Jingdata Research Institute | 2018 Industry and Investment Analysis Report on CAR-T Therapy

Author: Liu Jiaying, Analyst at Jingzhun Research Institute

Preface

n Research Background

Immunotherapy is one of the most promising avenues in current oncology treatment. As the application scope of immune checkpoint inhibitors such as Opdivo continues to expand, and new advancements continually emerge in CAR-T therapy research, tumor immunotherapy is gaining increasing momentum. Following targeted cancer therapies, immunotherapy is ushering in another revolution in the field of anti-cancer treatment.

In this revolution, CAR-T therapy plays a particularly unique role. As a “living drug” distinct from conventional pharmaceuticals, it has not only demonstrated breakthrough efficacy in patients with relapsed and refractory tumors, but its manufacturing system and clinical application scenarios also differ significantly from those of ordinary drugs. Given the rapid pace of advancements in biotechnology, CAR-T therapy is expected to bring further surprises to the market.

n Scope of Study

This report begins with the technical foundations of CAR-T therapy to analyze the current status and prospects of its industry development. It places particular emphasis on analyzing the structure and characteristics of the industrial chain extending from CAR-T therapy. Given that CAR-T technology has only recently emerged and its industrialization is in its early stages, the report will also focus on the current R&D landscape and the core competitive factors for companies at different future development stages. Furthermore, the financing and investment characteristics and opportunities within the CAR-T therapy sector fall within the scope of this study.

n Research Direction

The report will specifically address the following questions:

(1) At what stage of development is the CAR-T therapy industry currently? What factors are influencing its development?

(2) What is the current competitive landscape of the CAR-T therapy market? What development trends will emerge in the future?

(3) With nearly 100 CAR-T companies vying for market share, what are the key competitive factors among these enterprises?

(4) As multinational giants and publicly listed companies enter the fray, what investment opportunities remain in the CAR-T therapy sector?

1.CAR-TTherapy Overview

1.1 What is CAR-T Therapy: Using Immune T Cells as Raw Materials to Target and Kill Tumor Cells

n Definition:CAR-T TherapyChimeric Antigen Receptor T-Cell ImmunotherapyThis therapy utilizes gene recombination technology to generate T cells expressing chimeric antigen receptors (CARs). Following purification, ex vivo expansion, and activation, the CAR-T cells are infused back into the patient, enabling them to specifically recognize and bind to antigens on the surface of tumor cells, thereby exerting a tumor-killing effect.

n Mechanism of Action:As a typical form of tumor immunocellular therapy, the mechanism of action of CAR-T therapy is closely related to the human immune system. Recent studies have found that immune cells can work synergistically to inhibit tumor development during tumorigenesis; however, some tumor cells can evade recognition and clearance by the human immune system through various mechanisms. The core of CAR-T therapy lies in engineering human T cells to enhance the immune system’s ability to recognize and kill tumor cells.

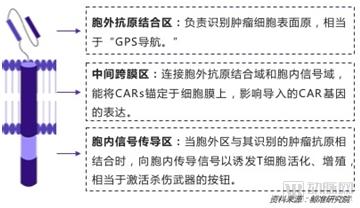

n CARs Structure: The CAR structure is the core component of CAR-T cells, generally consisting of three parts: an extracellular antigen-binding domain, a transmembrane domain, and an intracellular signaling domain.

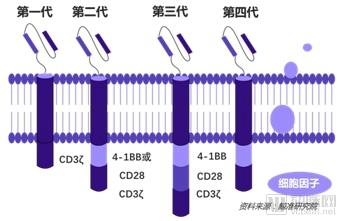

1.2 Evolution of CAR-T Therapy Technology: Four Generations Have Been Developed to Date, with Second-Generation CAR-T Therapy as the Current Mainstream

CAR-T therapy was first proposed by Gross et al. in the late 1980s. The emergence of earlier immunotherapies, such as LAK, TIL, and CIK cells, laid the foundation for CAR-T research. To date, other immunotherapeutic approaches, including DC-CIK and CTL therapies, remain active areas of investigation. However, given its technological maturity and clinical potential, CAR-T therapy continues to be the primary focus of both academic and industrial communities.

Four generations of CAR-T therapy have been developed to date. The first-generation CARs contain only an antigen recognition signal and exhibit limited proliferative capacity in vivo. Second- and third-generation CAR-T cells incorporate one and two co-stimulatory molecules, respectively, within the signal transduction domain to enhance T-cell proliferation, cytotoxicity, and survival. Unlike the previous three generations, fourth-generation CAR-T constructs introduce pro-inflammatory cytokines and co-stimulatory ligands, primarily aiming to overcome the immunosuppressive tumor microenvironment. Currently, most companies’ products are based on second-generation CAR-T technology; however, the boundaries between generations are becoming increasingly blurred as research directions evolve.

1.3 CAR-T Therapy Treatment Process: Key Steps—Cell Isolation, Ex Vivo Expansion, Genetic Modification, and Quality Control

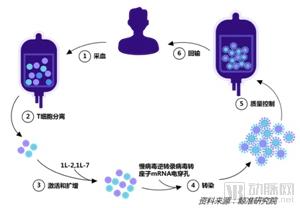

n Treatment Process:Similar to most tumor immunocellular therapies, the CAR-T treatment process is broadly divided into six steps: collection of patient peripheral blood, isolation and expansion of T cells, genetic modification of T cells to enable stable expression of chimeric antigen receptors (CARs), quality control testing of the engineered T cells, infusion of qualified CAR-T cells back into the patient to achieve targeted and sustained elimination of tumor cells, and monitoring for adverse reactions.

n Key Steps:The entire CAR-T cell manufacturing process takes approximately 15 days and requires fully closed-system operations. Among these steps, T cell isolation and expansion, as well as T cell engineering, are the most critical. During T cell culture, cytokines such as IL-2 (Interleukin-2) must be used, with careful attention paid to the ratio of CD4+ to CD8+ T cells. Currently, the most common method for engineering T cells involves using lentiviral or retroviral vectors to integrate the CAR gene into the T cell genome.

