When Hospitals Come Knocking: We Crunched the Numbers on a Multi-Billion-Dollar Opportunity

Recently, VCBeat has been closely focusing on digital innovation within the traditional healthcare sector, including pharmaceutical companies, hospitals, insurers, and even medical regulatory agencies. We have observed that after years of digital health innovation, traditional healthcare institutions are becoming the core driving force behind the second wave of digital health innovation. Hospitals, in particular, serve as the key nodes in this wave of innovation.

Over the past six months, VCBeat has interviewed numerous hospital presidents and department heads, as well as a wide range of IT, cloud computing, and hardware companies driving innovation in the healthcare sector. It also conducted on-site visits to representative innovative hospitals, including Yinchuan First People’s Hospital and Jiande First People’s Hospital. Based on these efforts, VCBeat authored the report “2018 Report on Hospital Informationization Construction: The Leap from Integration Platforms to Big Data Applications.”

Through analysis, we have derived the following key data and conclusions:

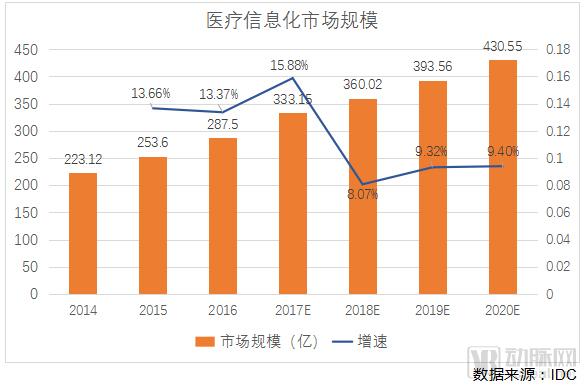

1. According to the “IDC: China Healthcare IT Market Forecast, 2017–2021” report, the total size of China’s healthcare informatization market was RMB 8.746 billion in 2009, grew to RMB 26.879 billion in 2015, and is projected to reach RMB 33.653 billion in 2017, representing a compound annual growth rate (CAGR) of 14.53% during this period.

2. Based on the IT infrastructure investments made by Grade III, Class B county-level hospitals over the past five years, such expenditures accounted for an average of 2.07% of total hospital revenue, with annual investment ranging from RMB 6 million to RMB 12 million. According to data from the China Health and Family Planning Statistical Yearbook 2017, there were a total of 29,140 hospitals in China as of the end of 2016, generating a total revenue of RMB 2,578.43221 billion. By calculating the proportion of IT investment relative to total hospital revenue, it is estimated that the market size for healthcare informatization in China reached RMB 53.3 billion in 2016, exceeding the figures provided by IDC.

3. Existing healthcare informatization can be roughly divided into four stages. Most healthcare institutions have currently passed the first stage and are in the second stage. Hospitals in the second stage account for approximately 75%, while those still remaining in the first stage represent about 10% of the total, indicating a substantial growth potential.

4. It takes one to two years for a hospital’s information system to evolve from initial construction to the establishment of a relatively comprehensive application framework (Stage 2.0). For tertiary hospitals, total software development costs amount to approximately RMB 12–20 million, while hardware infrastructure costs (covering only data center hardware such as servers, storage, and networking equipment, and excluding end-user devices like computers and printers) range from RMB 5–10 million.

5. Informatization Construction in Hospitals at Tertiary Level and AboveThe focus is on clinical systems, while secondary hospitals prioritize comprehensive system upgrades.

6. Infrastructure-focused technology companies, represented by Alibaba Cloud, are gradually penetrating public hospitals beyond top-tier tertiary institutions, establishing new digital footholds within these hospitals and reshaping their digital systems.

7.The most significant change is that hospitals are shifting from a passive to a proactive stance, becoming the initiators of digital innovation. This presents both opportunities and challenges for startups, requiring a deeper understanding of hospital language and needs, with cross-disciplinary talent being key to success.

