Amazon's Comprehensive Healthcare Ambition: Reshaping the Medical Ecosystem Through Technology, Logistics, and Consumer-Centric Innovation

Amazon aspires to dominate more than just online retail; the e-commerce giant has been striving to transform the healthcare ecosystem by leveraging its strengths and expertise to disrupt every segment of the industry, from pharmaceutical supply chains to health insurance management. By introducing unconventional business models, logistics, and information technology infrastructure, Amazon aims to enhance customer satisfaction in the healthcare sector.

From 1999 to 2000, Amazon invested in Drugstore.com, aiming to expand its e-commerce operations into the pharmacy sector. However, its ambitions were ultimately halted due to challenges involving intermediaries and regulatory agencies.

In early 2018, Amazon announced a partnership with JPMorgan Chase and Berkshire Hathaway to establish a joint venture focused on healthcare. Prior to this, Amazon had acquired the online pharmacy PillPack for nearly $1 billion.

However, Amazon is not the only tech company leveraging its strengths to expand into the healthcare sector. For instance, Google has applied artificial intelligence to medical devices and lifestyle management, while Microsoft is building health data management capabilities on its Azure cloud platform.

As Amazon, the e-commerce giant, ventures into the healthcare industry, many questions have arisen:

• What strategy does the company plan to adopt to enter new vertical sectors, particularly those with established market leaders?

• If Amazon enters the healthcare sector, which companies will be most affected? What business models will become obsolete?

• Will the advantages Amazon has already demonstrated in sectors such as retail continue to manifest in the healthcare sector?

• Is the timing right? What factors could enable Amazon to succeed in the healthcare sector?

VCBeat (WeChat: vbbeat) has translated a report by CB Insights. Leveraging data from CB Insights, we will gain an in-depth understanding of how Amazon is leveraging its current strategy to expand across sectors into the healthcare industry.

Amazon’s Healthcare Advantages: Customers, Employees, Capital, and Brand

As Amazon enters the healthcare industry for the second time, it brings some new advantages.

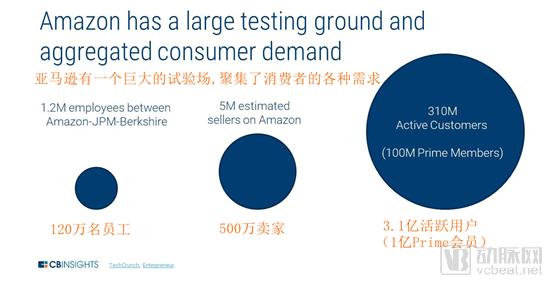

Amazon’s current scale and reach are unprecedented. With direct distribution advantages encompassing over 300 million active customers, 100 million Prime members, and nearly 5 million sellers, the company is well-positioned to develop health solutions for small businesses.

By partnering with JPMorgan and Berkshire Hathaway, Amazon currently has more than 1.2 million employees—spanning diverse socioeconomic backgrounds, geographic locations, and age groups—who test its products before they are released to the public.

This is helpful for identifying solutions that are applicable to both specific use cases (such as chronic disease management) and population-level needs (such as medication delivery).

Amazon’s ecosystem also provides it with greater capital for deployment, which is why it can bear the risk of low profit margins. As announced in its partnership with JPMorgan and Berkshire Hathaway, Amazon aims to establish an independent healthcare company “not just for profit.”

Amazon can generate revenue by expanding its core businesses, such as AWS and Prime, while entering the healthcare industry. As other business segments become increasingly valuable, Amazon has chosen not to prioritize short-term profits.

Existing healthcare giants will find it difficult to compete with a company that does not aim to generate profits in the healthcare sector.