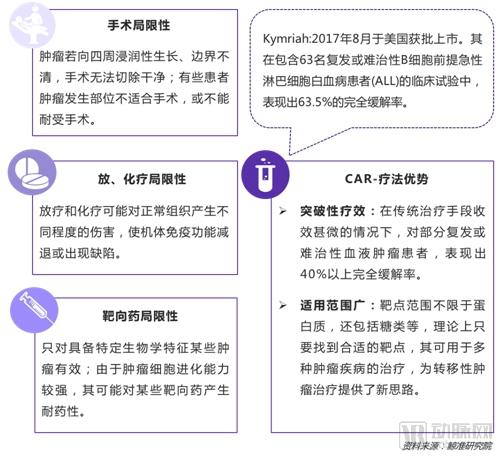

1.4 Prospects for CAR-T Therapy: A Breakthrough for Patients with Relapsed/Refractory Tumors

Compared with traditional cancer treatments such as surgery, chemotherapy, and radiotherapy, CAR-T therapy has become a hot spot in research and development primarily because it has demonstrated breakthrough efficacy in patients who are refractory to conventional therapies. Currently, two CAR-T products, Kymriah and Yescata, have been approved for marketing worldwide, and their indications are expected to continue expanding.

1.5 Limitations of CAR-T Therapy

1.5.1 Toxic side effects include cytokine storm, off-target effects, etc., and clinical risks have not yet been fully revealed

Like many drugs and treatment modalities, CAR-T therapy is associated with side effects, such as cytokine release syndrome manifested by fever and myalgia; indeed, some patients have died from these adverse events in clinical trials. Furthermore, as the industrialization of this therapy only began to gain momentum around 2015, it has not yet been widely adopted in clinical practice. Consequently, the clinical risks of this therapy have not been fully elucidated, and its toxic side effects warrant further observation.

n Cytokine Release Syndrome:Following the infusion of a large quantity of CAR-T cells into patients, T cells are activated and undergo rapid proliferation, leading to excessive release of cytokines such as interferons and interleukins. These cytokines mediate various immune responses, resulting in inflammatory reactions characterized by fever, myalgia, hypotension, dyspnea, and coagulation disorders.

In September 2017, the French pharmaceutical company Cellectis announced that a 78-year-old male patient with blastic plasmacytoid dendritic cell neoplasm died approximately 10 days after receiving CAR-T therapy in a clinical trial. The patient had experienced grade 5 cytokine release syndrome and grade 4 capillary leak syndrome.

n Off-target effects:Although CAR-T therapy targets are mostly expressed at low levels in normal tissues, it remains difficult to completely avoid cross-reactive immune cytotoxicity. Once CAR-T cells bind to the same target antigens expressed on normal tissues, they will attack these normal tissues, thereby causing tissue damage or immunodeficiency.

n Allergic Reactions and Neurotoxicity:There have been reports of a minority of patients with acute lymphoblastic leukemia experiencing neurotoxic symptoms such as language impairment, akinetic mutism, or seizures during CD19-targeted CAR-T cell therapy.

n Deficiencies of Viral Vectors:Currently, viral vectors are the mainstream transfection method for CAR-T cell therapy due to their high transfection efficiency; however, they have drawbacks such as insertional mutagenesis.

1.5.2 Difficulty in Overcoming Immunosuppression in the Solid Tumor Microenvironment; Potential Relapse of Hematologic Malignancies

Although CAR-T therapy has demonstrated therapeutic efficacy in numerous studies that is difficult to achieve with conventional cancer treatments, its clinical effectiveness remains subject to significant limitations.

n High Relapse Rate of Hematologic Malignancies:Based on short-term treatment outcomes, CAR-T therapy can nearly completely eradicate tumor cells in hematologic malignancies; however, with extended observation periods, it becomes evident that many patients experience tumor relapse several months or longer after receiving CAR-T therapy.

n In the clinical trial results for CTL019 involving 59 pediatric and adolescent patients with relapsed or refractory acute lymphoblastic leukemia (ALL) published by Novartis, only 18 patients maintained complete remission at 12 months. This indicates that the majority of patients experience relapse after receiving CAR-T therapy.

n Solid Tumor Therapies Await Breakthroughs:Compared with hematologic malignancies, the challenges encountered by CAR-T therapy in solid tumors are more intractable. On one hand, unlike hematologic systems that are distributed throughout the body, solid tumors occur at localized sites. The ability of CAR-T cells to reach the lesion site of solid tumors and infiltrate into the tumor interior is a prerequisite for their anti-solid tumor activity.

n On the other hand, even if CAR-T cells can infiltrate into solid tumors, they still face suppression from the internal immune microenvironment. For instance, high levels of immunosuppressive molecules such as IDO and PD-1 are produced within solid tumors, which prevent T cells from functioning properly. Furthermore, the acidic, hypoxic, and nutrient-deprived conditions within the tumor microenvironment are also unfavorable for the efficacy of CAR-T cells.

1.6 R&D Directions for CAR-T Therapy: Enhancing Efficacy and Controllability, Reducing CAR-T Cell Toxicity

In light of the limitations exposed by CAR-T therapy, current research and development efforts are primarily focused on three areas. The first is enhancing the efficacy of CAR-T therapy, such as by increasing the activation and proliferative capacity of CAR-T cells and prolonging their survival time in vivo. More effective approaches are particularly needed for the treatment of solid tumors. The second area involves reducing the toxicity of CAR-T cells to improve the safety profile of CAR-T therapy. To this end, many studies are exploring strategies such as incorporating safety switches or developing multi-targeted CARs. Furthermore, given the highly personalized nature of current CAR-T therapies and the associated high costs of quality control, the industry has placed significant hope in universal CAR-T (UCAR-T) cells.

n Dual CAR-T:Common dual CAR-T designs simultaneously target CD19 and CD22 molecules, primarily addressing the issue of hematologic tumor relapse after remission in patients treated with CD19-targeted CAR-T products. Studies have shown that during CAR-T therapy, some cancer cells originally expressing CD19 may switch to expressing CD22 protein. Therefore, targeting both CD19 and CD22 is theoretically expected to enhance the efficacy of CAR-T therapy.

n CAR-T Combined with PD-1: Given that cytokine-mediated PD-1/L1 immunosuppressive signaling pathways are present in many cancer types, including lung and liver cancers, inhibitors targeting immune checkpoints such as PD-1/L1 are also regarded as stars in the field of tumor immunotherapy. The exploration of combining CAR-T therapy with these agents is primarily aimed at overcoming the immunosuppressive tumor microenvironment in solid tumors; however, this combination may also lead to additive toxicity.

n CAR-NK:Due to their unique mechanisms for recognizing tumor cells and broad antitumor cytotoxicity, NK cells are considered to hold potential comparable to CAR-T cells after CAR modification. Compared with CAR-T cells, some studies have found that CAR-NK cells exhibit a better safety profile and do not require personalized customization like autologous CAR-T cells, thereby enabling scalable manufacturing.

n UCAR-T:This therapy is an allogeneic CAR-T therapy, in which T cells are derived from healthy donors. Gene-editing technologies such as TALENs and CRISPR are then employed to knock out genes that could trigger alloimmune rejection. Theoretically, its advantages lie in the potential for scalable, standardized manufacturing, thereby reducing production costs.

