Private Healthcare Sector in China Sees Remarkable Growth as 2017 National Health Statistics Released

Content Summary

2017 was a pivotal year for advancing the Healthy China initiative and implementing the 13th Five-Year Plan, as well as the ninth year of the “New Healthcare Reform.” While China’s medical and health sector achieved certain accomplishments, it also faced numerous challenges amid the unique transitional phase of social transformation. In June of this year, the National Health and Family Planning Commission released the “Statistical Bulletin on the Development of China's Health and Hygiene Undertakings in 2017》,presenting the basic status of China’s health resources, medical services, and primary healthcare in 2017; this report provides a comprehensive review of the development of China’s healthcare sector by integrating historical data from 2010 to 2016.

The New Healthcare Reform is the opinion on deepening the reform of the medical and health system announced by the Central Committee of the Communist Party of China and the State Council to the public, which came into effect on March 17, 2009. The New Healthcare Reform proposed "effectively reducing the burden of medical expenses for residents and effectively alleviating‘# Difficulty in Accessing Medical Care、the near-term goal of addressing “high medical costs,” and the long-term goal of “establishing and improving a basic healthcare system that covers both urban and rural residents, providing the public with safe, effective, convenient, and affordable healthcare services.”

The main components of the new healthcare reform include the following aspects:

First, accelerate the development of the basic medical security system, ensuring that participation rates in the Basic Medical Insurance for Urban Employees, the Basic Medical Insurance for Urban Residents, and the New Rural Cooperative Medical Scheme all exceed 90%. Improve the urban and rural medical assistance system to significantly reduce the out-of-pocket medical expenses borne by urban and rural residents.

Second, a national essential medicines system was preliminarily established, creating a relatively comprehensive framework for the selection, production and supply, utilization, and medical insurance reimbursement of essential medicines.

Third, improve the grassroots medical and health service system, accelerate the development of the three-tier rural medical and health service network and urban community health service institutions, and leverage the leading role of county-level hospitals.

Fourth, promote the gradual equalization of basic public health services. Since 2009, basic public health services—including disease prevention and control, maternal and child healthcare, and health education—have been progressively provided uniformly to both urban and rural residents. We will strengthen the urban-rural public health service system and improve the funding guarantee mechanism for public health services.

Fifth, advance pilot reforms of public hospitals, reform their compensation mechanisms, increase government funding, improve economic compensation policies for public hospitals, and gradually resolve the issue of “subsidizing medical services with drug revenues.”

2017 marked the ninth year since the implementation of the new healthcare reform, and the year following the 2016 advancement of systematic reforms through the “three-medical-linkage” approach. China’s healthcare reform has progressed steadily, and the country’s health sector has achieved certain accomplishments. The following section provides a detailed discussion on the current status and trends of China’s health development, based on historical statistical data from the National Health and Family Planning Commission.

1.1 Healthcare Reform Continues to Deepen, with Significant Improvement in the Overall Health of Residents

With the gradual implementation of the Healthy China strategy, healthcare reforms continue to deepen, increasingly meeting the public’s health needs and steadily improving the overall health status of the population. However, due to the accelerated pace of modern life and work, along with unhealthy dietary and lifestyle habits, the prevalence of diseases among residents has been rising day by day. There remains considerable room for improvement in disease prevention and control within China’s healthcare sector.