8. In the future, healthcare informatization will develop towards intelligence, mobility, integration, and regionalization.

During the 2009 healthcare reform, medical informatization became a key pillar of the “four beams and eight columns” framework, sparking a wave of information platform construction centered on electronic medical records (EMR). Hospitals embarked on building EMR-based information platforms and comprehensive digital hospital infrastructures. With EMR at the core, they prioritized the development of clinical information systems (CIS), exemplified by physician workstations supported by clinical pathways. By adopting a new architecture comprising an information center platform plus a data exchange layer, they achieved data interoperability and established in-hospital medical data centers.

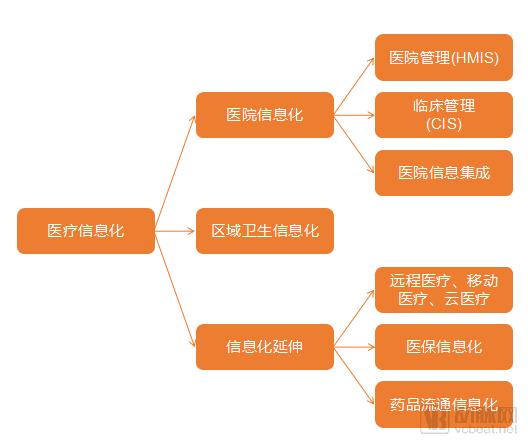

Classification of Healthcare Informatization, Chart by VCBeat.

The figure above illustrates the primary architecture in the field of healthcare informatization. Hospital informatization centers on electronic medical records (EMR), leveraging information technology to achieve data acquisition, processing, storage, transmission, and sharing of both hospital management and clinical information. This enables the digitalization of patient information, medical processes, management workflows, medical services, and information exchange, which constitutes the key focus of this report. In China’s healthcare informatization industry, more than 500 companies are actively involved. A number of listed enterprises have emerged, including Winning Health Technology Group, Wanda Information, Neusoft Corporation, B-Soft, SinoCare, DHC Software, Das Intellitech, Heren Technology, ZHEJIANG MEDIINFO I.T.CO.,LTD, Zhongyuan Share, and Yinjiang Share.

According to the “IDC: China Healthcare IT Market Forecast, 2017–2021” report, the total size of China’s healthcare informatization market was RMB 8.746 billion in 2009, grew to RMB 26.879 billion in 2015, and is projected to reach RMB 33.653 billion in 2017, representing a compound annual growth rate (CAGR) of 14.53% over this period. The market size for clinical informatization solutions in China was approximately RMB 1 billion in 2009, reached RMB 4.5 billion in 2015, and is expected to grow to RMB 5.67 billion in 2017, with a CAGR of 20% during this period.

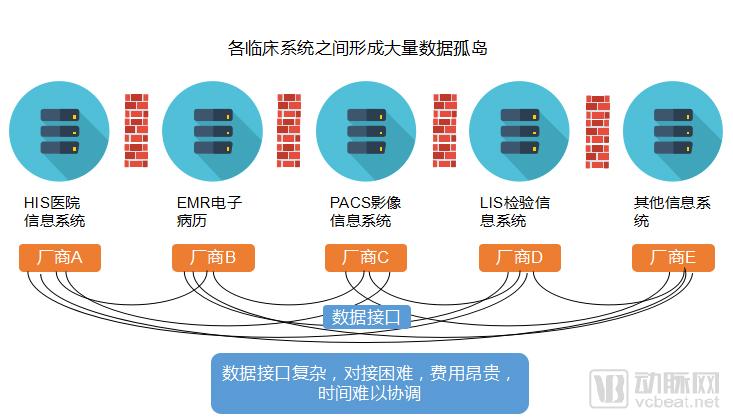

Since the late 20th century, healthcare informatization has been gradually promoted in large medical institutions, with the implementation of hospital-wide information management systems. Cost accounting and health insurance reimbursement served as the primary drivers of this wave of informatization, leading to the development of entry-level information management systems centered on financial management and the establishment of Hospital Information Systems (HIS) based on Client/Server (C/S) architecture. During this phase, hospitals developed their systems independently, resulting in numerous information silos.

