TCID Model for Evaluating Investment Value of Healthcare Startups Files Prospectus

Author: Wu Han

Since entering the industry, I have successively participated in the investment activities of more than ten early-stage healthcare startups. The project fields include in vitro diagnostics, minimally invasive surgery, digital health, and biotechnology, with a geographic scope covering China and Israel.

Recently, while reflecting on past investment logic, I have attempted to summarize a small analytical framework to assist in evaluating the investment value of healthcare startups. I hope to engage in discussion and exchange with everyone, and welcome corrections and critiques to continuously refine this model.

For simplicity, the author temporarily refers to this model as the “TCID Model”—Technology (R&D); Clinical; Industrialization; Distribution.

“TCID” Model

Mr. Liu Qin of Morningside Venture Capital once said, “Investment decision-making is a complex process, with a wide array of qualitative and quantitative tools in its decision-making toolkit. For early-stage investment decisions, due to significant information asymmetry, one cannot entirely rely away from investors’ experience and subjective judgment. However, I would like to emphasize that the more experienced an early-stage investor is, the more adeptly they will employ objective tools to make extensive rational assessments. Yet, at the critical moment of final decision-making, they will inevitably rely on their own inner art of decision-making.”

This statement has had a profound impact on the author. The investment evaluation of early-stage startups is the result of both rational and emotional assessments, and proficiency in various types of evaluation tools and models is an indispensable component thereof. The author once wrote an article titled"14 Dimensions for Analyzing Venture Capital Projects", which can be considered a more foundational model, while the author hopes to further focus on discussions within the healthcare industry in this article.

It is important to emphasize that any single model can only assist in evaluating projects from a specific perspective. Assessing healthcare startups requires the application of diverse thinking tools and models from various disciplines, such as management, economics, finance, business history, psychology, engineering, and basic sciences. The “TCID Model” was developed from the perspective of evaluating the industrialization process of medical products and is primarily applicable to investment assessments of medical device and biopharmaceutical startups.

Let us now proceed to deconstruct the “TCID Model,” with each module further subdivided into six dimensions by the author.

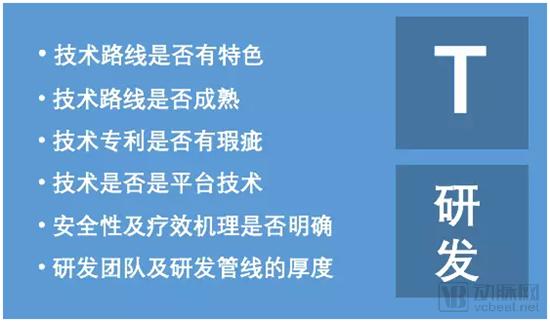

Six Dimensions to Consider When Evaluating R&D Capabilities

R&D capability is the aspect that venture capital firms focus on most in all pharmaceutical and medical device projects. The commercialization of virtually all such startups is driven by their R&D capabilities, and these companies are often founded based on inventions by scientists, inventors, or clinicians.

It is a significant advantage when a startup’s technology originates from top-tier scientists or engineers. However, it is crucial to recognize that technical founders may lack the capability to commercialize their inventions. The industrialization of their technology often requires collaboration with professionals from various disciplines, such as chemical engineers, materials engineers, mechanical engineers, biomedical engineers, manufacturing engineers, clinicians, and patent attorneys. In such cases, investors need to assess whether the startup’s R&D team includes experienced personnel who complement the technical founder’s expertise.

Due to limited funding and platform influence, startups often fail to secure the necessary professional talent. Even companies founded by renowned scientists frequently struggle to recruit strong R&D personnel within their specific fields. In such cases, investors must prioritize assessing the company’s ability to integrate resources through external collaborations and evaluate the maturity of the industry chain. This ensures that the company can successfully commercialize its core technologies by fully leveraging external resources.

Why is the majority of venture capital investment in China’s healthcare industry concentrated in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen, along with their surrounding areas? This is because these regions boast strong hospital capabilities, an abundant talent pool, and more mature industrial support systems with refined specialization, all of which can sustain the growth of startups.

The author breaks down the R&D capabilities of startups into the following six dimensions for evaluation:

The technological roadmap must demonstrate sufficient differentiation and unique selling points, while also establishing technical barriers that prevent easy replication by competitors.

The technological approach must be sufficiently mature for clinical use; one should not blindly pursue “cutting-edge” technologies. While “cutting-edge” is the goal of scientific research, clinicians prioritize product safety, efficacy, and thorough validation.

Has the company established a robust patent portfolio? Is there any risk of conflict with third-party patents? Can the existing patents adequately protect the products against imitation?

Venture capital firms seek sustained growth in their portfolio companies. In the medical device sector, niche markets are often too small; therefore, whether a technology possesses platform characteristics determines a medical device company’s potential for horizontal expansion using its core technology.

For pharmaceutical companies, given the substantial risks associated with developing individual new drugs, venture capital firms tend to favor companies equipped with platform technologies to hedge against R&D risks.