2.CAR-TIndustry Development Overview

2.1 Industry Development Scale: The potential market size for hematologic malignancies exceeds RMB 10 billion, with solid tumors offering even broader prospects

n Large Market Share of Antineoplastic Drugs:Given that cancer is one of the diseases with the highest incidence and mortality rates worldwide, anti-tumor drugs have long ranked among the top in terms of market share across various pharmaceutical categories, both globally and in the Chinese market. Data from IMS and the Southern Medical Economic Research Institute of the China Food and Drug Administration (CFDA) show that from 2012 to 2016, the compound annual growth rate (CAGR) of China’s anti-tumor drug market approached 14%. With more than ten anticancer drugs included in the national medical insurance reimbursement list in 2018, this market is expected to see further growth.

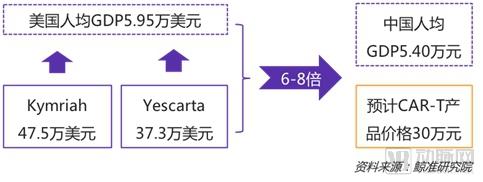

n CAR-T’s Potential Market Size in Hematologic Malignancies Approaches RMB 10 Billion:As a highly promising emerging therapeutic approach, CAR-T therapy is currently limited to third- and fourth-line treatment for hematologic malignancies in the short term. However, considering factors such as technological advancements and the size of the patient population, its market prospects are extremely broad. In China, there are over 4 million new cancer cases annually, including nearly 200,000 cases of common hematologic malignancies such as leukemia. Based on the pricing of CAR-T products in the United States and China’s GDP level, the domestic price of CAR-T therapy is estimated at approximately RMB 300,000. With a conservative market penetration rate of 20%, the potential market size for CAR-T therapy in hematologic malignancies in China approaches RMB 12 billion.The solid tumor market, accounting for over 90% of patients, holds greater potential.

2.2 Industry Development History: In the Technology Introduction Phase, Domestic CAR-T Industrialization Has Just Begun

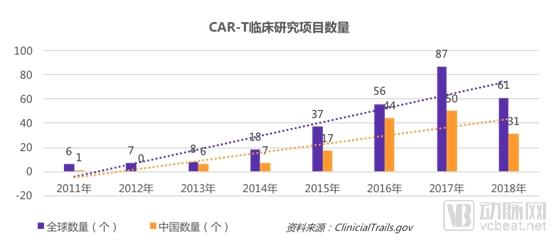

CAR-T technology has evolved over several decades. However, based on the number of clinical trials registered on the U.S. ClinicalTrials.gov website, CAR-T therapy truly entered a period of rapid development after 2015. From 2015 to 2017, the number of CAR-T clinical trials conducted globally and in China increased significantly. The industrialization of CAR-T therapy only began to accelerate after the FDA approved two CAR-T products for market launch in 2017.

To date, VBInsight has cataloged more than 70 companies in China that prioritize CAR-T therapy as their core R&D focus, with nearly half of these companies established after 2015. The vast majority of these companies have not yet initiated registered clinical trials for their CAR-T products. Based on the typical developmental stage classification characteristics of technology-driven industries—including the seed stage, introduction stage, growth stage, and maturity stage—the CAR-T therapy industry is currently in the technology introduction stage.

2.3 Industry Policy Environment: Aligned with drug administration regulations, but with more flexible review rules compared to traditional new drugs

As “living drugs” derived from human cells, CAR-T therapy has undergone a regulatory evolution from nonexistence to establishment, and from ambiguity to clarity, accompanied by ongoing controversies. It was not until December 2017, when the China Food and Drug Administration (CFDA) issued the Technical Guidelines for Research and Evaluation of Cell Therapy Products (Trial), that the regulatory framework for CAR-T therapy gradually became clear, classifying it as a pharmaceutical product rather than merely an emerging therapeutic technology.

Under the standard drug approval process, a product must undergo a series of procedures, including filing for clinical trials, before it can be granted market authorization. In contrast, the current regulatory and approval frameworks for CAR-T therapies offer considerable flexibility. On one hand, companies can collaborate with hospitals to initiate non-registration early-stage clinical studies before formally launching clinical trials, enabling them to assess R&D risks at an early stage and avoid blind progression into full-scale trials. On the other hand, the design of clinical trial phases for CAR-T therapies is more flexible, and the required sample sizes are relatively small, currently typically around 100 cases.

2.4 Industry Chain Composition and Characteristics

2.4.1 The industrial chain is divided into upstream, midstream, and downstream segments, with R&D and manufacturing as key components

In the CAR-T therapy industry chain, the upstream sector comprises manufacturers of equipment such as flow cytometers, reagents used for T-cell sorting and transfection, and raw and auxiliary materials including cytokines. The midstream and downstream sectors are dedicated to CAR-T therapy research and development (R&D) and product manufacturing, respectively. Notably, many R&D enterprises also choose to produce lentiviral vectors in-house for the generation of CAR-T cells.

2.4.2 Upstream, Midstream, and Downstream

(1) Key equipment, reagents, and raw materials are mostly sourced from multinational corporations, resulting in higher prices.

CAR-T cell preparation involves steps such as T-cell isolation and activation, requiring various equipment, reagents, and consumables, including cell separators. Suppliers of these critical devices and reagents are predominantly multinational corporations, such as GE, Miltenyi Biotec (Germany), and Thermo Fisher Scientific.

Domestic manufacturers of equipment and reagents also exist, with some prices being only one-tenth that of imported products; however, their product quality lags behind. Consequently, most domestic R&D enterprises opt to procure imported products, which account for nearly half of the production costs in CAR-T cell manufacturing.

If CAR-T therapy is viewed as a product, viral vectors can be regarded as key raw materials, whose manufacturing process and quality control require substantial capital investment. Currently, only a few companies worldwide, such as Oxford BioMedica, possess core technologies for viral vector production and stable, large-scale manufacturing processes, which results in relatively high prices. With the advancement of gene therapies like CAR-T, there may be a situation where demand for viral vectors outstrips supply.

