Seven Key Variables Shaping the Future of Chain Pharmacies: E-Prescriptions, Prescription Diversion, and M&A Integration

Chinese chain pharmacies are facing numerous uncertainties. Nearly every forward-thinking enterprise is making projections based on its own experience and strategically positioning itself in advance.

If history truly could shed light on the future, then, regrettably, the history of chain pharmacies in China is too short, while the future stretches far too long; with limited capacity to bridge this gap, its reference value remains constrained.

The United States has a long-standing history in the chain pharmacy sector, offering experience that may be more worthy of reference. Unlike the innovative drug industry, which is highly technology-driven and characterized by significant generational technological gaps, chain pharmacies operate as an integrated retail-and-service business model. Given the similar operating environments for chain pharmacies in China and the United States, the developmental trajectory of the U.S. chain pharmacy industry merits closer study, as its experiences may provide directional guidance.

For this reason, VCBeat (WeChat: vcbeat) has analyzed the development trajectory of the U.S. chain pharmacy industry and compared it with the current state of China’s pharmaceutical retail sector to offer directional insights.

In this article, you will see:

Overview of the U.S. Pharmaceutical Market;

The Development History of the U.S. Chain Pharmacy Industry;

Analysis of Factors Influencing the Development of the Chain Pharmacy Industry in the United States;

Leading Companies and Business Models in the U.S. Chain Pharmacy Industry;

Opportunities Currently Facing China’s Chain Pharmacy Industry;

Implications of the U.S. Model for China;

A quick “spoiler” of the key points: At the end of this article, we will outline seven major variables as our forecast for the future development trends of the pharmaceutical retail industry.

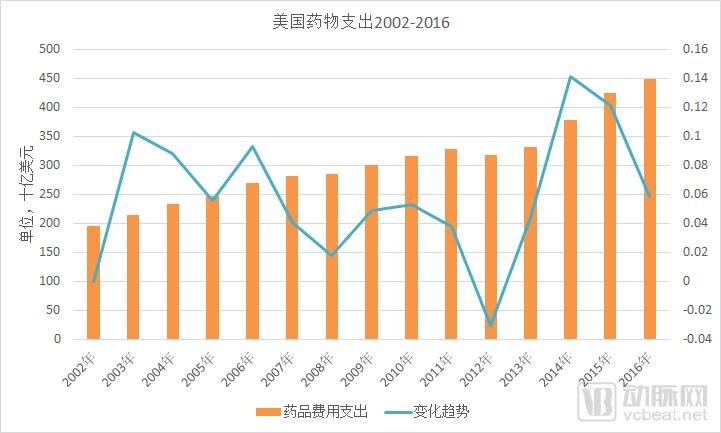

In terms of scale, the United States is the world’s largest pharmaceutical market, with drug expenditures reaching $450 billion in 2016. In the same year, global drug expenditures totaled $1.1 trillion, meaning that Americans “consumed” 40% of the world’s pharmaceuticals, fully earning the moniker of “biggest pill-popper.” IMS Health projected that U.S. drug spending would reach $560–$590 billion by 2020, representing a 34% increase from 2015 levels.

Data sources: IMS, Statista, VCBeat

From the perspective of product structure, the U.S. pharmaceutical market is dominated by patented drugs, with generic drugs playing a supplementary role. Although generics account for more than 80% of prescription volume, their market size represents only about 12%. This is closely related to the high number of new drug approvals and the short approval timelines in the United States, which enable patients to access new medications rapidly after launch.