During the clinical promotion of medical products, regulatory authorities and physicians prioritize product safety above all else, with efficacy being a secondary consideration. To obtain regulatory approval, medical products must fully elucidate their mechanisms of action; robust foundational research serves as a critical basis for successfully navigating clinical trials and securing regulatory clearance.

Startups often have limited human resources. The ability to continuously generate and build a pipeline of new product lines through collaborations with external research institutions and universities, thereby expanding future growth potential, would be a significant advantage in the eyes of investors.

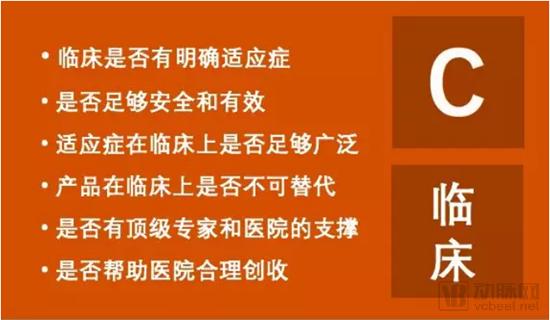

Six Dimensions to Consider in Assessing Clinical Competence

In countries with advanced healthcare entrepreneurship, such as the United States and Israel, clinical practice and R&D often collaborate seamlessly, with many physicians actively participating in product development at startups. In China, however, the scarcity of medical resources means that clinicians have insufficient time for patient care, while also dedicating substantial hours to teaching and academic research. This results in a relatively low willingness to engage in startup R&D, leading to numerous instances where startup products face significant challenges in clinical adaptation after being introduced into practice.

Therefore, it is particularly crucial for startups to engage in “close collaboration” with clinicians from the very inception of R&D, so as to develop products with clearly defined clinical use scenarios that hospitals and physicians are willing to pay for and distributors are willing to help promote.

Whether prominent clinical experts are involved and whether collaborations with prestigious hospitals are established are critical evaluation metrics for investors during investment assessments. To secure partnerships with leading hospitals and experts, a company’s product must address urgent clinical needs and provide substantial support for physicians’ and hospitals’ scientific research.

The author breaks down the clinical capabilities of startups into the following six dimensions for evaluation:

In clinical practice, disease treatment largely relies on “combination therapy,” where any given drug or medical device serves as just one component of such a regimen. Moreover, a single product is often not suitable for all patients within a particular disease category. Therefore, during project evaluation, investors need to clearly analyze the specific indications and scope of application of the product.

The safety and efficacy of the product are the most fundamental pillars for the sustained growth of a startup.

The number of patients with the indicated condition determines the potential market size.

For a specific patient population, various therapeutic options are available, and even for the same therapy, products are offered by different manufacturers. Product irreplaceability constitutes the core competitive advantage.

The medical community is highly conservative, and leaders in various specialties wield significant influence as opinion leaders within this group. Therefore, promoting new products in clinical settings without the support of these specialty leaders is inefficient and fraught with difficulties.

Meanwhile, in the clinical trial phase, key opinion leaders (KOLs) can provide substantial assistance to startups. The clinical experience of physicians overseeing trials significantly influences their outcomes. Furthermore, KOLs can leverage disciplinary resources more effectively, thereby accelerating the progress of clinical trials.

Although some products can improve the quality of medical care in clinical practice, they may still encounter obstacles during procurement if they fail to significantly increase hospital revenue. Analyzing whether a company’s product meets the interests of all stakeholders along the value chain can help investors assess its future market sales prospects.

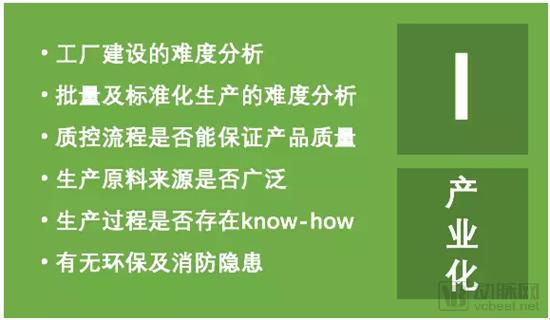

Six Dimensions to Consider When Assessing Industrialization Capability

The industrialization of high-tech medical products in Europe and the United States is highly mature, with a clear division of labor: large pharmaceutical and medical device companies typically handle industrialization and marketing, while small startups focus on product R&D and clinical trials. In contrast, founders of Chinese medical startups often have to “go it alone” throughout the entire process, managing everything from early-stage R&D and clinical trials to industrialization and market promotion. However, many founders lack experience in industrialization. Successfully transitioning from product R&D to production and then to sales requires either bringing in strong external support or possessing exceptional learning agility and execution capabilities.

For this reason, investors need to conduct a comprehensive assessment of whether a startup possesses the capability to build manufacturing facilities (which also significantly tests the founders’ fundraising abilities) and the ability to manage and control production processes.

China has implemented the marketing authorization holder (MAH) system for pharmaceuticals and medical devices, allowing product manufacturing to be outsourced to third-party factories with comprehensive production qualifications. While this policy helps alleviate related challenges, many startups still need to establish their own manufacturing facilities. Even when outsourcing production to third parties, startups must possess strong supply chain management capabilities.