(2)Low degree of industrial specialization, with limited scope for third-party outsourcing service providers

Domestic third-party pharmaceutical outsourcing service providers, such as CMOs, have grown significantly due to the development of the biopharmaceutical industry in recent years. However, in the field of CAR-T therapy, the scope for participation by third-party outsourcing service providers remains currently limited. Generally, third-party outsourcing service providers fall into three categories: Contract Research Organizations (CROs), Contract Manufacturing Organizations (CMOs), and Contract Sales Organizations (CSOs), which correspond to drug research and development, production, and sales services, respectively. In recent years, the CDMO model, which covers both drug R&D and production services, has also gradually emerged.

Currently, domestic CROs involved in the CAR-T therapy field provide services such as safety evaluation and clinical data management. The role of CMOs/CDMOs has not yet been fully realized. On one hand, as CAR-T therapy is an emerging modality, China lacks CMOs/CDMOs with the corresponding service capabilities, including plasmid production, viral vector manufacturing, and CAR-T cell preparation. On the other hand, many R&D companies are concerned about the leakage of core technologies and manufacturing processes.

This differs from the degree of specialization in the U.S. CAR-T industry. Currently, the U.S. CAR-T sector has initially formed a highly complementary division of labor, where viral vectors, clinical trial materials, and large-scale product manufacturing can be outsourced to corresponding CMO/CDMO companies. This allows R&D enterprises to focus more on technology and product development, thereby improving resource utilization efficiency.

2.4.3 Sales Terminals: Higher Application Threshold than Conventional Drugs; Hospitals and Physicians Must Possess Relevant Treatment Experience

As an emerging cell therapy, CAR-T treatment, like conventional anti-tumor drugs, must ultimately be administered to patients through hospitals and physicians. However, CAR-T therapy imposes higher requirements on healthcare institutions and medical professionals. Consequently, its future application scenarios and delivery models will differ from those of traditional pharmaceuticals.

The CAR-T therapy process involves steps such as cell extraction, cell infusion, and monitoring for adverse reactions. If patients receive treatment at a hospital while the enterprise transports CAR-T cells to the facility, specific requirements regarding the hospital environment and physician competency must be met to ensure the smooth conduct of therapy and timely management of potential adverse reactions in patients.

Following the domestic launch of CAR-T therapy in China, various implementation models may emerge. For instance, pharmaceutical companies may collaborate with hospitals to establish cell therapy centers within hospital facilities; these hospitals are likely to be the same institutions that partnered with the companies during clinical trials. Alternatively, companies may independently build their own cell therapy centers, pursuing both clinical research and clinical application simultaneously, though this approach still requires support from hospitals with relevant therapeutic expertise.

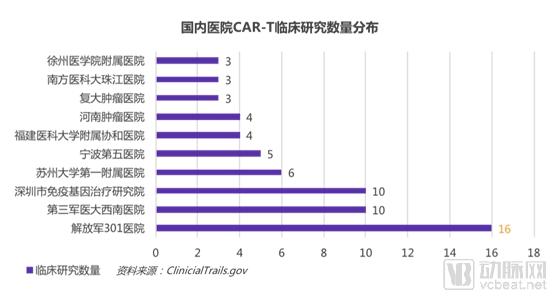

Based on the current number of CAR-T clinical trials conducted by hospitals in China, the PLA General Hospital (301 Hospital) has launched the highest number of research projects, followed by the Southwest Hospital of the Third Military Medical University and the Shenzhen Institute of Immune Gene Therapy, among others. It is foreseeable that these institutions will also become important channels for the future promotion of CAR-T therapy.

3.CAR-TTherapy R&D and Market Competition Landscape

3.1 Key Players in the CAR Therapy Market: Pharmaceutical Giants and Innovative Enterprises Compete Side by Side, with Most Entrepreneurs Coming from Scientific Research Backgrounds

In terms of company scale, the major players in the domestic and overseas CAR-T therapy markets can generally be categorized into two groups: one comprises established entities with extensive experience in chemical pharmaceuticals or biotechnology, characterized by substantial corporate size and scale, such as the multinational pharmaceutical giant Novartis and Hengrui Medicine, China’s most valuable listed pharmaceutical company; the other consists of relatively smaller, innovative biotechnology firms focused on technological advancement and drug R&D, such as the U.S.-based Bellicum, founded in 2004, and China-based CJ Bioscience, established in 2014.

Examining the strategic layouts of domestically listed pharmaceutical companies reveals three distinct categories. The first, represented by Fosun Pharma and WuXi AppTec, involves establishing joint ventures with leading international CAR-T players such as Kite and Juno Therapeutics to introduce relatively mature products and technological platforms, thereby enhancing R&D efficiency and accelerating time-to-market. The second category, exemplified by Zuoli Pharmaceutical and Anke Biotechnology, focuses on making equity investments in innovative biotech firms to expand their industrial footprint and compensate for inherent limitations in internal innovation capabilities. The third category, including Galaxy Bio, establishes subsidiaries dedicated exclusively to CAR-T research and development. During both clinical trial phases and post-launch commercialization, these listed companies can provide innovative biotech firms with financial backing and distribution channel support.

3.2 Landscape of CAR-T Therapy Development

3.2.1 Overview: Focused on hematologic malignancies, with the highest number of studies targeting CD19

As of August 23, 2018, a total of 158 CAR-T clinical trials had been registered on ClinicalTrials.gov in China, involving more than 40 targets. Over half of these trials focused on hematologic malignancies, with CD19-targeted studies being the most numerous. This trend is broadly similar to that observed in the United States.

3.2.2 Overseas Companies: Novartis and Kite Lead with Product Launches, While Multinational Giants Pursue External Collaborations and M&A

Two CAR-T products have been approved for marketing globally: Novartis’ Kymriah and Kite’s Yescarta. As a result, Novartis and Kite are positioned in the first tier of global CAR-T therapy research and development. Other companies that initiated CAR-T R&D earlier, such as Juno, Cellectis, and Bluebird, have also attracted attention due to their technological prowess, becoming targets for mergers, acquisitions, and collaborations by multinational pharmaceutical giants. In recent years, with the continuous rise in new drug R&D costs, many pharmaceutical giants have begun to pursue strategic transformations, focusing on their core competencies while engaging in joint R&D partnerships or acquiring high-quality assets from other enterprises.

