Unveiling Startup Unicorns: Traits and Where the Next Wave Will Emerge – 'Super Unicorns' Overview

Unicorn Companies: A term generally used in the investment community to refer to companies with a valuation exceeding $1 billion and a relatively short founding history.

During the growth trajectory of startups, two extreme phenomena often emerge: some companies toil for years only to secure meager funding, while others, akin to capital magnets, are surrounded by investors like stars in the spotlight. These latter companies rapidly close multiple rounds of substantial financing within just a few years, swiftly ascending to become industry unicorns.

What kinds of companies can become unicorns? What characteristics do they possess, and where lie their competitive advantages that set them apart from the rest?

VCBeat has launched the “Super Unicorn” special feature, compiling a list of companies that achieved unicorn status within three years of founding from its knowledge base, and rigorously selecting six enterprises for case study analysis.

According to the VCBeat knowledge base, as of August 2018, a total of 23 companies founded after 2015 had secured over $100 million in total financing. Among these, 13 were valued at unicorn level.

“Super Unicorn” List, Data from VCBeat Knowledge Base

Among the myriad of startups, only one in ten thousand manages to stand out. What types of companies can become industry unicorns, and which sectors are more likely to secure substantial funding? While it is difficult to provide definitive answers, an analysis of these companies’ characteristics reveals commonalities.

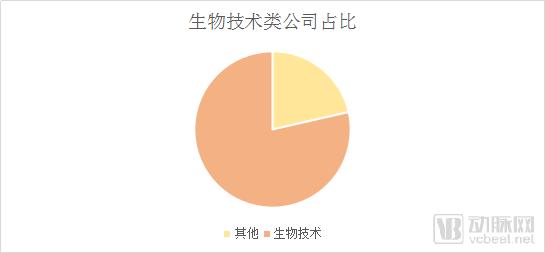

Even without statistical analysis, it is evident that biotechnology companies absolutely “dominate the spotlight” in the form. They occupy nearly all positions on the list, accounting for more than 75% of the total. Without prior notification, one might mistakenly assume at first glance that this is a roster of biotechnology enterprises.

These companies encompass genetic technologies, immunotherapy, and more, covering the entire spectrum from disease diagnosis and treatment to subsequent health management.

Data sourced from the VCBeat Knowledge Base

Also shortlisted were two artificial intelligence companies: iCarbonX and CloudMinds. Of course, to some extent, iCarbonX can be considered a company that is half artificial intelligence and half biotechnology.

Additionally, there is Kernel, the only medical device company on the list. This brain-chip company was founded in January 2016 and secured $100 million in its seed funding round. In this article series, we will analyze Kernel as a case study, so we will not elaborate further here.

It is worth noting that iCarbonX and Kernel both incorporate biotechnology concepts to varying degrees, making it reasonable to classify them as biotechnology companies. Tempus, which recently secured Series E funding, analyzes molecular diagnostics and clinical data using machine learning; however, the company is also directly involved in the molecular diagnostics business.

“With less than RMB 100 million, you’d be too embarrassed to even broach the subject.” So quipped an investor who requested anonymity.

Therefore, it is easier to see that in the 21st century, an era of rapid technological advancement, biotechnology is being enthusiastically embraced by capital.

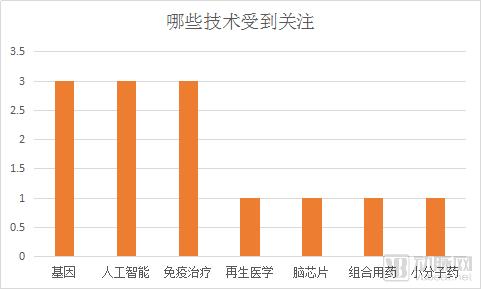

All 13 “super unicorns” are, without exception, technology companies. So, what types of technology are attracting capital interest?

Data sourced from the VCBeat Knowledge Base

Data shows that innovative drug-related technologies hold a dominant position, with 6 out of the 13 unicorns being new drug R&D enterprises. Artificial intelligence, gene technology, and immunotherapy are at the forefront of industry trends.