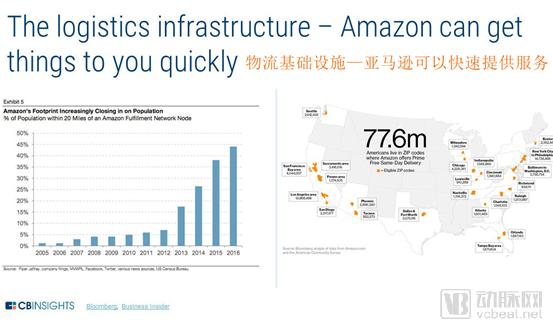

However, Amazon has been employing this strategy for decades. It has invested its revenue in large-scale infrastructure construction for logistics and data center space, which will be a significant advantage as it enters the healthcare sector.

For example, Amazon Web Services (AWS) can help handle the massive data storage and analysis required in the healthcare sector.

Amazon’s fulfillment centers, supply chain, and acquisition of Whole Foods all indicate its ability to rapidly deliver healthcare products and services.

Amazon’s final key advantage is its brand.

Customer experience is treated as an afterthought in nearly every aspect of healthcare, a reality reflected in Net Promoter Score (NPS) ratings (which are correlated with customer satisfaction).

Amazon may leverage its focus on the consumer experience to persuade customers to adopt its products. The question now is whether Amazon can introduce the “consumer-first” brand concept into the healthcare industry more rapidly than existing healthcare companies.

Amazon's Strategy: Focusing on Customer Experience and Standardization

As Amazon enters new territories, it adheres to the following strategy:

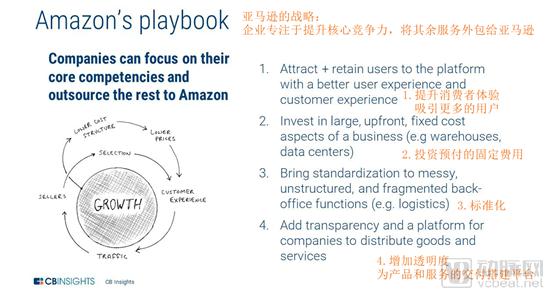

First, Amazon launched a customer-friendly product with superior user and customer experiences compared to its competitors. This enabled Amazon to achieve economies of scale, network effects, and enhanced bargaining power with other parties, such as suppliers.

Second, Amazon invests in prepaid fixed costs to optimize their utilization and offer outsourced services to customers. This is evident in Amazon Fulfillment by Amazon (FBA) and Amazon Web Services (AWS), both of which enable businesses to access traditionally expensive resources—such as warehouses and data centers—through a “lease-before-buy” model.

By attracting a sufficient number of users to its platform and offering its own fulfillment services, Amazon can standardize suppliers’ products on its marketplace. This enables it to create a transparent and competitive market for both buyers and suppliers.

Hiring Atul Gawande to lead its healthcare joint venture with JPM and Berkshire is also a continuation of Amazon’s strategy.

Gawande focuses on leveraging standardization as a means to scale healthcare operations, particularly for relatively commoditized products and services.

The lack of standardization and focus on consumer experience has led to a highly fragmented and opaque healthcare market, making the following stakeholders and sectors particularly vulnerable in the face of Amazon’s entry into healthcare:

• Intermediaries: They are value extractors, earning substantial profits

• Companies focused on formatting or coordinating information

• Customer experience is an area treated as an afterthought

• Companies that adopt opaque pricing as a business model

We will delve into the healthcare sectors where Amazon is poised to leverage its e-commerce dominance for strategic expansion.

Acquire PillPack to improve patient experience.

The U.S. pharmaceutical supply chain is intricate, rife with various intermediaries and convoluted business models.

For example, more than three entities are involved in the process of delivering drugs from manufacturers to patients, with each party obtaining a certain share of the profits.

Amazon has the opportunity to streamline the supply chain and improve the experience or cost issues for patients, payers, and manufacturers.

The company acquired the online pharmacy PillPack for $1 billion, marking a significant advancement in the pharmaceutical distribution sector. Through this acquisition, Amazon expanded its $100 million business to provide medication supplies across all 50 states.

PillPack aligns perfectly with Amazon’s philosophy. The company is highly favored by customers, boasting a Net Promoter Score (NPS) of 80, compared to the pharmacy industry average of 26. This strong focus on customer experience embodies the Amazon spirit.

