Global and Domestic Oncology Big Data Companies: Who Can Address Pharma's Pain Points?

Clinical medical data is akin to a treasure buried deep within remote mountains; although gold deposits exist, without advanced mining equipment, these vast resources remain as barren and unproductive as a Gobi Desert. Clinical big data holds immense value for pharmaceutical companies, healthcare providers, payers, and patients alike. However, due to low data density, data silos, and the lack of linkage between large volumes of data and long-term patient follow-up, this potential remains largely untapped.

With the unprecedented growth of medical data, many companies are leveraging analytical tools, artificial intelligence, and machine learning technologies to obtain data-driven decision support, thereby reducing healthcare costs, enhancing hospital revenue streams, developing personalized medicines, and managing patient care. As more payers enter the market, the role of big data applications in improving healthcare outcomes at the clinical level has become increasingly evident. We can see that a new generation of pioneers is reaching the pinnacle of success.

Data also corroborates this point. According to a report by BIS Research titled “Global Big Data Analytics in Healthcare Market: Analysis and Forecast, 2017–2025,” the market size for big data in the healthcare sector was estimated at $14.25 billion in 2017 and is projected to grow to over $68.75 billion by the end of 2025.

Which companies have achieved breakthroughs in the field of medical big data, and from what directions have innovative enterprises tackled the challenges of applying medical big data to tap into this lucrative resource? VCBeat (WeChat: vcbeat) has conducted a comprehensive review.

The medical big data market has experienced such significant growth because it can meet diverse requirements.

For pharmaceutical companies, large volumes of patient data can drive real-world studies (RWS), addressing critical industry needs. After a drug is launched, pharmaceutical companies are required to submit post-marketing safety monitoring data; failure to do so may result in the risk of market withdrawal. Real-world studies can help meet these regulatory compliance requirements while expanding drug accessibility and market capacity. For example, consider a medication indicated for patients with late-stage cancer. By leveraging real-world data to demonstrate the drug’s efficacy, it may be reclassified from a second-line to a first-line therapy, thereby extending its use to earlier stages of treatment and tapping into a broader market, ultimately increasing the drug’s market capacity.

In new drug development, the advancement of precision medicine and personalized medicine enables medical big data to provide strategic direction. Observational studies based on real-world data can elucidate disease incidence, prevalence, burden, complications, and diagnosis and treatment patterns, thereby identifying critical clinical issues that urgently need to be addressed. Furthermore, real-world evidence (RWE) may offer insights into pathogenic mechanisms, facilitating the discovery of potential therapeutic targets.

Big data can also address the challenge of patient recruitment. The probability of clinical trials gaining FDA approval is approximately 7%. About one-third of Phase III clinical studies are terminated due to difficulties in patient recruitment. Data from IQVIA indicates that 37% of clinical trial sites fail to meet their patient enrollment targets. Pharmaceutical companies and CROs struggle to match suitable patients; with the advent of precision medicine and personalized healthcare, the target populations for drugs are expected to become increasingly smaller.

Taking oncology, a therapeutic area fiercely contested by major pharmaceutical companies, as an example, the discovery of an increasing number of molecular subtypes has led to continuously shrinking patient populations in each subgroup, making it increasingly difficult for traditional randomized controlled trials (RCTs) to identify and enroll eligible participants. Meanwhile, with the substantial influx of new anticancer drugs, the demand for evaluating their efficacy has grown significantly. In 2017 alone, Roche had 488 ongoing oncology clinical trials.

Furthermore, the FDA is also mandating greater patient diversity, both in clinical trials and post-marketing. Experience has demonstrated that the more diverse the patient population enrolled in clinical trials, the safer and more effective the products tend to be. However, identifying a sufficient number of eligible clinical trial participants within appropriate parameters is considerably challenging without the aid of big data. Traditional randomized controlled trials (RCTs) have imposed strict exclusion and inclusion criteria, resulting in significant patient homogeneity and preventing many patients from accessing clinical trials.

Post-marketing, vast amounts of healthcare big data can also help expand the scope of drug utilization. In new drug development, fewer than one in a thousand active compounds advance to Phase I clinical trials; therefore, identifying new indications for existing drugs offers substantial returns on investment. Historically, pharmaceutical companies could only discover new indications through costly randomized controlled trials (RCTs), a process that was both time-consuming and expensive. Registration costs were exceedingly high, accompanied by significant risks. In terms of effectiveness, RCTs represent highly specialized scenarios, whereas real-world studies, involving large numbers of participants and considerable patient samples with long-term follow-up, place greater emphasis on outcome measures with clinical significance.