The author breaks down the industrialization capabilities of startups into the following six dimensions for evaluation:

The geographic location of the industrial park where the factory is situated, the management standards of the park, the extent of policy incentives, and the level of supply chain integration are particularly critical for medical startups.

In the era of precision medicine, the launch of personalized medical products such as CAR-T will continue to test manufacturers’ personalized production capabilities.

The “Changsheng Vaccine” incident fully underscores the critical importance of production quality control for medical companies, a matter vital to their very survival. Yet, due diligence on production quality is often overlooked by many investors.

The breadth of sourcing for raw materials determines the stability of a company’s production capacity and its bargaining power over upstream suppliers.

Protecting production process know-how is another key factor for medical startups to maintain competitiveness, in addition to intellectual property.

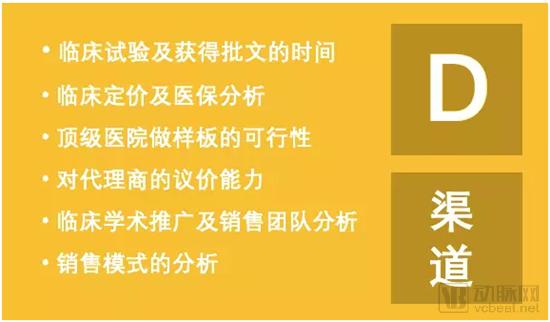

Six Dimensions to Consider When Assessing Channel Capabilities

Channel promotion capability is the core foundation for medical startups to achieve "self-sustaining cash flow." For medical startups, it typically takes 1–3 years for R&D and another 1–3 years for clinical trials. During the first two years after obtaining market access approval, companies are largely engaged in academic promotion with minimal revenue generation. However, robust channel promotion capabilities can enable companies to reach the break-even point more quickly.

The author breaks down the channel capabilities of startups into the following six dimensions for evaluation:

Most healthcare startups that secure venture capital funding develop Class III medical devices or novel drugs. These products typically entail prolonged clinical trial cycles and involve numerous uncertainties. An objective assessment of clinical trial design, site selection, trial costs, regulatory communication status, and the timeline for obtaining approvals has a decisive impact on the valuation and pricing of investment projects.

For domestically produced substitute products, clinical pricing and medical insurance coverage are relatively mature, so the challenges are not significant. However, for innovative products, considerable effort is required to be included in the fee schedules of public hospitals or to gain medical insurance reimbursement. Therefore, investors need to assess the difficulty and timing of a product’s inclusion in fee schedules and medical insurance coverage.

For both physicians and distributors, whether a company’s products have gained entry into top-tier hospitals and received substantial recognition serves as a key indicator, laying the foundation and acting as a stepping stone for future large-scale market penetration.

Given China’s vast territory, multi-tiered market structure, and complex interest chains, most medical device and pharmaceutical companies rely on distributors for sales. If a company’s product generates low sales volume per individual healthcare institution and the market is highly fragmented, or if large distributors wield strong channel resources while the company’s products account for only a small fraction of the distributors’ total sales, the company lacks bargaining power vis-à-vis its distributors. In such scenarios, the company faces extended payment terms, lower gross profit margins, and significant cash flow pressure.

Startups rarely cultivate their own Marketing and Sales Directors; instead, they typically recruit professional managers from multinational corporations or large domestically listed pharmaceutical companies to serve as Chief Marketing Officer (CMO) and Chief Sales Officer (CSO). Key assessment criteria include the candidate’s cultural fit with the company, the alignment of their prior experience and resources with the company’s product portfolio, and their ability to lead teams.

Sales models for medical products are diverse, including government centralized procurement, hospital centralized procurement, intensive on-the-ground promotion by sales representatives, bundling with other manufacturers’ offerings into larger product portfolios for monetization, and direct-to-consumer (DTC) sales. The level of difficulty varies across each sales model. Investors should comprehensively assess the feasibility and complexity of a company’s sales model.

This concludes the analysis of the four-dimensional TCID model for investment evaluation of healthcare startups.

Finally, the author believes that when using the TCID model to evaluate the investment value of early-stage healthcare companies, it is not necessary for a company to excel in all four dimensions to be considered a worthwhile investment. However, high-quality companies must demonstrate sufficient excellence in both the R&D and clinical dimensions. If their valuation is reasonable, such companies are attractive acquisition targets. If a company performs excellently across all four dimensions, it possesses the potential to become a platform-type enterprise.

Author Introduction:

Wu Han, Project Manager at Qunfeng She. He holds a Master’s degree in Biomedical Engineering from the University of Southern California and a Bachelor’s degree in Biological Sciences from Huazhong University of Science and Technology. At Qunfeng She and Fenxiang Investment, he has participated in investment projects across multiple medical sectors. He was involved in founding a startup service platform for the healthcare industry and has experience in the preparatory work for establishing private general hospitals. He focuses on investment opportunities in early-stage healthcare startups.