Furthermore, PillPack’s prescription drug management platform, pharmacyOS, is highly similar to Amazon’s order management and fulfillment services.

PillPack will handle medication dispensing, monitoring, and support through pharmacyOS. It also delivers these services to payers, manufacturers, and new companies via a delivery interface. This can be well integrated with Amazon’s existing distribution model.

Starting with pharmacy benefit management (PBM) to provide end-to-end solutions.

In 2017, more than 250 million prescriptions were paid for in cash. Amazon can offer lower prices to patients who pay for their medications through PillPack in cash, thereby accumulating capital.

This is an effective way to test product pricing, as cash prices vary significantly across different pharmacies. In some cases, these prices may even be lower than those offered by health insurers, which could prompt insured individuals to check Amazon for price comparisons first.

In addition to patients paying in cash, Amazon also needs to invest in a more expensive pharmaceutical supply chain.

Logically, the next step should be to enhance PillPack’s online pharmacy to enable same-day prescription dispensing. Amazon could achieve this by establishing a retail pharmacy and/or point-of-sale locations within Whole Foods, or by partnering with independent pharmacies in regions where its business presence is less robust.

Once Amazon establishes a drug delivery system targeting end patients, it can replace traditional pharmacy benefit managers (PBMs) and provide pharmaceutical benefits to payers.

The benefits of this approach include establishing a pharmacy network for patients, negotiating drug prices on behalf of small health plans and self-insured employers, and monitoring anomalies in patients’ medication use (such as poor medication adherence).

Relevant companies are seeking alternatives to the existing Pharmacy Benefit Manager (PBM) model. A survey conducted by the National Pharmaceutical Council among 88 large enterprises revealed that only 30% of respondents understood the contracts they had signed with PBMs, while nearly 70% expressed a desire to change this discount-driven business model.

Cigna’s acquisition of Express Scripts means that smaller health plans competing with Cigna may also consider seeking alternatives to pharmacy benefit managers (PBMs). Amazon can replace PBMs and provide the same services to both groups, while generating little to no profit from this activity, as Amazon does not need to rely on this channel alone for revenue.

However, to succeed in this project, Amazon needs to negotiate prices through partnerships with pharmaceutical manufacturers, as it can also provide services to them.

By 2023, in accordance with the provisions of the Drug Supply Chain Security Act (DSCSA), every entity within the pharmaceutical supply chain must become part of an interoperable tracking system, and each individual unit (such as a medicine bottle) must be traceable from end to end.

Amazon has applied for a wholesale pharmacy license. Combined with the licenses acquired through its purchase of PillPack, it only needs a manufacturing license to complete end-to-end drug delivery.

This will enable Amazon to handle products directly from manufacturers, relabeling them or breaking them down into different units as needed. UPS already holds its own manufacturing license and appears capable of managing the entire process.

With all the necessary licenses and logistics infrastructure in place, Amazon can effectively operate an outsourced fulfillment system for pharmaceutical companies akin to its Fulfillment by Amazon (FBA) service, while handling all traceability requirements mandated by the Drug Supply Chain Security Act (DSCSA).

However, a critical component is missing—cold chain or temperature-controlled logistics solutions—which Amazon requires to ship any pharmaceuticals with specific environmental requirements. Amazon could start with products that are easy to transport, and once it enters the pharmaceutical manufacturers’ market, it can ultimately expand into the broader healthcare sector.

Delve into Claims Management to Enhance Healthcare Efficiency.

Only by providing pharmaceutical benefits to employers can the healthcare challenges they face be resolved.

To improve efficiency, Amazon could also become a platform for health benefits management—meaning it would need to delve deeply into the areas of claims management and billing.

The current system comprises multiple components, including manual data entry/cleaning and third-party intermediaries. This process is also slow—relevant laws have been enacted to prevent the claims and reimbursement process from taking more than 30–45 days.

Claims management impacts the payment backend of the entire healthcare system.