Ø In August 2018, Gilead announced its acquisition of Kite for $11.9 billion; in March 2016, Kite entered into a collaboration agreement with Roche to jointly develop combination therapies involving CAR-T and PD-1 inhibitors.

Ø In January 2018, Celgene announced the acquisition of Juno Therapeutics for approximately $9 billion. In March 2018, Celgene entered into a collaboration agreement with Bluebird Bio to jointly develop bb2121, building on their partnership that had begun in 2013.

Ø In April 2018, Pfizer announced the acquisition of a 25% stake in Allogene; in June 2014, Pfizer and Cellectis announced a collaboration.

3.2.3 Domestic Enterprises: Most are hospital-initiated clinical studies, with only a few products having their IND applications approved

The vast majority of domestic CAR-T products are still in the stage of non-registration clinical studies initiated by researchers such as hospital physicians, and have not yet entered drug clinical trials in the strict sense. It was not until the end of 2017, when the China Food and Drug Administration (CFDA) issued the "Technical Guidelines for Research and Evaluation of Cell Therapy Products," that progress was made. As of August 23, the CFDA had received a total of 26 Investigational New Drug (IND) applications for CAR-T therapies. Among these, the IND applications from Nanjing Legend, Hengrundaisheng, and Mingju Bio (an affiliate of WuXi Juno) have been approved, entering the formal phase of drug clinical trials. The status of Ucartid’s four IND applications was updated to "Approval Letter Issued" in April and May; however, clinical trials have been significantly delayed in subsequent practical implementation. The IND applications of other companies, including Fosun Kite, Caris Biotech, Precision Biologics, Stargene, CytoMed Therapeutics, Huadao Bio, Inno Immune, Progenicy, Yimiao Shenzhou, and Baiji Gene, are still under review.

Among the total of 26 IND applications for CAR-T therapies, more than 80% target CD19, while the remaining four IND applications target BCMA; one of Legend Biotech’s IND applications targets GPC3. This trend is primarily driven by the fact that two CD19-targeted CAR-T products have already been launched globally. Late-entering companies can reduce the risk of drug development failure and preliminarily validate the stability of their CAR-T technology platforms and manufacturing processes by starting with this target. However, the solid tumor studies currently being conducted by many companies represent the true focus of future market competition.

3.3 Competitive Factors in the CAR-T Therapy Market

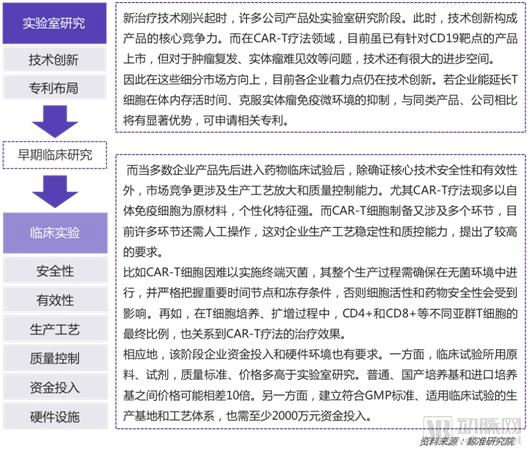

3.3.1 Productization Phase: From Laboratory to Product, Technology, Manufacturing Process, and Quality Control Are All Indispensable

However, R&D progress is not the sole determinant of the CAR-T therapy market. Although some domestic companies have been the first to obtain approval for clinical trials, CAR-T therapy, as an emerging treatment submitted for regulatory approval as a drug, must undergo a series of stages—from laboratory research and product development to commercialization—before it can ultimately achieve large-scale clinical application. At each stage of market advancement, companies lacking the necessary competitive factors will gradually be eliminated from the market.

3.3.2 Commercialization Stage: Production Efficiency, Cost Control, and Channel Promotion Become Prominent

As products obtain marketing approval and enter the commercialization phase, in addition to technological innovation, manufacturing processes, and quality control—which continue to be key competitive factors in the CAR-T therapy market—the importance of a company’s scalable production capacity, cost-control capabilities, and channel promotion models has become increasingly prominent.

