Who Will Win the Trillion-Yuan Prescription Diversion Market: Retail Pharmacies, DTP Pharmacies, E-Pharmacies, or Hospital-Adjacent Stores?

Prescription outflow and the resulting hundred-billion-yuan market are currently the focus of widespread attention.

In discussions with industry professionals, VCBeat (WeChat: vcbeat) has observed that stakeholders are making various projections about the vast market opportunities created by the outflow of prescription drugs, while actively positioning themselves and strategizing their market presence.

What everyone is particularly concerned about is: In the new market landscape, what are the respective advantages and disadvantages of retail pharmacies, DTP (Direct-to-Patient) pharmacies, pharmaceutical e-commerce platforms, and hospital-adjacent pharmacies, and who will emerge as the biggest winner?

In response, VCBeat proposes to conduct an analysis across five dimensions—including prescription acquisition, pharmaceutical supply assurance capabilities, and medical insurance support—based on extensive investigation and research.

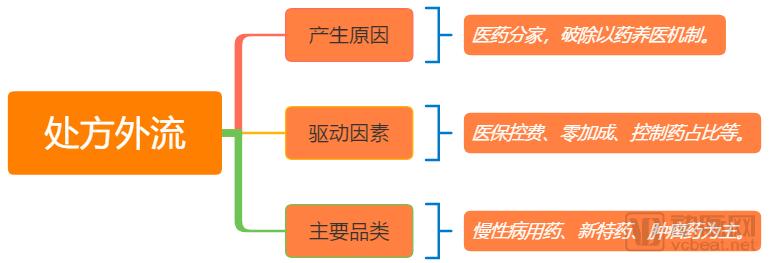

Prescription outflow refers to the external circulation of prescriptions. Previously, patients completed consultations, received prescriptions, and obtained medications all within hospitals. Now, with restrictions on the free flow of prescriptions lifted, medications are provided by community pharmacies, thereby separating medical consultations from drug dispensing.

The emergence of prescription outflow is driven by the dismantling of the “drug-revenue-dependent healthcare” mechanism, aiming to refocus hospitals on their core medical functions and weaken their “monopoly” over prescriptions. Policies such as health insurance cost containment, zero mark-up on drugs, and controls on the proportion of drug expenditures serve as the primary incentives for hospitals to release certain prescriptions. Thus, prescription outflow represents both a “political mandate” and an outcome of “market-based adjustment.”

Prescriptions for medications used in chronic disease management, new and specialized drugs, and oncology agents will be among the “first batch” to be dispensed outside hospitals. This move will not only provide convenience for patients, particularly those with chronic conditions, but also help control the proportion of pharmaceutical revenue in hospital income and alleviate operational pressures on hospital pharmacies.

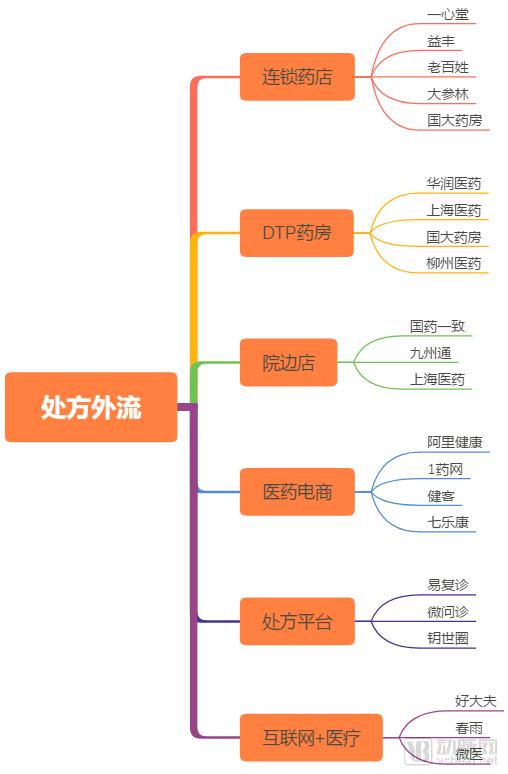

The outflow of prescriptions will drive structural adjustments in pharmaceutical distribution channels, representing both a reallocation of existing market share and a new growth engine for the industry. Consequently, retail pharmacy chains, DTP (Direct-to-Patient) pharmacies, hospital-adjacent stores, pharmaceutical e-commerce platforms, and “Internet + Healthcare” enterprises are targeting this opportunity and actively strategizing their market presence.