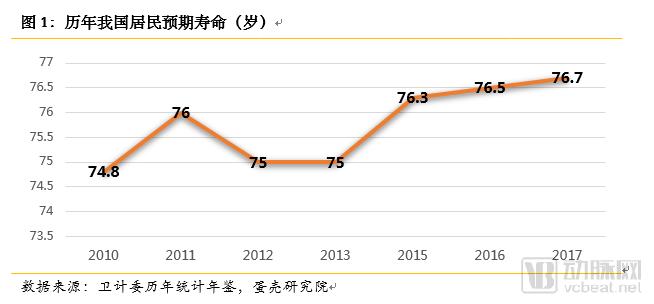

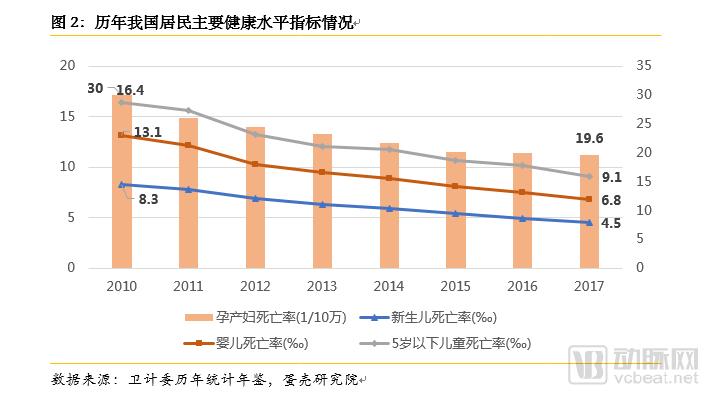

Life expectancy at birth is an indicator used to measure the health status of residents in a country, ethnic group, or region, reflecting the quality of life of the local population. A review of data from 2010 to 2017 reveals that life expectancy among Chinese residents generally exhibited a slow growth pattern with minor fluctuations. In 2017, average life expectancy reached 76.7 years, representing a year-on-year increase of 0.2 years. Assessing the health status of a country or region requires not only examining life expectancy but also considering mortality rates among pregnant women and young children, which serve as additional indicators of healthcare service quality and living standards. From 2010 to 2017, China’s neonatal mortality rate, infant mortality rate, under-five mortality rate, and maternal mortality ratio all demonstrated a consistent year-over-year decline, highlighting the significant progress made in maternal and child healthcare since the launch of the new round of healthcare reforms.

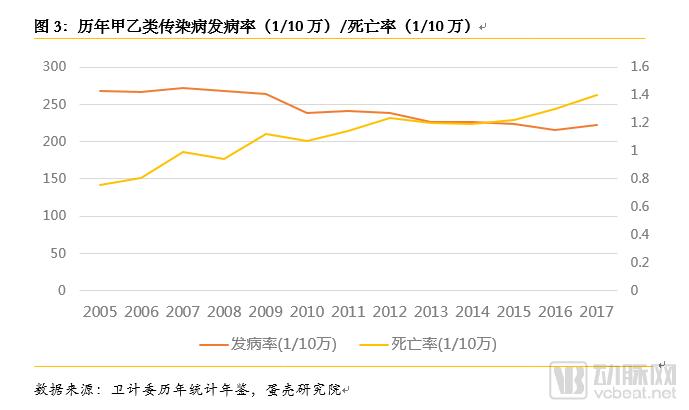

According to the data in the chart above, China has achieved favorable control over the incidence of infectious diseases. The period prior to 2008 marked a peak in infectious disease incidence in China. During this phase, the high incidence rate was attributable to inadequate sanitation facilities, unhealthy lifestyle and dietary habits among residents, and a lack of health care knowledge. In 2009, the National Health and Family Planning Commission, in conjunction with other departments, jointly promulgated and implemented the new healthcare reform, aiming to significantly address the challenges hindering the development of China’s medical and health sector. From 2009 to 2017, the incidence of infectious diseases in China was effectively controlled, decreasing from 268.01 per 1,000 population in 2008 to 222.1 per 1,000 in 2017. These vigorous prevention and control efforts have substantially improved residents’ quality of life. However, it is important to note that while the incidence rate has been curtailed to some extent, the trend in infectious disease mortality remains concerning, showing a year-on-year increase from 0.76 per 1,000 population in 2005 to 1.40 per 1,000 in 2015. Many infectious diseases pose fatal risks if left uncontrolled. It is recommended that relevant authorities intensify their efforts in the prevention and treatment of infectious diseases, or encourage social capital to invest in the infectious disease prevention and control industry.