In the early 21st century, the focus of healthcare information system development shifted toward clinical care. Clinical information systems, centered around physician workstations, included subsystems such as Laboratory Information Systems (LIS), Picture Archiving and Communication Systems (PACS) for medical image processing, and rational drug use monitoring. In addition to the pre-existing information silos, vertical “stovepipe” systems emerged across various hospital business lines, hindering information interoperability and data exchange.

Classification of Healthcare Informatization, Chart by VCBeat

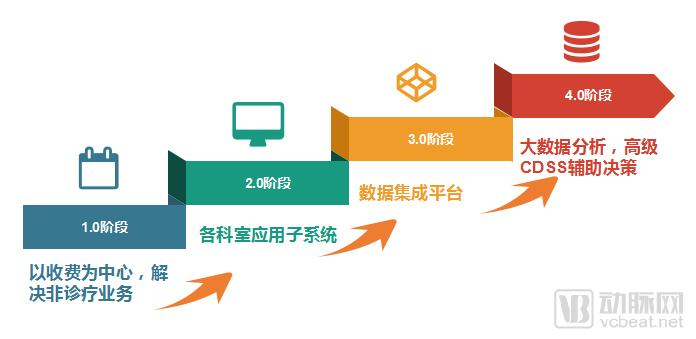

Existing medical informatization can be roughly divided into four stages:

Phase 1.0: Only the Hospital Information System (HIS) addresses the management of non-clinical operations (e.g., registration, billing, and medication dispensing) and internal hospital administration (e.g., payroll management and human resources management).

Phase 2.0: Application of departmental subsystems, including LIS, PACS, Anesthesia Information Management System (AIMS), ICU Information System, etc.

Phase 3.0: Launch of the integrated platform, achieving interoperability among different subsystems to form a comprehensive system.

Phase 4.0: Introduction of big data analytics and advanced clinical decision support systems (CDSS) to assist clinical practice.

Four Stages of Hospital Informatization Development, Chart by VCBeat

The Phase I HIS system primarily supports operational management, including financial management and cost accounting, but does not assist in clinical diagnosis. The construction cost for this phase is relatively low, typically around RMB 2 million, which is affordable for most healthcare institutions.

In the second phase, systems such as the Laboratory Information System (LIS), Picture Archiving and Communication System (PACS), Surgical Anesthesia Information System, and ICU Information System can provide a certain level of support for clinical diagnosis and treatment workflows. This includes organizing diagnostic and therapeutic data to generate illustrated reports, providing medication safety information, and managing surgical scheduling information. The construction cost for this phase typically ranges from RMB 10 million to 20 million. Upon completion, it can basically meet the hospital’s needs for informatization applications. However, interface standards remain chaotic during this stage, as different systems are developed by different vendors, making interoperability between systems challenging.

Amidst the chaos of Phase II, integrated systems emerged in Phase III. IT companies such as SiChuang YiHui, Microsoft, IBM, and ZHEJIANG MEDIINFO I.T.CO.,LTD developed integration platforms to connect disparate medical subsystems, consolidate data from various systems, and establish Clinical Data Repositories (CDR). By this stage, the hospital’s information system had evolved into a comprehensive framework. The construction costs for tertiary hospitals at this stage exceeded RMB 10 million, while those for secondary hospitals amounted to approximately RMB 5 million, with the cost ratio between the integration platform and the clinical data repository being roughly 3:7.

Phase IV builds upon a comprehensive information technology infrastructure by incorporating big data and advanced Clinical Decision Support Systems (CDSS). The CDSS itself costs approximately RMB 1–3 million, enabling hospitals to implement more refined management practices and support clinical diagnosis and treatment.