Prescription Outflow Fulfillment Models and Key Players

Chain Pharmacies Are the Most Promising

Currently, the primary policy direction for guiding prescription outflow is toward retail pharmacies. For instance, the 2016 "Healthcare Reform" task list explicitly prohibited hospitals from restricting prescription outflow, allowing patients to freely choose between purchasing medications at hospital outpatient pharmacies or at retail pharmacies with a valid prescription.

The 2017 “Healthcare Reform” Task List indicated that a tiered management system for retail pharmacies would be piloted, the development of chain pharmacies would be encouraged, and interoperability and real-time sharing of prescription information from medical institutions, health insurance settlement data, and pharmaceutical retail consumption data would be explored. This signifies that policies have provided clearer direction on how pharmacies can accommodate the outflow of prescriptions, offering support to retail pharmacies in terms of prescription sources and health insurance payment mechanisms.

Recognizing the positive policy trends, listed industry leaders such as Yixintang, Yifeng Pharmacy, Laobaixing Pharmacy, Dashenlin Pharmaceutical Group, and Guoda Drugstore are actively positioning themselves to capture outpatient prescription outflows by emphasizing the enhancement of professional service capabilities.

As Laobaixing stated in the Board of Directors’ Management Discussion and Analysis, the company has actively promoted professional service initiatives in recent years, including chronic disease lifestyle centers, WeDoctor online consultations, customer-facing mobile apps, medication counseling via WeChat service accounts, and disease management programs. It has increased the staffing of licensed pharmacists at retail outlets, utilized an employee app to train store staff on symptom assessment and associated medication recommendations, and deployed automated kiosks to enhance employees’ professional capabilities in disease and pharmaceutical knowledge. These measures are designed to prepare for the outflow of prescriptions from hospitals.

Other leading listed pharmaceutical retail chains have adopted expansion strategies similar to those of Laobaixing, starting with enhancing professional service capabilities, strengthening member management and operations, and particularly increasing their focus on patients with chronic diseases and chronic disease medications.

DTP Pharmacies Show the Fastest Growth

DTP (Direct to Patient) pharmacies, which originated in the United States, represent a specialized pharmaceutical sales model. Under this model, pharmaceutical manufacturers directly authorize pharmacies to distribute their products, enabling patients to purchase medications directly from these pharmacies using prescriptions issued by physicians.

DTP pharmacies are characterized by a “dual-high” profile: first, a high proportion of prescription drug sales, exceeding 90%, with virtually no over-the-counter (OTC) medications sold; second, a high degree of brand concentration, with top-selling products predominantly being oncology drugs from major pharmaceutical manufacturers, such as Herceptin, Conmana, Humira, Gleevec, Tagrisso, and Nexavar. Furthermore, most of these medications are included in the national or local medical insurance formularies; in other words, medical insurance coverage is also a significant factor influencing DTP pharmacies.

The core product portfolio of DTP (Direct-to-Patient) pharmacies consists of novel and specialty drugs for conditions such as cancer and autoimmune diseases, as well as medications for chronic diseases requiring long-term use. From the perspective of drug supply, the availability of novel and specialty drugs is set to increase as China implements policies such as zero tariffs on anticancer drugs and prioritized review and approval for innovative medicines. Furthermore, there is a time lag between market approval and inclusion in the National Reimbursement Drug List (NRDL), during which DTP pharmacies will serve as a critical channel. Even after drugs are included in the NRDL, DTP pharmacies can maintain their channel advantage through medical insurance reimbursement mechanisms.

Currently, there are roughly four types of players laying out DTP (Direct-to-Patient) pharmacies, including pharmaceutical manufacturers, distributors, retailers, and “Internet + Healthcare” enterprises. Notable large-scale players include China Resources Pharmaceutical, Sinopharm, Shanghai Pharmaceuticals, and Liuzhou Pharma. For instance, China Resources Pharmaceutical operates 88 DTP pharmacies covering more than 50 cities across China. Following its acquisition of Cardinal Health’s China business, Shanghai Pharmaceuticals also boasts over 70 DTP pharmacies.

Overview of Major DTP Pharmacy Institutions in China

According to calculations by VCBeat based on annual reports of listed companies and public data, the market size of DTP (Direct-to-Patient) pharmacies in China was approximately RMB 13 billion in 2017. The growth rate of DTP pharmacies exceeded that of the overall pharmaceutical retail market, and the market size is projected to reach around RMB 19 billion by 2020.