It is worth noting that in recent years, the application of real-world studies (RWS) in clinical research on Traditional Chinese Medicine (TCM) has also attracted considerable attention. Real-world studies break through the constraints of traditional randomized controlled trials (RCTs), which require simple and well-defined interventions, effective control measures, and highly homogeneous study populations. Centered on patients, RWS emphasizes holistic therapeutic outcomes in its evaluation metrics, making it more suitable for the characteristics of TCM.

Large volumes of real-world data (RWD) not only address the critical needs of pharmaceutical companies but, once reaching a sufficient level of evidence, also fulfill physicians’ research requirements. This helps physicians reduce the time spent on academic publications while achieving superior research outcomes. For hospitals, RWD offers richer application scenarios, enabling more efficient management and more patient-centered services. Big data can be leveraged to evaluate medical practice processes. For instance, vinorelbine tartrate, a chemotherapy agent used in the treatment of lung cancer and breast cancer, is available in both oral and intravenous formulations. By comparing and analyzing patients receiving these different routes of administration, it has been found that oral administration significantly reduces patient waiting times and improves the throughput efficiency of chemotherapy centers.

Although big medical data is a gold mine, exploiting it is by no means easy. From a policy perspective, the introduction of regulations typically involves both oversight and promotion. In 2016, the United States enacted the 21st Century Cures Act, which introduced two concepts: RWD (Real-World Data) and RWE (Real-World Evidence). This legislation established requirements for health big data to meet the standards of medical evidence. For health big data to achieve the level of medical evidence, it must attain a certain degree of relevance and reliability. Data traceability must also be ensured, while strictly safeguarding privacy and security.

In 2016, the European Union introduced the General Data Protection Regulation (GDPR), its most stringent data protection regulation. It mandates transparency in personal data processing and adherence to the principle of data minimization, while granting data subjects rights such as the right to withdraw consent at any time, the right to be forgotten, and the right to data portability.