It takes one to two years for a hospital’s health information system to evolve from initial implementation to a relatively comprehensive application framework (Stage 2.0). For tertiary hospitals, total software development costs amount to approximately RMB 12–20 million, while hardware infrastructure costs (covering only data center facilities such as servers, storage, and networking equipment, excluding end-user devices like computers and printers) range from RMB 5–10 million. For secondary hospitals, software investment is approximately RMB 8–15 million, and hardware investment is around RMB 4–8 million.

Overall, most medical institutions have currently moved past the first stage and are in the second stage. Hospitals in the second stage account for approximately 75%, while those still remaining in the first stage make up about 10% of the total. Hospitals have generally begun to apply information systems to assist in diagnosis and treatment. Currently, the third and fourth stages are progressing nearly simultaneously; during this phase, various systems are integrated and consolidated, and Clinical Decision Support Systems (CDSS) are employed to provide alerts and assistance for clinical diagnosis and treatment. Hospitals at this stage account for approximately 15%. China’s healthcare informatization construction is overall at a relatively low level, the road ahead for development remains long, and the prospects for medical IT are very broad.

According to the data presented in the "Survey Report on the Status of Hospital Informatization in China (2015–2016)" released by the Professional Committee on Information Management of the Chinese Hospital Association (CHIMA), among the 536 hospitals surveyed, 45.9% had formulated comprehensive informatization plans, 38.06% had developed plans that were not comprehensive, 10.45% had only established partial plans, and 0.93% had not formulated any informatization plans. The results indicate that 94.41% of the hospitals had developed either partial or comprehensive informatization development plans. Further analysis by hospital tier reveals that 55.85% of tertiary hospitals had formulated comprehensive informatization plans, compared with 28.35% of hospitals below the tertiary level, demonstrating that tertiary hospitals have a significantly higher demand for informatization than non-tertiary hospitals.

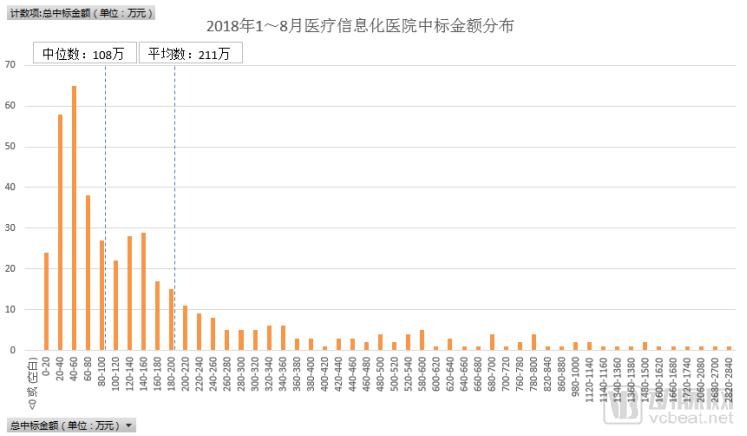

VCBeat’s Eggshell Research Institute collected and analyzed data on winning bids for medical informatics products procured by public hospitals through government open tendering, as published on the China Government Procurement Network from January to August 2018. Although the volume of data available on the Government Procurement Network is significantly lower than that in the China Bidding Network database, its structured format facilitates analysis. Public hospitals at all levels in China are classified as public institutions and are required to strictly comply with laws and regulations such as the Bidding Law and the Government Procurement Law. However, not all hospital information systems are acquired through government procurement; alternative acquisition methods include independent bidding, single-source procurement, and negotiated agreements. Data on government procurement winning bids represent only a small portion of the overall medical informatics market. From January to August 2018, there were 442 winning bids, involving a total procurement amount of RMB 930 million, accounting for approximately 3% of the estimated total market size for medical informatics during the same period. The sample size is sufficiently large to reflect the basic conditions of the medical informatics market.

Data source: Government Procurement and Bidding Network; compiled by VCBeat.