Hospital-Adjacent Pharmacies: Proximity Breeds Priority

Strictly speaking, “hospital-adjacent pharmacies” do not constitute a distinct business model, but rather describe a specific operational characteristic. Nevertheless, given that numerous industry players emphasize this factor when accommodating the outflow of prescriptions from hospitals, it merits dedicated analysis.

As the name suggests, “hospital-adjacent pharmacies” are drugstores located next to hospitals. After receiving medical care and obtaining a prescription, patients can conveniently stop by these pharmacies on their way out of the hospital to purchase their medications.

Upon closer examination, the “hospital-adjacent pharmacy” model is far from simple. First, these pharmacies benefit from prime locations, resulting in higher layout and operational costs compared to pharmacies in general areas. Second, when capturing prescriptions flowing out of hospitals, factors such as prescription sources and the capacity to ensure drug supply must be taken into account. Particularly given that entry costs are already higher than those of ordinary pharmacies, what grounds exist for confidence in cost recovery and sustained profitability?

Through observations of major hospital-adjacent pharmacies, we found that many such pharmacies are operated by pharmaceutical distribution companies. For example, Sinopharm Accord and Shanghai Pharmaceuticals: As of the end of 2017, Guoda Drugstore, a subsidiary of Sinopharm Accord, had a total of 253 hospital-adjacent stores, with 53 newly added during the year (among which 28 were designated for medical insurance reimbursement), and 16 of these stores had achieved cumulative profitability. By the end of 2017, Shanghai Pharmaceuticals operated 54 hospital-adjacent pharmacies, adding 14 new ones. Meanwhile, Jointown Pharmaceutical Group also collaborated with Buchang Pharma to establish Jiubu Pharmacy, with one of its business focuses being hospital-adjacent pharmacy operations.

In this light, hospital-adjacent pharmacies are not merely benefiting from their proximity to healthcare facilities; rather, they represent traditional pharmaceutical distribution companies’ adaptation to the trend of prescription outflow. Leveraging extensive product portfolios and strong ties with hospitals, these companies have transformed their B2B distribution operations into B2C sales businesses, thereby achieving a structural adjustment in revenue streams.

An industry veteran told VCBeat that pharmaceutical distributors have additional advantages in establishing pharmacies adjacent to hospitals. First, although the separation of prescribing and dispensing has been implemented, it remains difficult to completely sever financial ties in the short term; distributors maintain diverse interactions with medical institutions and physicians, facilitating the handling of various fees. Second, distributors already possess established distribution networks (“points”), offering greater pricing flexibility and stronger bargaining power and capacity to offer concessions.

It is expected that the potential of the hospital-adjacent pharmacy model, led by pharmaceutical distributors, will be further tapped in the future. Distributors represented by Sinopharm, China Resources Pharmaceutical, Shanghai Pharmaceuticals, and Jointown Pharmaceutical Group will actively expand into this area and explore greater integration with pharmaceutical and medical device distribution businesses.

Pharma E-Commerce Ventures into “Medicine + Healthcare” to Build a Closed-Loop Service

Pharmaceutical e-commerce has been the fastest-growing segment within the pharmaceutical retail industry in recent years. After several years of rapid development, the market landscape has gradually become clear, with a tier of leading enterprises emerging. A number of companies with strong capabilities, abundant resources, and deep market understanding have established their brands and secured corresponding market shares. However, the pharmaceutical e-commerce market remains subject to many variables, including policy changes, technological innovation, and business model innovation.

First, from a policy perspective, the online sale of prescription drugs has remained restricted, forcing e-commerce platforms to navigate this space tentatively. Once clear regulatory boundaries are established, many companies’ operations will be significantly impacted. Even though the recently issued “Internet + Healthcare” policy has eased certain regulatory constraints, it has not crossed the red line of strict oversight. The policy continues to encourage models that have an offline foundation and can establish robust connections with hospitals.

In terms of medication safety, online sales of prescription drugs will remain restricted for the foreseeable future, creating a ceiling for the expansion of pharmaceutical e-commerce businesses and constraining industry growth.

Secondly, from the perspective of technological innovation, the core competencies of e-commerce lie in enhancing supply chain efficiency, acquiring traffic, and serving a larger user base at lower costs. These elements are constantly evolving, with technological upgrades following a spiral upward trajectory.

