111, Inc. (YI) Prices $100 Million IPO on NASDAQ, Closing Market Cap at $1.143 Billion

Image source: provided by the company

VCBeat News: On the 12th, U.S. Eastern Time, 111 Group, the parent company of China’s online pharmaceutical and healthcare platform Yihaodian (1 Drug Network), listed on the Nasdaq Stock Market (stock ticker: YI). This makes 111 Group the first Chinese internet pharmaceutical and healthcare company to go public in the United States.

In this IPO, 111 Group issued a total of 9.3 million American Depositary Shares (ADSs) at an offering price of $14 per share, raising $100 million in total. The proceeds will be primarily used for research and development, marketing and promotion, as well as strategic investments and acquisitions. J.P. Morgan, Citigroup, and CICC served as the joint underwriters for this IPO.

At the listing ceremony held that day, Dr. Yu Gang, Co-founder and Chairman of 111 Group, and Liu Junling, Co-founder, Chairman, and CEO of 111 Group, jointly delivered speeches.

Image source: Provided by the company

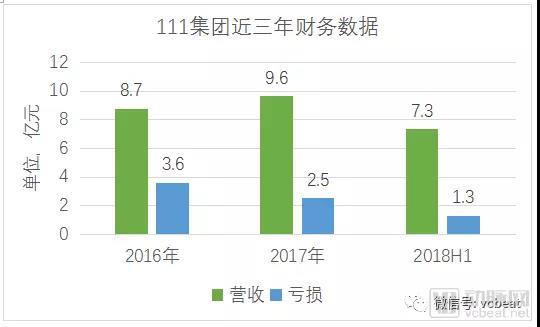

2017 Revenue Nears RMB 1 Billion, with Losses Continuing to Narrow

The name “111 Group” is derived from its three distinct business lines: 1YaoWang, 1Zhen Internet Hospital, and 1YaoCheng.

111 Group was co-founded by Dr. Yu Gang and Mr. Liu Junling, both of whom previously held positions at Yihaodian. Established in 2008, Yihaodian pioneered the “online supermarket” model in China. In 2015, Yu Gang and Liu Junling left Yihaodian to devote themselves fully to the operations of 111 Group.

1. 111.com was initially a sub-channel of Yihaodian, launching its business in 2010 and operating independently from 2012; in 2016, the 1 Doctor Internet Hospital went online; in 2017, 111 City went online.

According to the VCBeat database, 1YaoWang raised a total of more than RMB 1.5 billion in financing prior to its IPO, with investors including Ivy Capital and Tonghe Yucheng, among others.

The prospectus shows that, according to a research report by the U.S. research institution Frost & Sullivan, 1 Drug Network has been China's largest B2C self-operated online pharmacy since 2016, calculated based on Gross Merchandise Volume (GMV).

As of June 30, 2018, 111 Group served more than 100,000 offline pharmacies. 111 Group’s B2B pharmaceutical platform, 1 Yao Cheng (1 Drug City), serves as a one-stop service platform providing pharmacies with a comprehensive range of pharmaceutical products. According to a report by Frost & Sullivan, as of May 18, 2018, 111 Group had built the world’s largest virtual pharmacy network in terms of the number of pharmacies.

As stated in the prospectus, as of June 30, 2018, 111 Group’s professional medical team comprised more than 2,000 healthcare professionals, including over 80 direct employees. By integrating healthcare and pharmaceutical services, 111 Group has created a closed-loop platform, through which its professional medical team provides consumers with online consultation and electronic prescription services.

111 Group Key Data

Image source: 111 Group's prospectus

111 Group’s revenue is primarily derived from the sales and distribution of pharmaceutical products and other healthcare products, with nearly 300,000 SKUs available for sale.

In addition, 111 Group generates revenue from various business segments, such as providing services to platform merchants and collecting commissions. Meanwhile, the group also derives income by offering marketing services—including brand promotion and data support—to pharmaceutical companies and other clients.

111 Group’s revenue in 2017 was RMB 960 million, a year-on-year increase of 10%. In the first half of 2018, its revenue reached RMB 730 million, including RMB 97.2 million from B2B products and RMB 324.5 million from services.

B2B business is the fastest-growing segment of 111 Group, with its B2B gross merchandise value (GMV) reaching RMB 230 million in Q2 2018, up from RMB 160 million in Q1 2018, representing a year-on-year increase of 44.0%.