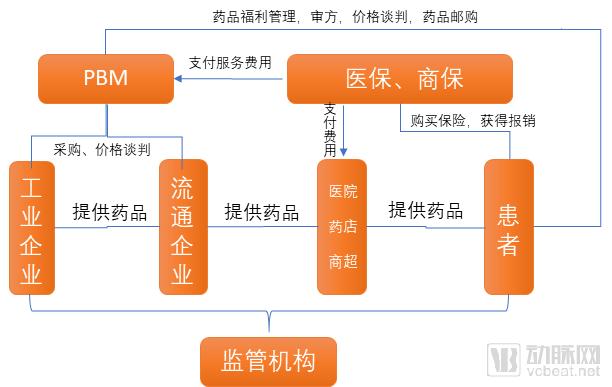

The United States enforces a strict separation between medical practice and pharmaceutical dispensing, coupled with robust prescription management, resulting in a drug distribution terminal structure that differs significantly from China’s. Based on sales volume, the ratio of in-hospital to out-of-hospital channels in the U.S. pharmaceutical market is approximately 3:7. Major out-of-hospital channels include retail chain pharmacies, independent pharmacies, PBM mail-order services, and supermarket pharmacies.

U.S. Pharmaceutical Market Division of Labor

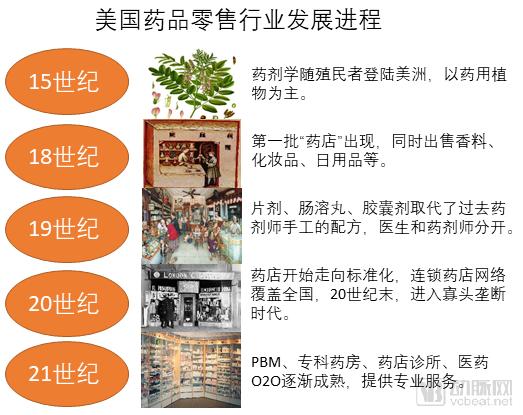

Following Columbus’s initiation of his American adventures in the late 15th century, the ancient science of pharmacy arrived on the American continent with the colonists. Therapeutic practices at that time relied primarily on medicinal plants, including sassafras from Florida and cinchona bark from Peru, the latter of which became an effective treatment for malaria.

The history of pharmaceutical retail in the United States dates back to the latter half of the 18th century, when the first “drugstores” in North America emerged in New York, Philadelphia, and Boston. These establishments not only dispensed medications but also sold spices, cosmetics, and daily necessities. Pharmacists held “exclusive” formulations and provided medical and pharmaceutical services based on their personal experience. At that time, the roles of physician and pharmacist were often indistinguishable, and there was a lack of systematic standards.

By the 19th century, the United States had rapidly emerged as an industrial nation with a highly developed chemical industry, laying the foundation for the growth of the pharmaceutical sector. Tablets, enteric-coated pills, and capsules replaced the traditional hand-compounded preparations made by pharmacists. It was in this context that the roles of physicians and pharmacists became distinct, and medicines evolved into standardized products, giving rise to the modern pharmacy.

Throughout the 20th century, the U.S. retail pharmacy industry underwent a process of “standardization,” characterized by the emergence of chain and standardized pharmacies and the establishment of nationwide retail pharmacy networks. By the end of the 20th century, an oligopolistic market structure had emerged, with chain affiliation rates reaching unprecedented levels. Meanwhile, driven by factors such as drug price control legislation, the rise of generic drugs, cost-containment demands from commercial insurers, the advent of Pharmacy Benefit Managers (PBMs), and the growth of specialty pharmacies, the pharmaceutical retail industry began to move toward greater consolidation and specialization.

Providing medical and pharmaceutical services in retail pharmacies is a distinctive feature of the U.S. healthcare system. Major pharmacy chains such as Walgreens and CVS offer basic diagnostic and treatment services within their stores. These companies also serve as Pharmacy Benefit Managers (PBMs), collaborating with health insurance providers to deliver services including prescription review, pharmacy benefit plans, procurement negotiations, and patient management, with pharmaceutical care constituting a core component of their offerings.

Currently, the key players in the U.S. pharmaceutical retail sector include chain pharmacies, independent pharmacies, specialty pharmacies, PBM mail-order services, and supermarket pharmacies, with varying products and services offered by these different types of endpoints.

