Six Major Shifts in China's Pharmaceutical Terminal Market under the New Healthcare Reform

On August 12, the 2018 Westpu Conference, hosted by Sinohealth Information, grandly opened in Boao, Hainan. Themed “Crossing the ‘No Man’s Land’—Division of Labor and Connectivity in Industrial Leapfrogging,” the event was covered in full by VCBeat (WeChat ID: vcbeat), which provided detailed reporting.

2017In recent years, against the backdrop of overall social and economic stability, the most significant factor influencing the pharmaceutical market has been the series of new healthcare reform policies that have already been issued and those yet to be released.

Data reveals significant shifts in the market landscape:

In 2017, the overall growth rate of terminal pharmaceutical consumption was 6%, with physical pharmacies growing by 9.9% and the segment including non-pharmaceutical products growing by 8.5%;

The growth rate of medical terminals in cities declined to 1.5%, affected by zero markup and the control of drug proportion.

Notably, the growth rate of medication use at the urban primary care level rose sharply to 8.9%, nearly 2.5 percentage points higher than the growth rate in 2016.

According to Sinohealth Information, the growth rate of pharmaceutical sales at the terminal level is expected to reach 8.3% in 2018, with a total value of RMB 1.7108 trillion. Among this, physical pharmacies are projected to grow by 8.5%, while including non-pharmaceutical products, the growth rate will be 7.5%, resulting in a total market size of RMB 393.89 billion across all categories. Urban primary healthcare institutions are anticipated to achieve a 14.1% growth rate, and the overall scale of specialized pharmacies is expected to reach RMB 48 billion.

Under the Background of New Healthcare Reform, Six Major Changes Have Emerged in the Terminal Drug Market.

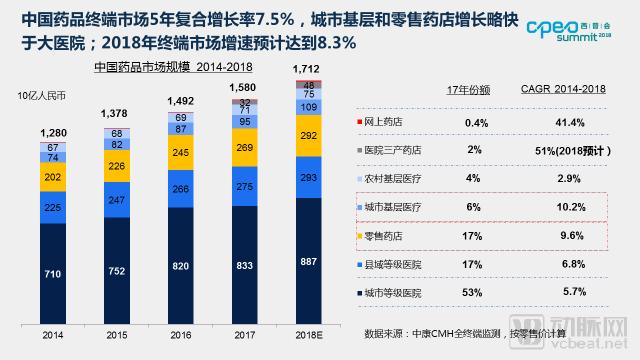

In 2017, the total size of China’s pharmaceutical market (excluding retail herbal medicines) reached RMB 1.58 trillion, representing a 6.0% increase from 2016. The five-year compound annual growth rate (CAGR) was 7.5%, with growth in urban primary care institutions and retail pharmacies slightly outpacing that of large hospitals. In 2018, the scale of China’s pharmaceutical market is projected to reach RMB 1.712 trillion, an 8.3% year-on-year increase from 2017, indicating a rebound in growth momentum.

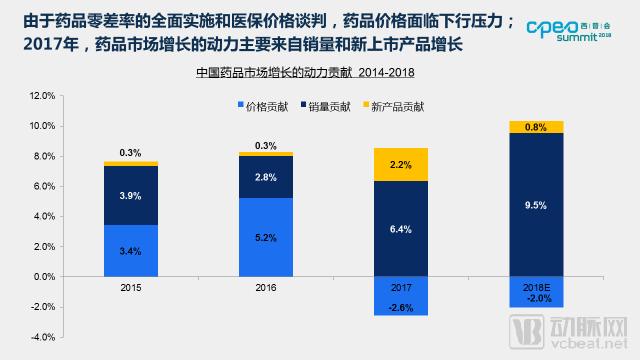

Driven by the full implementation of the zero-markup policy for pharmaceuticals and the impact of medical insurance price negotiations, drug prices are facing downward pressure. In 2017, the growth momentum of the pharmaceutical market was primarily driven by increased sales volume and the launch of new products.