1.2 Health Resource Structure Trends Toward Optimization, New Progress in Socially-Run Healthcare

Hospitals have always been the core of a country or region’s healthcare service system. In particular, Grade A tertiary hospitals, with their superior medical resources, have long attracted a large influx of patients, leading to overcrowding and severe shortages of hospital beds—a phenomenon commonly referred to as “difficulty in accessing medical care.” The new healthcare reform emphasizes that developing primary care and non-public medical services is the fundamental approach to resolving this issue, thereby diverting patients from large hospitals and alleviating the pressure on their medical services. The following section provides a detailed analysis of the allocation of medical resources in China from three perspectives: the number of medical institutions, the number of hospital beds, and healthcare personnel.

Data Source: National Health and Family Planning Commission Statistical Yearbooks, VCBeat

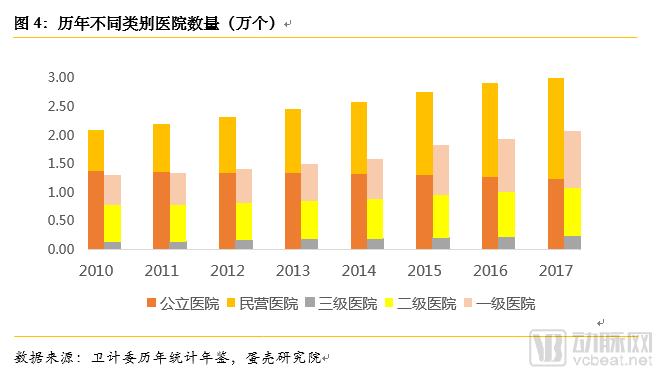

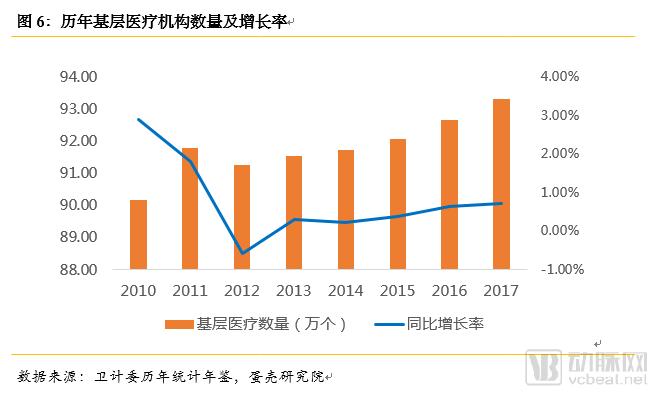

Overall, the number of medical institutions in China has shown a slow but steady upward trend, increasing from 937,000 in 2010 to 987,000 in 2017, a net increase of approximately 50,000. However, there was a decline in 2012, primarily due to the implementation of integrated rural management, which led to the merger of numerous village clinics and a reduction of about 5,000 primary healthcare institutions. In terms of the distribution across different types of medical institutions, primary healthcare institutions overwhelmingly dominate, significantly outnumbering other categories. Their annual share consistently exceeds 93%, maintaining a slight yet stable growth. In contrast, hospitals and specialized public health institutions are relatively fewer in number and comparable in scale. Hospitals have experienced consistent annual growth, whereas specialized public health institutions have followed a trend of initial increase followed by decline. The sharp rise in data in 2013 was mainly attributable to the inclusion of family planning technical service institutions previously administered by the former family planning departments. Following the nationwide implementation of the universal two-child policy in 2016, the number of family planning technical service institutions dropped sharply, directly leading to a year-on-year decrease in the total number of specialized public health institutions.