To capitalize on the outflow of prescriptions from hospitals, we are also observing pharmaceutical e-commerce platforms innovating their business models. For instance, some are adopting a “pharmacy + healthcare” model by collaborating with internet hospitals, acquiring hospitals, or launching mobile health applications. This approach addresses the source of prescriptions for pharmaceutical e-commerce while enhancing user stickiness and securing a loyal customer base. Others are creating closed-loop business ecosystems by integrating multiple operational formats, including B2B, B2C, and O2O. Additionally, some players are expanding into niche markets, deepening their service offerings, and exploring synergies with insurance and health management services.

In summary, pharmaceutical e-commerce platforms and online pharmacies were previously “absent” from the prescription drug market, due not only to regulatory red lines but also to factors related to consumer channels and behavior. As internet hospitals and remote diagnosis and treatment models gain recognition, the “pharmaceuticals + healthcare” model adopted by pharmaceutical e-commerce will become mainstream. This approach not only prepares for the outflow of prescriptions from hospitals but also serves as a key strategy for the compliant sale of prescription drugs and for capturing incremental market growth.

Supported by Prescription Platforms and Internet Hospitals

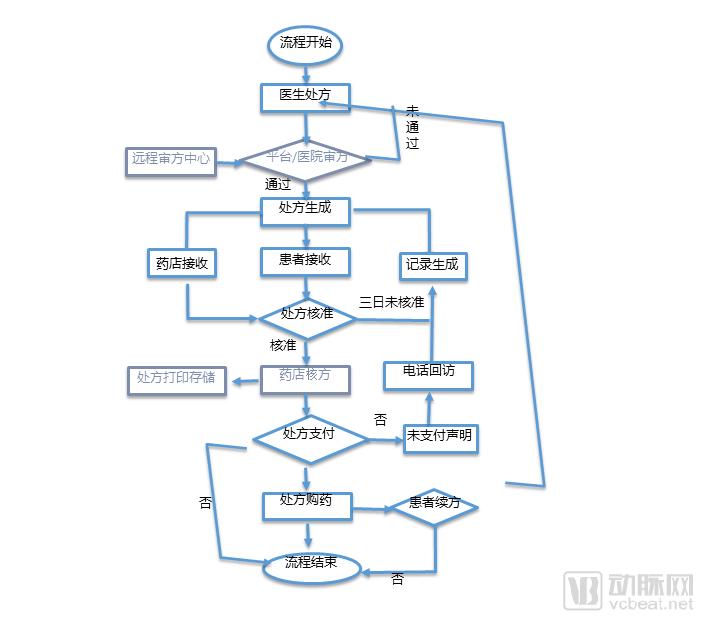

The other two key players facilitating prescription outflow are prescription-sharing platforms and internet healthcare companies, which provide the necessary infrastructure for this process. Prescription-sharing platforms refer to information systems established between hospitals and pharmaceutical retail institutions, such as pharmacies, to connect and enable the sharing of prescriptions. Internet hospitals primarily supply online physician resources to retail pharmacies, e-commerce platforms, and O2O (online-to-offline) enterprises, while also providing electronic prescription services.

The prescription sharing platform operates by integrating with hospital systems to share prescriptions after patients complete their consultations. Prescription information is synchronized to patients and pharmacies via mobile apps, WeChat, and web portals, allowing patients to choose whether to fill their prescriptions at in-hospital or external pharmacies.

Process of a Prescription-Sharing Platform

The core objective of prescription-sharing platforms is to ensure the authenticity, compliance, and validity of prescription information, thereby eliminating issues such as fraudulent prescriptions and the repeated dispensing of medications based on a single prescription. Some companies have integrated blockchain technology into these platforms, leveraging its decentralized, traceable, and tamper-proof features to guarantee the compliant circulation of prescriptions.

Internet hospitals provide services online, limited to follow-up visits for common and chronic diseases, and issue electronic prescriptions as proof for purchasing medications. These electronic prescriptions can be shared with pharmaceutical e-commerce platforms, pharmaceutical O2O services, and retail pharmacies.

For instance, building on the Wuzhen Internet Hospital, WeDoctor has established its “WeDoctor Pharma” segment, which encompasses integrated pharmacy-clinic services and prescription sharing. This initiative scales up connectivity among hospital information systems, retail pharmacy drug distribution and logistics systems, and medical insurance settlement systems, thereby enabling multi-party information sharing and application across healthcare providers, medical insurance payers, and pharmaceutical suppliers.