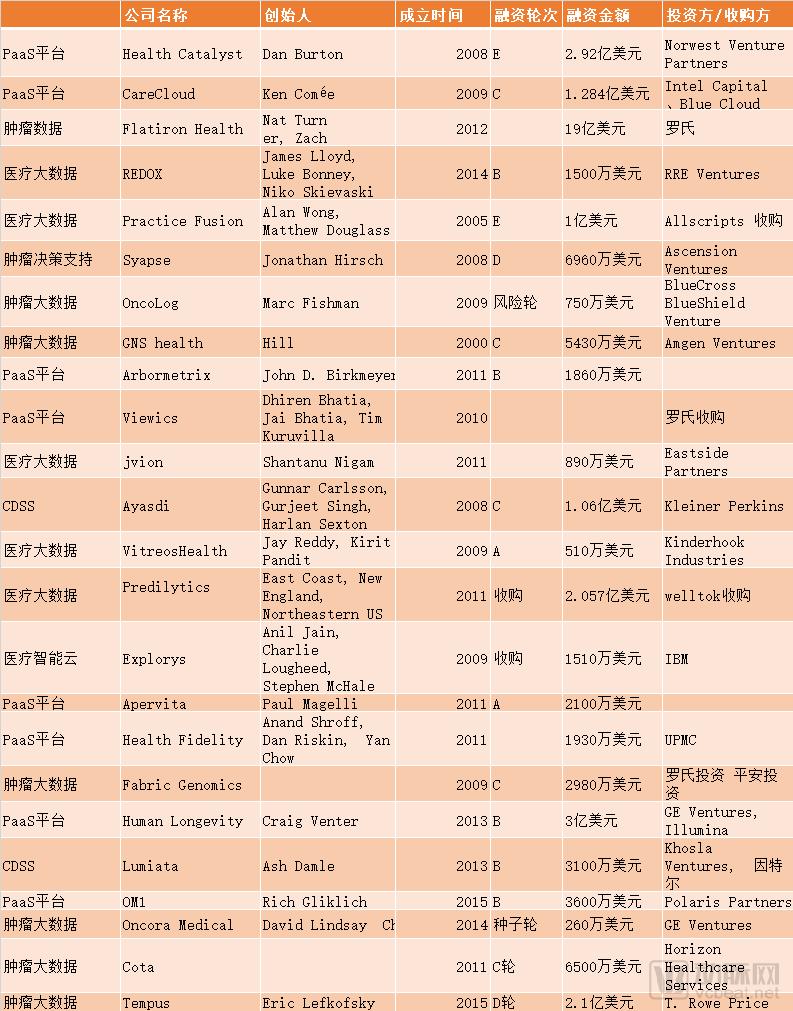

Data Sourcecrunchbase 、CBInsight Chart by VCBeat

A review reveals that many foreign companies primarily provide Platform-as-a-Service (PaaS) to healthcare providers. By transforming vast amounts of data into actionable insights, these platforms leverage artificial intelligence or machine learning to offer decision support. In addition to startups, this sector has attracted numerous industry giants. Major corporations involved include GE Healthcare, Truven Health Analytics, UnitedHealth Group, Philips, Premier, Inc., SAP, SAS, Siemens Healthineers, Tableau Software, Inc., Xerox, Verisk Analytics, Allscripts, Sparx IT Solutions, and Oracle. Similar to the domestic market in China, the oncology sector is the area where precision medicine is advancing most rapidly and where the highest number of startups are concentrated.

The recent rise of clinical oncology companies stems from the high complexity of cancer treatment. Data can transform this process, enabling healthcare professionals to convert optimal treatment plans into replicable templates rather than relying solely on empirical experience.

Oncology big data holds immense value.Tumor types are diverse and can occur in every organ. EMR, digital imaging systems, omics data, and more can all generate massive amounts of data.Oncology has always been a top priority for pharmaceutical companies. In 2017, the top 25 oncology drugs worldwide generated combined sales of $79 billion. According to an IQVIA report, “The global oncology therapeutics market is projected to reach $200 billion by 2022, with an average annual growth rate of 10–13% over the next five years. The U.S. market alone is expected to reach $100 billion by 2022, growing at an average annual rate of 12–15%.”

Spending on cancer drugs is concentrated in a few treatments, with the top 35 drugs accounting for 80% of total expenditure, while more than half of cancer drugs have annual sales of less than $90 million. Over the past decade, the launch prices of new anticancer drugs have steadily increased, with the median annual cost exceeding $150,000 in 2017, compared to $79,000 in 2013.

Overseas startups primarily adopt two business models, one of which involves charging healthcare providers and insurers. This is because the decision support enabled by big data can lead to better clinical outcomes, improved efficiency, and cost savings. As health insurance increasingly shifts toward value-based care and outcome-based payment models, both healthcare providers and payers are facing mounting pressure to control costs. Consequently, the customer base for such companies continues to expand.

The second model involves offering services similar to Google’s, as seen with companies like Flatiron and Tempus. These companies provide free or low-cost services and generate revenue by leveraging data collected in the background. The largest payers for such data are pharmaceutical companies. Data holds immense value for pharmaceutical firms; regardless of the business model, they remain significant potential customers. Cancer care costs have been rising year over year, with global spending on cancer drugs continuing to grow. Expenditures on treatment and supportive care reached $133 billion in 2017, up from $96 billion in 2013.

Although large volumes of patient data hold significant monetization potential for pharmaceutical companies’ sales efforts, data firms abroad have not yet capitalized on this value from a sales perspective. Currently, their primary focus is on customer acquisition, particularly in a market already crowded with powerful incumbents such as IBM Watson and GE Health.

The second challenge is how to meet compliance requirements in a strictly regulated market. It will take some time to transform real-world data into real-world evidence.

Undoubtedly, pharmaceutical companies must actively participate in this endeavor. As evidenced by the above overview, pharmaceutical giants such as Roche have already targeted multiple big data companies through investments and mergers and acquisitions. Leveraging big data to transform pharmaceutical processes is also a policy trend promoted by the U.S. Food and Drug Administration (FDA). Dr. Scott Gottlieb, then Commissioner of the FDA, stated in an oral presentation: “Reform of clinical trials is imperative. Efficient and modern clinical trial designs can accelerate the market approval of new drugs. If you adopt modern, evidence-based, and rigorous approaches, you can ensure substantial efficiency and provide strong assurance for the FDA’s gold standard.” To promote clinical trial reform, the FDA has issued multiple guidance documents, including recommendations for interoperability between Electronic Data Capture (EDC) systems and Electronic Health Record (EHR) systems, and allowing the omission of placebo controls in most cancer clinical trials.