According to sample data statistics, a total of 442 medical informatization procurement projects were recorded from January to August 2018, with a total winning bid amount of RMB 930 million. Among these medical informatization projects, the average winning bid amount was RMB 2.11 million, and the median amount was RMB 1.08 million. The price range with the highest number of projects was RMB 400,000–600,000, while the primary winning bid price range fell between RMB 200,000 and RMB 800,000.

Data source: Government Bidding and Procurement Network, compiled by VCBeat.

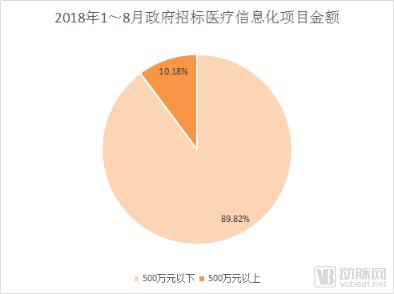

Among the winning bids, it is common for individual hospital informatization tenders to exceed RMB 5 million, with numerous contracts reaching the tens of millions. As of mid-August this year, there were 45 projects valued at over RMB 5 million, accounting for 10.18% of the total number of projects. Thirteen of these were worth tens of millions, primarily involving comprehensive overhauls of overall hospital informatization, or major upgrades of secondary subsystems such as data integration platforms and clinical information systems.

The project with the highest total winning bid amount was the comprehensive overhaul of the main information system at Heilongjiang Provincial Cancer Hospital, jointly awarded to seven companies for a combined total of RMB 28.3892 million. The highest winning bid amount awarded to a single company was RMB 26.98 million, for the comprehensive overhaul of the hospital informatization platform construction at Meizhou City Meixian District Traditional Chinese Medicine Hospital, which was awarded to Landun Information. Both projects involved comprehensive informatization overhauls, accounting for their higher amounts. The project with the lowest winning bid amount was Phase II construction of the HRP (Hospital Resource Planning) economic management system at the Stomatological Hospital of Xi’an Jiaotong University, with a winning bid price of RMB 88,000.

Data source: Government Procurement and Bidding Network; compiled by VCBeat.

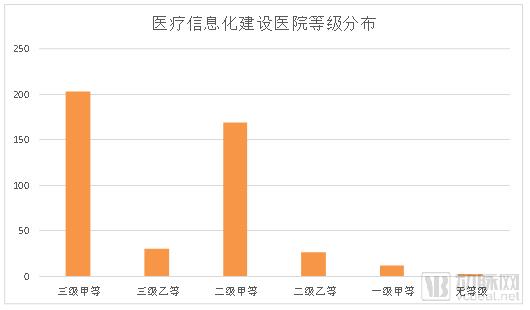

From the perspective of hospital classification, tertiary A-grade hospitals remain the primary drivers of investment and development in healthcare informatization. Due to their heavy clinical workload, the complexity of clinical and hospital management, and their high acceptance of new technologies, these hospitals have an extremely strong demand for informatization solutions. In addition to deploying new information subsystems, tertiary A-grade hospitals, having invested in informatization at an earlier stage, are now beginning to phase out and upgrade certain legacy projects. Secondary A-grade hospitals, predominantly county-level hospitals, are also seeing a growing demand for healthcare informatization transformation, with their needs approaching those of tertiary A-grade hospitals.

How large is the market for healthcare informatization? In a 2016 report, IDC projected that the total market size would reach RMB 33.315 billion in 2017. VCBeat conducted its own analysis using proprietary data models. Data from the “2015–2016 Survey Report on Hospital Informatization in China,” published by CHIMA, indicate that 45.9% of hospitals had formulated comprehensive informatization plans, 38.06% had developed plans that were not fully comprehensive, and 10.45% had only established partial plans. This suggests that more than 90% of hospitals have needs to procure or upgrade their informatization systems.