Starting in 2014, provinces across China gradually implemented the zero-markup drug policy in public hospitals. By September 2017, this policy was fully rolled out in public hospitals nationwide, resulting in growth rates of only 1.5% for urban tiered hospitals and 3.4% for county-level tiered hospitals in 2017. Additionally, factors such as caps on the drug-to-revenue ratio, diagnosis-related group (DRG) payment systems, deepening reforms in medical insurance payment mechanisms, restrictions on the growth rate of medical expenses, and the expansion and deepening of comprehensive reforms in county-level public hospitals have all impacted the growth pace of tiered hospitals. However, driven by sustained growth in residents’ healthcare demands, expanded medical insurance coverage, and an enlarged national reimbursement drug list, the growth rate of urban tiered hospitals is projected to reach 6.5% in 2018, while that of county-level tiered hospitals is expected to reach 6.7%, marking a rebound in growth momentum.

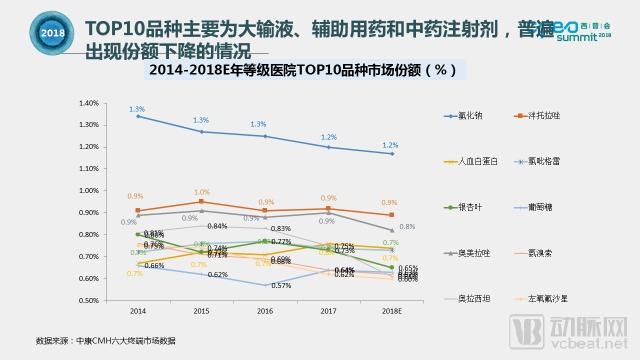

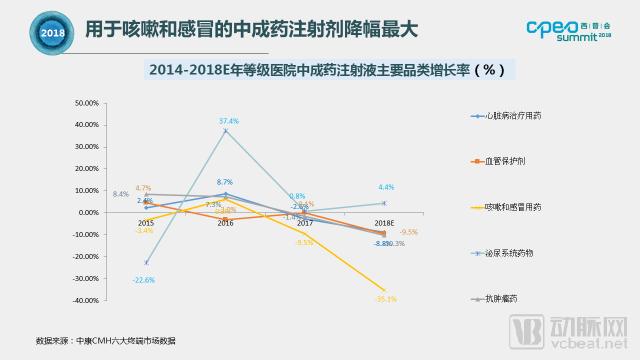

Influenced by policies such as the catalog of adjuvant drugs, control of the drug-to-revenue ratio, and restrictions on the growth rate of medical expenses, the market shares of major product categories in tiered hospitals, including large-volume parenterals, adjuvant drugs, and traditional Chinese medicine injections, have all declined.

Among major proprietary Chinese medicine injections, drugs for heart disease, anti-tumor agents, and cough and cold medications (primarily anti-inflammatory TCM injections) all experienced negative growth in 2017, with cough and cold medications declining by nearly 10%. The decline in cough and cold medications is expected to widen further in 2018.

In 2017, the market size of pharmaceuticals in urban primary healthcare institutions reached RMB 95.1 billion, representing a year-on-year growth of 8.9% and a compound annual growth rate (CAGR) of 16.0%. It is projected to grow at a rate of 14.1% in 2018, with the market size reaching RMB 108.5 billion and a CAGR of 10.2%. In 2017, the market size of pharmaceuticals in rural primary healthcare institutions reached RMB 71.2 billion, with a year-on-year growth of 3.8% and a CAGR of 7.2%. The market size is expected to reach RMB 75.0 billion in 2018, reflecting a growth rate of 5.4%.

The growth of primary healthcare institutions is mainly attributed to the initial success of tiered diagnosis and treatment initiatives, as well as the gradual relaxation of restrictions on medication use at the primary care level by various provinces.

From 2015 to 2017, the share of chronic disease medications in tiered hospitals gradually declined, while the scale and market share in primary healthcare institutions and retail pharmacies continued to rise, with the growth rate of chronic disease medication sales in retail pharmacies exceeding 10%.

Prescription outflow has recently become a hot topic of discussion. Taking the “Wuzhou Model” as an example, a prescription information-sharing platform linking hospitals and pharmacies was established, allowing patients to voluntarily choose to fill their prescriptions at pharmacies within the external sharing platform. Since the launch of the prescription information-sharing platform, the proportion of chronic disease medications sold by retail pharmacies in Wuzhou has steadily increased compared with 2016 levels. After the number of participating pharmacies was expanded in November 2017, the share of chronic disease medications reached its highest level in nearly two years. In July 2018, direct settlement of outpatient special chronic disease prescriptions covered by basic medical insurance at participating shared pharmacies was piloted, giving reason to believe that this proportion will continue to rise. Establishing a prescription information-sharing platform between hospitals and pharmacies is an effective approach to promoting prescription outflow.