New insurance solutions such as Oscar and Collective Health consider the claims processing workflow outdated and inefficient. Consequently, many emerging technology companies have invested substantial resources in building their own claims management systems and infrastructure, using this as a foundational starting point.

Amazon is poised to offer payers its own solution to this issue. While there are already clear use cases for health management, this also represents a way for Amazon to begin assuming certain claims management functions, such as detecting inaccuracies at the time of submission.

It is reported that this project has undergone more than three years of development and is currently being used in commercial health plans.

Provide platforms and products to drive the benefits management market.

Claims management software may become a “white-label” solution, offering employers an advantageous opportunity to address benefits administration.

If Amazon can standardize and build a back-end system for claims payment and management, this technology could drive the emergence of a benefits market, allowing service providers such as pharmacies, health care companies, and primary care physicians (PCPs) to outsource their claims processing to Amazon.

Amazon can then provide a platform for employers or small health plans, creating a distribution channel for other healthcare services. This incentivizes both sides of the market to partner with Amazon, leveraging its backend services and frontend platform.

Amazon can also offer self-insured employers a common product, typically purchased alongside benefits management services: stop-loss insurance. This is an insurance product that self-insured employers use to guard against catastrophic scenarios.

Berkshire’s specialized insurance subsidiary has been offering this product since 2016, an advantage that Amazon can leverage. This is similar to Collective Health, which is partnering with Sun Life Financial to provide stop-loss insurance.

Why Choose the Medicare/Medicaid Population?

Across multiple settings with various patient touchpoints (home, grocery stores, online, etc.), Amazon can become a lifestyle manager for Medicaid and Medicare populations.

The United States has over 52 million Medicare beneficiaries, more than 71 million Medicaid beneficiaries, and over 10 million dual eligibles.

In 2017, Medicare and Medicaid expenditures exceeded $1.3 trillion, with the majority concentrated among the top 10% of patients with severe illnesses. Many of these patients suffer from chronic diseases or mental health conditions and require daily lifestyle management. This population is most likely to become Amazon Prime members.

Amazon’s penetration rate is significantly lower among individuals with an annual income below $68,000 compared to other income brackets. Furthermore, Amazon has far fewer Prime members aged 55 and older than competitors such as Walmart.

As the U.S. Centers for Medicare & Medicaid Services (CMS) drafts proposals to expand Medicare coverage, Amazon is poised to enter the healthcare sector at a particularly opportune moment.

Amazon is closely monitoring primary care and seeks to expand its definition to include social determinants of health such as transportation, diet, and home services. It also plans to propose new reimbursement rules aimed at covering telehealth services for Medicare beneficiaries.

Amazon can leverage these evolving health insurance regulations to attract more people to become Prime members by offering attractive incentives.

It was reported that Amazon held negotiations with the American Association of Retired Persons (AARP) early this year, aiming to identify products and solutions for its members.

Meeting Special Needs to Promote Fresh Food Business.

Amazon now offers discounted memberships to Medicaid beneficiaries, although this benefit has not yet extended to Amazon Fresh or Prime Pantry. This could change in the future—we may even be able to use SNAP (Supplemental Nutrition Assistance Program) benefits directly on the website.

Amazon’s strengths in the food and grocery sector could, in fact, drive its net fresh-food business.

Offering fresh food products tailored to specific diseases will bring significant benefits, especially for those who have difficulty accessing fresh produce. According to a recent study in Health Affairs, meals customized for dual-eligible beneficiaries can reduce adverse health events. If Amazon wants its fresh food service to stand out, addressing the health needs of Medicaid and Medicare populations will be a viable strategy.

Leveraging Smart Home Technology to Advance Home Care.

Amazon can also adopt a similar strategy for smart homes, as every tech giant is fiercely competing for market share in the smart home sector. While Amazon may hold a larger market share, its competitors are catching up.

Amazon can apply its smart home technology to the healthcare sector, leveraging its first-mover advantage to stand out.