Since 2016, immunotherapy has emerged as a major trend in oncology research. It began with PD-1/PD-L1 inhibitors, and nearly all pharmaceutical giants—including Bristol-Myers Squibb, Merck & Co., and Roche—have joined this competitive race.

In July 2014, Bristol Myers Squibb’s PD-1 inhibitor Opdivo (nivolumab) was approved in Japan, becoming the first PD-1 inhibitor approved globally. Shortly thereafter, Merck & Co.’s PD-1 drug Keytruda (pembrolizumab) received FDA approval, marking it as the first PD-1 inhibitor approved in the United States. Subsequently, pharmaceutical giants such as Merck KGaA, Pfizer, Roche, and AstraZeneca sequentially entered the market, intensifying the already simmering competition in the PD-1/PD-L1 landscape.

In June 2018, Bristol-Myers Squibb’s drug Opdivo was successfully approved for entry into the Chinese market. One month later, Merck & Co.KeytrudaApproval was also announced. The PD-1/PD-L1 wave has swept from European and American markets to China, with Bristol-Myers Squibb’s Opdivo now officially on sale.

In addition to foreign companies, domestic Chinese pharmaceutical firms are also engaged in development. Drugs from Innovent, Hengrui Medicine, and BeiGene have entered the final stage of regulatory submission. Furthermore, the PD-L1 inhibitor from CStone Pharmaceuticals, which emphasizes combination therapies, has entered Phase II clinical trials and currently holds a leading position in China. The company raised $260 million in its Series B financing round and has reportedly reached unicorn valuation (Click for details)。

“No other target has attracted as much fervent pursuit as PD-1/PD-L1,” Jin Ge, CEO of Rendong Medicine, once told VCBeat in an interview. Globally, hundreds of companies are conducting research centered on PD-1/PD-L1.

In addition to PD-1/PD-L1 immune checkpoint inhibitors, another groundbreaking technology is cellular immunotherapy, represented by CAR-T. Novartis once used this technology to cure Emily, a 12-year-old girl with acute lymphoblastic leukemia. Five years have passed, and her cancer has not recurred. CAR-T is currently the only technology with the potential to truly cure cancer.

Unlike humoral immune therapies such as CAR-T and antibody drugs, this approach equips the body’s innate cellular immune system with a powerful new cytotoxic weapon, offering the potential to completely eradicate tumor cells and cure malignant cancers, thus representing a revolutionary therapeutic modality.

In previous cancer research, the discussion has almost exclusively focused on how to extend the five-year survival rate and transform cancer into a chronic disease. However, complete control or even eradication of tumor cells within the body was unachievable with prior technologies.

Since the successful market launches of products from Novartis and Kite, the global community has been abuzz. “In China, there are hundreds of companies focusing solely on the CD19 target,” a senior industry investor mentioned in an interview.

Since the introduction of standardized guidelines for cell therapy, China’s cell therapy industry has officially entered a new era of promise. CAR-T, as the most highly anticipated modality within this field, has experienced rapid development.

JUNO Therapeutics and WuXi AppTec established a joint venture, JW Therapeutics, while Kite Pharma and Fosun Pharma founded Fosun Kite. Leading international CAR-T companies have formed joint ventures with Chinese enterprises to establish a presence in the Chinese market. Among domestic companies, Legend Biotech and others have entered clinical trials. The CD19+CD22 dual-target CAR-T technology, successfully developed by Hebei Senlang Biotechnology Co., Ltd., successfully treated a leukemia patient at the Second Hospital of Hebei Medical University. This marks the first successful case in China of clinical research using CD19+CD22 dual-target CAR-T technology.

Overall, cancer immunotherapy is moving toward personalized medicine, with combination therapies employed to enhance efficacy. As these treatments rely on engineering the patient’s own T cells to elicit an autoimmune response, their cytotoxic and neurotoxic effects cannot be overlooked. Investigating potential long-term sequelae or other disease risks in patients undergoing cancer immunotherapy represents a key future direction for the field.