4. Case Study of CAR-T Therapy Companies

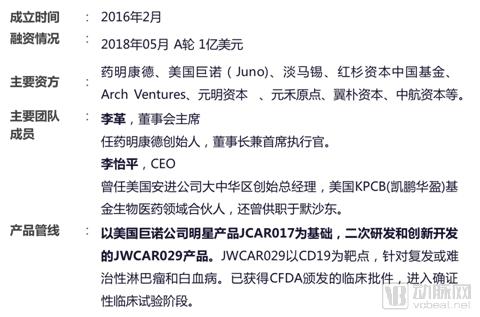

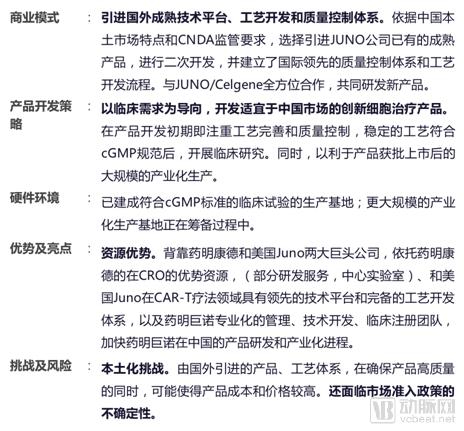

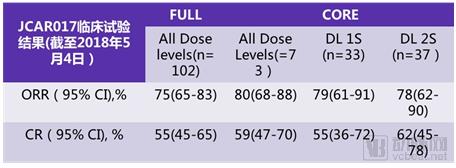

4.1 JW Therapeutics: Backed by Two Industry Giants, Introducing Overseas Products and Process Systems

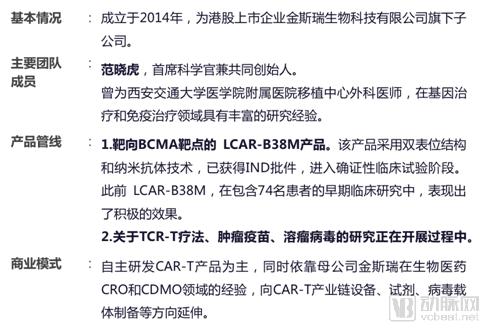

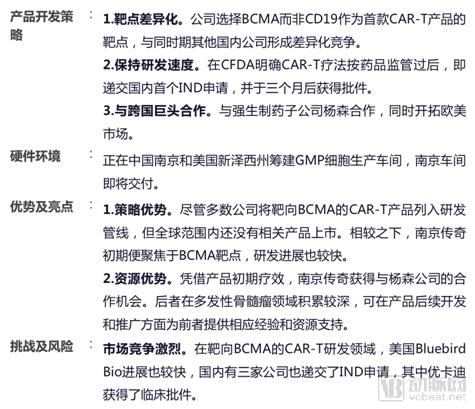

4.2 Nanjing Legend: Targeting BCMA, with rapid R&D progress

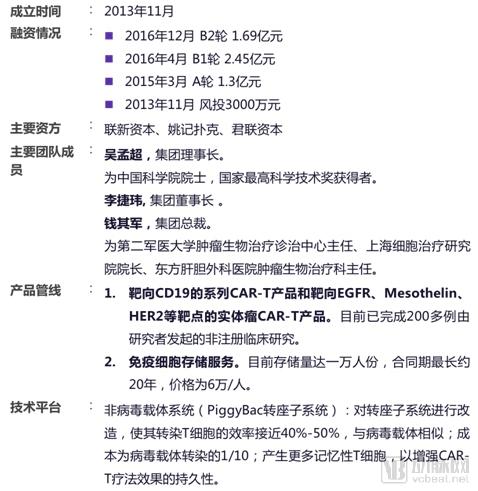

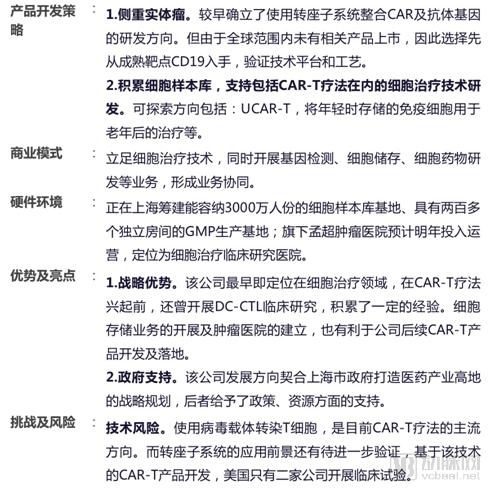

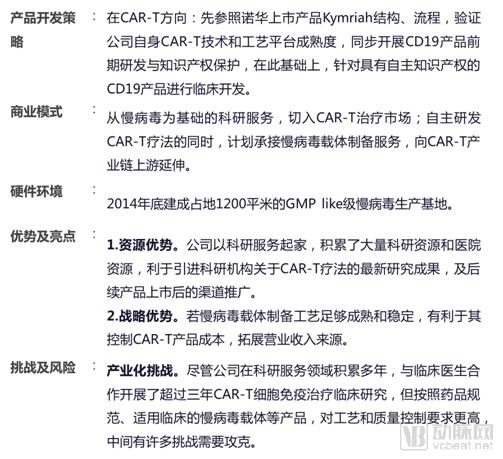

4.3 Shanghai Cell Therapy Group: Leveraging Transposon Systems to Tackle Solid Tumors

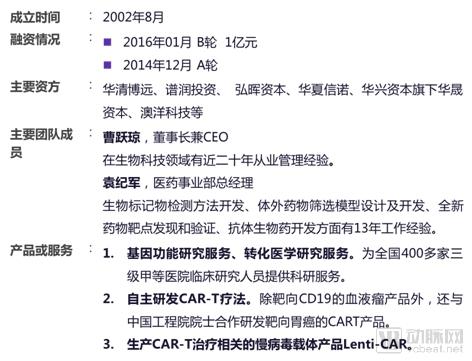

4.4 GeneChem: Originating from Research Services, with Abundant Hospital Resources

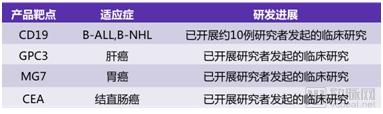

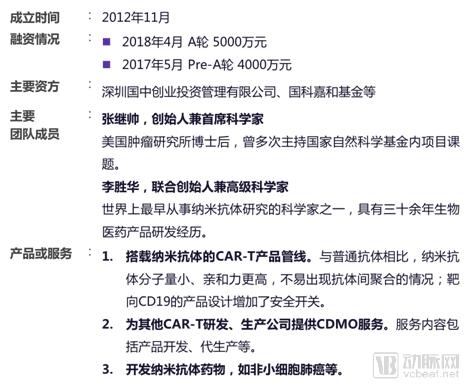

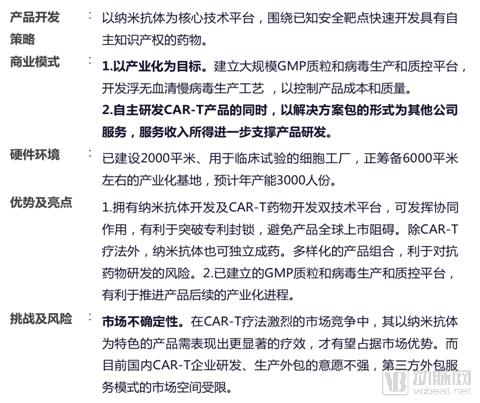

4.5 Puruijin: Leveraging a Nanobody Technology Platform with a Rich Product Pipeline

5. Analysis of Investment and Financing Status in CAR-T Therapy

5.1 Overview:CAR-T Therapy Is at the Investment Hotspot, with a Shorter Payback Period Than Conventional Biologic New Drugs

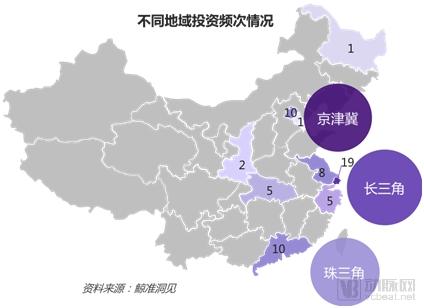

From the perspective of overall investment and financing trends, CAR-T therapy has been a hot investment sector over the past two years. In just the eight months from 2018 to date, there have been 12 recorded investment deals in this field, with half of them being large transactions exceeding RMB 100 million. The Yangtze River Delta region, centered on Shanghai, has seen the most active investment in the CAR-T sector, consistent with the regional distribution trend of overall biomedical industry investments in China over the past two years.