In March 2016, WeDoctor launched the “Internet Hospital + Pharmacy Cooperation Program.” Partner pharmacies can provide members with services such as precise appointment scheduling, remote consultations, and electronic prescriptions by logging into the Wuzhen Internet Hospital Pharmacy System, thereby directly upgrading to virtual clinics. Currently, the WeDoctor Medical-Pharmacy Platform has integrated more than 20,000 pharmacies, serving nearly 50,000 patients on a daily basis.

Prescription-sharing platforms and electronic prescription sharing via internet hospitals serve as auxiliary support for the industry to accommodate the outflow of prescriptions. As system builders and resource connectors, they hold significant future potential.

Since the launch of healthcare reform, “separating pharmaceuticals from medical services” has been a key component. The underlying reason is that a significant portion of the revenue for public medical institutions and their staff in China has historically come from pharmaceutical sales, which were used to offset the artificially low pricing of medical services. The practice of “funding healthcare through drug sales” has been characterized by opaque funding sources, non-transparent distribution, and inadequate regulatory oversight, thereby fostering issues such as pharmaceutical bribery, overprescription, and elevated healthcare expenditures.

“The separation of pharmaceuticals from medical services” aims to decouple drug revenues from the income of healthcare institutions, weaken the direct financial ties among drug bidding and procurement processes, healthcare institutions, medical personnel, pharmaceutical companies, and drug distributors, and establish a mechanism in which clinical diagnosis and treatment operate independently from medication prescribing.

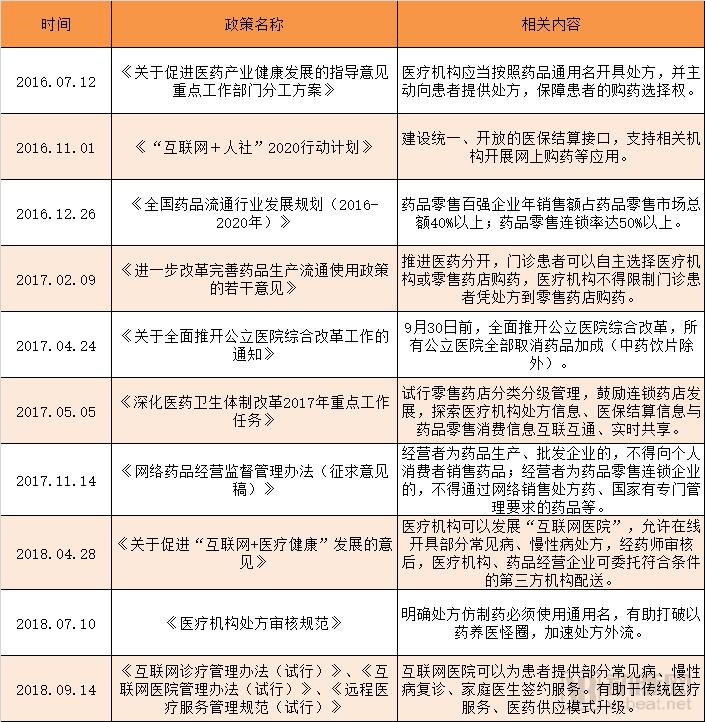

In terms of policy, the origins can be traced back to the “Guiding Opinions on Reform of the Urban Medical and Health System” issued by the State Council’s Office for Healthcare Reform in 2000. This document first stipulated that pharmaceuticals and medical services should be “accounted for separately, managed independently, with revenues remitted centrally and reasonably returned.” Over the subsequent decade-plus, the phrase “eliminating the mechanism of subsidizing healthcare with drug profits” has been repeatedly emphasized. Policies such as controlling the proportion of drug costs, implementing zero markups on drugs, and promoting prescription sharing have been progressively introduced, making the separation of pharmaceuticals from medical services an irreversible trend.

Recent Policies on the "Separation of Prescribing and Dispensing"

The development of “Internet + Healthcare” has provided new approaches to healthcare reform. By leveraging telemedicine and remote diagnosis, high-quality medical resources can be extended to grassroots levels, while the guarantee of drug supply is also under planning.

In April this year, the General Office of the State Council issued the "Opinions on Promoting the Development of 'Internet + Medical Health'," pointing out that medical institutions can develop "Internet hospitals," allowing online prescriptions for some common and chronic diseases. After review by pharmacists, medical institutions and drug operation enterprises may entrust qualified third-party institutions to deliver the medications.