Estimation of the Scale of Hospital Medical Informatics Investment in 2016

Although we have calculated the market size of healthcare informatization in 2016 to be RMB 53.3 billion, there is still considerable room for growth in this sector. This potential is driven by two main factors: first, policy initiatives are expanding the existing market; second, the increase in the number of medical institutions is contributing incremental market growth.

In the "Notice on Further Promoting the Construction of Information Systems in Medical Institutions Centered on Electronic Medical Records" issued by the Bureau of Medical Administration and Medical Services on August 20, 2018, quantitative requirements were proposed for the construction of electronic medical records (EMR) in hospitals. The Bureau required local health administrative departments at all levels to guide medical institutions within their jurisdictions to strengthen the construction and management of EMR information systems in accordance with the "Specifications for the Application and Management of Electronic Medical Records (Trial)" and the "Functional Specifications for Electronic Medical Record Systems (Trial)." By 2019, all tertiary hospitals within their jurisdictions were required to reach Level 3 or above in the graded evaluation of EMR application, achieving data exchange between different departments within the hospital. By 2020, they were required to reach Level 4 or above, achieving hospital-wide information sharing and possessing clinical decision support capabilities. By 2020, tertiary hospitals were to achieve full coverage of EMR-based informatization in diagnosis and treatment service processes. The clear short-term requirements put forward by health authorities for hospital informatization will also promote market development.

On the other hand, according to the latest data from the "2017 Statistical Bulletin on the Development of Health and Family Planning in China," by the end of 2017, the total number of hospitals in China reached 31,056, an increase of more than 1,000 compared to 2016. These newly added hospitals will also start from scratch in terms of information technology construction, further expanding the market space for medical informatics. Therefore, in 2018, the market size for medical informatics is expected to exceed RMB 60 billion.

Jiande First People’s Hospital (Jiande Hospital) was established in November 1968. Although it is a grassroots county-level hospital with Grade III, Class B accreditation, it places significant emphasis on medical quality management and the development of health information technology. In August 2015, Jiande Hospital passed the international Joint Commission International (JCI) accreditation with high scores, becoming the first hospital in the Hangzhou region to achieve JCI certification. In September 2015, it was designated as one of the first batch of National Stroke Centers in China. In November 2016, it became one of the first batch of Primary Chest Pain Centers in China and the first such center in Zhejiang Province, taking on the responsibility of guiding the construction of chest pain centers in primary hospitals across the province. In September 2017, it became the only county-level hospital in China at that time to successfully pass the international HIMSS Stage 6 certification. In December 2017, it became the first hospital in Zhejiang Province to achieve Level 5 certification in the National Electronic Medical Record Application Level Evaluation.

Jiande First People’s Hospital began its basic information technology infrastructure development in 2000, completing the transition from initial financial billing systems to core functionalities such as laboratory and diagnostic testing and computerized physician order entry (CPOE) over the course of more than a decade. In 2014, in accordance with international HIMSS standards, the hospital upgraded and optimized its hospital-wide information systems, including electronic medical records (EMR), medication management, medical and nursing quality management, logistics, and self-service kiosks. By centering its architecture on EMR, the hospital achieved interoperability and data exchange across its systems, providing robust informational support for clinical operations and effectively safeguarding healthcare quality and patient safety.

The primary objective of a Hospital Information System (HIS) is to support administrative management and transactional operations, reduce the workload of administrative staff, assist in hospital management and executive decision-making, and improve operational efficiency. This enables hospitals to achieve greater social and economic benefits with minimal investment. Furthermore, the system supports clinical activities by collecting and processing patients’ clinical medical information, enriching and accumulating clinical medical knowledge, and providing clinical consultation, diagnostic assistance, and clinical decision support. These capabilities enhance the efficiency of medical personnel and deliver more comprehensive, timely, and higher-quality services to patients.

