Orphan Drug Market Surge: Unveiling the Strategic Roadmaps of Domestic and Global Pharma Companies

2017In [Year], the global rare disease drug market totaled703USD 100 million.VCFunding allocated to the rare disease sector has also been increasing year by year.

Although rare diseases affect a small population, they represent a major business opportunity. Gleevec, the drug that inspired the film “Dying to Survive,” was initially approved as an orphan drug and ultimately achieved peak annual sales approaching50Billion-Dollar Super "Blockbuster"”。

In the United States, orphan drugs have served as a breeding ground for “blockbuster” medicines, with some even becoming pillars of pharmaceutical giants. However, no such examples have yet emerged in the Chinese market. Nevertheless, as supportive policies continue to be introduced, an increasing number of pharmaceutical companies are recognizing the vast potential of this market.

How are domestic and international companies strategizing and competing in the vibrant orphan drug market?

In response, VCBeat has conducted follow-up reporting to uncover its roadmap for profit generation.

The World Health Organization (WHO) defines rare diseases as those affecting 0.65% to 1% of the population. In the United States, a rare disease is defined as one that affects fewer than 200,000 people annually (or has a prevalence of less than 1 in 5,000). Regardless of the calculation method used, given China’s large population base, the community of patients with rare diseases is by no means a minority.

However, the rare disease community is like the “elephant in the room.” Currently, there are 621 orphan drugs approved for marketing by the U.S. Food and Drug Administration (FDA), whereas only 282 have been approved by the China Food and Drug Administration (CFDA) for entry into the Chinese market, and they come with hefty price tags. Behind these cold numbers lie stark and painful realities.

At the 7th Rare Disease Summit in 2018, Liu Jinzhu, Director of the Beijing Tuberous Sclerosis Complex Care Center, stated that during the period when no treatments were available for tuberous sclerosis complex in China, they attempted to import medications from abroad; however, three children lost their lives due to delays in receiving timely treatment.

“Time lag” is somewhat of a blessing for patients with rare diseases, as the majority still face the reality of having no available treatments. Currently, more than 7,000 rare diseases are known worldwide, yet only 5% have effective therapies. In China, that figure stands at merely 1%.

Although the population of patients with rare diseases is relatively small, the market size for rare disease medications is substantial. In 2017, the global market for rare disease drugs reached $70.3 billion, with an annual growth rate of 11%, significantly higher than the 5.3% growth rate for prescription drugs overall. By 2024, sales of orphan drugs are projected to reach $262 billion, accounting for one-fifth of global prescription drug sales.

Pharmaceutical companies’ willingness to engage in the seemingly unprofitable business of rare diseases was initially driven not by altruism, but by a combination of policy incentives. Abroad, “orphan drugs” enjoy significant policy advantages. As early as 1983, the United States enacted the Orphan Drug Act, granting orphan drugs a 50% tax credit and waiver of user fees to subsidize pharmaceutical companies’ investments in clinical trials and development. Furthermore, once an orphan drug is approved, it benefits from seven years of market exclusivity. Most importantly, regarding payment for rare disease treatments, commercial insurance covers the high costs of these medications, amounting to $300,000–$450,000 per patient annually.

To this day, the policy benefits for orphan drugs in the United States continue to be realized. Amid increasingly stringent FDA approval standards for new drugs, the FDA has provided greater flexibility for the marketing approval of orphan drugs. According to FDA statistics, 77 rare disease drugs were approved for marketing in 2017, achieving a 100% approval rate.

Despite their high pricing and relatively small patient populations, certain rare-disease drugs have achieved “blockbuster” status. According to the Drugs to Watch 2018 report, Hemlibra®, recently approved by the U.S. Food and Drug Administration (FDA) for the treatment of hemophilia A, is projected to reach blockbuster level in 2019, with estimated annual sales of $1.457 billion.