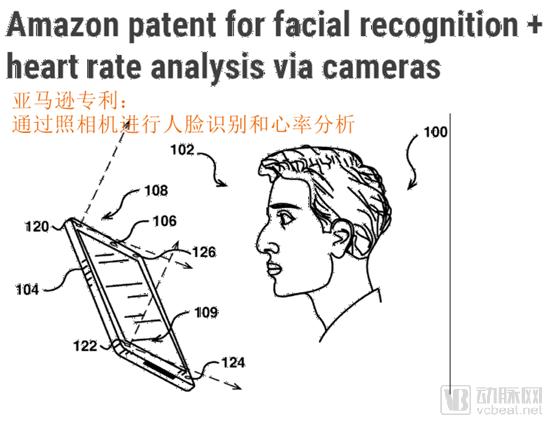

Amazon’s Echo is a voice-controlled speaker with video capabilities, making it well-suited for monitoring, particularly in home settings. However, to handle medical-related data, it must be HIPAA-compliant.

In accordance with HIPAA requirements, the company can pursue multiple strategic directions. Echo can be utilized to monitor compliance and provide medication reminders. Amazon also holds patents for using cameras to monitor blood flow and heart rate, which could be extended to fall detection or gait analysis.

Echo can also serve as a service hub for telemedicine and digital health companies, coaches, and others, helping to manage Medicaid and Medicare beneficiaries. Amazon is already considering developing an ecosystem for third-party medical applications on Alexa.

It funded the Alexa Diabetes Challenge. The Alexa app platform features lightweight medical applications from institutions such as Mayo Clinic and Libertana, which can answer medical questions, send alerts in emergencies, and help users communicate with caregivers.

Amazon can handle HIPAA-compliant and voice technology backend processes, while providing platforms and distribution channels for enterprises through Alexa and Echo.

Establish offline brick-and-mortar clinics.

Amazon can also bring healthcare into the real world and establish its own clinics.

The company recently hired Martin Levine, the former medical director of Iora Health in Seattle. Iora is dedicated to establishing clinics and providing primary care services for Medicare beneficiaries.

For Amazon, establishing clinics within Whole Foods stores is a swift strategy, as the company already operates a retail presence there. In an interview with Bloomberg, Whole Foods CEO John Mackey stated, “The second idea is more ambitious: to establish a Whole Foods medical clinic.”

He was inspired by Rosen Care, the employer-sponsored healthcare program of Orlando-based Rosen Hotels & Resorts, which provides medical facilities for its employees. The clinic employs 38 healthcare professionals and serves 5,300 employees, with a focus on nutrition and preventive medicine. Harris Rosen, the company’s founder, stated that the company has reduced per-employee healthcare costs to approximately half the national average. Last summer, Mackey met Rosen at a healthcare conference in Las Vegas and subsequently visited the clinic in Florida. He is considering establishing a Whole Foods clinic for his employees, with potential future expansion to serve customers as well.

Amazon can test and refine its clinic concept within Whole Foods stores, then establish additional clinics in areas with a higher concentration of Medicare/Medicaid beneficiaries. This approach is similar to that of companies such as Cityblock Health or Oak Street Health.

Reverse Integration Strategy to Alleviate Management Burden.

Amazon is also exploring management approaches that are useful for existing physicians, hospitals, and suppliers. Over the past few decades, the healthcare industry has hired more people for administrative roles, many of which involve coordinating information among different parties and handling data entry/cleaning.

Certain regulations mandate extensive monitoring and oversight of services, leading to an increase in administrative workload.

Many healthcare institutions prefer hiring more staff rather than investing in modern technological systems as a solution. This is because upfront costs are lower, implementation is faster, and adjusting staffing levels is easier when regulatory requirements change.

Amazon has the opportunity to alleviate the burden on users and build a new backend for providers. For Amazon, it makes more sense to adopt a reverse integration strategy rather than attempting to disrupt existing processes.

By providing a more intuitive layer on top of existing systems and processes, Amazon can attract more users to its user interface and gradually replace manual backend processes.

Leverage voice functionality to achieve efficient data entry.