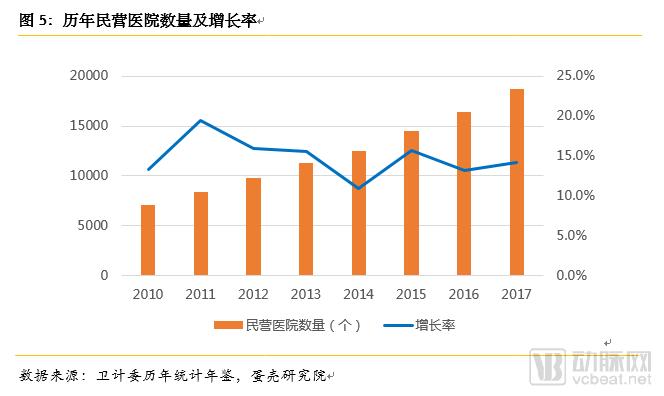

Furthermore, although the initial number of private hospitals was lower than that of public hospitals, their growth rate has been significantly faster, maintaining a continuous annual increase of over 10%. Since 2015, the number of private hospitals has surpassed that of public hospitals. This rapid expansion is primarily attributable to the release of policy dividends from the new healthcare reform, in which the government advocates for social participation in healthcare delivery and encourages the development of the private medical sector.

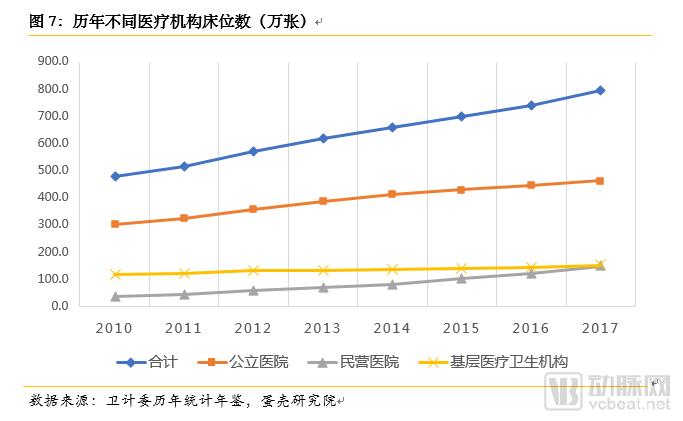

The number of medical and health institutions can, to some extent, reflect the overall scale of medical resources in China; however, there are significant disparities in the size and capability of different medical institutions. For instance, in 2017, primary care medical and health institutions accounted for 95% of all medical institutions in China, but this single indicator alone does not suffice to conclude that the primary care sector possesses the vast majority of medical resources. The number of hospital beds is a more indicative measure of a medical institution’s service capacity and resource endowment, and may better reflect the distribution of medical resources than the mere count of medical institutions.

In 2017, the total number of hospital beds in medical institutions across China reached 7.94 million, an increase of 530,000 from the previous year, representing a year-on-year growth of 7.2%. Public hospitals dominated bed supply, with 4.613 million beds, an increase of 176,000 from the previous year. The number of beds in private hospitals grew from 374,000 in 2010 to 1.234 million in 2016, a net increase of 860,000 and a cumulative growth rate of up to 230%! However, the current development status of private hospitals can be summarized as “numerous but not strong,” remaining largely marginalized overall. According to the National Health and Family Planning Commission’s “Guiding Principles for the Planning of Medical Institution Establishment (2016–2020)” (hereinafter referred to as the “Principles”), the indicative targets for the number of hospital beds per 1,000 residents in public hospitals and socially run hospitals are 3.3 and 1.5, respectively, with a ratio of 2.2:1. In 2017, however, the bed ratio between public hospitals and socially run hospitals was 3.1:1. The number of beds in socially run hospitals still falls short of the indicative targets set forth in the “Principles,” indicating that there remains significant room for growth in the development of private hospitals.