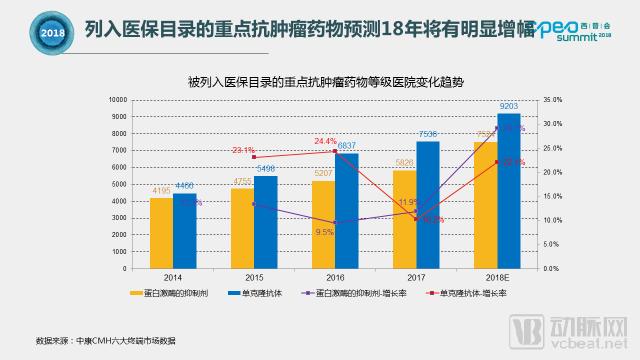

The market share of antineoplastic agents continues to grow, with key oncology drugs included in the National Reimbursement Drug List (NRDL) expected to see a significant increase in 2018. Although inclusion in the NRDL exerts downward pressure on drug prices, patient demand and reimbursement policies will further expand the user base and drive up utilization volumes. Taking novel antineoplastic agents such as protein kinase inhibitors and monoclonal antibodies as examples, their average annual growth rate in tiered hospitals from 2014 to 2018E was between 17% and 18%.

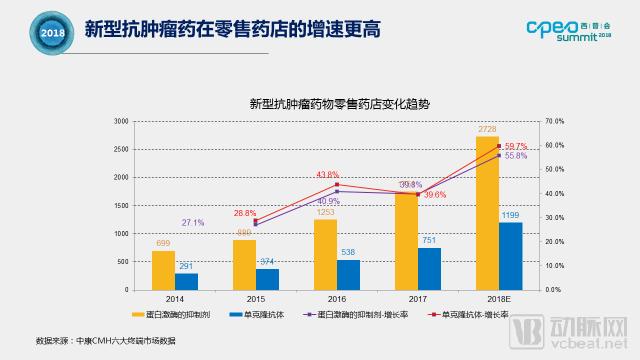

Due to factors such as healthcare insurance cost containment, price caps in centralized procurement and bidding, and prolonged bidding processes, some new specialty drugs have chosen to launch first in retail pharmacies. High-priced drugs already on the market, such as anti-tumor agents, are also shifting toward the retail pharmacy channel. From 2014 to 2018E, the average growth rate of retail pharmacies reached as high as 40%–42%. Notably, the market size of protein kinase inhibitors in retail pharmacies accounted for 25.8% of that in tertiary hospitals in 2017, and is projected to exceed 30% in 2018. Retail pharmacies, particularly emerging DTP (Direct-to-Patient) pharmacies, will become important channels for newly launched drugs and high-priced medications such as novel anti-tumor therapies.

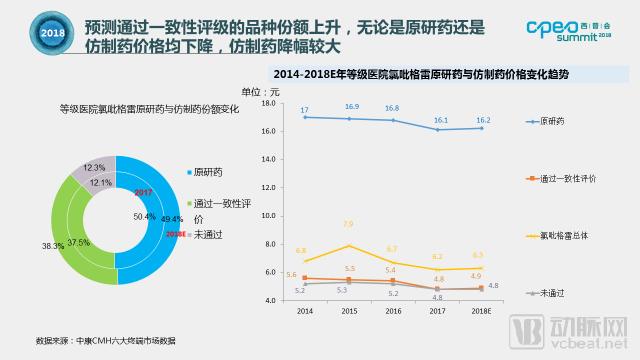

As of May 2018, there were 21 drug varieties for which at least one generic product had confirmed passage of the consistency evaluation, and 45 generic drug specifications (product-strength combinations) had either passed or were deemed to have passed the consistency evaluation. The market size for these relevant generic names was expected to see a significant increase in 2018. As an increasing number of domestic manufacturers pass the consistency evaluation, further downward pressure will be exerted on both the market share and pricing of non-patented originator drugs. Taking clopidogrel as an example, the market share of the originator product is projected to decline in 2018, while the share of generic products that have passed the consistency evaluation will continue to expand; in contrast, the share of generic varieties that have not passed the evaluation will experience only a slight increase. In terms of pricing, both originator and generic drugs have seen price reductions, with generics experiencing a more substantial decrease. The substitution of imported originator drugs by generics that have passed the consistency evaluation represents a long-term trend.