In addition to the high investment, high risk, and high return characteristics common to investments in the biopharmaceutical sector, CAR-T therapy features a shorter R&D cycle compared to conventional large-molecule biologics, implying a shortened payback period for investors. Typically, the development of new drugs from preclinical studies to market approval takes at least 10 years, with average costs exceeding $1 billion. However, the launch process of Kymriah, the world’s first CAR-T product under Novartis, took only five years. With the accumulation of regulatory experience by government authorities and technological advancements, the time to market for CAR-T products is expected to shorten further.

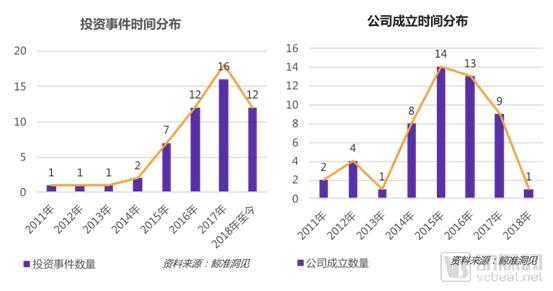

5.2 Characteristics of the Temporal Distribution of Investment and Financing:The Peak of CAR-T Therapy Investment Occurred Around 2017, with Momentum Expected to Continue

From a temporal distribution perspective, CAR-T therapy has gradually attracted the attention of investment institutions since 2014. This trend is largely attributable to the fact that multinational pharmaceutical giant Novartis and biopharmaceutical company Kite, among others, announced their latest research advancements in CAR-T therapy for hematologic malignancies at the 56th Annual Meeting of the American Society of Hematology (ASH) held that year, preliminarily demonstrating the therapeutic potential of this approach. Over the subsequent two to three years, both the number of investment deals and newly established companies continued to rise. Although the number of newly founded CAR-T companies declined in 2018, 12 investment transactions still occurred, indicating that investor enthusiasm in this field remains strong. As extensive scientific research on CAR-T technology continues—such as in solid tumors and universal CAR-T (UCAR-T)—this sector is expected to witness a new wave of investment activity.

5.3 Geographic Distribution Characteristics of Investment and Financing

From a geographical perspective, as an emerging biotechnology, CAR-T has seen most of its investment activities concentrated in the eastern coastal regions. A small number of investments have also occurred in central provinces such as Shaanxi and Hubei (with Wuhan as its capital). Within the eastern coastal area, the Yangtze River Delta region, centered on Shanghai, hosts the largest cluster of CAR-T companies, making it the most active region for CAR-T-related investments. This is followed by the Beijing-Tianjin-Hebei region, centered on Beijing, and the Pearl River Delta region, centered on Guangzhou and Shenzhen.

It is worth noting that most regions with relatively active CAR-T investment have established specialized biopharmaceutical industrial bases. The local governments regard the biopharmaceutical industry as a strategic emerging industry prioritized for development, offering enterprises numerous policy incentives and financial subsidies. In particular, in the Yangtze River Delta region, while Shanghai has already formed a relatively comprehensive biopharmaceutical innovation system by leveraging its early advantage of hosting multinational pharmaceutical companies, surrounding cities such as Suzhou, Nanjing, and Hangzhou have also attracted a batch of enterprises and talent due to factors like policy support and rapid economic growth. With the development of the CAR-T industry and the existing cluster effect of the biopharmaceutical sector, it is expected that a full-industry-chain ecosystem centered on CAR-T therapy will take shape in the Yangtze River Delta. This region will also attract greater capital inflows.

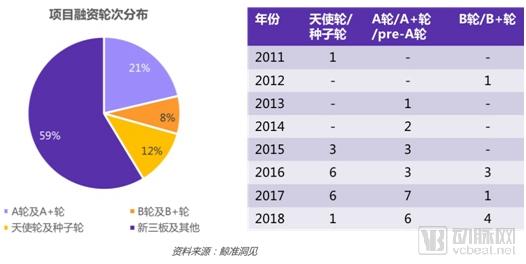

5.4 Distribution Characteristics of Investment and Financing Rounds: Projects are predominantly in early-stage financing, with participation from both venture capital and strategic investors

From the perspective of the distribution characteristics of financing types, among projects that disclosed external financing information, the majority are in the early stages of financing, with Series A and angel rounds accounting for more than 30% of the total number of companies. Additionally, more than half of the projects have not raised external capital or are majority-owned by publicly listed companies.

Industries driven by technology can generally be divided into four stages: the seed stage, the introduction stage, the growth stage, and the maturity stage. During the seed and introduction stages, technologies face multiple uncertainties, such as technical efficacy, lifecycle, and market acceptance, which often attract venture capital investment. Currently, investment in the CAR-T therapy sector exhibits this characteristic. Furthermore, since most mature domestic pharmaceutical companies originated from generic drugs or traditional Chinese medicine and lack the inherent capabilities for novel drug development, coupled with the high costs associated with R&D, they also tend to invest in or acquire innovative projects to enter the CAR-T therapy field.

During the subsequent industrialization and commercialization phases of CAR-T products, strategic investors—primarily pharmaceutical companies—can provide growth-stage projects with experience and resource support in GMP manufacturing and channel promotion. Meanwhile, venture capitalists can achieve exit from their investments through mergers and acquisitions (M&A) by mature enterprises. Currently, based on the development of the U.S. biopharmaceutical industry, M&A transactions have significantly outnumbered IPOs as a means of project exit in recent years.

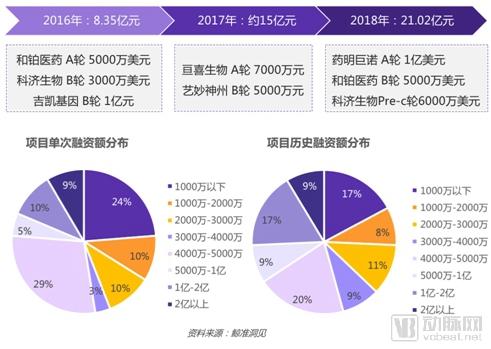

5.5 Distribution Characteristics of Investment and Financing Amounts: Historical project financing amounts were mostly around RMB 50 million, with relatively higher financing amounts in 2018

In terms of financing amounts, among the companies that disclosed their external financing figures, more than half secured single-round financing exceeding RMB 40 million. The most concentrated range for historical cumulative financing was between RMB 40 million and RMB 50 million. There were nearly ten large-scale financing events involving single rounds of RMB 100 million or more, six of which occurred in 2018. Compared with 2017, although fewer new companies were established in 2018, their cumulative financing to date has already surpassed the total for the entire year of 2017. This indicates that the field still holds investment potential and value during this stage of technological immaturity. In addition to WuXi Juno, Harbour Biomed, and Carsgen Therapeutics, which each secured single-round financing exceeding RMB 300 million in 2018, other companies such as Puruijin, Weiming Xuyan Biologics, Annobio, and Biolysicon obtained Series A financing ranging from RMB 20 million to RMB 40 million in 2018. Financing in the CAR-T sector is expected to continue increasing in 2019.