Global multinational pharmaceutical companies are increasingly expanding their presence in the rare disease drug market, with a level of commitment to rare disease drug development that rivals their focus on oncology and immunology therapies. For instance, Japan’s Takeda Pharmaceutical acquired Shire, a leader in the rare disease sector, to bolster its rare disease drug pipeline.

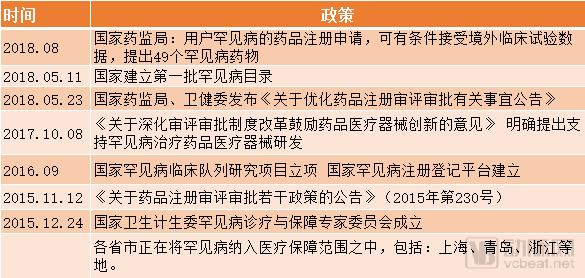

A Comparison of “Orphan Drug” Policies in China and Abroad

Following international development models, policy incentives serve as a catalyst for the growth of the orphan drug market. In China, although policies were initially absent, they are now being progressively introduced and implemented.

Overview of Rare Disease Policies in China:

As shown in the table, policy support has begun to fill the gaps. It is expected that more detailed implementation rules and continuous policy follow-ups will be introduced in the future. Compared with the environment created abroad for rare disease treatment, there is still a significant void in China. The most critical issue is that while the high costs of orphan drugs are covered by commercial insurance in other countries, it remains uncertain what proportion of rare disease treatment costs can be borne by China’s basic medical insurance system.

Differences in policy environments between China and other countries merely constitute a threshold, whereas the disparity in R&D capabilities between domestic and foreign enterprises represents the true barrier. Among the 39 drugs currently granted priority review status in China, 20 are from local pharmaceutical companies and research institutions, with the remainder primarily originating from foreign companies such as Bayer and Roche.

Domestic pharmaceutical companies may be able to surpass multinational corporations by leveraging their advantages in innovative drugs, whether by bringing a new era of hope for rare diseases through standout innovative therapies or by pooling diverse strengths to advance precision medicine in the treatment of rare diseases.

The leapfrog development achieved by domestic pharmaceutical companies in orphan drugs is primarily driven by an overall enhancement in their capabilities. It is well known that in recent years, numerous pharmaceutical professionals have embarked on innovative drug entrepreneurship, with many possessing experience at multinational pharmaceutical companies and core technologies. Approximately one-quarter to one-third of these returning overseas talents (“sea turtles”) come from the pharmaceutical sector. In 2008, the China Food and Drug Administration (CFDA) was reviewing only around 10 Class 1.1 new drugs; today, the number of Class 1.1 new drugs under review exceeds 50. These returning overseas experts have not limited their strategic focus to generic drugs; instead, they have placed significant emphasis on developing pipelines for rare diseases.

Yi’an Jishi Biopharma, founded by Dr. Zhao Yining, a former Pfizer executive, has a research and development pipeline covering oncology, genetic rare diseases, and metabolic disorders. Notably, the company is developing therapies for rare conditions such as hemophilia and Prader-Willi syndrome. Yi’an Jishi Biopharma’s competitive advantage lies not only in its “robust” R&D pipeline for rare diseases but also in Dr. Zhao’s broader portfolio, which includes Yizhen Bio and Yijing Bio. The extensive genetic testing data accumulated by Yizhen Bio can facilitate the targeted development of innovative biologics.

Canhelp Genomics is also a domestic innovative pharmaceutical company in China focused on the research and development of drugs for rare diseases. Its founder, Xue Qun, was the first General Manager of Sanofi Genzyme’s China region. Genzyme was primarily responsible for Sanofi’s specialty drug businesses in developed markets, covering rare diseases, oncology, and immunology. Currently, Canhelp Genomics’ development strategy is transitioning from an oncology-focused portfolio to a dual-platform model encompassing both “oncology drugs + rare disease drugs.”