The investment community has witnessed a surge in interest for immunotherapy, with companies delivering satisfactory results in both clinical trials and investment returns. Consequently, capital enthusiasm for cancer immunotherapy has not waned over time.

Celularity is a company engaged in embryonic stem cell therapies and is also conducting applied research in tumor immunotherapy. Founded in 2016, the company has raised a total of $290 million in funding to date. We will provide a detailed analysis of Celularity in this case study series.

In addition to capital inflows, the field of oncology immunotherapy has also witnessed significant exit events. For instance, in January 2018, Juno Therapeutics, an oncology immunotherapy company, was acquired by the pharmaceutical giant Celgene in a deal valued at $9 billion. Five years prior, this Seattle-based company had been founded with venture capital support, and it went public two years later, achieving a valuation of several billion dollars at that time.

Fundamentally, the significance of genetic technology lies in its ability to provide a deeper molecular-level understanding of diseases and human biology, thereby enabling more precise diagnosis and treatment. In the era of precision medicine, whether it involves immunotherapy, cell therapy, or targeted drug administration, none can proceed without the support of genetic technologies.

Meanwhile, driven by advances in sequencing technology itself and declining costs, genetic technologies have begun to be commercialized across various fields, such as microbial sequencing.

Before next-generation sequencing (NGS) technology was applied to microbial sequencing, microbiome research was limited to single-strain and qualitative analyses, and the understanding of microbial detection was confined to infectious diseases. NGS has enabled multi-strain detection and quantitative analysis, revealing correlations between many diseases previously thought to be unrelated to human commensal microbes—such as diabetes and depression—and these microbial communities.

What other diseases are associated with microbes, and what are the mechanisms by which microbes influence human health? With the application of next-generation sequencing to microbial sequencing, these questions have been revisited and reexamined. Likewise, as microbiomics has advanced, gene technologies themselves have been promoted and developed.

Around 2015, an artificial intelligence boom swept through the industry, with tech giants such as Google and Apple scrambling to enter the field of artificial intelligence (AI). The two high-profile Go matches between AlphaGo and Lee Sedol, followed by Ke Jie, brought artificial intelligence into the public spotlight.

In the medical field, artificial intelligence is being widely applied to image recognition, data processing and analysis, and drug development. When a domain involves massive amounts of data that need to be processed, refined, and distilled—volumes far exceeding human capacity—the demand for data processing will significantly drive the rapid advancement of artificial intelligence.

Much like the internet, artificial intelligence (AI) will not evolve into a standalone industry in the way that dentistry or pharmaceuticals have; instead, it will serve as a powerful tool that permeates various sectors, accelerating their development. This trajectory is quite similar to that of genetic technologies (although AI’s scope of influence is broader). As industries advance, AI itself will continue to evolve, presenting substantial market prospects.

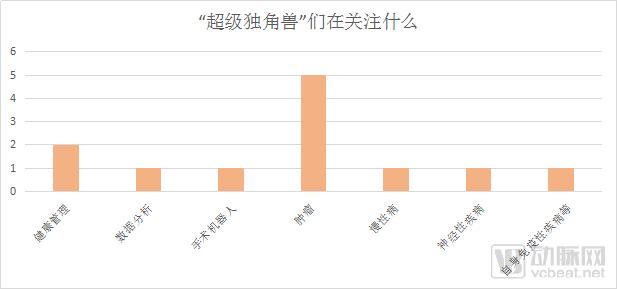

Data sourced from the VCBeat Knowledge Base

Unsurprisingly, oncology-related companies account for the largest proportion. With advances in modern medicine, once-fatal conditions such as diabetes and heart disease have been brought under control and reclassified as chronic diseases. However, people remain largely helpless in the face of malignant diseases like cancer. Undoubtedly, cancer is one of the greatest challenges confronting modern medicine in the 21st century.

Similarly, neurological disorders such as Parkinson’s disease and Alzheimer’s disease have long represented a major pitfall in pharmaceutical R&D. Pharmaceutical giants have invested heavily in this field, yet tangible progress has been scant. However, as population aging intensifies, the societal burden imposed by neurological disorders is becoming increasingly severe.