Secondly, with the application of real-world data, pharmaceutical companies that continue to adhere to traditional R&D paradigms will face greater risks. Once oncologists and other stakeholders are able to precisely track the treatment trajectories of cancer patients, the efficacy—or relative efficacy—of a specific therapy can be rapidly and accurately determined if it proves ineffective, or appears ineffective in a (potentially molecularly defined) subset of the patient population. This could immediately puncture pharmaceutical companies’ narratives and undermine their confidence.

The panacea narratives touted by pharmaceutical companies may pale in comparison to real-world data. Do these companies have the confidence to face this? A report from Accenture points out that among the top 10 best-selling drugs, these medications are effective in only 4% to 25% of the patients who take them.

Therefore, it is essential for pharmaceutical companies to predict real-world efficacy prior to market launch, as the constraint on commercialization may no longer be the FDA’s review based on clinical trial data, but rather whether the drugs can pass real-world validation conducted by oncology clinical data companies.

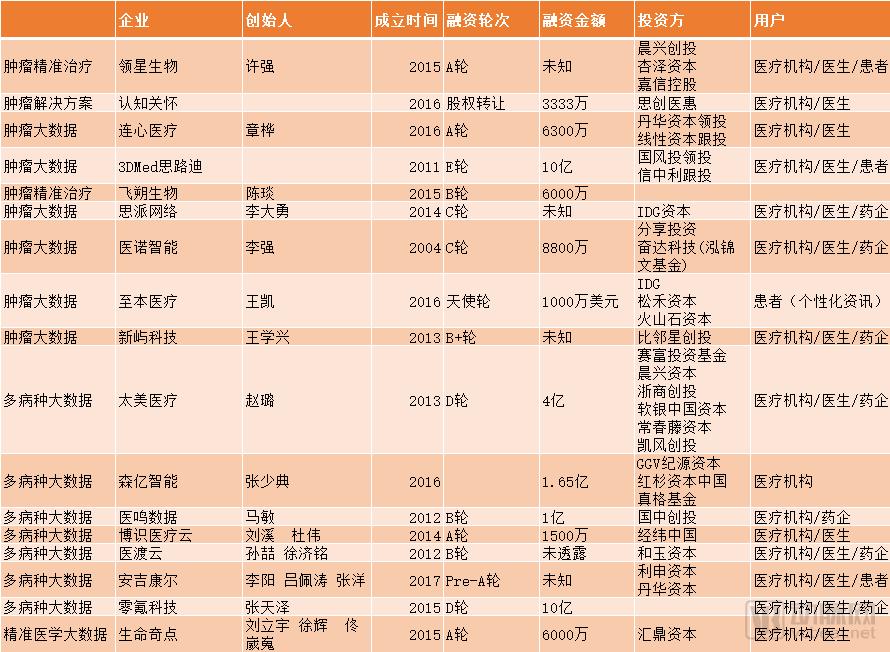

Data source: Qichacha; Chart by VCBeat

Due to the late start of digital health in China, many domestic enterprises are addressing data collection issues by focusing on structuring data through unified data standards.

In China, both policy makers and the capital market are highly optimistic about the development of medical big data. In 2016, the General Office of the State Council issued Document No. 47 to promote and standardize the application of health and medical big data. Health big data has been designated as a critical foundational strategic resource, subject to state control akin to petroleum and electricity. VCBeat has also reported that between 2013 and 2015,A total of 58 policies related to health and medical big data have been issued by local authorities across various regions.。

In terms of data standardization, the state has successively issued guiding documents such as the Basic Architecture and Data Standards for Electronic Medical Records and the Specification for Shared Documents of Electronic Medical Records. In addition, many hospital information systems have participated in the interoperability maturity assessment, laying the foundation for future data applications.

It is worth noting that the policy explicitly mentions the need to study and formulate government support policies, providing necessary support for the development of health and medical big data applications in areas such as fiscal and tax incentives, investment, and innovation.

In terms of policy support, the U.S. FDA has made significant efforts to promote data structuring and standardization. The federal government has spent over $28 billion in the past decade to implement digital electronic health records. In China, however, unified standards have not yet been established. Chinese policies cover a broader scope; in addition to promoting data sharing and standardization, they also include cultivating talent in medical big data and encouraging both state-owned and private capital to participate in the development of the medical big data sector.

In the domestic market, although medical big data companies started later than their foreign counterparts, they have already established an upstream and downstream layout across the entire industry chain. Analysts point out that while there have been numerous financing projects in China’s medical big data sector over the past six months, current domestic applications still lag behind in capabilities for data mining, analysis, and analytical platform development. Platform-based data analytics capabilities remain weak; efforts are largely concentrated on single dimensions, with limited integration of diversified data analysis objectives. Furthermore, value presentation and value circulation have yet to form an ecological loop.