6. Summary of Key Points

6.1 Summary of the Current State of the CAR-T Therapy Industry: The Market Consolidation Phase Has Not Yet Arrived, and Product Homogenization Is Significant

n Status 1: CAR-T industrialization has just begun

Although multiple companies in China have entered the CAR-T therapy sector, the industry is currently still in its technology introduction phase. Globally, only two CAR-T products have been approved for market launch to date. In China, it was not until 2018 that a few enterprises obtained Investigational New Drug (IND) approvals. There remains a considerable distance before CAR-T therapies achieve large-scale clinical application. This is particularly true in the field of solid tumors, which holds broader market prospects, where CAR-T therapy still awaits further technological breakthroughs.

n Status Quo 2: The Market Shuffle Has Not Yet Arrived

Given that drug marketing approval typically involves multiple stages, including preclinical studies and clinical trials, and is subject to stringent regulations and oversight by drug regulatory authorities, companies currently leading in R&D progress are not necessarily guaranteed to be the ultimate winners. As more companies launch registered drug clinical trials in the second half of 2018 and throughout 2019, a substantive market reshuffling will gradually emerge.

n Status Quo 3: Significant Product Homogenization

Based on current clinical studies and corporate R&D pipelines, most companies’ CAR-T products are concentrated on the CD19 and BCMA targets. Although many companies claim to have unique CAR structural designs, the actual differences among them are not significant. It is expected that a batch of CD19-targeted CAR-T products will be launched in the next 2–3 years, leading to more intense market competition.

6.2 Risks and Challenges in the CAR-T Therapy Industry: Uncertainties in Technology, Policy, and Market, Along with a Talent Shortage

n Challenge 1: Technology remains unstable, with rapid update cycles

Currently marketed CAR-T therapies and ongoing research studies are exclusively targeted at patients with relapsed or refractory hematologic malignancies. Existing clinical trials have demonstrated high response rates only in a subset of patients, while uncertainties remain regarding the durability of responses and strategies to prevent tumor relapse, indicating that the technology is not yet fully stable. Furthermore, with the future advancement of universal (off-the-shelf) CAR-T technologies, autologous CAR-T products currently under development by companies may face the risk of being replaced.

n Challenge 2: Policies are relatively lagging, and regulatory details remain to be explored

Similar to the early stages of many biotechnology booms, the introduction of regulatory policies for CAR-T therapy has lagged behind technological advancements. In particular, the CAR-T treatment process involves multiple steps, posing challenges for government regulation. This is compounded by the limited experience of China’s drug regulatory authorities in reviewing new drugs. Although regulatory principles were issued in late 2017, the document is only “trial” in nature, implying that future regulatory rules may change and affect the development direction of enterprises.

n Challenge 3: High Product Prices and Uncertain Market Acceptance

Based on the pricing of currently marketed CAR-T products and the production costs of CAR-T therapy, the price of CAR-T treatment is expected to remain in the range of several hundred thousand yuan in the short term. This implies that only a small subset of patients will have the purchasing power to afford it. Particularly in the early stages of market development, patient awareness of this technology remains low; consequently, post-launch sales performance may fail to meet the expectations of companies and investors.

n Challenge 4: Quality control is difficult, and there is a lack of professional talent

Compared with conventional antibody drugs, although the R&D progress of domestic enterprises in CAR-T therapy is not significantly behind that of major pharmaceutical innovation powerhouses such as the United States, long-standing weaknesses in drug manufacturing processes and quality control will continue to constrain the development of China’s CAR-T industry. Furthermore, as CAR-T therapy is an emerging modality, many management teams currently consist of personnel from research institutions, lacking professionals with in-depth expertise in process engineering and new drug regulatory submissions.

6.3 Development Trends and Investment Opportunities in the CAR-T Therapy Industry

n Trend 1: Market Barriers Will Gradually Increase

Since the China Food and Drug Administration (CFDA) clarified that CAR-T therapies are regulated as drugs, Investigational New Drug (IND) applications have become the first litmus test of a company’s productization capabilities. In particular, following WuXi Juno and Fosun Kite’s introduction of foreign manufacturing processes and quality control systems, the CFDA may further raise application and review standards by drawing on the regulatory experience of the U.S. FDA, posing greater challenges to enterprises. As industrialization deepens, market barriers for CAR-T therapies will gradually rise, and companies with insignificant therapeutic efficacy, unstable manufacturing processes, or inadequate quality control will be eliminated.

n Trend 2: Intensifying Competition in Solid Tumors

Currently, competition among companies in the CAR-T field is primarily focused on hematologic malignancies. However, the R&D and manufacturing experience gained in this area serves as a foundation for capturing the broader market of solid tumors. If companies can validate their technology platforms, manufacturing processes, and quality control capabilities through hematologic indications, they will be well-positioned to rapidly capture market share once significant technological breakthroughs in CAR-T therapy for solid tumors are achieved. Consequently, more intense market competition among enterprises will center on solid tumors.

n Investment Opportunity 1: UCAR-T Is Still in the Technology Incubation Phase

Nearly 100 companies in China are currently engaged in CAR-T research and development, with some valuations reaching billions. However, there is still significant room for growth in the application of CAR-T therapy to solid tumors, and universal (off-the-shelf) CAR-T technology remains in its incubation stage. These niche sectors continue to offer early-stage investment opportunities.

n Investment Opportunity 2: Demand for Domestically Produced Equipment and Reagents Will Grow

With the advancement of CAR-T therapy technology and the market launch of more CAR-T products, demand for upstream equipment, reagents, and raw materials is set to grow. Currently, the upstream sector is predominantly dominated by high-quality foreign suppliers. Domestically produced equipment and reagents, if they demonstrate stable quality, will have significant market potential. This is particularly true for automated equipment, where there is a market gap both in China and abroad.