It is reported that Amazon is researching how to input and extract data from electronic health records (EHRs). Voice technology is an increasingly popular feature, particularly well-suited for the healthcare sector. Hospitals are already exploring voice-based applications.

Premier Health, which operates five hospitals and two large medical centers, spent $1.6 million to develop voice recognition software integrated with Epic. The system helps alleviate physicians’ workload, saving approximately 90 minutes per day. Thanks to more efficient workflows, the software has enabled Premier Health to reduce medical costs by about $1.3 million.

Alexa is undergoing trials at hospitals across the country, including Northwell, Mass General, and Boston Children's Hospital.

However, because Alexa is not yet HIPAA-compliant, the tasks performed by this software are generally limited to non-identifiable uses, such as surgical checklists, patient disease and medication information, and hospital information.

If Alexa were HIPAA-compliant, use cases could be further expanded.

Most physicians find current electronic medical records (EMRs) inefficient and time-consuming, as they require healthcare professionals to manually document information. Alexa can be integrated into EMR systems to serve as a passive scribe.

Alexa can help Amazon transition from an EMR middleware to a full-fledged EMR.

Several startups have incorporated this strategy as they entered the voice technology sector. Products like Dragon Medical have been on the market for some time, while newer companies such as Suki, Notable, and Saykara have recently raised additional funding, making them potential acquisition targets.

Simplify the supply chain to reduce costs.

As in the pharmaceutical industry, the supply chain is currently intricate and replete with various intermediaries. Manufacturers engage in transactions with distributors, who in turn deal with Group Purchasing Organizations (GPOs) that negotiate on behalf of hospitals to reduce the costs of drugs and technologies (although hospitals sometimes negotiate directly).

Aside from labor costs, the supply chain represents the second-largest expense for hospitals, and this cost is projected to continue rising in the near future.

Amazon has already offered some services in this area: its B2B division has a healthcare branch that mainly handles low-risk products (partly because it has not yet established cold-chain logistics capabilities).

Since Amazon does not yet offer a full suite of services, hospitals can partner with existing distributors that are capable of meeting all their needs and already have established processes in place. Many hospitals hold equity stakes in Group Purchasing Organizations (GPOs), which further diminishes their incentive to transition to new systems.

Amazon will find it difficult to immediately save costs for its customers. Steven Corwin, CEO of New York Presbyterian, mentioned in a recent interview that the company is unable to offer better prices to hospitals.

But the metrics for success are changing. Chris Holt, head of Amazon’s B2B supply division, discussed in an interview with HealthcareDive how to reduce labor costs, create better interfaces, and build technology that can be integrated backward into existing systems and processes.

Amazon is selling products that enhance efficiency and integrate with backend systems to attract more users to its platform. This can also draw in more suppliers, who may offer better deals, helping Amazon strengthen its marketplace capabilities.

Amazon will gradually replace more of its backend ordering processes and may secure better deals than those offered by existing GPOs.

Amazon can also focus its pharmaceutical strategy on the consumer side, handling post-diagnosis delivery and communication between doctors and patients.

The company recently announced a partnership with Xealth, enabling physicians to order medical supplies on behalf of patients. Xealth also provides doctors with digital health solutions, such as diabetes management programs and disease-specific content or treatment protocols.

AWS: Focus on Genomics.

Amazon’s existing AWS (Amazon Web Services) infrastructure is critical to the success of many healthcare initiatives. As more tech giants attempt to expand their cloud platforms, this has become a competitive arena.

Every tech giant views healthcare as a high-growth segment for cloud services, given its capacity to generate vast amounts of data and the need for high-performance computing to interpret it.

Amazon has offered several AWS solutions to existing healthcare companies, particularly in the areas of security and compliance.

This has remained a hot topic, as 2017 saw large-scale hacker breaches of datasets containing identifiable information—including Social Security numbers and other personally identifiable information—and several hospitals became targets of ransomware attacks.

As data security becomes a concern in cloud migration, these attacks have exposed the vulnerabilities of on-premises storage, which could present an opportunity for companies aspiring to become healthcare giants.