In the domestic market, which has been focused on data collection, data analysis is considered the true value of big data, in line with estimated industry development trends. According to IQVIA’s forecast report, among various big data components and services, analytics services dominate the market, generating $5.8 billion in revenue in 2017, with a projected compound annual growth rate (CAGR) of 22.3% during the 2017–2025 forecast period.

After realizing the value of data, future efforts will leverage computational tools to facilitate intelligent decision-making, enabling the development of systems that can track patient information and provide rapid feedback. The primary payers for medical big data fall into six main categories: consumers, enterprises, insurance companies, governments, hospitals, and pharmaceutical companies.

In the short term, hospitals demonstrate the strongest willingness to pay among insurers and pharmaceutical companies. Representative enterprises in both sectors have begun exploring big data applications. For instance, Chinese pharmaceutical and biotechnology firms such as Hengrui Medicine, Hua Medicine, and Tiantan Biological Products have already partnered with Oracle on healthcare big data initiatives. Among startups, Simpai Network has collaborated with nine leading multinational pharmaceutical companies in areas including market positioning, pharmacoeconomic evaluation, telemedicine, tiered diagnosis and treatment, and smart healthcare, achieving substantial revenue at scale.

We believe that the demand for medical big data, particularly oncology big data, among hospitals, governments, and enterprises remains significant, although current adoption is relatively conservative. Meanwhile, technologies such as artificial intelligence, deep learning, and natural language processing continue to advance in China. Medical big data companies in the country are increasingly focusing on specialized domains, leading to a growing divergence in their capabilities. Driven by supportive policies and favorable capital investment, the market is poised to mature.

Health Catalyst

Health Catalyst is a U.S.-based healthcare data management and analytics services company. Its business includes helping various healthcare organizations analyze and manage clinical, financial, and operational data, thereby improving efficiency, reducing waste of healthcare resources, and promoting the standardization of medical processes.

HealthCatalyst has also developed a suite of novel analytics applications to help diverse teams identify best practice patterns, implement necessary clinical, financial, and operational interventions, filter out specific and personalized solutions, and optimize clinical, financial, and operational outcomes. Previously, HealthCatalyst was solely responsible for data collection and building its own large-scale database; however, it later transitioned to providing structured and standardized data to meet the needs of different users.

This July, it acquired MedCity to expand its leadership in the field of healthcare big data. Health Catalyst added more than 100 clients to its customer base, which previously included employers and health plans across 21 states and regions, as well as 75 health systems comprising over 1,000 hospitals and provider groups with more than 185,000 physicians and extended care facilities, supporting over 75 million patients. The merged company will be dedicated to addressing many of the most pressing challenges facing large healthcare delivery networks as they seek to improve quality and reduce the cost of community patient care.

Flatiron health

Flatiron Health is a healthcare technology company that has developed software connecting community oncologists, academics, hospitals, life sciences researchers, and regulatory agencies on a shared technology platform. Its flagship product, the Flatiron Platform, is a web-based business and clinical information data platform that integrates and structures information systems from diverse patient populations to generate comprehensive patient views. It provides business intelligence analytics for resource utilization, marketing, treatment patterns, network management, and research and clinical trials. The platform enables cancer care providers and life sciences companies to track metrics related to cancer treatment, manage cancer patient adherence in compliance with regulations, and pose customized queries to their data.

Flatiron Health also offers OncoCloud, a suite of software and services, and OncoEMR, which provide cancer care model tools for cancer care providers. In other words, they can intelligently generate cancer care models with nursing recommendations for healthcare professionals to choose from.

OncoBilling, a practice management system integrated with OncoEMR and OncoAnalytics, features surface-level actionable dashboard designs for data insights. OncoTrials is a tool platform for managing oncology clinical trial projects within community oncology trials. Furthermore, the company provides a real-world evidence platform for oncology research in life sciences, as well as an electronic health record (EHR) data platform for academic medical centers and hospitals.

Flatiron Health provides services to hospitals, physicians, and patients in the United States. It has entered into a strategic partnership with the National Cancer Institute (NCI) to explore how real-world evidence derived from de-identified patient data collected at the point of care can be utilized for clinical trial design and prospective research. Previously, it received investments from Google, Roche, and others. In February 2018, it was acquired by Roche for a total consideration of $2.1 billion.