Meanwhile, 111 Group’s net loss margin decreased from 41.6% in 2016 to 26.0% in 2017, and from 28.2% in the first half of 2017 to 17.7% in the first half of 2018.

Leading Players in Pharmaceutical E-commerce Solidified: The Strong Grow Stronger

"Industry insiders say that 1 Drug's listing in the US will kick off a wave of IPOs for pharmaceutical e-commerce companies."

In fact, there are already several “pharmaceutical e-commerce” concept stocks in the A-share market. Those listed on the main board include Kang Aiduo, Haoyaoshi, Renhe Pharmacy Online, and Kede Wang, while those listed on the National Equities Exchange and Quotations (NEEQ) include Quanyuantang and Kangzhijia.

It is evident that listed pharmaceutical e-commerce companies hold a significant share of the market. The underlying reason is that the pharmaceutical e-commerce sector remains heavily resource-dependent. For instance, obtaining approval for an online pharmacy requires first securing an Internet Drug Information Service Qualification Certificate, followed by an Internet Drug Transaction Service Qualification Certificate based on an existing offline chain infrastructure. This regulatory framework gives companies with established chain operations a distinct advantage in entering the market. Furthermore, leveraging pharmaceutical supply chain resources and industry marketing capabilities demands experienced professionals with deep industry expertise. Consequently, early participants in the pharmaceutical e-commerce industry were predominantly those with traditional pharmaceutical backgrounds.

However, it should also be noted thatNon-listed companies and those with an internet DNA account for a significant proportion of the pharmaceutical e-commerce industry, such as Jianke, 111.com.cn, Qilekang, Yun Kai Ya Mei, 360 Hao Yao, and Ba Bai Fang.These companies, among others, have entered the pharmaceutical e-commerce sector with internet-driven philosophies, introducing new approaches to technology, operations, and marketing within the industry.

Overall, the competitive landscape of the pharmaceutical e-commerce market has gradually become clear, with a tier of leading enterprises emerging. A group of companies possessing strong capabilities, abundant resources, and deep market understanding have established their brands and secured corresponding market shares. However, the pharmaceutical e-commerce market remains subject to many variables, including policy changes, technological innovations, and business model innovations.

First, from a policy perspective, the online sale of prescription drugs has remained restricted, forcing e-commerce platforms to navigate this space tentatively. Once clear regulatory red lines are established, many companies’ operations will be significantly impacted. Even though the recently issued “Internet + Healthcare” policy has eased certain regulatory constraints, it has not crossed the fundamental regulatory red lines; what is encouraged remains models that have an offline foundation and can establish robust connections with hospitals.

In terms of medication safety,, prescription drugs will remain subject to sales restrictions online for a certain period, which will impose a ceiling on the business expansion of pharmaceutical e-commerce., constraining industry expansion.

Secondly, from the perspective of technological innovation, the core competency of e-commerce lies in enhancing supply chain efficiency to serve a larger user base at lower costs.

When e-commerce served as a growth channel, it was able to maintain strong relationships with industrial enterprises. However, as the market matures and efficiency gains hit a ceiling, the cost savings achieved through supply chain optimization can no longer cover expansion costs. This leads to reduced willingness among industrial enterprises and supply chain participants to engage, or results in exclusive cooperation models, which undoubtedly causes some pharmaceutical e-commerce platforms to lose supply chain support.

Therefore, the pharmaceutical e-commerce model requires innovation; indeed, we have also observed pharmaceutical e-commerce companies engaging in business model innovation.

For instance, companies are adopting the “pharmaceuticals + healthcare” model by collaborating with internet hospitals, acquiring hospitals, and launching mobile health apps. This approach addresses the source of prescriptions for pharmaceutical e-commerce platforms while enhancing user stickiness and effectively “capturing” users. Another strategy involves operating a hybrid business model that integrates B2B, B2C, and O2O formats to create a closed-loop ecosystem. Additionally, some players are expanding into niche markets, deepening their service offerings, and exploring synergies with insurance and health management services.

No market is static; the essence of business lies in change. Pharmaceutical e-commerce has exerted a profound impact on drug distribution and the retail sector. As policies such as the “Two-Invoice System” and the separation of prescribing from dispensing continue to be implemented, pharmaceutical e-commerce will play an increasingly vital role in drug distribution and shape national health consumption habits. Throughout its development, innovation will be the key to breaking through competitive barriers.