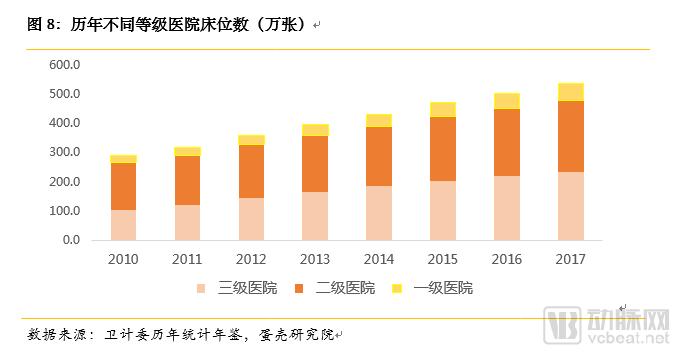

Across different hospital tiers, it is evident that tertiary and secondary hospitals account for over 90% of all hospital beds, thereby meeting the inpatient care needs of the vast majority of patients. In contrast, primary hospitals—primarily community-level facilities such as local clinics and health centers—provide preventive, therapeutic, healthcare, and rehabilitation services to defined populations. Their bed capacity is generally allocated to minor illnesses and emergency care rather than inpatient hospitalization, resulting in a relatively small overall scale, with their share accounting for only approximately 10%.

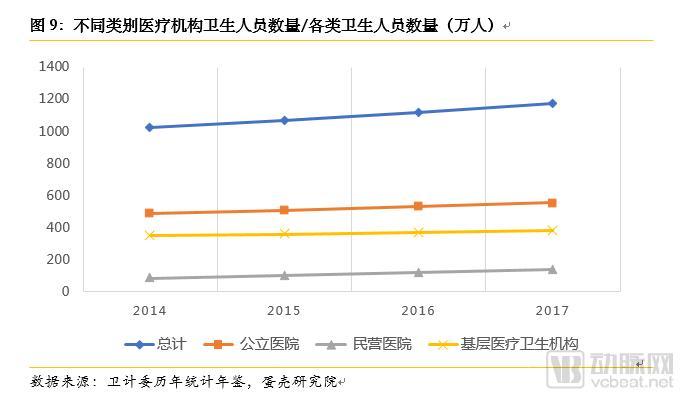

The development of the healthcare sector relies not only on hardware support from medical resources but, more importantly, on the dedication of a vast workforce of health personnel. From 2010 to 2017, the total number of health personnel in China increased from 8.208 million to 11.749 million, representing a net increase of 3.541 million and a growth rate of 43.1%. Among these, the number of professional health technicians rose by 3.112 million, with a substantial growth rate of 53.0%, indicating that the overall growth in health personnel was primarily driven by the increase in professional health technicians. In contrast, the number of village doctors and health aides decreased by 123,000, reflecting a negative growth rate of 11.3%. The number of licensed (assistant) physicians saw a rapid net increase of 977,000 during this period, corresponding to a growth rate of 40.5%.

Across different categories of hospitals, the number of healthcare personnel in public hospitals is significantly higher than that in private hospitals and primary healthcare institutions. However, private hospitals have witnessed a rapid growth in their healthcare workforce, which increased from 860,000 in 2014 to 1.428 million in 2017, representing a net increase of 563,850 and a cumulative growth rate of 66.0%. This trend reflects the growing attractiveness of private hospitals to talent, with an increasing number of healthcare professionals choosing to work in private medical institutions.

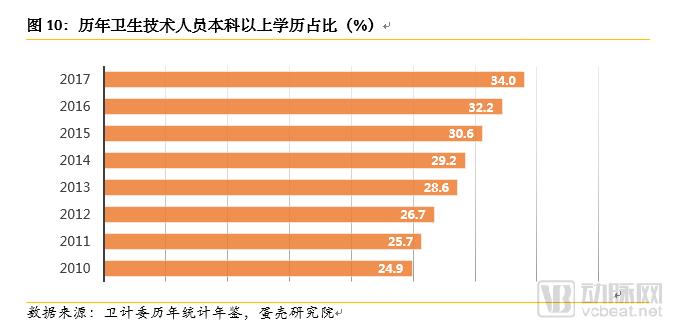

Healthcare professionals are the core of healthcare service delivery within the medical system, making workforce development critically important. A review of historical data clearly demonstrates a year-on-year optimization trend in the development of China’s healthcare professional workforce. Using the proportion of personnel with a bachelor’s degree or higher as an indicator of educational attainment, we observe a continuous increase in this metric: rising from 24.9% in 2010 to 34.0% in 2017, representing a cumulative increase of nearly 10 percentage points.