In terms of market share, chain pharmacies account for over 40%, while the share of independent pharmacies is gradually declining to around 15%. PBM mail-order services hold a 25% share, and supermarkets and specialty pharmacies account for 20%.

From the perspective of factors influencing the development of the U.S. pharmaceutical retail industry, there are four major drivers: demographic shifts, increased health insurance coverage, accelerated approval and launch of new drugs, and intensifying cost-containment pressures.

First, population aging drives the demand for management of chronic diseases and long-term medication. According to U.S. Census Bureau data, as the Baby Boomer generation ages, the population aged 55 and older is projected to increase by 67% from 2000 to 2020, while the total population grows by only 19% over the same period. The average number of prescriptions among the elderly is more than five times that of middle-aged and younger adults, leading to substantial demand for pharmaceuticals.

Secondly, the United States passed the Affordable Care Act (ACA) in 2010, extending health insurance coverage to more than 30 million additional individuals. The increase in insurance coverage has boosted demand for pharmaceuticals, generating an incremental drug market worth $20–30 billion.

Meanwhile, the accelerated market launch of new drugs and innovative therapies has created opportunities for the specialized development of pharmaceutical retail. An increasing number of pharmaceutical manufacturers are choosing to provide patients with specialty medications and pharmaceutical care services through retail pharmacies rather than medical institutions, making Direct-to-Patient (DTP) pharmacies the fastest-growing segment in the pharmaceutical retail market.

The demand for controlling medical insurance costs has driven retail pharmacies to lower drug prices through group purchasing, price negotiations, and other means. Scale has become a crucial bargaining power, further accelerating the trend toward large-scale and intensive development in the retail pharmacy sector.

PBM organizations and the “pharmacy + clinic” model are increasingly becoming market favorites. The former’s original business focused on cost containment for insurers through prescription review, price negotiation, patient management, and differentiated reimbursement rates. However, over the course of its development, it has gradually penetrated into the pharmaceutical retail sector by providing long-term prescriptions and chronic disease medications via mail-order services, thereby becoming a significant force in pharmaceutical retail that cannot be overlooked.

The “pharmacy-plus-clinic” model, known as a pharmacy-clinic or retail clinic, refers to primary care clinics located within pharmacies. Staffed by nurse practitioners and pharmacists with prescriptive authority, these clinics manage common conditions and offer significant cost advantages—pricing 30% lower than community clinics and 80% lower than hospital emergency departments. Consequently, they have gained widespread acceptance, rapidly expanding across retail pharmacies, and achieved high patient satisfaction.

The two most prominent companies in the U.S. retail pharmacy industry are Walgreens Boots Alliance and CVS Health. Over the past few decades, these two enterprises have engaged in intense competition, consistently occupying the top two positions in the U.S. pharmaceutical retail sector. However, their development trajectories exhibit both similarities and differences.

Walgreens Boots Alliance

Walgreens Boots Alliance (WBA) was formed in 2014 through the merger of Walgreens, the largest chain pharmacy group in the United States, and Alliance Boots, a UK-based pharmaceutical retailer and distributor. Both companies boast century-long histories: Walgreens was founded in 1901, and Alliance Boots was established in 1834.

Walgreens Boots Alliance is headquartered in Delaware, United States, and operates in 251 countries and regions worldwide. Its business segments include the Walgreens pharmacy chain, Duane Reade pharmacy chain, Alliance Healthcare pharmaceutical distribution, and health and consumer brands such as No7, Soap & Glory, Liz Earle, Sleek MakeUP, and Botanics.