In 2017, Canaan Healthcare officially announced the establishment of a platform dedicated to the development of rare disease therapeutics. The platform will focus on introducing a portfolio of rare disease drugs that are already marketed abroad or in late-stage clinical trials, creating synergistic effects to provide payers with more cost-effective solutions and thereby stimulating and advancing China’s rare disease market.

Domestic innovative pharmaceutical companies are highly optimistic about orphan drug development. Shanghai Zhongqiang Pharmaceutical’s pipeline is divided into three categories: prostaglandins, orphan drugs, and anti-hepatitis C agents. The founding team of Zhongqiang Pharmaceutical primarily comes from Roche, with its founder, Dr. Ren Yi, previously serving as Senior Director at Roche’s China R&D Center.

In addition to returnee-led enterprises, domestic pharmaceutical giants are also making inroads into the rare disease sector. Xu Tian, Chief Scientific Advisor at Fosun Pharma, has stated that the company’s technology innovation incubation platform is currently prioritizing investments in oncology diagnostics and precision medicine, AI applications, and rare disease research.

Another significant resource that domestic pharmaceutical companies can leverage is China’s specialized rare disease organizations. At the 7th China Rare Disease Summit, Gu Hongfei, founder of the patient advocacy groups “Lymphoma Home” and “Multiple Sclerosis Home,” shared a case study: “PD-1 clinical trials have recently garnered considerable attention. Many domestic companies are pursuing lung cancer indications; however, given the large lung cancer patient population, completing clinical studies requires substantial investment. In contrast, certain rare tumors, such as lymphoma, have low incidence rates. Companies that choose to focus on these indications can often achieve rapid progress, addressing an urgent unmet clinical need. Ultimately, we assisted the company in enrolling 40 patients, and the trial was completed in less than six months. They promptly submitted their marketing application, astonishing foreign pharmaceutical firms by accelerating to a pace comparable to Phase III clinical trials.”

Certainly, the efforts of domestic pharmaceutical companies in generic drugs can also enable more patients with rare diseases to access medications. For example, among the newly approved drugs is melphalan from Yibang Dongli.

Ninety percent of rare diseases are genetic disorders, and 80% of patients are children. In China, only 1% of rare diseases have effective treatments. This means that some patients with rare diseases are effectively sentenced to death at birth. With the relaxation of the two-child policy and rising health demands, eliminating the fatal threat posed by rare diseases has become an urgent necessity. Genetic testing plays a crucial role in advancing the treatment of rare diseases, both in research-grade new drug development and disease diagnosis, as well as in clinical applications for reproductive health and genetic disorder screening.

Some rare diseases may affect only a handful of patients worldwide, yet genetic testing ends their anonymity by enabling the discovery and diagnosis of more conditions.

At the 7th Rare Disease Summit, Sun Jun, Technical Director of BGI’s Reproductive Health Division, pointed out: “In 2016, there were 18.46 million live births in China, with 1.03 million infants born with birth defects, representing a rate of 5.6%. The overall incidence of monogenic disorders was 1%, and effective pharmacological treatments are lacking. It is well established that birth defects result from the combined effects of genetic and environmental factors. Genetic factors encompass structural malformations, chromosomal disorders, monogenic diseases, polygenic diseases, and multifactorial genetic conditions.”

For chromosomal disorders, genetic testing methods can largely facilitate non-invasive prenatal testing. Structural chromosomal abnormalities mainly consist of microdeletions and microduplications, numbering approximately 200 types. Among these, BGI Genomics can detect around 100 types with established clinical associations.

Polygenic diseases, due to their unclear causal relationships, currently lack a particularly suitable testing method. In contrast, monogenic genetic disorders exhibit a clear association between phenotypes and anomalies, enabling highly effective prevention and control.