By providing tailored solutions to various entities in the healthcare sector, Amazon can capture a larger share of the medical cloud market. Several of the aforementioned initiatives may have been launched by AWS, including claims management, patient monitoring, electronic health records (EHR), and supply chain management software.

AWS places significant emphasis on genomics, a field that is becoming increasingly important to payers, providers, researchers, and other stakeholders. Driven by declining sequencing costs and expanded screening and clinical applications (such as tumor profiling), the demand for computational power and storage capacity to analyze these datasets has correspondingly increased.

Amazon participated in GRAIL’s Series B financing round of over $900 million, signaling its doubled-down investment in this field.

GRAIL is attempting to enable early cancer diagnosis by monitoring tumor DNA in the blood. The company has provided Amazon with extensive genomic data and sophisticated analytical tools, along with a case study that could help attract more customers.

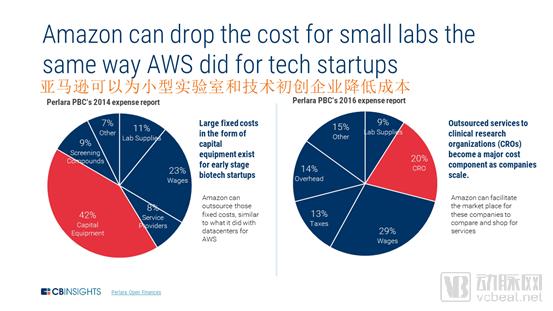

Expand laboratory business through outsourcing services.

Amazon will expand its laboratory operations through AWS. It has already provided several AWS solutions to pharmaceutical and biotechnology companies and may broaden its service offerings—particularly targeting the early stages of laboratories and biotech firms.

Many laboratories and small biotechnology companies face high upfront costs for equipment and laboratory setup. As these companies expand, a significant portion of their budgets is also allocated to outsourced services.

Amazon allows small businesses to outsource the substantial upfront costs of operating data centers by renting access rather than purchasing infrastructure. Amazon can absorb these costs itself, serving as a backend laboratory.

This is similar to how companies such as Transcriptic and Emerald operate with cell-based models. Companies like Vium are creating building blocks for mouse models.

AWS for laboratories enables companies to send samples, conduct experiments, and receive both raw and analyzed data (provided by AWS). This allows businesses to utilize equipment only when necessary, particularly during the early stages when capital is limited.

One advantage is that Amazon can establish partnerships with enterprises at an early stage and provide additional services as these companies grow. This represents a market for AWS services, as well as for other outsourced research services similar to Science Exchange. In this way, Amazon can make it easier for small laboratories to operate, identify customers for its services while scaling up, and provide cloud computing services for fields such as biology and chemistry.

AWS enabled many tech companies in their early stages to get off the ground smoothly—if Amazon can help small laboratories launch and grow in the same way, it can capture similar value.

Amazon’s Foray into Healthcare Prompts Incumbents to Reassess Their Core Competencies.

Although Amazon has only made some preliminary attempts, it has the potential to disrupt this sector with its e-commerce expertise. If there is no need to generate profits in the healthcare industry, the high-margin and complex segments of healthcare are highly susceptible to disruption.

Amazon’s strategy allows other companies to outsource parts of their operations that are both chaotic and outside their core business scope. This involves multiple aspects:

• Payer—Amazon can handle claims and marketplaces, allowing companies to focus on delivering their services.

• Suppliers—Amazon can integrate relevant information into electronic health records or coordinate the purchase and transportation of supplies.

• Pharmaceuticals/Biotechnology – Amazon can conduct actual trials, allowing researchers to focus on experimental design and analysis; alternatively, Amazon can handle packaging, tracking, and shipping processes for larger pharmaceutical manufacturers.

Amazon holds a significant advantage in transforming the healthcare sector, as intermediaries in this field are primarily driven by profit motives.

Despite various obstacles, including market leaders, established processes, and buyers’ general concerns about new entrants, Amazon’s foray into the healthcare sector will transform the entire current system or force existing players to become more competitive.