On one hand, contradictions are intensifying; on the other, the market’s value is becoming increasingly apparent. Major pharmaceutical companies such as Eli Lilly and Novo Nordisk continue to invest heavily in neuroscience and neurological disorders. Meanwhile, research into oncology has never ceased, and this sector remains home to a large number of enterprises.

Subsidiaries spun off from large corporations far surpass most startups in terms of both resources and industry attention.

Helix and GRAIL both originated from the sequencing giant Illumina. The parent company made a high-profile announcement at the 2016 J.P. Morgan Healthcare Conference regarding the establishment of these two companies, joining forces with a consortium of partners to invest in them. Both companies secured $100 million in their initial funding rounds, instantly achieving unicorn status.

$1 Billion Series B Financing, MergerDennis LoofCirina, two large-scale trials; since its inception, every move by GRAIL has attracted global attention.

Its sibling company, Helix, although not making frequent major moves like GRAIL, has introduced the concept of a “Gene App Store,” offering a new possibility for the commercialization of genetic technologies in consumer and health markets. Helix’s Series B financing also reached hundreds of millions of dollars.

Celularity is a spin-off from the pharmaceutical giant Celgene, primarily engaged in research on embryonic stem cell therapies. Additionally, it conducts applied research in tumor immunotherapy and has several products in clinical stages. Founded in 2016, the company has raised a total of $290 million in funding to date.

SpringWorks Therapeutics is an emerging biotechnology startup that spun off from Pfizer in 2017. In its Series A financing round, the company raised $103 million, with participation from prominent industry investors including Bain Capital Life Sciences, Bain Capital Double Impact, OrbiMed, Pfizer, and LifeArc. After acquiring four clinical-stage investigational therapies from Pfizer, SpringWorks Therapeutics is fully committed to advancing the development of these novel drugs, aiming to bring therapeutic hope to patients as soon as possible.

Founded in 2015, Mingma Biotechnology is a subsidiary of the WuXi AppTec Group, primarily providing comprehensive gene sequencing and bioinformatics services to global clients.

In 2015, WuXi AppTec acquired NextCODE Health for $65 million and subsequently merged it with its own genomics center to establish WuXi NextCODE Genomics. From its inception, WuXi NextCODE Genomics has pursued a global strategy. Headquartered in Shanghai, the company operates in Cambridge (UK), Massachusetts (US), and Reykjavik, the capital of Iceland. Additionally, it invested tens of millions of dollars in purchasing HiSeq X Ten sequencers from Illumina, marking its significant entry into the field of genomic medicine.

Mingma Biotech completed its Series B and Series B+ financing rounds in 2017, raising a total of RMB 315 million. Its investors included top-tier venture capital firms such as Sequoia Capital, Temasek, Yunfeng Capital, Amgen Ventures, and 3W Partners.

Likewise, if a company’s founders are already highly successful entrepreneurs or well-respected researchers in the industry, its growth trajectory will inevitably be smoother than that of other companies.

Cullinan Oncology secured $150 million in Series A financing in 2017. Its co-founder and CEO, Patrick Baeuerle, is a pioneer in immuno-oncology who has successfully founded multiple companies. He also led the development of Blincyto, a therapy for relapsed or refractory acute lymphoblastic leukemia, which received FDA approval within three months.

Gossamer Bio is a startup focused on the discovery and development of novel and differentiated therapeutic products. Its two founders, Dr. Faheem Hasnain and Dr. Sheila Gujrathi, are prominent figures in the biopharmaceutical industry. Both previously served at Receptos, a company specializing in immunology and metabolic diseases, where they held the positions of former CEO and former Chief Medical Officer, respectively. Hasnain and Gujrathi jointly led the development of Receptos’ new drug, ozanimod. Receptos was acquired by Celgene in 2015 in a deal valued at $7.2 billion. Ozanimod is currently under development for the treatment of multiple sclerosis, ulcerative colitis, and Crohn’s disease.