Walgreens Boots Alliance’s Health and Personal Care Brands

Image source: Walgreens Boots Alliance official website

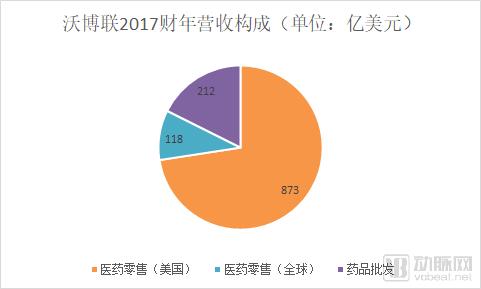

As of fiscal year 2017 (ended August 31, 2017), Walgreens Boots Alliance operated more than 13,200 pharmacies across 111 countries and regions worldwide (including 8,100 locations in the United States, with approximately 76% of the U.S. population living within five miles of a Walgreens or Duane Reade retail pharmacy); 3,901 distribution centers supplying medications to up to 230,000 pharmacies, physicians, healthcare centers, and hospitals; a workforce of 385,000 employees; and fiscal year 2017 revenue of $118.2 billion.

“Focusing on pharmacies and diversifying operations” encapsulates the secret to Walgreens Boots Alliance’s success. Pharmacies constitute the core business of Walgreens Boots Alliance; both Walgreens and Boots United, prior to their merger, were primarily pharmacy-focused. However, there are slight differences between the U.S. and UK pharmaceutical markets. In the United States, where prescribing and dispensing are separated, pharmacies exhibit a higher degree of specialization. In the United Kingdom, under the National Health Service (NHS) system, prescription drugs are centrally procured and price-controlled, with pharmacies mainly dealing in over-the-counter medications, health products, and daily chemical goods.

Source: Walgreens Boots Alliance FY2017 Annual Report; Graphic by VCBeat

Focusing on the pharmacy business model, Walgreens has experimented with various innovative services, including “pharmacy + clinic” models, pharmacy benefit management (PBM), and online-to-offline (O2O) integration. In the United States, Walgreens Boots Alliance operates approximately 400 “pharmacy + clinic” locations (primarily within Walgreens pharmacies), where customers receive services from professional medical and pharmaceutical personnel—such as pharmacists, physicians, and nurse practitioners—employed by or partnered with its healthcare organizations. Additionally, Walgreens Boots Alliance integrates online and offline channels through its mobile app and membership programs. Its Balance® Rewards program allows members to earn points through activities like walking, weight tracking, and health management, serving as the pioneer for incentive initiatives such as “Step into Gold.”

In recent years, Walgreens Boots Alliance has been continuously pursuing global mergers and acquisitions, investing in pharmaceutical distribution and retail companies in countries including the United Kingdom, France, Germany, the United States, and China. For instance, it established a joint venture, Guangzhou Pharmaceutical Holdings Limited, with Guangzhou Pharmaceutical Group in 2008 (Guangzhou Pharmaceutical Group repurchased its shares in December 2017). On November 30, 2017, Sinopharm Holding Guoda Drugstore confirmed the introduction of Walgreens Boots Alliance as a strategic investor. Resource integration has become a key pathway for Walgreens Boots Alliance’s global expansion.

CVS Health

CVS originated in the 1960s. Its initial business was not pharmaceutical retail; it gradually shifted its focus to pharmaceutical retail after two or three years of operating health products. By 1970, CVS had reached 100 stores in New England and the Northeastern United States. By 1985, CVS’s annual sales exceeded $1 billion.

While expanding its scale through continuous acquisitions, CVS also focused on horizontal mergers and acquisitions to broaden its business scope. In 2006, CVS acquired MinuteClinic, establishing a new business model featuring small clinics within its pharmacies. In 2007, CVS merged with Caremark, a pharmacy benefit manager (PBM), to strengthen its PBM operations. In 2015, CVS acquired Target’s retail pharmacy business, gaining more than 1,600 pharmacies and 80 clinics, thereby becoming the second-largest pharmaceutical retailer and pharmacy services provider in the United States.