In early July, the National Health Commission, the National Administration of Traditional Chinese Medicine, and the Logistics Support Department of the Central Military Commission jointly issued the “Specifications for Prescription Review in Medical Institutions,” which explicitly requires that generic drugs in prescriptions be designated by their generic names. This measure helps break the vicious cycle of hospitals relying on drug sales for revenue and accelerates the outflow of prescriptions from hospitals.

Mandating the use of generic names for prescribed generic drugs will accelerate the de-branding of off-patent originator drugs and generics, particularly following the widespread implementation of consistency evaluations. Coupled with regulations that establish generic names as the basis for medical insurance payment standards, healthcare institutions will curtail the practice of prescribing excessive volumes, and physicians’ discretion in selecting generic drug manufacturers will diminish. These factors collectively contribute to accelerating the outflow of prescriptions from hospitals.

This September, the implementation rules for measures such as the “Administrative Measures for Internet-based Diagnosis and Treatment” and the “Administrative Measures for Internet Hospitals” took effect, making “Internet + Healthcare” a key driver in upgrading traditional medical and pharmaceutical models.

In summary, policies such as medical insurance cost containment, the zero-markup policy for drugs in public hospitals, and restrictions on the drug-to-revenue ratio have become significant drivers of prescription outflow. Medications for chronic diseases and antineoplastic agents will constitute the mainstay of this trend.

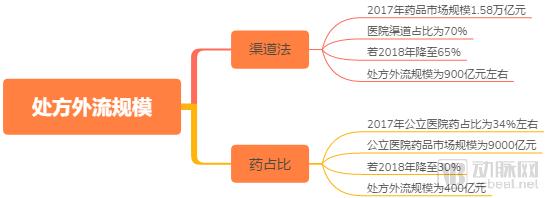

Prescription outflow does not constitute a fully quantifiable market; therefore, it is difficult to obtain precise measurements of the scale of this model. Regarding the estimation of the prescription outflow market size, there are generally two approaches: one is the channel-based method, which roughly estimates the scale of prescription outflow based on the proportion of out-of-hospital channels; the other is the drug expenditure ratio method, as the primary source of outflowing prescriptions is hospitals, which affects the hospital drug expenditure ratio. Changes in this ratio can also be used to estimate the industry’s scale.

Estimation of the Scale of Prescription Outflow

Based on the above calculations, the scale of prescription outflow in 2018 was between RMB 40 billion and RMB 90 billion. However, due to the difficulty in standardizing prescription outflow, this is only a rough estimate and may deviate somewhat from actual conditions. Furthermore, influenced by factors such as tiered diagnosis and treatment and the deregulation of medication at primary care levels, patients from public tertiary hospitals may be diverted to primary care institutions, which will also become important recipients of outflowing prescriptions.

We scored the current major models for handling outbound prescriptions across dimensions such as prescription acquisition capability, drug portfolio availability, pharmaceutical care service capability, cost investment, and profitability, resulting in the table below:

Analysis of the Primary Models for Handling Outflowing Prescriptions

Under the trend of prescription outflow, new specialty drugs and long-term medications for chronic diseases will be the first to move out of medical institutions. Retail pharmacies located near hospitals and Direct-to-Patient (DTP) pharmacies, with their strong backgrounds and solid foundations, will become the biggest beneficiaries of this shift. Meanwhile, chain pharmacies, pharmaceutical e-commerce platforms, and prescription sharing platforms each have their own strengths and also enjoy promising development opportunities.

Prescription outflow is a systemic phenomenon involving healthcare reform, adjustments in pharmaceutical distribution and retail channels, shifts in business structures, changes in medical insurance policies, transformations in healthcare delivery models, and evolving patient preferences. This process will entail a complex and winding path of exploration.

In practice, the "separation of pharmaceuticals from medical services" also faces numerous challenges. The most apparent issue is that after drug revenue is stripped away from medical institutions, the compensation received by healthcare professionals no longer aligns with their labor input, due to a lack of adequate benefit-compensation mechanisms.

Another issue is the acceptance of outpatient prescriptions. The pharmaceutical distribution channel has long been dominated by public medical institutions, while community pharmacies still lag behind in terms of drug supply assurance and pharmaceutical care capabilities. Therefore, efforts should be made to enhance prescription acquisition, product portfolio management, and pharmaceutical care services, ensuring that outpatient prescriptions can be effectively diverted from hospitals and properly handled by retail pharmacies. This approach aligns with healthcare reform initiatives and better serves patients.