owned enterprises, whose capital operations focused on internationalization—its joint venture with Walgreens Boots Alliance has already been completed.

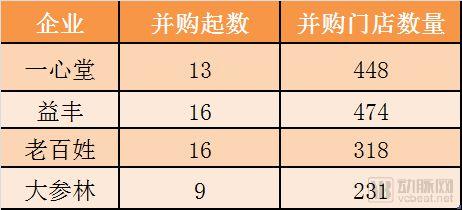

According to incomplete statistics based on publicly available information, the four major listed companies have completed a total of 54 mergers and acquisitions (M&A) since 2017, acquiring 1,471 stores. Although no public data is available for Gaoji Medical and Quanyi Health, it is widely believed within the industry that their M&A activities have been even more aggressive, with rumors circulating that Gaoji Medical aims to build a business portfolio with annual sales of RMB 50 billion.

InAmid the frenzied scramble for acquisition targets, prices have been driven ever higher, making high-premium acquisitions no longer a rare occurrence. Fuelled by this fervour, selling pharmacies has become more profitable than selling medicines. Setting aside common practices such as shopping around and hoarding to drive up prices, there are two most typical models of “pharmacy speculation”:

One approach is to sell the existing chain of stores, then immediately open a new one, rapidly expanding to 80–100 outlets before selling again;

Another approach is rapid consolidation, aggressively scaling up operations with the sole aim of bundling a larger number of stores to command a higher sale price.

Many industry insiders have expressed concern over this trend: Under such circumstances, how many people can truly settle down to conduct customer research and deliver professional services?

It also raises the question: Given the currently more severe business environment, when will the cost be recouped from such a high-premium acquisition? Some have even questioned whether large-scale, high-premium mergers and acquisitions by non-industry capital truly constitute long-term industrial investment.

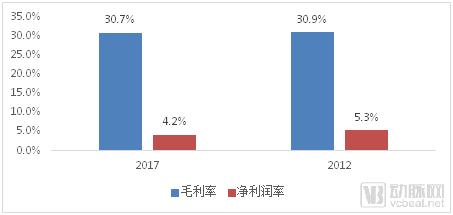

It is indeed true that the business environment has become more severe. According to a comprehensive competitiveness survey by Sinohealth Information, in 2017, the rental costs of the top 100 pharmacy chains increased by 10.7% compared to the previous year, and labor costs rose by 16.9%, yet their gross profit margin and net profit margin fell below the operational levels seen in 2012.