The informatization development of Jiande First People's Hospital has undergone three stages:

The first phase was the construction of Hospital Information Systems (HIS) centered on financial billing, spanning from 1999 to 2005. At that time, computers were just beginning to gain widespread adoption across various industries, and advancements in computer and communication technologies had a significant impact on the healthcare sector. Prior to the implementation of computerized information management systems, hospital fee settlement processes were entirely manual, which not only increased the workload of medical staff but also resulted in a substantial volume of work for auditing itemized bills, leading to high error rates. The HIS system represents the initial step in the informatization journey for most hospitals. It is a vast and complex information management system designed to establish a finance-centric informational infrastructure to address billing issues. This system can significantly reduce the workload of hospital financial and health insurance administrators and markedly lower error rates.

From the perspective of its core functions, the primary purpose of Hospital Information Systems (HIS) is computerization, focusing mainly on financial and operational management. These systems leverage network communications to transmit data, and by collecting, storing, processing, transmitting, aggregating, and analyzing various types of hospital-generated data, they enable comprehensive management of patient flow, material flow, and financial flow. Therefore, in terms of functionality, HIS systems during the early stages of health informatization were very rudimentary.

The second phase of Jian De Hospital’s informatization construction, spanning from 2005 to 2012, was centered on patients and guided by clinical practices. During this phase, the hospital adopted a patient-centered approach, driven by departmental application needs, shifting away from the previous management philosophy that prioritized economic accounting. Instead, it focused on enhancing the quality of patient care, strengthening medical quality management, streamlining diagnosis and treatment processes, reducing patient waiting times and length of stay, and improving the utilization efficiency of medical resources.

During this period, with the advancement of information technology, various hospital business lines have been equipped with corresponding information systems. The application of subsystems such as LIS, PACS, RIS, and CPOE has gradually matured, marking the initial scale of hospital informatization. However, hospital informatization at this stage was primarily achieved by procuring and stacking various products. These systems generally operated as internal silos; originating from different vendors, they featured disparate software architectures, widely varying data structures, and inconsistent communication protocols. The lack of interoperability among these systems hindered data sharing and exchange.

The third stage of informatization development is centered on electronic medical records (EMR), primarily aiming to achieve the interconnectivity and integration of medical data. This patient-centric phase focuses on EMR-based informatization, leveraging data integration as a means and data management and application as goals to enhance hospital management standards and operational efficiency, thereby building an advanced, comprehensive, and modern digital hospital.

Jiande Hospital’s journey in building its health information technology (HIT) products initially mirrored that of other hospitals. However, as it advanced into the second phase, Jiande Hospital identified increasingly severe issues with the traditional approach of procuring disparate products to construct a hospital-wide HIT system. Consequently, the hospital began to revamp its Hospital Information System (HIS) and establish an electronic medical record (EMR)-centric HIT infrastructure.

Compared with other hospitals, Jiande Hospital’s informatization development has involved more than just procurement; it has collaborated with multiple medical informatics vendors to co-develop products since their early stages.For instance, the MediInfo Integration Platform, Huimei Technology’s Clinical Intelligent Decision Support System, Alibaba Cloud’s Data Middle Platform, and Alibaba’s Medical Record Quality Control System were all first piloted at Jiande Hospital, where they underwent iterative upgrades. By participating in the design phase of these informatization products, Jiande Hospital was able to fully integrate healthcare IT requirements into product development, thereby enabling effective mining and application of medical data. This further enhanced the hospital’s level of intelligent management, establishing it as a benchmark for informatization construction among county-level hospitals.

The above content is an excerpt from “The Leap from Integration Platforms to Big Data Applications—2018 Hospital Informatics Construction Report.” The full report comprises approximately 32,000 words and was originally priced at RMB 499. During the World Medical Technology Forum hosted by VCBeat (September 26–28), this report will be available free of charge for a limited period of three days!

How to Get It for Free: Long-press the QR code below to scan it, or follow the VCBeat WeChat Official Account (vcbeat) and reply with the keyword “Hospital Informatization” to read the full report for free!