REDOX Modern API Interfaces in the Health Sector

Redox accelerates the development and deployment of healthcare software solutions through a full-service integration platform that enables secure and efficient data exchange. It establishes an industry-standard platform for seamless interoperability between healthcare IT professionals and health systems.

Typically, sharing patient data across systems is a complex, manual, and time-consuming process. Founded in 2014 by former Epic Systems engineers, Redox integrates with all major EHR systems by connecting to existing health IT infrastructure. By eliminating the need to account for system differences and configure integrations, it significantly reduces implementation time. This API platform also enables applications to push and pull patient data to and from EHRs, creating an extended, comprehensive patient health record. As a result, Redox customers experience less disruption, achieve continuity in patient care benefits, and realize a faster return on investment.

To date, more than 120 applications leverage Redox’s integration platform, including solutions for care coordination, telehealth, medication adherence, patient engagement, chronic care, and disease management. Over the past year, the Redox network has experienced significant growth, processing more than 600,000 clinical messages daily.

“The CEO of the company stated that although some policies and standards for clinical data standardization are currently being implemented, I believe our customers no longer need to wait so long by leveraging our system.”

Syapse

Syapse partners with health systems to implement precision medicine programs in hospitals and care facilities, enabling oncologists and nurses to deliver personalized treatment to every patient who needs it.

Syapse has developed a precision medicine software platform that enables academic and community healthcare providers to implement and scale precision medicine programs. The Syapse Precision Medicine Platform captures clinical data, genomic and other molecular data, and biomedical knowledge; integrates the relationships among these data types; and consolidates complex genomic and clinical data to provide decision support for clinicians, thereby facilitating diagnosis, treatment, and patient follow-up.

Syapse Oncology provides treatment recommendations based on molecular profiling data derived from patients’ clinical histories for oncologists. Syapse PGx is an application that enables healthcare institutions to integrate pharmacogenomics knowledge into routine clinical workflows when clinicians order medications through the EMR.

Syapse serves as a solution platform for precision medicine. Traditionally, cancer patients had to undergo various tests, which consumed significant time and delayed treatment opportunities. In contrast, Syapse leverages biomarkers and genetics to tailor solutions for individual patients. The Syapse team has designed a collaborative ecosystem that enables healthcare professionals to make treatment decisions based on comprehensive patient information.

Syapse recently partnered with pharmaceutical company Roche to develop new software and analytics solutions for healthcare providers, enabling them to implement precision medicine at scale.

Oncology

Oncology Analytics provides evidence-based, technology-driven utilization management solutions for health plans, with a focus on oncology.

Used by physicians to support over 2.5 million health plan members in the United States and Puerto Rico, the Oncology e-Prior Authorization platform is updated daily to accurately reflect more than 6,000 oncology treatment regimens across all cancer types and stages, including chemotherapy, radiation therapy, precision medicine, targeted therapy, and supportive care.

The oncology analytics company provides solutions for managing cancer patients. Its oncology management services include prior authorization services; clinical decision support, physician education, and expert peer review services; oncology network assessment and optimization consulting; and performance reporting and analytics services. The company offers MATIS, a clinical decision support software designed for health plans and providers in the United States and Puerto Rico, which enhances evidence-based oncology methodologies for evaluating cancer treatments and benefits management.

GNS health

GNS Health is dedicated to advancing and applying industrial-scale data analytics to empower key healthcare stakeholders in addressing complex challenges related to care, treatment, and costs. The GNS Health team comprises a multidisciplinary group of physicists, actuaries, geneticists, engineers, business professionals, and computer scientists who are passionate about uncovering evidence on how healthcare works and whom it serves. GNS Health has developed machine learning and data analytics technologies designed to improve healthcare treatments and practices through computational modeling.

The company’s spokesperson stated: Pharmaceutical companies believe that GNS technology may help improve the efficiency of drug research and development. This is because the analytical methods from GNS Health can analyze vast amounts of patient-related data and their disease conditions, including genomic sequencing information, health records, bioinformatics, as well as the successes and failures of existing therapies and relevant data from drug testing.

GNS Health’s machine learning- and artificial intelligence-based analytics tools enable pharmaceutical companies to test multiple versions of a specific drug, such as those for multiple sclerosis, more quickly and accurately, thereby identifying the optimal medication for individual patients.

The company’s CEO stated, “We can now simulate the impact of multiple sclerosis drugs No. 3, No. 5, and No. 8 on clinical outcomes for a new patient, and even assess their effect on the total cost of treatment for that patient.”

GNS Health and Roche have launched a collaboration.