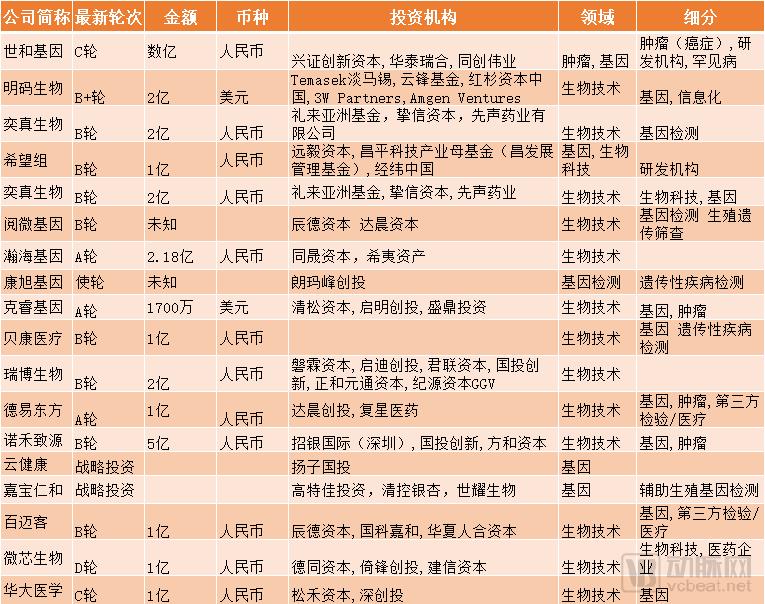

Multiple companies, including BGI Genomics, Berry Genomics, and Mingma Bio, are also positioning themselves in the field of genetic testing for rare diseases.

Overview of Genetic Testing Companies Focusing on Rare Diseases | Data Source: VCBeat Knowledge Base

Rare Diseases: 80% Are Genetic Disorders. In the field of genetic diseases, gene therapy holds broad application prospects. China’s scientific research capabilities in gene therapy are at a world-leading level, making it another niche sector poised for leapfrog development beyond cell therapy. Clinical research activities in gene therapy are expected to be unprecedentedly active. Currently, there is also a large number of startups providing solutions for genetic testing of rare diseases.

There are still many barriers to overcome for the true application of genetic testing in rare diseases. Currently, apart from non-invasive prenatal screening (NIPS), which has largely reached maturity, other clinical-grade genetic testing products—such as those for tumor diagnosis and treatment, and genetic disease diagnosis—are still in pilot phases and require the establishment of more comprehensive industry standards. The substantial need for professional data interpretation and analysis demands specialized talent, for whom there remains a significant shortage in the Chinese market. It is essential to establish training and educational pathways and systems.

Yuan Jianzhong, Senior Vice President and General Manager of China Region at WuXi NextCODE, stated to VCBeat: “Currently, there is little difference between domestic and international genetic testing technologies; however, products lack standardization, interpretation has not yet achieved consistency, and further talent development is required.”

Sun Jun of BGI Group also pointed out, “As everyone knows, the cost of sequencing is decreasing. This has led to a phenomenon that I believe needs to be controlled. The prevailing belief that ‘the more extensive and comprehensive the testing, the better’ is an issue that requires joint reflection by clinical practitioners and testing institutions. While performing the tests is straightforward, the critical questions to consider are how to provide follow-up counseling and how to apply the results effectively, so that individuals undergoing testing can truly benefit.”

At the 7th China Rare Disease Summit, Professor Ding Jie, a professor at Peking University First Hospital and Deputy Director of the National Health Commission’s Expert Committee on Diagnosis, Treatment, and Security for Rare Diseases, stated, “Although there are still many gaps in the treatment of rare diseases, and regulatory and payment policies require further alignment, the introduction of the national rare disease catalog marks the beginning of our progress.”

Except forIn addition to prioritizing the research and development of drugs for rare diseases, pharmaceutical companiesRare disease patient organizations are growing increasingly powerful, leveraging their influence to participate in the research, development, and approval of new drugs. This trend is beneficial for both the market and patients with rare diseases.