1.3 Continued Increase in Government Health Spending and Full Launch of Drug Cost Reform

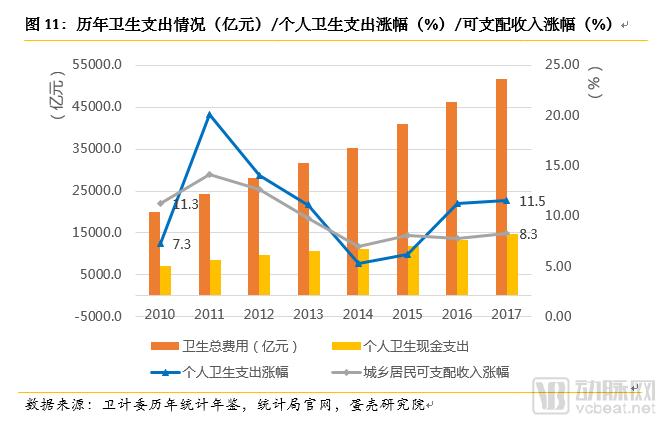

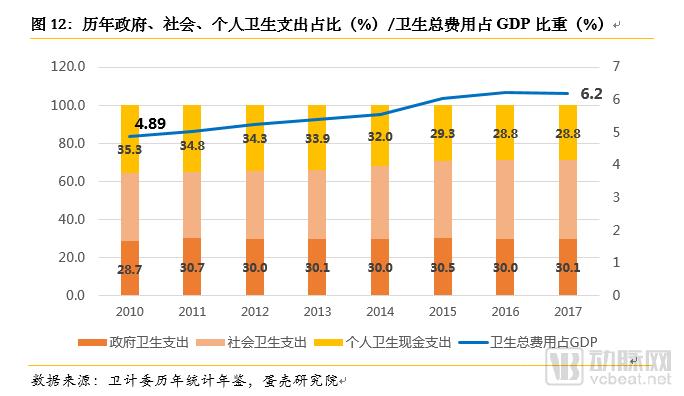

Since the launch of the new healthcare reform, government investment in healthcare has increased year by year. In 2017, total health expenditure reached RMB 5.16 trillion, accounting for 6.2% of GDP. The share of government health expenditure rose from 28.7% in 2010 to 30.1% in 2017. However, there remains a certain gap between this figure and the target set forth in the Healthy China 2030 Strategy, which aims to raise the proportion of total health expenditure to GDP to 6.5%–7%.

In addition, the share of out-of-pocket health expenditures decreased from 35.3% to 28.8%, indicating some improvement in health equity; however, a considerable gap remains compared with the 10%–15% target for equitable health financing proposed by the World Health Organization. It is worth noting that although the proportion of out-of-pocket spending has been declining, total health expenditure continues to grow rapidly. In 2017, the growth rate of out-of-pocket health expenditures remained significantly higher than that of residents’ per capita disposable income, meaning that the financial burden of healthcare on Chinese residents remains substantial.