Dr. Robert Hariri, Founder and Chief Executive Officer of Celularity, is also one of the most renowned figures in the field of regenerative medicine. Dr. Hariri discovered pluripotent stem cells in the placenta and has made pioneering contributions to human placenta-derived cell therapies and biomaterials. He received the Thomas Alva Edison Award in 2007 and the Fred J. Epstein Lifetime Achievement Award in 2011.

Before founding Celularity, Hariri had already worked at Celgene. He also co-founded Human Longevity, Inc. with genomics pioneer Craig Venter.

This phenomenon is not limited to foreign countries; it is also prevalent in China. iCarbonX completed its Series A financing round of nearly RMB 1 billion shortly after its establishment, with investors including Tencent and Vcanbio. To some extent, the success of this financing round can be attributed to its team.

Wang Jun, Founder and CEO, previously served as CEO of BGI. He participated in the founding of BGI in 1999 during his doctoral studies. During his tenure at BGI, Wang Jun spearheaded multiple rounds of financing and led the company’s acquisition of Complete Genomics (CG), a U.S.-based sequencer manufacturer. Li Yingrui, Co-founder and Chief Scientist of iCarbonX, also hails from BGI. He served as BGI’s Chief Scientist starting in 2014 and was named to the Forbes Asia 30 Under 30 list in the Life Sciences category in 2016. Li Hao, the company’s Co-founder and Chief Information Officer, brings 15 years of experience in the telecommunications carrier industry. He previously served as Head of the Global IPO Business Group at China Netcom Group and as Deputy Director of the Marketing Command Center for the 2008 Beijing Olympic Games.

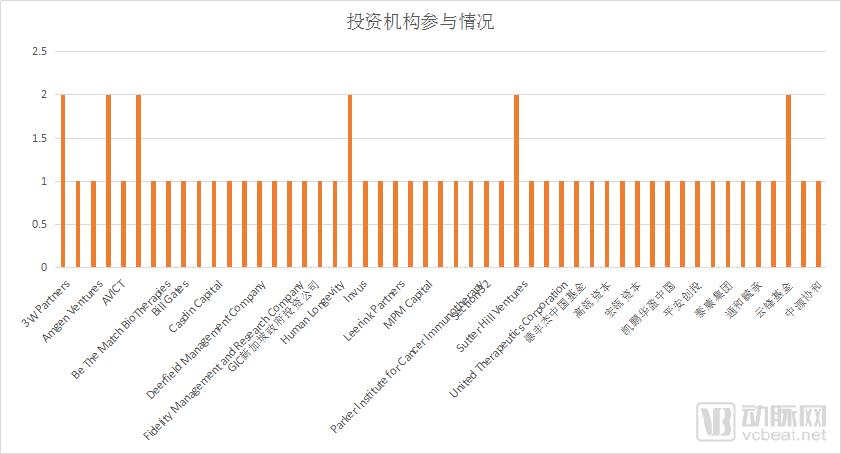

As startups seek investors, investors are also on the lookout for promising startups. Among these rapidly growing unicorns, 51 institutions have emerged as their strong supporters.

In addition to well-known investors such as Sequoia Capital, Temasek, and ARCH Venture Partners, 3W Partners, Bain Capital, Sutter Hill Ventures, and Yunfeng Capital have also demonstrated strong performance. They are the most active institutional investors.

Data sourced from the VCBeat Knowledge Base

In summary, it is evident that the emergence of unicorns is by no means accidental. These companies invariably capitalize on favorable timing, geographic advantages, and strong human resources; they stand at the forefront of their era, seizing critical opportunities arising from market evolution. Assembling the strongest teams, doing the right things at the right time, and attracting top-tier investors may not constitute the complete formula, but these elements are undoubtedly part of the secret to the success of “super unicorns.” For entrepreneurs currently building their ventures, how many of these traits do you possess?

Easter Egg:

In addition to “super unicorns,” the author has also compiled a list of companies that have raised approximately $100 million within three years, based on the VCBeat knowledge base. Although these figures may not be as striking as those of “super unicorns,” these companies have similarly gained industry and capital recognition within just three years, making them highly likely to become the next unicorn enterprises!

Potential Unicorn – Data sourced from the VCBeat Knowledge Base