CVS’s Latest Acquisition Sets a New Record for M&A in the U.S. Pharmaceutical Retail IndustryIn December 2017, CVS announced it would acquire Aetna, a health insurance company, for $69 billion. This deal marked the largest transaction in the history of the U.S. pharmaceutical retail sector and was also the biggest deal globally within the pharmaceutical industry in 2017. Aetna is a leading commercial insurer in the United States, providing property and casualty, life, and health insurance services to governments, businesses, and individuals. With over 23 million members in its health insurance segment, Aetna reported health insurance premium revenues of $13.469 billion in 2016. In March 2018, the transaction was approved by Aetna’s Board of Directors.

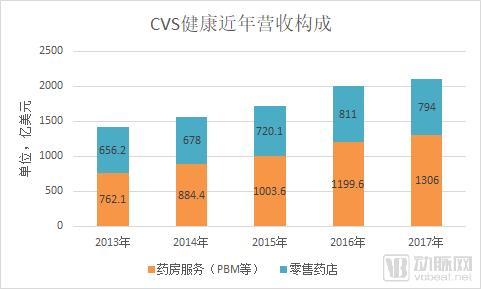

CVS’s revenue is derived from two core businesses: retail pharmacy and pharmaceutical services. The latter refers to comprehensive pharmacy benefit management (PBM) services, including mail-order pharmacy services, specialty pharmacy and infusion services, health management programs, prescription management, and claims processing provided by CVS Caremark. The primary clients for this business segment include employers, insurance companies, labor unions, government employee organizations, health plans, managed Medicaid programs, as well as other health benefits plan sponsors or individuals.

Data Source: CVS Annual Report; Graphic by VCBeat

In its annual report, CVS stated that since 2014, the compound annual growth rate (CAGR) of PBM revenue has reached 13.9%, with a CAGR of 10.6% for operating profit. Net revenue from PBMs is projected to climb to approximately $134 billion in 2018, while the segment’s operating profit is expected to approach $5 billion.

The core of CVS’s growth lies in the “dual-engine” strategy driven by its PBM business and pharmaceutical retail operations. In the U.S. drug expenditure landscape, which is dominated by commercial insurance and out-of-pocket payments, this approach offers significant advantages, enabling comprehensive fulfillment of payers’ needs to control drug costs and secure medication supply. Following its merger with Aetna, a specialized health insurer, CVS’s business model has evolved into an integrated “health insurance + PBM + pharmaceutical retail” framework, delivering stronger synergies and enhanced customer retention. The key takeaway from CVS is the importance of horizontal expansion, rather than remaining confined solely to pharmaceutical retail.

Although both Walgreens Boots Alliance and CVS Health are companies with pharmaceutical retail as their core business, their development paths and business landscapes differ significantly. The most apparent distinction is that Walgreens Boots Alliance has greater depth in its business operations, while CVS’s diversification strategy has enabled it to gain competitiveness beyond the retail sector.

There is no inherent superiority or inferiority among business models; what matters most is their suitability for a company’s development. For domestic pharmaceutical retail enterprises undergoing rapid transformation, the choice between the Walgreens Boots Alliance model and the CVS model may well determine their future fate.

Walgreens Boots Alliance vs. CVS Health Comparison

Data sources: Walgreens Boots Alliance, CVS Health annual reports; compiled by VCBeat

From the perspective of influencing factors, China’s pharmaceutical retail industry shares both similarities and differences with that of the United States. The similarities lie in demographic shifts, the accelerated separation of prescribing from dispensing, improved drug supply, and heightened cost-containment demands from payers. The differences are evident in market concentration, levels of informatization, and the payment capacity of commercial insurance. However, it is highly probable that China’s pharmaceutical retail format will evolve toward the U.S. model, or at least become a “variant” thereof.

During this process, domestic pharmaceutical retail enterprises primarily undertook two key initiatives: large-scale mergers and acquisitions for consolidation, and the enhancement of pharmaceutical and medical service capabilities.