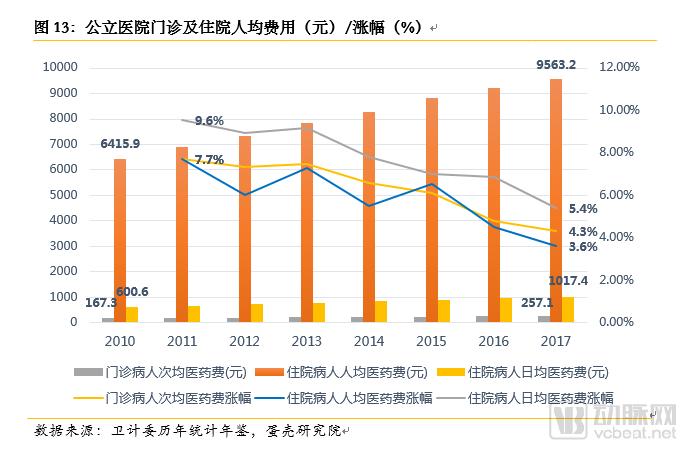

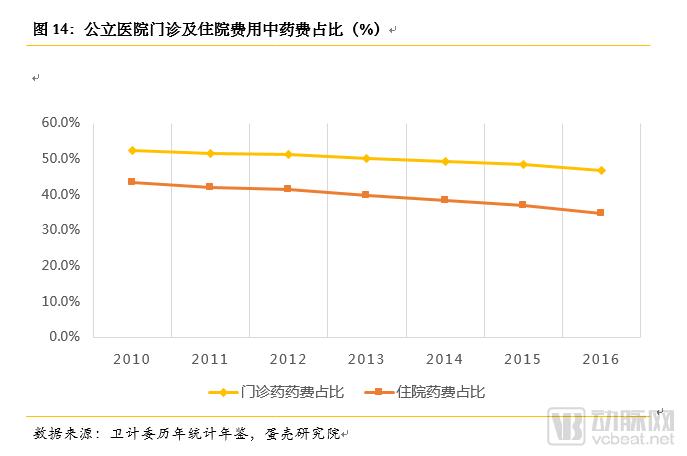

Within the logic of China’s new healthcare reform, reducing drug costs is a fundamental step in addressing the problem of “high medical expenses” and controlling the growth of health expenditures. The primary focus of this reform is public hospitals. In 2017, comprehensive reforms were fully rolled out across all public hospitals, eliminating all drug markups and abolishing the practice of subsidizing hospital operations through drug sales. Data on medical and pharmaceutical expenditures from recent years show that the proportion of drug costs in both outpatient and inpatient expenses at public hospitals has been continuously declining. Although the absolute value of medical expenses remains high and continues to rise year by year, the growth rate of these expenses is decelerating significantly. This trend demonstrates that China’s drug cost reforms have achieved certain phased results.

The remainder of Chapter 1 covers topics such as the efficiency and quality of health services, the development of primary healthcare, and the “universal two-child policy.”

Chapter 2: Based on health data analysis, this chapter highlights four major achievements of the new healthcare reform to date, including tiered diagnosis and treatment, pharmaceutical cost reform, development of private healthcare, and optimization of health resource allocation.

Chapter 3: A Summary of the Progress of China’s New Healthcare Reform, Focusing on the Achievements and Challenges Mentioned in Previous Chapters

Below is the complete table of contents of the report, which comprises three chapters and 31 pages in total.

1.1 Deepening Healthcare Reform and Significant Improvement in Overall Population Health

1.2 Optimization of Health Resource Structure and New Progress in Private Healthcare

1.3 Continuous Increase in Government Health Expenditure and Drug CostsComprehensive Launch of Reforms

1.4 Increased Utilization of Health Services by Residents and Improved Service Quality

II. New Healthcare Reform Rises to the Challenge, Healthy China Strategy Takes New Steps

2.2 Alleviating the High Cost of Medical Care: Reform of Drug PricingAchieved Phased Results

2.3 Full Release of Policy Dividends, Private Medical Institutions Gain Room for Development

III. The Long Road Ahead: The New Healthcare Reform Will Ultimately Benefit All Citizens

To read the remaining chapters, please scan the QR code to become a VCBeat member and download the full report, or purchase the report individually in the VCBeat Reports section.