From the perspective of mergers and acquisitions (M&A) integration, capital participation is the primary manifestation. In recent years, professional investment firms such as GF Xinde and Hillhouse Capital, along with industrial enterprises including GPC Baiyunshan, Tasly Group, and Buchang Pharmaceuticals, have actively engaged in investments and M&A within the pharmaceutical retail sector. Coupled with listed pharmaceutical retail companies intensifying their acquisitions of small chain pharmacies, the industry has witnessed a vigorous “land grab” campaign. Meanwhile, the entry of internet-plus-pharmaceutical companies, such as Ali Health, has introduced additional counterbalancing forces to the industry.

The chain store penetration rate is a key metric. Under large-scale mergers and acquisitions (M&A) and integration, the chain store penetration rate in the pharmaceutical retail industry has risen rapidly, with leading enterprises gaining market share at an even faster pace. M&A and integration activities in the chain pharmacy sector are expected to continue until the cost of acquisition exceeds the market’s future expectations. Furthermore, given regional disparities in China’s retail pharmacy industry, a nationwide pharmacy network comparable to Walgreens Boots Alliance or CVS is unlikely to emerge; instead, the landscape will likely be characterized by dominant regional players.

The separation of pharmaceuticals from medical services and the outflow of prescriptions are regarded as significant growth opportunities for the retail pharmacy industry in the future. Currently, companies such as Baiyang Yifuzhen, WeChat, AliHealth, Jointown Pharmaceutical Group, and Yaoshiquan are actively positioning themselves in this sector. Policies in cities like Xi’an, Chengdu, Chongqing, and Tianjin are also relatively supportive. However, a nationwide, large-scale system for the external circulation of hospital prescriptions has not yet taken shape.

Three major factors constrain the outflow of prescriptions from hospitals: prescription sources, medical insurance support, drug supply assurance, and pharmaceutical care service capabilities. These issues involve adjustments to the interests and revenue structures of hospitals and physicians, increased difficulty in controlling medical insurance costs, and a lack of service capabilities among chain pharmacies.

Based on U.S. experience, the electronic prescription sharing platform model is feasible: According to Medscape data, electronic prescriptions account for 77% of all prescriptions in the United States. Physicians obtain prescribing credentials from regulatory authorities, and their prescribing behaviors are monitored through measures such as physician identification numbers and electronic signatures to prevent the misuse of prescription drugs. Electronic prescriptions can be seamlessly integrated between physicians’ clinics and retail pharmacies, facilitating medication pickup and refills for patients. From a technical implementation perspective, electronic prescription sharing platforms are not complex. With the introduction of detailed regulatory guidelines, this model could be implemented in China, which would benefit the development of the pharmaceutical retail industry.

Drawing on U.S. experience, the following projections are made for the future development of China’s pharmaceutical retail industry:

1. The separation of prescribing from dispensing will continue to be implemented, with the scale of retail pharmacies surpassing that of hospitals;

2. The prescription sharing platform will become a critical hub connecting hospitals and pharmacies, with the use of electronic prescriptions becoming the norm;

3. M&A integration will increase industry concentration, and the future industry landscape may consist of a few national leaders plus several regional leaders;

4. DTP pharmacies and specialty pharmacies are rapidly developing, becoming an important business format independent of general chain pharmacies;

5. Drug supply assurance capabilities and pharmaceutical care service capabilities will become the competitive moat for retail pharmacies; enterprises that “empower” chain drugstores by providing such services have certain market opportunities;

6. The PBM model still lacks a foundational basis in China, relying on the development of commercial health insurance, the willingness to control medical insurance costs, and an increased demand for pharmaceutical care services;

7. Retail pharmacies will integrate with models such as internet healthcare, pharmaceutical e-commerce, and O2O (Online-to-Offline), making omni-channel integration the industry norm. Membership management and operational capabilities will enhance competitiveness in the market and also spur entrepreneurial opportunities.